Shinhan Financial Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Shinhan Financial Group pinpoints the regulatory shifts, macroeconomic pressures, and technological trends reshaping its strategy and risk profile—crucial intelligence for investors and strategists seeking a competitive edge. Purchase the full, ready-to-use report to access detailed, actionable insights and forecasts that save research time and power better decisions.

Political factors

South Korean Government Financial Policy

The South Korean government maintains strict oversight of the financial sector to ensure systemic stability and fair competition, with bank non-performing loan ratios held near 0.6% in 2025 to date. Throughout 2025 the Financial Services Commission pushed corporate value-up programs and higher shareholder returns, prompting Shinhan to target a CET1 ratio around 12.5% while boosting dividends and buybacks. Political leadership changes could quickly alter credit guidelines and mortgage caps, affecting loan growth and NIMs.

Geopolitical Tensions in the Korean Peninsula

Persistent tensions with North Korea keep investor risk aversion high, contributing to a 2025 surge in implied equity volatility for Korean banks—KOSPI bank index VIX rose ~28% during flare-ups—pressuring valuations of Shinhan Financial Group (market cap ₩24.3tr as of Jan 2026).

Escalations prompt capital flight risk: nonresident holdings of Korean equities dipped to 31.8% in 2024, raising Shinhan’s cost of funding and risking rating pressure; Moody’s and S&P monitor regional stability when assessing sovereign-linked credit spreads.

Shinhan must maintain robust contingency plans—liquidity buffers (LCR >100%), diversified funding, and crisis IRR management—to manage tail risks and protect capital adequacy (2025 CET1 ~12.1%).

Global Trade Relations and Protectionism

Shinhan Financial Group’s expansion in Southeast Asia and the US exposes it to global trade volatility and rising protectionism; US-China tariff tensions since 2018 have contributed to a 12-18% supply-chain cost increase for affected Korean exporters, raising corporate borrower stress. Trade disputes can alter clients’ revenue and working capital, shifting credit-risk models—Korean exporters saw non-performing loan ratios tick up 0.2–0.5 percentage points during major tariff episodes. Managing geopolitical risk is therefore critical to Shinhan’s overseas loan growth and capital allocation strategies.

Taxation Policies and Fiscal Reforms

Legislative shifts in corporate tax and financial transaction taxes directly affect Shinhan Financial Group’s net income; in 2024 South Korea’s effective corporate tax changes could alter Shinhan’s 2023 net profit KRW 4.2 trillion by several percentage points, impacting ROE and capital allocation.

Policy debates on wealth redistribution have driven proposals for bank windfall taxes and dividend tax hikes; increased dividend taxation reduces shareholder after-tax returns and may force Shinhan to retain earnings rather than distribute from its 2023 dividend payout ratio ~20%.

Such fiscal reforms constrain Shinhan’s ability to reinvest earnings into digital transformation and loan growth, affecting capital adequacy and shareholder value amidst a CET1 ratio around 13–14% in 2024.

- Corporate tax rate moves can swing net profit by multiple % points

- Windfall/dividend tax proposals pressure payout policies and retention

- Fiscal changes influence reinvestment, CET1, ROE, and shareholder returns

Government Social Responsibility Mandates

Political pressure keeps major banks like Shinhan tied to SME and vulnerable-population support; in 2024 Shinhan reported KRW 12.4 trillion in SME lending, reflecting government-driven priorities.

Shinhan is regularly expected to join government relief schemes and extend low-interest loans during downturns—its Household & SME loans rose 7.1% YoY in 2024 amid policy programs.

Executive leadership must balance these mandates with shareholder fiduciary duties as mandated programs can compress net interest margins (NIM 1.45% in 2024) and increase credit risk exposure.

- KRW 12.4T SME lending (2024)

- Household & SME loans +7.1% YoY (2024)

- NIM 1.45% (2024) highlights margin pressure

Shinhan faces political, fiscal and market shocks: CET1 12–13%, NIM 1.45%, KOSPI VIX +28%

Political oversight, geopolitical tensions, and fiscal policy materially shape Shinhan’s capital, funding and credit costs: 2024–25 CET1 ~12–13%, NIM 1.45% (2024), SME lending KRW12.4T (2024), nonresident equity share 31.8% (2024), KOSPI bank VIX spike ~28% (2025). Proposed tax/windfall measures and government relief mandates press payout policy and ROE.

| Metric | Value |

|---|---|

| CET1 | ~12–13% |

| NIM | 1.45% |

| SME lending | KRW12.4T |

| Nonresident equity | 31.8% |

| KOSPI bank VIX move | ~+28% |

What is included in the product

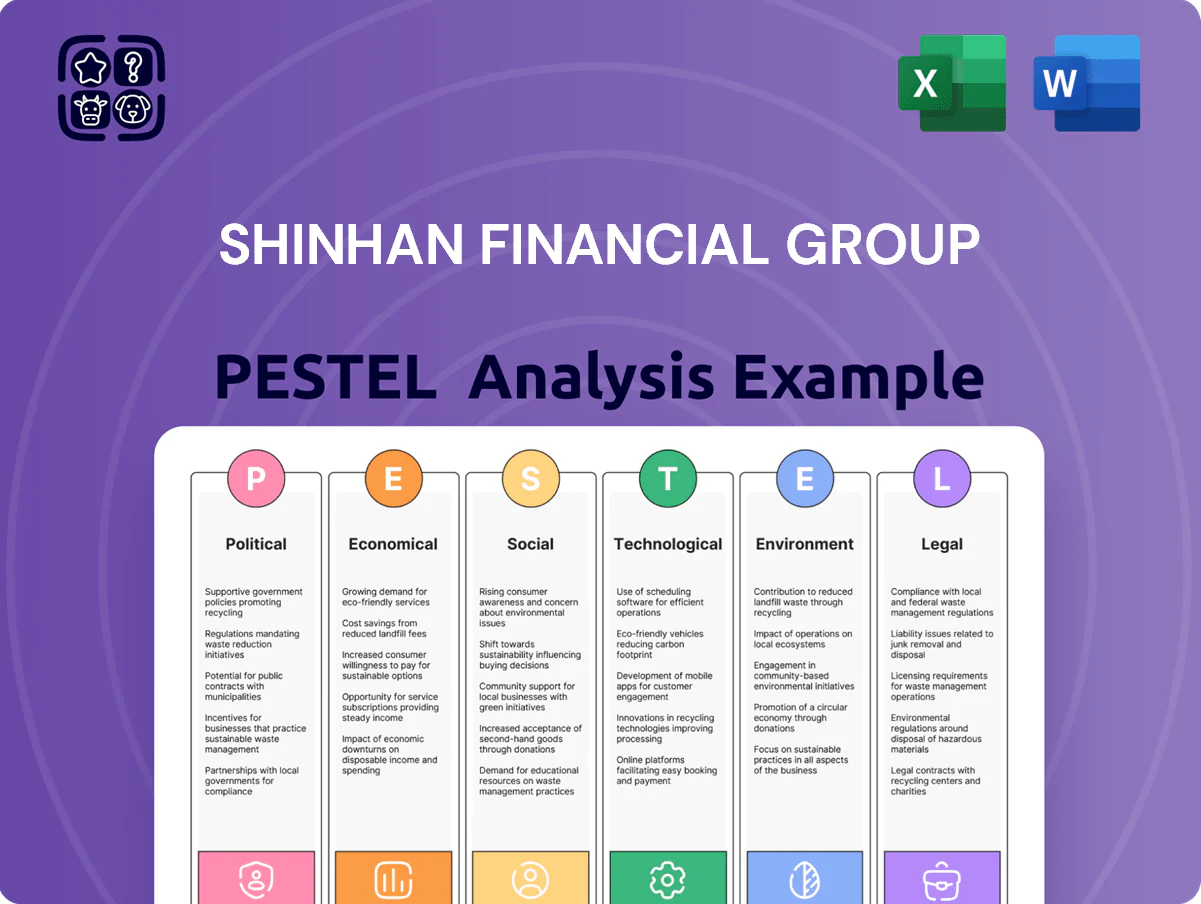

Explores how external macro-environmental factors uniquely affect Shinhan Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary of Shinhan Financial Group that fits neatly into presentations or strategy packs, enabling quick cross-team alignment on regulatory, economic, and technological risks.

Economic factors

Interest Rate Environment and Net Interest Margin

The Bank of Korea and US Fed rate moves are primary drivers of Shinhan Financial Group’s profitability; Korea’s policy rate rose from 0.50% in 2021 to 3.50% by end-2023 and hovered near 3.25–3.50% into 2024–25, while the Fed’s funds rate reached 5.25–5.50% in 2023–24, shaping funding costs. Net interest margin, 1.66% in 2023 for Shinhan Bank, is sensitive to such shifts, and by late 2025 a move to neutral rates forced active asset-liability management to protect spreads.

South Korean GDP Growth and Economic Health

Shinhan’s performance tracks South Korea GDP growth, which slowed to 1.6% in 2024 after 2.6% in 2023, with IMF projecting ~1.4% for 2025 amid an aging population and weak consumption; this dampens demand for corporate loans, mortgages and wealth products.

Inflationary Pressures and Operating Costs

Persistent inflation in South Korea — 3.7% in 2024 (KOSTAT) — raises Shinhan Financial Group’s operating costs and reduces retail clients’ disposable income, pressuring loan demand and fee income.

Wage growth and rising IT maintenance costs, with Korea’s average annual wage up ~4% in 2024, can squeeze margins unless offset by efficiency gains and automation.

High inflation erodes real value of AUM; Korean household financial assets growth slowed to 1.2% YoY in 2024, shifting client preferences toward inflation-hedged products and real assets.

Household Debt Levels and Credit Risk

- Household debt ~KRW 1,980 trillion (Q3 2025)

- Key metrics to watch: NPL ratio, stage 2 loans, DSR

- 0.2–0.4 pp NPL rise → notable net income/provision impact

Currency Exchange Rate Volatility

As a global financial player, Shinhan faces KRW volatility versus USD, JPY and VND; a 2024 KRW 6% swing vs USD would alter reported overseas asset values materially and compress consolidated net income.

Exchange moves change profitability of international units and can erode CET1 ratios—Shinhan reported 14.5% CET1 in 2024, so currency losses could meaningfully affect buffers.

Robust hedging and FX risk limits are therefore essential to protect capital adequacy and earnings stability.

- Exposure: USD, JPY, VND; 2024 KRW/USD volatility ~6%

- Capital: CET1 14.5% (2024)

- Hedge need: reduces P&L swings and protects consolidated ratios

Korea: Tight Rates, Slowing Growth and Rising Household Debt Squeeze Bank Margins

Economic drivers—policy rates (BOK ~3.25–3.50% in 2024–25; Fed 5.25–5.50% in 2023–24), GDP slowing to ~1.6% (2024) with IMF ~1.4% (2025), inflation 3.7% (2024), household debt ~KRW 1,980tn (Q3 2025), NIM 1.66% (2023) and CET1 14.5% (2024)—compress margins, raise credit risk and heighten FX sensitivity; monitor NPLs, Stage-2, DSR and hedge FX.

| Metric | Value |

|---|---|

| BOK rate | 3.25–3.50% |

| GDP | 1.6% (2024) |

| Inflation | 3.7% (2024) |

| Household debt | KRW 1,980tn (Q3 2025) |

| NIM | 1.66% (2023) |

| CET1 | 14.5% (2024) |

Same Document Delivered

Shinhan Financial Group PESTLE Analysis

The preview shown here is the exact Shinhan Financial Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Shinhan Financial Group pinpoints the regulatory shifts, macroeconomic pressures, and technological trends reshaping its strategy and risk profile—crucial intelligence for investors and strategists seeking a competitive edge. Purchase the full, ready-to-use report to access detailed, actionable insights and forecasts that save research time and power better decisions.

Political factors

South Korean Government Financial Policy

The South Korean government maintains strict oversight of the financial sector to ensure systemic stability and fair competition, with bank non-performing loan ratios held near 0.6% in 2025 to date. Throughout 2025 the Financial Services Commission pushed corporate value-up programs and higher shareholder returns, prompting Shinhan to target a CET1 ratio around 12.5% while boosting dividends and buybacks. Political leadership changes could quickly alter credit guidelines and mortgage caps, affecting loan growth and NIMs.

Geopolitical Tensions in the Korean Peninsula

Persistent tensions with North Korea keep investor risk aversion high, contributing to a 2025 surge in implied equity volatility for Korean banks—KOSPI bank index VIX rose ~28% during flare-ups—pressuring valuations of Shinhan Financial Group (market cap ₩24.3tr as of Jan 2026).

Escalations prompt capital flight risk: nonresident holdings of Korean equities dipped to 31.8% in 2024, raising Shinhan’s cost of funding and risking rating pressure; Moody’s and S&P monitor regional stability when assessing sovereign-linked credit spreads.

Shinhan must maintain robust contingency plans—liquidity buffers (LCR >100%), diversified funding, and crisis IRR management—to manage tail risks and protect capital adequacy (2025 CET1 ~12.1%).

Global Trade Relations and Protectionism

Shinhan Financial Group’s expansion in Southeast Asia and the US exposes it to global trade volatility and rising protectionism; US-China tariff tensions since 2018 have contributed to a 12-18% supply-chain cost increase for affected Korean exporters, raising corporate borrower stress. Trade disputes can alter clients’ revenue and working capital, shifting credit-risk models—Korean exporters saw non-performing loan ratios tick up 0.2–0.5 percentage points during major tariff episodes. Managing geopolitical risk is therefore critical to Shinhan’s overseas loan growth and capital allocation strategies.

Taxation Policies and Fiscal Reforms

Legislative shifts in corporate tax and financial transaction taxes directly affect Shinhan Financial Group’s net income; in 2024 South Korea’s effective corporate tax changes could alter Shinhan’s 2023 net profit KRW 4.2 trillion by several percentage points, impacting ROE and capital allocation.

Policy debates on wealth redistribution have driven proposals for bank windfall taxes and dividend tax hikes; increased dividend taxation reduces shareholder after-tax returns and may force Shinhan to retain earnings rather than distribute from its 2023 dividend payout ratio ~20%.

Such fiscal reforms constrain Shinhan’s ability to reinvest earnings into digital transformation and loan growth, affecting capital adequacy and shareholder value amidst a CET1 ratio around 13–14% in 2024.

- Corporate tax rate moves can swing net profit by multiple % points

- Windfall/dividend tax proposals pressure payout policies and retention

- Fiscal changes influence reinvestment, CET1, ROE, and shareholder returns

Government Social Responsibility Mandates

Political pressure keeps major banks like Shinhan tied to SME and vulnerable-population support; in 2024 Shinhan reported KRW 12.4 trillion in SME lending, reflecting government-driven priorities.

Shinhan is regularly expected to join government relief schemes and extend low-interest loans during downturns—its Household & SME loans rose 7.1% YoY in 2024 amid policy programs.

Executive leadership must balance these mandates with shareholder fiduciary duties as mandated programs can compress net interest margins (NIM 1.45% in 2024) and increase credit risk exposure.

- KRW 12.4T SME lending (2024)

- Household & SME loans +7.1% YoY (2024)

- NIM 1.45% (2024) highlights margin pressure

Shinhan faces political, fiscal and market shocks: CET1 12–13%, NIM 1.45%, KOSPI VIX +28%

Political oversight, geopolitical tensions, and fiscal policy materially shape Shinhan’s capital, funding and credit costs: 2024–25 CET1 ~12–13%, NIM 1.45% (2024), SME lending KRW12.4T (2024), nonresident equity share 31.8% (2024), KOSPI bank VIX spike ~28% (2025). Proposed tax/windfall measures and government relief mandates press payout policy and ROE.

| Metric | Value |

|---|---|

| CET1 | ~12–13% |

| NIM | 1.45% |

| SME lending | KRW12.4T |

| Nonresident equity | 31.8% |

| KOSPI bank VIX move | ~+28% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Shinhan Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary of Shinhan Financial Group that fits neatly into presentations or strategy packs, enabling quick cross-team alignment on regulatory, economic, and technological risks.

Economic factors

Interest Rate Environment and Net Interest Margin

The Bank of Korea and US Fed rate moves are primary drivers of Shinhan Financial Group’s profitability; Korea’s policy rate rose from 0.50% in 2021 to 3.50% by end-2023 and hovered near 3.25–3.50% into 2024–25, while the Fed’s funds rate reached 5.25–5.50% in 2023–24, shaping funding costs. Net interest margin, 1.66% in 2023 for Shinhan Bank, is sensitive to such shifts, and by late 2025 a move to neutral rates forced active asset-liability management to protect spreads.

South Korean GDP Growth and Economic Health

Shinhan’s performance tracks South Korea GDP growth, which slowed to 1.6% in 2024 after 2.6% in 2023, with IMF projecting ~1.4% for 2025 amid an aging population and weak consumption; this dampens demand for corporate loans, mortgages and wealth products.

Inflationary Pressures and Operating Costs

Persistent inflation in South Korea — 3.7% in 2024 (KOSTAT) — raises Shinhan Financial Group’s operating costs and reduces retail clients’ disposable income, pressuring loan demand and fee income.

Wage growth and rising IT maintenance costs, with Korea’s average annual wage up ~4% in 2024, can squeeze margins unless offset by efficiency gains and automation.

High inflation erodes real value of AUM; Korean household financial assets growth slowed to 1.2% YoY in 2024, shifting client preferences toward inflation-hedged products and real assets.

Household Debt Levels and Credit Risk

- Household debt ~KRW 1,980 trillion (Q3 2025)

- Key metrics to watch: NPL ratio, stage 2 loans, DSR

- 0.2–0.4 pp NPL rise → notable net income/provision impact

Currency Exchange Rate Volatility

As a global financial player, Shinhan faces KRW volatility versus USD, JPY and VND; a 2024 KRW 6% swing vs USD would alter reported overseas asset values materially and compress consolidated net income.

Exchange moves change profitability of international units and can erode CET1 ratios—Shinhan reported 14.5% CET1 in 2024, so currency losses could meaningfully affect buffers.

Robust hedging and FX risk limits are therefore essential to protect capital adequacy and earnings stability.

- Exposure: USD, JPY, VND; 2024 KRW/USD volatility ~6%

- Capital: CET1 14.5% (2024)

- Hedge need: reduces P&L swings and protects consolidated ratios

Korea: Tight Rates, Slowing Growth and Rising Household Debt Squeeze Bank Margins

Economic drivers—policy rates (BOK ~3.25–3.50% in 2024–25; Fed 5.25–5.50% in 2023–24), GDP slowing to ~1.6% (2024) with IMF ~1.4% (2025), inflation 3.7% (2024), household debt ~KRW 1,980tn (Q3 2025), NIM 1.66% (2023) and CET1 14.5% (2024)—compress margins, raise credit risk and heighten FX sensitivity; monitor NPLs, Stage-2, DSR and hedge FX.

| Metric | Value |

|---|---|

| BOK rate | 3.25–3.50% |

| GDP | 1.6% (2024) |

| Inflation | 3.7% (2024) |

| Household debt | KRW 1,980tn (Q3 2025) |

| NIM | 1.66% (2023) |

| CET1 | 14.5% (2024) |

Same Document Delivered

Shinhan Financial Group PESTLE Analysis

The preview shown here is the exact Shinhan Financial Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.