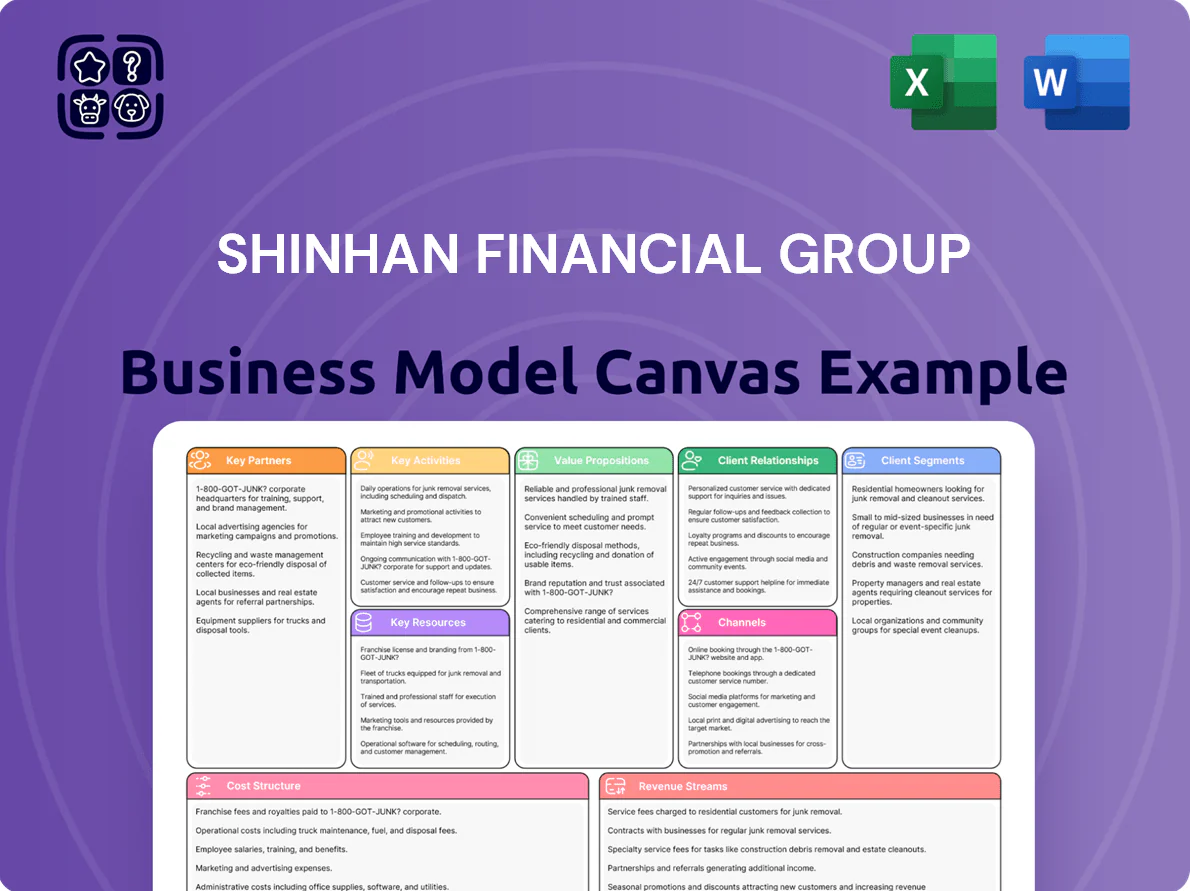

Shinhan Financial Group Business Model Canvas

Shinhan Financial Group: Actionable Business Model Canvas to Boost Strategy & ROI

Unlock the full strategic blueprint behind Shinhan Financial Group’s business model—this in-depth Business Model Canvas exposes how the bank drives customer value, diversifies revenue, and leverages digital partnerships to scale; ideal for investors, consultants, and executives seeking actionable, ready-to-use insights. Download the complete Word/Excel canvas to benchmark strategy, model revenue impacts, and accelerate decision-making.

Partnerships

Strategic Fintech Alliances

Shinhan Financial Group partners with emerging fintechs to embed payment and wealth-management tools across its network, accelerating deployments that cut time-to-market by roughly 30% versus internal builds; by end-2025 these alliances include global blockchain and AI research centers. This model reduces R&D spend volatility, shifting an estimated KRW 120–150 billion in experimental costs to partner-backed pilots while keeping Shinhan competitive with digital-only banks.

Global Banking Networks

Shinhan Financial Group partners with global banks such as Japan’s Mizuho Financial Group to enable cross-border deals and joint ventures, supporting expansion in Southeast Asia where Shinhan’s overseas assets reached about KRW 60 trillion (2024). These alliances yield joint credit facilities and co-investments, giving Shinhan local market expertise, shared infrastructure, and diversified geographic revenue and risk exposure.

Technology and Cloud Providers

Shinhan partners with global and Korean cloud leaders (eg, AWS, Google Cloud, Naver Cloud) to run the Shinhan Super SOL app and data platforms, using scalable cloud-native infrastructure that handled peak loads of 5M daily sessions in 2024; contracts mandate encryption, SOC2/ISO27001 compliance and Korea’s Financial Services Commission rules to keep customer data protected, ensuring >99.95% uptime and low-latency performance.

Government and Regulatory Bodies

As a systemic financial institution, Shinhan Financial Group coordinates with the Financial Services Commission and other regulators to support market stability and secure licenses, with regulatory capital ratio (BIS CET1) at 13.2% as of 2025 Q1 reflecting strong compliance.

Engaging in policy dialogue aligns Shinhan’s strategy with South Korea’s economic goals and changing laws, reducing legal risk and protecting long-term operations.

- Regular dialogue with FSC and BoK

- 13.2% CET1 ratio (2025 Q1)

- Licensing across 20+ jurisdictions

- Proactive compliance reduces systemic risk

Retail and Lifestyle Ecosystem Partners

Shinhan embeds banking into e-commerce, mobility, and delivery apps, enabling in-app loans, payments, and insurance; by 2024 these partnerships helped generate over KRW 1.2 trillion in fee and interchange revenue across channel integrations.

Sharing transaction data and loyalty points cuts customer acquisition cost—est. 40% lower vs. digital ads—and increases daily touchpoints, raising active customer engagement by ~18% year-over-year in 2023–24.

- In-app payments, loans, insurance

- KRW 1.2T revenue (2024)

- ~40% lower acquisition cost

- +18% active engagement (2023–24)

Shinhan cuts time-to-market 30%, drives KRW1.2T fees, KRW60T overseas assets, CET1 13.2%

Shinhan’s key partners—fintechs, global banks (eg, Mizuho), cloud providers (AWS/Google/Naver), regulators—cut time-to-market ~30%, shift KRW 120–150B experimental costs to pilots, support KRW 60T overseas assets (2024), ensure >99.95% uptime, and generated KRW 1.2T fees (2024); CET1 13.2% (2025 Q1).

| Metric | Value |

|---|---|

| Time-to-market | -30% |

| R&D shifted | KRW 120–150B |

| Overseas assets | KRW 60T (2024) |

| Fee revenue | KRW 1.2T (2024) |

| CET1 | 13.2% (2025 Q1) |

What is included in the product

A concise Business Model Canvas for Shinhan Financial Group outlining customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure, reflecting real-world banking, insurance, and fintech operations.

Condenses Shinhan Financial Group’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and use in boardroom or teaching settings.

Activities

Digital Platform Development and Optimization

Shinhan’s key activity is continuous Super SOL app improvement to unify banking, brokerage, and insurance into one high-speed interface, targeting a 20–30% increase in cross-sell rates; developers deploy agile sprints—weekly releases—and A/B tests informed by 12m user-feedback samples (2024) to cut drop-off by 15%.

Risk Management and Credit Analysis

Shinhan uses AI-driven credit models and real-time market monitors to keep non-performing loan ratio near 0.35% (2024) and protect CET1 capital, adjusting lending criteria as global PMI, CPI, and FX moves change; this helped sustain net interest margin around 1.92% in 2024. Constant macro monitoring lets Shinhan lower PDs and offer competitive rates, supporting loan growth while preserving capital buffers.

Financial Product Innovation

Shinhan Financial Group’s research teams design new instruments—like ESG-themed funds and tailored retirement solutions—using data analytics to pinpoint market gaps; in 2024 Shinhan Asset Management launched three ESG ETFs that helped grow group AUM to about KRW 420 trillion, capturing fresh fee income. By staying ahead of trends, the group targets higher-margin retail and institutional mandates, aiming to lift product-driven revenue share versus peers.

Customer Relationship Management and Marketing

Shinhan Financial Group runs data-driven marketing that segments customers for personalized advice and product offers, using omnichannel campaigns across ~1,000 branches and digital channels to keep messaging consistent; digital sales grew 28% y/y in 2024, boosting fee income.

Loyalty program Shinhan Plus drives retention and lifetime value—over 10 million members as of Dec 2024—with targeted promotions that help keep brand top-of-mind in a crowded Korean financial market.

- Data-driven personalization: segment-level targeting

- Omnichannel: ~1,000 branches + web/app

- Digital sales growth: +28% y/y (2024)

- Shinhan Plus: 10M+ members (Dec 2024)

Asset Management and Wealth Advisory

Shinhan offers high-net-worth and institutional clients active portfolio management across equities, bonds and alternatives, leveraging proprietary research to target long-term returns and risk control; wealth advisory fees contributed about 18% of 2024 Shinhan Financial Group fee income, supporting stable recurring revenue.

- Fee income share: ~18% of 2024 fees

- Assets under management: ~KRW 210 trillion (2024)

- Client segments: HNWIs, pensions, insurers

- Services: discretionary mandates, bespoke advice, alternatives

Shinhan Super SOL boosts cross-sell 20–30%, AUM KRW420T, NPL 0.35% — 10M+ members

Shinhan’s key activities: iterate Super SOL for unified banking/brokerage/insurance—weekly agile releases and A/B tests on 12m user samples (2024) to raise cross-sell 20–30% and cut drop-off 15%; AI credit models keep NPL ~0.35% and NIM ~1.92% (2024); asset management grew AUM to KRW 420T, fees +18% share; loyalty Shinhan Plus 10M+ members (Dec 2024).

| Metric | 2024 |

|---|---|

| Cross-sell target | 20–30% |

| Users sampled | 12M |

| NPL ratio | 0.35% |

| NIM | 1.92% |

| AUM (group) | KRW 420T |

| Fee share (wealth) | 18% |

| Shinhan Plus members | 10M+ |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Shinhan Financial Group Business Model Canvas you’ll receive after purchase — not a mockup or sample, but a direct snapshot from the final file.

When you complete your order, you’ll get full access to this same professional, ready-to-use document in editable formats, structured and formatted exactly as shown here.

No surprises or fillers: the previewed content is part of the final deliverable, instantly downloadable and ready to present, edit, or share.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Shinhan Financial Group: Actionable Business Model Canvas to Boost Strategy & ROI

Unlock the full strategic blueprint behind Shinhan Financial Group’s business model—this in-depth Business Model Canvas exposes how the bank drives customer value, diversifies revenue, and leverages digital partnerships to scale; ideal for investors, consultants, and executives seeking actionable, ready-to-use insights. Download the complete Word/Excel canvas to benchmark strategy, model revenue impacts, and accelerate decision-making.

Partnerships

Strategic Fintech Alliances

Shinhan Financial Group partners with emerging fintechs to embed payment and wealth-management tools across its network, accelerating deployments that cut time-to-market by roughly 30% versus internal builds; by end-2025 these alliances include global blockchain and AI research centers. This model reduces R&D spend volatility, shifting an estimated KRW 120–150 billion in experimental costs to partner-backed pilots while keeping Shinhan competitive with digital-only banks.

Global Banking Networks

Shinhan Financial Group partners with global banks such as Japan’s Mizuho Financial Group to enable cross-border deals and joint ventures, supporting expansion in Southeast Asia where Shinhan’s overseas assets reached about KRW 60 trillion (2024). These alliances yield joint credit facilities and co-investments, giving Shinhan local market expertise, shared infrastructure, and diversified geographic revenue and risk exposure.

Technology and Cloud Providers

Shinhan partners with global and Korean cloud leaders (eg, AWS, Google Cloud, Naver Cloud) to run the Shinhan Super SOL app and data platforms, using scalable cloud-native infrastructure that handled peak loads of 5M daily sessions in 2024; contracts mandate encryption, SOC2/ISO27001 compliance and Korea’s Financial Services Commission rules to keep customer data protected, ensuring >99.95% uptime and low-latency performance.

Government and Regulatory Bodies

As a systemic financial institution, Shinhan Financial Group coordinates with the Financial Services Commission and other regulators to support market stability and secure licenses, with regulatory capital ratio (BIS CET1) at 13.2% as of 2025 Q1 reflecting strong compliance.

Engaging in policy dialogue aligns Shinhan’s strategy with South Korea’s economic goals and changing laws, reducing legal risk and protecting long-term operations.

- Regular dialogue with FSC and BoK

- 13.2% CET1 ratio (2025 Q1)

- Licensing across 20+ jurisdictions

- Proactive compliance reduces systemic risk

Retail and Lifestyle Ecosystem Partners

Shinhan embeds banking into e-commerce, mobility, and delivery apps, enabling in-app loans, payments, and insurance; by 2024 these partnerships helped generate over KRW 1.2 trillion in fee and interchange revenue across channel integrations.

Sharing transaction data and loyalty points cuts customer acquisition cost—est. 40% lower vs. digital ads—and increases daily touchpoints, raising active customer engagement by ~18% year-over-year in 2023–24.

- In-app payments, loans, insurance

- KRW 1.2T revenue (2024)

- ~40% lower acquisition cost

- +18% active engagement (2023–24)

Shinhan cuts time-to-market 30%, drives KRW1.2T fees, KRW60T overseas assets, CET1 13.2%

Shinhan’s key partners—fintechs, global banks (eg, Mizuho), cloud providers (AWS/Google/Naver), regulators—cut time-to-market ~30%, shift KRW 120–150B experimental costs to pilots, support KRW 60T overseas assets (2024), ensure >99.95% uptime, and generated KRW 1.2T fees (2024); CET1 13.2% (2025 Q1).

| Metric | Value |

|---|---|

| Time-to-market | -30% |

| R&D shifted | KRW 120–150B |

| Overseas assets | KRW 60T (2024) |

| Fee revenue | KRW 1.2T (2024) |

| CET1 | 13.2% (2025 Q1) |

What is included in the product

A concise Business Model Canvas for Shinhan Financial Group outlining customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure, reflecting real-world banking, insurance, and fintech operations.

Condenses Shinhan Financial Group’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and use in boardroom or teaching settings.

Activities

Digital Platform Development and Optimization

Shinhan’s key activity is continuous Super SOL app improvement to unify banking, brokerage, and insurance into one high-speed interface, targeting a 20–30% increase in cross-sell rates; developers deploy agile sprints—weekly releases—and A/B tests informed by 12m user-feedback samples (2024) to cut drop-off by 15%.

Risk Management and Credit Analysis

Shinhan uses AI-driven credit models and real-time market monitors to keep non-performing loan ratio near 0.35% (2024) and protect CET1 capital, adjusting lending criteria as global PMI, CPI, and FX moves change; this helped sustain net interest margin around 1.92% in 2024. Constant macro monitoring lets Shinhan lower PDs and offer competitive rates, supporting loan growth while preserving capital buffers.

Financial Product Innovation

Shinhan Financial Group’s research teams design new instruments—like ESG-themed funds and tailored retirement solutions—using data analytics to pinpoint market gaps; in 2024 Shinhan Asset Management launched three ESG ETFs that helped grow group AUM to about KRW 420 trillion, capturing fresh fee income. By staying ahead of trends, the group targets higher-margin retail and institutional mandates, aiming to lift product-driven revenue share versus peers.

Customer Relationship Management and Marketing

Shinhan Financial Group runs data-driven marketing that segments customers for personalized advice and product offers, using omnichannel campaigns across ~1,000 branches and digital channels to keep messaging consistent; digital sales grew 28% y/y in 2024, boosting fee income.

Loyalty program Shinhan Plus drives retention and lifetime value—over 10 million members as of Dec 2024—with targeted promotions that help keep brand top-of-mind in a crowded Korean financial market.

- Data-driven personalization: segment-level targeting

- Omnichannel: ~1,000 branches + web/app

- Digital sales growth: +28% y/y (2024)

- Shinhan Plus: 10M+ members (Dec 2024)

Asset Management and Wealth Advisory

Shinhan offers high-net-worth and institutional clients active portfolio management across equities, bonds and alternatives, leveraging proprietary research to target long-term returns and risk control; wealth advisory fees contributed about 18% of 2024 Shinhan Financial Group fee income, supporting stable recurring revenue.

- Fee income share: ~18% of 2024 fees

- Assets under management: ~KRW 210 trillion (2024)

- Client segments: HNWIs, pensions, insurers

- Services: discretionary mandates, bespoke advice, alternatives

Shinhan Super SOL boosts cross-sell 20–30%, AUM KRW420T, NPL 0.35% — 10M+ members

Shinhan’s key activities: iterate Super SOL for unified banking/brokerage/insurance—weekly agile releases and A/B tests on 12m user samples (2024) to raise cross-sell 20–30% and cut drop-off 15%; AI credit models keep NPL ~0.35% and NIM ~1.92% (2024); asset management grew AUM to KRW 420T, fees +18% share; loyalty Shinhan Plus 10M+ members (Dec 2024).

| Metric | 2024 |

|---|---|

| Cross-sell target | 20–30% |

| Users sampled | 12M |

| NPL ratio | 0.35% |

| NIM | 1.92% |

| AUM (group) | KRW 420T |

| Fee share (wealth) | 18% |

| Shinhan Plus members | 10M+ |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Shinhan Financial Group Business Model Canvas you’ll receive after purchase — not a mockup or sample, but a direct snapshot from the final file.

When you complete your order, you’ll get full access to this same professional, ready-to-use document in editable formats, structured and formatted exactly as shown here.

No surprises or fillers: the previewed content is part of the final deliverable, instantly downloadable and ready to present, edit, or share.