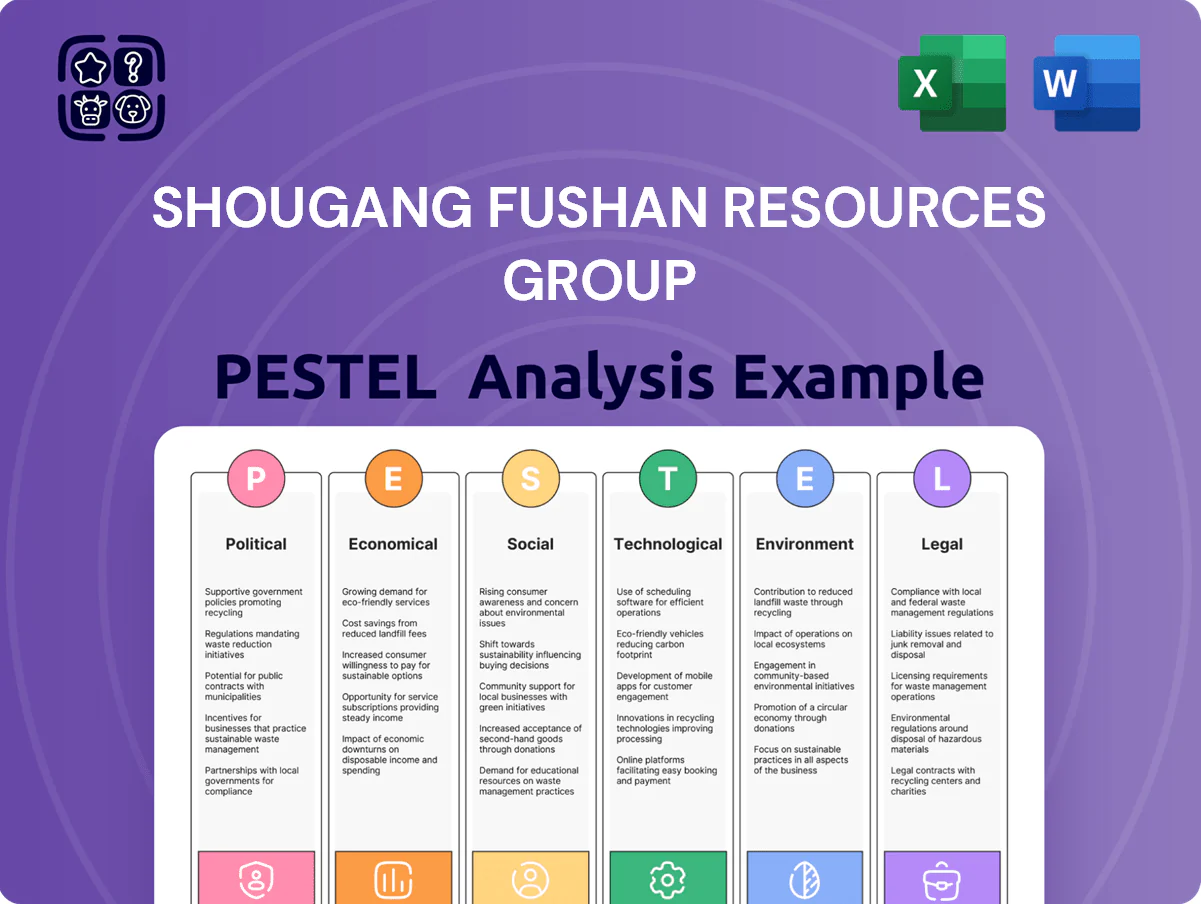

Shougang Fushan Resources Group PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE snapshot reveals how regulatory shifts, commodity cycles, and environmental pressures shape Shougang Fushan Resources Group's strategic risks and opportunities—vital intel for investors and planners. Gain clarity on policy exposure, market trends, and tech risks to refine forecasts and strategic moves. Purchase the full PESTLE for a complete, editable report with actionable insights and immediate download.

Political factors

Centralized Energy Policy Alignment

As of late 2025 Shougang Fushan operates under tight state control: Beijing set 2025 national coal output guidance at about 4.1 billion tonnes, with coking coal quotas closely managed to safeguard steel feedstock, forcing Shougang Fushan to align production to quota ceilings to retain licenses; failure risks fines or curtailment, and in 2024 the group reported coking coal sales contributing ~62% of revenue (RMB 8.9bn of RMB 14.4bn), underscoring political leverage over its operations.

Geopolitical Trade Relations

Geopolitical trade dynamics between China and major coal exporters like Australia and Mongolia affect Shougang Fushan via price and demand shifts; China imported 191 Mt of thermal and coking coal in 2023, with Australia and Mongolia key suppliers, driving spot coking coal prices that impact margins.

Diplomatic shifts can trigger tariffs or bans—e.g., 2021–2023 trade frictions saw intermittent restrictions—raising risk of abrupt import cost swings that alter domestic coking coal competitiveness.

To mitigate, Shougang Fushan must strengthen domestic supply chains and leverage state-backed partnerships; state-backed domestic coal accounted for a growing share of coking coal supply in 2024–2025, supporting price stability and supply security.

State Ownership and Influence

The group’s linkage to state-owned Shougang Group grants political protection and easier access to capital—Shougang Group’s 2024 reported assets exceeded RMB 300 billion—facilitating participation in large-scale infrastructure and state mining projects. This affiliation can also impose political mandates, such as employment stability and strategic resource allocation, which may reduce short-term margins. Management must balance commercial returns with national industrial-stability objectives when planning investments and dividends.

Regional Governance in Shanxi

Operations concentrated in Shanxi mean Shougang Fushan faces provincial political stability and mining regulations; Shanxi reported 2024 coal output of 1.12 billion tonnes, making regulatory shifts material to revenue and operations.

Local initiatives on mine safety, land reclamation and rural development—where provincial budgets earmarked RMB 14.6 billion for mine closures and land rehab in 2024—require coordination and recurring financial contributions.

Changes in provincial leadership can alter enforcement intensity or introduce local taxes; Shanxi added temporary levies affecting coal miners in 2023 that raised effective tax rates by ~1.2 percentage points.

- Concentration risk: Shanxi = core regulatory exposure

- 2024 coal output 1.12bn t highlights scale

- RMB 14.6bn provincial rehab budget drives obligations

- Leadership changes can shift enforcement and taxes (+1.2pp impact observed)

Industrial Consolidation Mandates

Chinese policy since 2016 has targeted coal consolidation; Beijing aims to cut capacity and close inefficient mines, reducing provincial coal firms by over 30% in some regions by 2024, favoring large operators for safety and efficiency improvements.

Shougang Fushan, with 2024 coal output ~23 Mt and improved margins from scale, is often positioned to acquire distressed smaller mines under local government encouragement, expanding market share.

- Government push reduces small competitors (~30% regional declines by 2024)

- Shougang Fushan 2024 output ≈23 Mt aids acquisitions

- Policy favors safety, efficiency—benefits large operators

Shougang Fushan: Capacity Caps, Political Mandates and Strong Group Backing

State quotas and Beijing’s 2025 coal guidance (≈4.1bn t) tightly constrain Shougang Fushan (2024 coking coal revenue RMB 8.9bn; output ≈23Mt), while Shanxi’s 2024 output (1.12bn t) and provincial rehab budget (RMB 14.6bn) drive regulatory obligations; affiliation with Shougang Group (2024 assets >RMB 300bn) eases capital access but imposes political mandates.

| Metric | 2024/2025 |

|---|---|

| National coal guidance | ≈4.1bn t (2025) |

| Shougang Fushan output | ≈23 Mt (2024) |

| Coking coal revenue | RMB 8.9bn (2024) |

| Shanxi output | 1.12bn t (2024) |

| Provincial rehab budget | RMB 14.6bn (2024) |

| Shougang Group assets | >RMB 300bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Shougang Fushan Resources Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, investors, and consultants identify industry-specific risks and opportunities and inform strategic planning.

A compact PESTLE snapshot of Shougang Fushan Resources Group, formatted for quick team alignment and presentations, highlighting key political, economic, social, technological, legal, and environmental risks and opportunities to streamline external-risk discussions and strategic planning.

Economic factors

Steel Industry Demand Cycles

Demand for coking coal for Shougang Fushan closely tracked steel output; global steel production fell 0.4% in 2025 to 1.76 billion tonnes, and China’s crude steel slipped 1.2% Y/Y to ~1.02 billion tonnes, pressuring coking coal prices which declined ~15% in 2025; a real estate slowdown (China new home starts down ~12% in 2025) cut steel consumption, while announced 2025–26 infrastructure stimulus totaling ~RMB 2.5 trillion could lift metallurgical coal demand and margins.

Commodity Price Volatility

Fluctuations in global coking coal prices—which averaged about USD 220–260/tonne in 2024 after peaking near USD 320/tonne in 2022—directly squeeze Shougang Fushan’s margins and cash flow forecasts given its cost structure. As a price taker, the group is exposed to downside from oversupply or weaker steel demand; a 10% international price drop can cut EBITDA materially. Investors should track the China premium/discount versus global index (China FOB ~USD 20–40/tonne below seaborne in 2024) to gauge competitive position.

Cost of Capital and Inflation

Rising inflation in 2024–25 has pushed labor, machinery and electricity input costs up about 4–6% y/y, risking margin compression for Shougang Fushan if thermal coal prices, which averaged RMB 740/ton in 2024, do not rise similarly.

State-linked status helps secure lower-cost loans—China policy bank yields averaged 3.1% in 2025—but benchmark lending rates and PBOC tightening affect debt servicing and capex timelines.

Heavy-equipment replacement and specialized mining tech capex remain material: global mining equipment prices rose ~5% in 2024, making cost control critical for expansion plans.

Currency Exchange Rate Risks

Fluctuations in the RMB/USD affect Shougang Fushan by raising costs for imported mining equipment and increasing US-dollar debt servicing—China FX reserves fell to about $3.05 trillion in 2025, pressuring policy flexibility.

A weaker RMB lowers the landed cost of imported coal relative to domestic coal, but when RMB weakens domestic coal becomes more price-competitive for local steel mills, supporting Shougang Fushan volumes.

- Imported equipment and FX debt exposure

- RMB moves alter imported vs domestic coal pricing

- 2025 FX reserves ~ $3.05 trillion signal policy constraints

Infrastructure and Logistics Costs

The company’s unit economics hinge on transport costs; rail freight for coal in China averaged about 0.04–0.06 CNY/ton·km in 2024, so shorter haul distances from Shanxi mines materially lower per-ton costs versus national averages.

Recent state investments—2023–25 rail capacity expansions adding ~2,000 km—can cut logistics spend, while diesel and electricity price volatility (up to 15% year-on-year in 2024) raises risk.

Proximity to major transport arteries in Shanxi reduces average haul distances and buffer against bottlenecks, improving margins and resilience to national energy cost swings.

- Rail freight ~0.04–0.06 CNY/ton·km (2024)

- National rail expansions +~2,000 km (2023–25)

- Energy price volatility up to 15% YoY (2024)

- Shanxi proximity lowers average haul and logistics risk

China steel slump cuts coking coal demand; costs up as RMB weakens

China steel slump (crude steel -1.2% to ~1.02bn t in 2025) cut coking coal demand; 2025 coking prices fell ~15% after 2024 avg USD 220–260/t. Inflation pushed input costs +4–6% (2024–25); rail freight ~0.04–0.06 CNY/ton·km (2024). RMB weakness and FX reserves ~USD 3.05tn (2025) affect imported equipment costs and USD debt servicing.

| Metric | Value |

|---|---|

| Crude steel 2025 | ~1.02bn t (-1.2%) |

| Coking coal price 2025 | -15% (2025); 2024 avg USD 220–260/t |

| Input cost inflation | +4–6% (2024–25) |

| Rail freight | 0.04–0.06 CNY/ton·km (2024) |

| China FX reserves | ~USD 3.05tn (2025) |

Preview the Actual Deliverable

Shougang Fushan Resources Group PESTLE Analysis

The preview shown here is the exact Shougang Fushan Resources Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, final file you’ll be able to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Our PESTLE snapshot reveals how regulatory shifts, commodity cycles, and environmental pressures shape Shougang Fushan Resources Group's strategic risks and opportunities—vital intel for investors and planners. Gain clarity on policy exposure, market trends, and tech risks to refine forecasts and strategic moves. Purchase the full PESTLE for a complete, editable report with actionable insights and immediate download.

Political factors

Centralized Energy Policy Alignment

As of late 2025 Shougang Fushan operates under tight state control: Beijing set 2025 national coal output guidance at about 4.1 billion tonnes, with coking coal quotas closely managed to safeguard steel feedstock, forcing Shougang Fushan to align production to quota ceilings to retain licenses; failure risks fines or curtailment, and in 2024 the group reported coking coal sales contributing ~62% of revenue (RMB 8.9bn of RMB 14.4bn), underscoring political leverage over its operations.

Geopolitical Trade Relations

Geopolitical trade dynamics between China and major coal exporters like Australia and Mongolia affect Shougang Fushan via price and demand shifts; China imported 191 Mt of thermal and coking coal in 2023, with Australia and Mongolia key suppliers, driving spot coking coal prices that impact margins.

Diplomatic shifts can trigger tariffs or bans—e.g., 2021–2023 trade frictions saw intermittent restrictions—raising risk of abrupt import cost swings that alter domestic coking coal competitiveness.

To mitigate, Shougang Fushan must strengthen domestic supply chains and leverage state-backed partnerships; state-backed domestic coal accounted for a growing share of coking coal supply in 2024–2025, supporting price stability and supply security.

State Ownership and Influence

The group’s linkage to state-owned Shougang Group grants political protection and easier access to capital—Shougang Group’s 2024 reported assets exceeded RMB 300 billion—facilitating participation in large-scale infrastructure and state mining projects. This affiliation can also impose political mandates, such as employment stability and strategic resource allocation, which may reduce short-term margins. Management must balance commercial returns with national industrial-stability objectives when planning investments and dividends.

Regional Governance in Shanxi

Operations concentrated in Shanxi mean Shougang Fushan faces provincial political stability and mining regulations; Shanxi reported 2024 coal output of 1.12 billion tonnes, making regulatory shifts material to revenue and operations.

Local initiatives on mine safety, land reclamation and rural development—where provincial budgets earmarked RMB 14.6 billion for mine closures and land rehab in 2024—require coordination and recurring financial contributions.

Changes in provincial leadership can alter enforcement intensity or introduce local taxes; Shanxi added temporary levies affecting coal miners in 2023 that raised effective tax rates by ~1.2 percentage points.

- Concentration risk: Shanxi = core regulatory exposure

- 2024 coal output 1.12bn t highlights scale

- RMB 14.6bn provincial rehab budget drives obligations

- Leadership changes can shift enforcement and taxes (+1.2pp impact observed)

Industrial Consolidation Mandates

Chinese policy since 2016 has targeted coal consolidation; Beijing aims to cut capacity and close inefficient mines, reducing provincial coal firms by over 30% in some regions by 2024, favoring large operators for safety and efficiency improvements.

Shougang Fushan, with 2024 coal output ~23 Mt and improved margins from scale, is often positioned to acquire distressed smaller mines under local government encouragement, expanding market share.

- Government push reduces small competitors (~30% regional declines by 2024)

- Shougang Fushan 2024 output ≈23 Mt aids acquisitions

- Policy favors safety, efficiency—benefits large operators

Shougang Fushan: Capacity Caps, Political Mandates and Strong Group Backing

State quotas and Beijing’s 2025 coal guidance (≈4.1bn t) tightly constrain Shougang Fushan (2024 coking coal revenue RMB 8.9bn; output ≈23Mt), while Shanxi’s 2024 output (1.12bn t) and provincial rehab budget (RMB 14.6bn) drive regulatory obligations; affiliation with Shougang Group (2024 assets >RMB 300bn) eases capital access but imposes political mandates.

| Metric | 2024/2025 |

|---|---|

| National coal guidance | ≈4.1bn t (2025) |

| Shougang Fushan output | ≈23 Mt (2024) |

| Coking coal revenue | RMB 8.9bn (2024) |

| Shanxi output | 1.12bn t (2024) |

| Provincial rehab budget | RMB 14.6bn (2024) |

| Shougang Group assets | >RMB 300bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Shougang Fushan Resources Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, investors, and consultants identify industry-specific risks and opportunities and inform strategic planning.

A compact PESTLE snapshot of Shougang Fushan Resources Group, formatted for quick team alignment and presentations, highlighting key political, economic, social, technological, legal, and environmental risks and opportunities to streamline external-risk discussions and strategic planning.

Economic factors

Steel Industry Demand Cycles

Demand for coking coal for Shougang Fushan closely tracked steel output; global steel production fell 0.4% in 2025 to 1.76 billion tonnes, and China’s crude steel slipped 1.2% Y/Y to ~1.02 billion tonnes, pressuring coking coal prices which declined ~15% in 2025; a real estate slowdown (China new home starts down ~12% in 2025) cut steel consumption, while announced 2025–26 infrastructure stimulus totaling ~RMB 2.5 trillion could lift metallurgical coal demand and margins.

Commodity Price Volatility

Fluctuations in global coking coal prices—which averaged about USD 220–260/tonne in 2024 after peaking near USD 320/tonne in 2022—directly squeeze Shougang Fushan’s margins and cash flow forecasts given its cost structure. As a price taker, the group is exposed to downside from oversupply or weaker steel demand; a 10% international price drop can cut EBITDA materially. Investors should track the China premium/discount versus global index (China FOB ~USD 20–40/tonne below seaborne in 2024) to gauge competitive position.

Cost of Capital and Inflation

Rising inflation in 2024–25 has pushed labor, machinery and electricity input costs up about 4–6% y/y, risking margin compression for Shougang Fushan if thermal coal prices, which averaged RMB 740/ton in 2024, do not rise similarly.

State-linked status helps secure lower-cost loans—China policy bank yields averaged 3.1% in 2025—but benchmark lending rates and PBOC tightening affect debt servicing and capex timelines.

Heavy-equipment replacement and specialized mining tech capex remain material: global mining equipment prices rose ~5% in 2024, making cost control critical for expansion plans.

Currency Exchange Rate Risks

Fluctuations in the RMB/USD affect Shougang Fushan by raising costs for imported mining equipment and increasing US-dollar debt servicing—China FX reserves fell to about $3.05 trillion in 2025, pressuring policy flexibility.

A weaker RMB lowers the landed cost of imported coal relative to domestic coal, but when RMB weakens domestic coal becomes more price-competitive for local steel mills, supporting Shougang Fushan volumes.

- Imported equipment and FX debt exposure

- RMB moves alter imported vs domestic coal pricing

- 2025 FX reserves ~ $3.05 trillion signal policy constraints

Infrastructure and Logistics Costs

The company’s unit economics hinge on transport costs; rail freight for coal in China averaged about 0.04–0.06 CNY/ton·km in 2024, so shorter haul distances from Shanxi mines materially lower per-ton costs versus national averages.

Recent state investments—2023–25 rail capacity expansions adding ~2,000 km—can cut logistics spend, while diesel and electricity price volatility (up to 15% year-on-year in 2024) raises risk.

Proximity to major transport arteries in Shanxi reduces average haul distances and buffer against bottlenecks, improving margins and resilience to national energy cost swings.

- Rail freight ~0.04–0.06 CNY/ton·km (2024)

- National rail expansions +~2,000 km (2023–25)

- Energy price volatility up to 15% YoY (2024)

- Shanxi proximity lowers average haul and logistics risk

China steel slump cuts coking coal demand; costs up as RMB weakens

China steel slump (crude steel -1.2% to ~1.02bn t in 2025) cut coking coal demand; 2025 coking prices fell ~15% after 2024 avg USD 220–260/t. Inflation pushed input costs +4–6% (2024–25); rail freight ~0.04–0.06 CNY/ton·km (2024). RMB weakness and FX reserves ~USD 3.05tn (2025) affect imported equipment costs and USD debt servicing.

| Metric | Value |

|---|---|

| Crude steel 2025 | ~1.02bn t (-1.2%) |

| Coking coal price 2025 | -15% (2025); 2024 avg USD 220–260/t |

| Input cost inflation | +4–6% (2024–25) |

| Rail freight | 0.04–0.06 CNY/ton·km (2024) |

| China FX reserves | ~USD 3.05tn (2025) |

Preview the Actual Deliverable

Shougang Fushan Resources Group PESTLE Analysis

The preview shown here is the exact Shougang Fushan Resources Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers—this is the real, final file you’ll be able to download immediately after payment.