Shinhan Financial Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Shinhan Financial Group faces intense domestic competition, regulatory scrutiny, and evolving tech-driven threats, yet benefits from strong brand equity and diversified services that help mitigate supplier and buyer pressures; this snapshot outlines key dynamics but omits force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Cost of Capital and Deposits

Depositors supply the bulk of Shinhan Financial Group’s funding, so their collective moves matter more than individual bargaining; retail depositors exert limited direct power but can shift funds en masse.

Interest rate sensitivity forces Shinhan to price deposits competitively—Shinhan’s 2024 average deposit cost rose to about 1.8% as market rates climbed, squeezing net interest margins.

By end-2025, faster digital transfers and real-time rate visibility let savers reallocate quickly, increasing short-term funding volatility and pressuring margins unless Shinhan boosts yields or diversifies funding.

IT and Fintech Infrastructure Providers

As Shinhan accelerates digital transformation, dependence on global cloud, AI and cybersecurity vendors (AWS, Microsoft, Google, Palo Alto) raises supplier power: these firms control platforms that handle trillions in transaction data and uptime SLAs, making their services mission-critical.

High switching costs—estimated at hundreds of millions of dollars and months to years for large-scale migration—plus regulatory data-residency and security requirements further lock Shinhan into incumbent providers, strengthening supplier leverage.

Skilled Human Capital

The demand for specialists in data science, blockchain, and financial engineering is very high in South Korea; 2024 job postings for AI and data roles rose 38% year-over-year, tightening supply. Shinhan Financial Group competes with other banks, fintechs, and big techs like Naver and Kakao, forcing salaries up—median data scientist pay climbed ~22% from 2022 to 2024. That gives top talent strong bargaining power over pay and remote/flexible terms, raising Shinhan’s operating costs and hiring budgets. In 2024 Shinhan reported staff costs rising 6.8%, reflecting this pressure.

Regulatory and Central Bank Influence

The Bank of Korea (BoK) sets the base rate that determines Shinhan Financial Group’s wholesale funding cost; its 2025 policy rate was 3.50% as of Jan 2025, so Shinhan cannot negotiate that core input and must price loans around it.

BoK actions also control money supply and macroprudential rules (LTV/DTI caps); tighter stances in 2024–25 reduced Shinhan’s lending capacity and pressured net interest margin.

Credit Rating Agencies

Institutional credit rating agencies are essential for Shinhan Financial Group’s access to global debt markets; Moody’s, S&P, and Fitch ratings shape investor demand and pricing.

Their assessments directly affect Shinhan’s funding cost—each notch change can shift spreads by ~20–40 basis points, altering annual interest expense by tens of millions USD on ~KRW 40 trillion debt (2024-end).

To keep high ratings Shinhan must meet strict global standards on capital, liquidity, and governance, creating dependency on favorable agency perceptions.

- Agency ratings set bond spreads (≈20–40 bps per notch)

- Shinhan had ~KRW 40 trillion debt (2024)

- Maintaining ratings needs strong CAR, LCR, governance

Rising supplier power: funding, ratings and talent squeeze margins

Suppliers (depositors, cloud/AI vendors, talent, BoK, ratings agencies) exert moderate-to-high power: deposit costs rose to ~1.8% in 2024, BoK policy rate 3.50% (Jan 2025) sets non-negotiable funding baseline, ~KRW 40tn debt (2024) makes ratings moves shift spreads ~20–40bps, and vendor lock-in plus 22% higher median data scientist pay (2022–24) raise costs and switching barriers.

| Input | Key 2024–25 data |

|---|---|

| Avg deposit cost | ~1.8% (2024) |

| BoK policy rate | 3.50% (Jan 2025) |

| Debt | ~KRW 40 trillion (2024) |

| Rating spread impact | ~20–40 bps per notch |

| Data scientist pay rise | ~22% (2022–24) |

What is included in the product

Tailored exclusively for Shinhan Financial Group, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping its profitability.

A concise Porter's Five Forces snapshot for Shinhan Financial Group—speed up strategy decisions with clear force ratings and actionable implications tailored to Korea's banking landscape.

Customers Bargaining Power

Low Switching Costs for Retail Users

Open Banking maturation and account migration services in South Korea have cut switching effort to minutes, with 2024 data showing 28% of retail customers used migration tools and mobile bank switching up 42% year-over-year.

This click-to-transfer ease lets users compare fees and products across providers instantly, raising bargaining power and pushing price sensitivity higher—average household banking fee complaints rose 15% in 2024.

Shinhan Financial Group must therefore invest in UX and retention: Shinhan increased digital customer experience spending to KRW 320 billion in 2024, or ~12% of its IT budget, to curb attrition.

Corporate Client Negotiating Power

Price Sensitivity in Interest Rates

Modern consumers use real-time digital comparison tools, and 72% of South Korean retail banking customers checked rates online before choosing a bank in 2024, so price sensitivity squeezes Shinhan’s net interest margin (NIM) — 1.20% in 2024 vs. KB Financial’s 1.35%—limiting room to widen spreads on loans and deposits.

To retain deposits and loans, Shinhan must keep rates at or near market leaders; otherwise volume shifts quickly: market-rate gaps over 10–15 bps drove notable deposit outflows in Q3 2024, effectively giving customers pricing control.

Demand for Integrated Financial Ecosystems

By late 2025, 62% of Korean retail customers expect a single app for banking, insurance, and investments, pushing Shinhan to prioritize integrated UX or risk migration to rivals like KakaoBank and Toss.

If Shinhan lags, churn could rise; Toss reported 18% YoY active-user growth in 2024, showing appetite for seamless lifestyle finance.

Customers now shape Shinhan’s tech roadmap and bundling strategy, forcing investments in APIs, open banking, and cross-sell algorithms to retain share.

- 62% of customers want Super App by 2025

- Toss 18% active-user growth (2024)

- Risk: higher churn if UX lags

- Action: invest in APIs, open banking, cross-sell

Impact of Consumer Protection Regulations

Strict South Korean financial rules now force Shinhan Financial Group to disclose fees and loan terms, narrowing the bank’s information edge; a 2024 Financial Services Commission survey found 68% of consumers use disclosed APRs to compare lenders.

Consumers can file complaints and seek remedies—Korea Consumer Agency reported a 12% rise in banking-related disputes in 2023—so customers press for fairer fees and service, shifting bargaining power toward them.

- 2024: 68% use APR disclosures

- 2023: 12% rise in banking disputes

- Mandatory fee transparency reduces bank information advantage

Rising Customer Leverage: Rate-Checks, Open Banking Cut NIMs—1% Churn Costs KRW120bn

Customers have rising leverage: 2024 open-banking migration (28%) and 72% rate-checking raise price sensitivity; Shinhan’s NIM fell to 1.20% (2024) vs KB 1.35%. Chaebol loans (≈18% of corporate market) give corporates bargaining clout; 1% top-client churn risks ≈KRW 120bn. Regulation and disclosures (68% use APRs, 12% rise in disputes) further shift power to customers.

| Metric | Value (Year) |

|---|---|

| Open-banking migration | 28% (2024) |

| Rate checks | 72% (2024) |

| Shinhan NIM | 1.20% (2024) |

| Chaebol share | 18% (2024) |

| Top-client churn cost | KRW 120bn per 1% (2025) |

What You See Is What You Get

Shinhan Financial Group Porter's Five Forces Analysis

This preview shows the exact Shinhan Financial Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

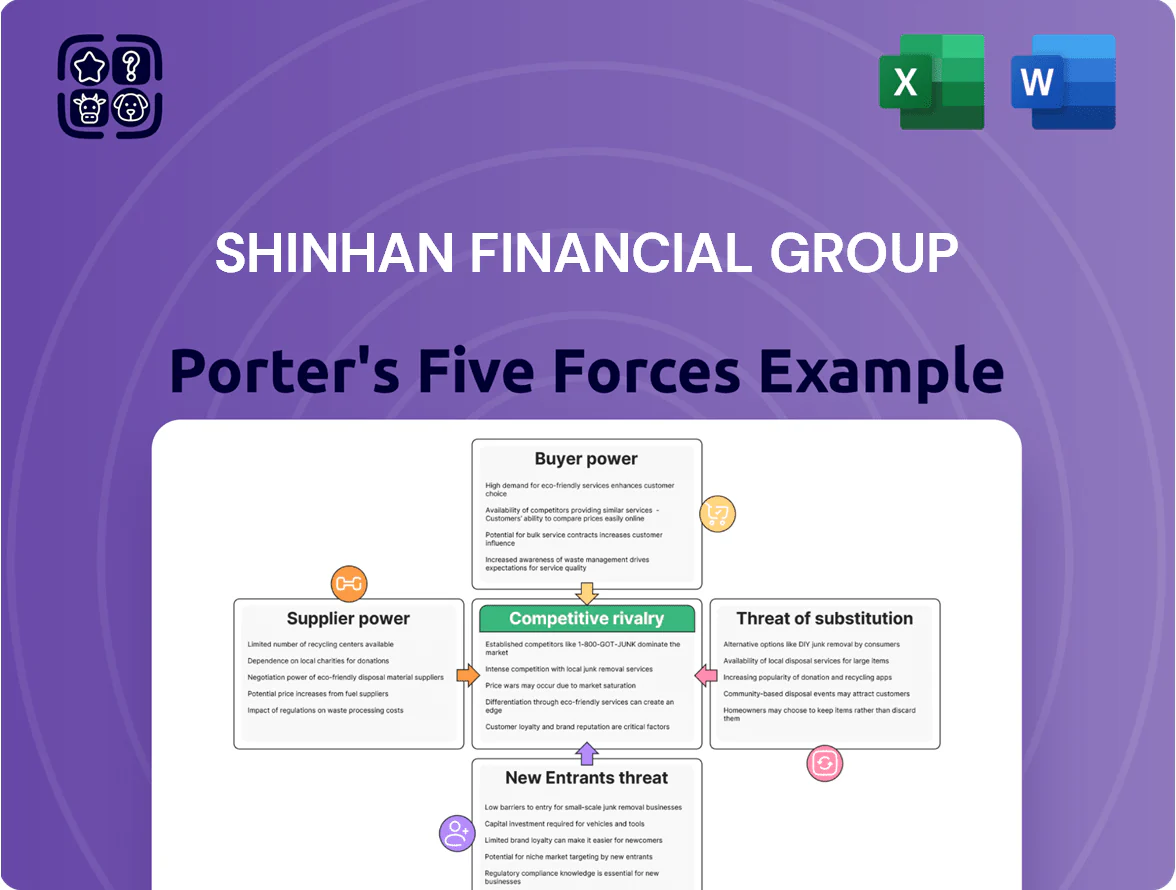

It is the same professional document available for instant download upon payment, containing detailed assessments of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitution risks.

No samples or excerpts—what you see here is the complete deliverable, ready to support your strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Shinhan Financial Group faces intense domestic competition, regulatory scrutiny, and evolving tech-driven threats, yet benefits from strong brand equity and diversified services that help mitigate supplier and buyer pressures; this snapshot outlines key dynamics but omits force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Cost of Capital and Deposits

Depositors supply the bulk of Shinhan Financial Group’s funding, so their collective moves matter more than individual bargaining; retail depositors exert limited direct power but can shift funds en masse.

Interest rate sensitivity forces Shinhan to price deposits competitively—Shinhan’s 2024 average deposit cost rose to about 1.8% as market rates climbed, squeezing net interest margins.

By end-2025, faster digital transfers and real-time rate visibility let savers reallocate quickly, increasing short-term funding volatility and pressuring margins unless Shinhan boosts yields or diversifies funding.

IT and Fintech Infrastructure Providers

As Shinhan accelerates digital transformation, dependence on global cloud, AI and cybersecurity vendors (AWS, Microsoft, Google, Palo Alto) raises supplier power: these firms control platforms that handle trillions in transaction data and uptime SLAs, making their services mission-critical.

High switching costs—estimated at hundreds of millions of dollars and months to years for large-scale migration—plus regulatory data-residency and security requirements further lock Shinhan into incumbent providers, strengthening supplier leverage.

Skilled Human Capital

The demand for specialists in data science, blockchain, and financial engineering is very high in South Korea; 2024 job postings for AI and data roles rose 38% year-over-year, tightening supply. Shinhan Financial Group competes with other banks, fintechs, and big techs like Naver and Kakao, forcing salaries up—median data scientist pay climbed ~22% from 2022 to 2024. That gives top talent strong bargaining power over pay and remote/flexible terms, raising Shinhan’s operating costs and hiring budgets. In 2024 Shinhan reported staff costs rising 6.8%, reflecting this pressure.

Regulatory and Central Bank Influence

The Bank of Korea (BoK) sets the base rate that determines Shinhan Financial Group’s wholesale funding cost; its 2025 policy rate was 3.50% as of Jan 2025, so Shinhan cannot negotiate that core input and must price loans around it.

BoK actions also control money supply and macroprudential rules (LTV/DTI caps); tighter stances in 2024–25 reduced Shinhan’s lending capacity and pressured net interest margin.

Credit Rating Agencies

Institutional credit rating agencies are essential for Shinhan Financial Group’s access to global debt markets; Moody’s, S&P, and Fitch ratings shape investor demand and pricing.

Their assessments directly affect Shinhan’s funding cost—each notch change can shift spreads by ~20–40 basis points, altering annual interest expense by tens of millions USD on ~KRW 40 trillion debt (2024-end).

To keep high ratings Shinhan must meet strict global standards on capital, liquidity, and governance, creating dependency on favorable agency perceptions.

- Agency ratings set bond spreads (≈20–40 bps per notch)

- Shinhan had ~KRW 40 trillion debt (2024)

- Maintaining ratings needs strong CAR, LCR, governance

Rising supplier power: funding, ratings and talent squeeze margins

Suppliers (depositors, cloud/AI vendors, talent, BoK, ratings agencies) exert moderate-to-high power: deposit costs rose to ~1.8% in 2024, BoK policy rate 3.50% (Jan 2025) sets non-negotiable funding baseline, ~KRW 40tn debt (2024) makes ratings moves shift spreads ~20–40bps, and vendor lock-in plus 22% higher median data scientist pay (2022–24) raise costs and switching barriers.

| Input | Key 2024–25 data |

|---|---|

| Avg deposit cost | ~1.8% (2024) |

| BoK policy rate | 3.50% (Jan 2025) |

| Debt | ~KRW 40 trillion (2024) |

| Rating spread impact | ~20–40 bps per notch |

| Data scientist pay rise | ~22% (2022–24) |

What is included in the product

Tailored exclusively for Shinhan Financial Group, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping its profitability.

A concise Porter's Five Forces snapshot for Shinhan Financial Group—speed up strategy decisions with clear force ratings and actionable implications tailored to Korea's banking landscape.

Customers Bargaining Power

Low Switching Costs for Retail Users

Open Banking maturation and account migration services in South Korea have cut switching effort to minutes, with 2024 data showing 28% of retail customers used migration tools and mobile bank switching up 42% year-over-year.

This click-to-transfer ease lets users compare fees and products across providers instantly, raising bargaining power and pushing price sensitivity higher—average household banking fee complaints rose 15% in 2024.

Shinhan Financial Group must therefore invest in UX and retention: Shinhan increased digital customer experience spending to KRW 320 billion in 2024, or ~12% of its IT budget, to curb attrition.

Corporate Client Negotiating Power

Price Sensitivity in Interest Rates

Modern consumers use real-time digital comparison tools, and 72% of South Korean retail banking customers checked rates online before choosing a bank in 2024, so price sensitivity squeezes Shinhan’s net interest margin (NIM) — 1.20% in 2024 vs. KB Financial’s 1.35%—limiting room to widen spreads on loans and deposits.

To retain deposits and loans, Shinhan must keep rates at or near market leaders; otherwise volume shifts quickly: market-rate gaps over 10–15 bps drove notable deposit outflows in Q3 2024, effectively giving customers pricing control.

Demand for Integrated Financial Ecosystems

By late 2025, 62% of Korean retail customers expect a single app for banking, insurance, and investments, pushing Shinhan to prioritize integrated UX or risk migration to rivals like KakaoBank and Toss.

If Shinhan lags, churn could rise; Toss reported 18% YoY active-user growth in 2024, showing appetite for seamless lifestyle finance.

Customers now shape Shinhan’s tech roadmap and bundling strategy, forcing investments in APIs, open banking, and cross-sell algorithms to retain share.

- 62% of customers want Super App by 2025

- Toss 18% active-user growth (2024)

- Risk: higher churn if UX lags

- Action: invest in APIs, open banking, cross-sell

Impact of Consumer Protection Regulations

Strict South Korean financial rules now force Shinhan Financial Group to disclose fees and loan terms, narrowing the bank’s information edge; a 2024 Financial Services Commission survey found 68% of consumers use disclosed APRs to compare lenders.

Consumers can file complaints and seek remedies—Korea Consumer Agency reported a 12% rise in banking-related disputes in 2023—so customers press for fairer fees and service, shifting bargaining power toward them.

- 2024: 68% use APR disclosures

- 2023: 12% rise in banking disputes

- Mandatory fee transparency reduces bank information advantage

Rising Customer Leverage: Rate-Checks, Open Banking Cut NIMs—1% Churn Costs KRW120bn

Customers have rising leverage: 2024 open-banking migration (28%) and 72% rate-checking raise price sensitivity; Shinhan’s NIM fell to 1.20% (2024) vs KB 1.35%. Chaebol loans (≈18% of corporate market) give corporates bargaining clout; 1% top-client churn risks ≈KRW 120bn. Regulation and disclosures (68% use APRs, 12% rise in disputes) further shift power to customers.

| Metric | Value (Year) |

|---|---|

| Open-banking migration | 28% (2024) |

| Rate checks | 72% (2024) |

| Shinhan NIM | 1.20% (2024) |

| Chaebol share | 18% (2024) |

| Top-client churn cost | KRW 120bn per 1% (2025) |

What You See Is What You Get

Shinhan Financial Group Porter's Five Forces Analysis

This preview shows the exact Shinhan Financial Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

It is the same professional document available for instant download upon payment, containing detailed assessments of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitution risks.

No samples or excerpts—what you see here is the complete deliverable, ready to support your strategic or investment decisions.