Shift4 SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Shift4’s SWOT snapshot highlights robust merchant solutions and recurring revenue but also competitive pressures and regulatory exposure; uncover the strategic levers and financial context behind these points in the full SWOT report. Purchase the complete analysis for a professionally written, editable Word report plus an Excel matrix—ideal for investors, advisors, and strategists who need research-backed insights to plan, pitch, or invest with confidence.

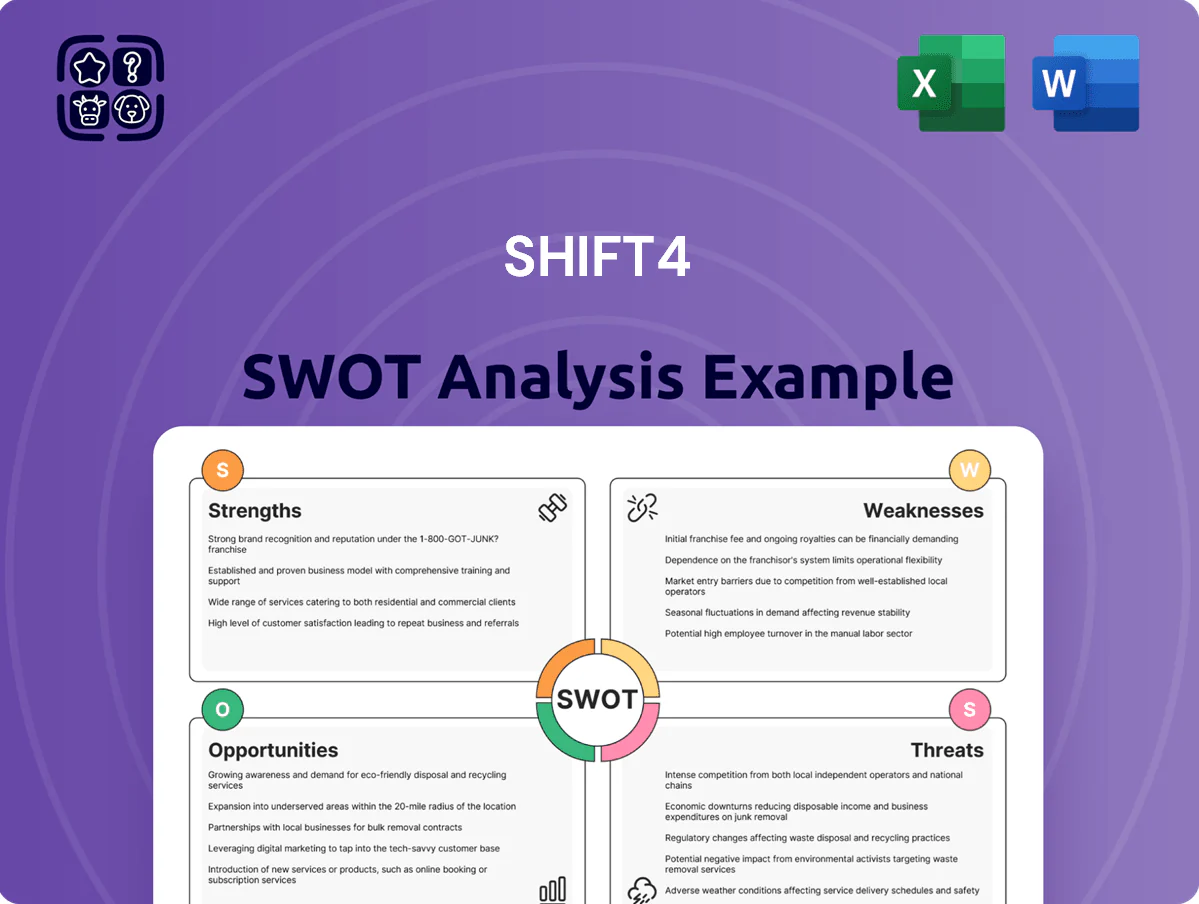

Strengths

Proprietary Integrated Technology Stack

Shift4’s proprietary SkyTab and Lighthouse platforms create an end-to-end payments stack, processing ~1.8 billion transactions and $US115 billion TPV in 2024, cutting third-party middleware and boosting gross margins (2024 adjusted gross margin ~57%).

Owning the full transaction flow improves data control and uptime—Shift4 reports 99.99% payment availability in 2024—enabling richer features for complex merchants and higher take-rates versus gateway-only providers.

Dominant Position in High-Volume Verticals

Shift4 holds a leading share in hospitality, stadium and gaming payments, processing an estimated $30B+ in annual volume across those verticals in 2024, driving outsized fee revenue and lower churn.

These verticals require deep integrations with legacy property-management and point-of-sale systems; Shift4’s certified integrations cut implementation time and error rates, creating a durable moat versus generic processors.

Strong Founder-Led Visionary Leadership

High Recurring Revenue and Low Churn

Shift4’s integrated payments plus POS and back-office tools create high customer stickiness; in 2024 the company reported net retention above 100% and subscription revenue up ~22% year-over-year, keeping ARR predictable.

Most merchants use multiple modules, so estimated switching costs (integration, retraining, downtime) exceed months of fees, helping churn stay below industry median of ~6% annually.

- Net retention >100% (2024)

- Subscription rev +22% YoY (2024)

- Churn < industry median ~6% annually

Successful Strategic Acquisition Execution

Shift4 has completed over 20 acquisitions since 2014, integrating payments and software assets to lift annual recurring revenue (ARR) and enter 7 new countries by 2024, while keeping net promoter score stable.

The firm targets undervalued POS and gateway tech, scaling them through its API platform; gross margin on acquired units rose ~6 percentage points in first 12 months in recent deals.

Shift4: $115B TPV, 1.8B txns, 57% gross margin—>100% retention & +22% subscription growth

Shift4 runs an end-to-end payments+POS stack processing ~1.8B txns and $115B TPV in 2024, with adjusted gross margin ~57% and 99.99% uptime, driving higher take-rates and net retention >100% (2024) plus subscription rev +22% YoY and churn below ~6%.

| Metric | 2024 |

|---|---|

| Transactions | ~1.8B |

| TPV | $115B |

| Adj. gross margin | ~57% |

| Uptime | 99.99% |

| Net retention | >100% |

| Subscription rev YoY | +22% |

| Churn | <6% est. |

What is included in the product

Provides a concise SWOT overview of Shift4, outlining its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise Shift4 SWOT summary for quick strategic alignment and executive snapshot readiness.

Weaknesses

Sector Concentration Risks

Substantial Long-Term Debt Obligations

Shift4’s aggressive M&A push has left long-term debt near $1.6 billion as of FY2024, raising leverage; net debt to EBITDA was about 3.8x in Q4 2024, above peer medians. Current EBITDA and cash flow cover interest, but high leverage reduces flexibility if credit tightens or rates rise. Lowering the debt-to-equity ratio is essential to secure cheaper capital and sustain growth.

Integration Complexity of Legacy Systems

Shift4’s strength in integrations comes with high maintenance costs: supporting hundreds of legacy POS and ERP variants drove tech spend up 18% in 2024 vs 2023, per company disclosures, and raised per-merchant support costs by an estimated $12–18 annually. Each bespoke integration needs ongoing patches and testing, straining engineering capacity and slowing feature rollouts across the merchant base by weeks to months.

Geographic Concentration in North America

Shift4 still earns about 82% of net revenue from North America as of FY2024, leaving it exposed to U.S. rule changes and a 2023–24 regional downturn that cut hospitality transactions by ~7% year-over-year.

International expansion into Europe and Asia is vital to diversify risk but requires navigating PSD2-style regulations, local acquiring rules, and cultural payment preferences, raising expansion costs and extending payback beyond 3–5 years.

- ~82% FY2024 revenue North America

- Hospitality transactions down ~7% in 2023–24

- 3–5+ year payback for EU/Asia entry

- Regulatory hurdles: PSD2, local acquiring, data residency

Dependence on Third-Party Hardware Partners

Shift4 depends on multiple third-party hardware makers for POS terminals; in 2024 about 35% of merchants used non-proprietary devices, exposing Shift4 to suppliers’ quality or supply-chain issues that can delay deployments and hit revenue.

Supply disruptions in 2021–23 raised device lead times by ~40%, and a similar hiccup could dent transaction volume and reputation; building proprietary hardware would cut dependence but needs large CapEx—likely $50–150M upfront.

What this hides: hardware R&D and certification take 12–24 months, and slower merchant rollouts raise churn risk.

- 35% merchants on third-party devices (2024)

- Supply lead times rose ~40% (2021–23)

- Estimated proprietary CapEx $50–150M

- R&D/certification 12–24 months

Shift4 risks: hospitality/NA concentration, high debt, rising tech costs, long EU/Asia payback

| Metric | Value (2024) |

|---|---|

| Hospitality revenue | 40–50% |

| North America | ~82% |

| Net debt | ~$1.6B |

| Net debt/EBITDA | ~3.8x |

| Tech spend growth | +18% |

| Third-party devices | 35% |

| EU/Asia payback | 3–5+ yrs |

What You See Is What You Get

Shift4 SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real, editable analysis that becomes available after checkout. Buy now to unlock the complete, structured report ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Shift4’s SWOT snapshot highlights robust merchant solutions and recurring revenue but also competitive pressures and regulatory exposure; uncover the strategic levers and financial context behind these points in the full SWOT report. Purchase the complete analysis for a professionally written, editable Word report plus an Excel matrix—ideal for investors, advisors, and strategists who need research-backed insights to plan, pitch, or invest with confidence.

Strengths

Proprietary Integrated Technology Stack

Shift4’s proprietary SkyTab and Lighthouse platforms create an end-to-end payments stack, processing ~1.8 billion transactions and $US115 billion TPV in 2024, cutting third-party middleware and boosting gross margins (2024 adjusted gross margin ~57%).

Owning the full transaction flow improves data control and uptime—Shift4 reports 99.99% payment availability in 2024—enabling richer features for complex merchants and higher take-rates versus gateway-only providers.

Dominant Position in High-Volume Verticals

Shift4 holds a leading share in hospitality, stadium and gaming payments, processing an estimated $30B+ in annual volume across those verticals in 2024, driving outsized fee revenue and lower churn.

These verticals require deep integrations with legacy property-management and point-of-sale systems; Shift4’s certified integrations cut implementation time and error rates, creating a durable moat versus generic processors.

Strong Founder-Led Visionary Leadership

High Recurring Revenue and Low Churn

Shift4’s integrated payments plus POS and back-office tools create high customer stickiness; in 2024 the company reported net retention above 100% and subscription revenue up ~22% year-over-year, keeping ARR predictable.

Most merchants use multiple modules, so estimated switching costs (integration, retraining, downtime) exceed months of fees, helping churn stay below industry median of ~6% annually.

- Net retention >100% (2024)

- Subscription rev +22% YoY (2024)

- Churn < industry median ~6% annually

Successful Strategic Acquisition Execution

Shift4 has completed over 20 acquisitions since 2014, integrating payments and software assets to lift annual recurring revenue (ARR) and enter 7 new countries by 2024, while keeping net promoter score stable.

The firm targets undervalued POS and gateway tech, scaling them through its API platform; gross margin on acquired units rose ~6 percentage points in first 12 months in recent deals.

Shift4: $115B TPV, 1.8B txns, 57% gross margin—>100% retention & +22% subscription growth

Shift4 runs an end-to-end payments+POS stack processing ~1.8B txns and $115B TPV in 2024, with adjusted gross margin ~57% and 99.99% uptime, driving higher take-rates and net retention >100% (2024) plus subscription rev +22% YoY and churn below ~6%.

| Metric | 2024 |

|---|---|

| Transactions | ~1.8B |

| TPV | $115B |

| Adj. gross margin | ~57% |

| Uptime | 99.99% |

| Net retention | >100% |

| Subscription rev YoY | +22% |

| Churn | <6% est. |

What is included in the product

Provides a concise SWOT overview of Shift4, outlining its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise Shift4 SWOT summary for quick strategic alignment and executive snapshot readiness.

Weaknesses

Sector Concentration Risks

Substantial Long-Term Debt Obligations

Shift4’s aggressive M&A push has left long-term debt near $1.6 billion as of FY2024, raising leverage; net debt to EBITDA was about 3.8x in Q4 2024, above peer medians. Current EBITDA and cash flow cover interest, but high leverage reduces flexibility if credit tightens or rates rise. Lowering the debt-to-equity ratio is essential to secure cheaper capital and sustain growth.

Integration Complexity of Legacy Systems

Shift4’s strength in integrations comes with high maintenance costs: supporting hundreds of legacy POS and ERP variants drove tech spend up 18% in 2024 vs 2023, per company disclosures, and raised per-merchant support costs by an estimated $12–18 annually. Each bespoke integration needs ongoing patches and testing, straining engineering capacity and slowing feature rollouts across the merchant base by weeks to months.

Geographic Concentration in North America

Shift4 still earns about 82% of net revenue from North America as of FY2024, leaving it exposed to U.S. rule changes and a 2023–24 regional downturn that cut hospitality transactions by ~7% year-over-year.

International expansion into Europe and Asia is vital to diversify risk but requires navigating PSD2-style regulations, local acquiring rules, and cultural payment preferences, raising expansion costs and extending payback beyond 3–5 years.

- ~82% FY2024 revenue North America

- Hospitality transactions down ~7% in 2023–24

- 3–5+ year payback for EU/Asia entry

- Regulatory hurdles: PSD2, local acquiring, data residency

Dependence on Third-Party Hardware Partners

Shift4 depends on multiple third-party hardware makers for POS terminals; in 2024 about 35% of merchants used non-proprietary devices, exposing Shift4 to suppliers’ quality or supply-chain issues that can delay deployments and hit revenue.

Supply disruptions in 2021–23 raised device lead times by ~40%, and a similar hiccup could dent transaction volume and reputation; building proprietary hardware would cut dependence but needs large CapEx—likely $50–150M upfront.

What this hides: hardware R&D and certification take 12–24 months, and slower merchant rollouts raise churn risk.

- 35% merchants on third-party devices (2024)

- Supply lead times rose ~40% (2021–23)

- Estimated proprietary CapEx $50–150M

- R&D/certification 12–24 months

Shift4 risks: hospitality/NA concentration, high debt, rising tech costs, long EU/Asia payback

| Metric | Value (2024) |

|---|---|

| Hospitality revenue | 40–50% |

| North America | ~82% |

| Net debt | ~$1.6B |

| Net debt/EBITDA | ~3.8x |

| Tech spend growth | +18% |

| Third-party devices | 35% |

| EU/Asia payback | 3–5+ yrs |

What You See Is What You Get

Shift4 SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real, editable analysis that becomes available after checkout. Buy now to unlock the complete, structured report ready for use.