Sidley Austin Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Sidley Austin operates in a highly competitive legal market where client bargaining power, rivalry among elite firms, and regulatory shifts shape profitability; supplier influence and substitutes like boutique specialists add pressure while scale and reputation provide defense. This snapshot highlights key tensions but skips force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to gain a consultant-grade breakdown and actionable insights for strategy or investment.

Suppliers Bargaining Power

Scarcity of elite legal talent

The primary suppliers for Sidley Austin are elite attorneys and specialized legal professionals, and by late 2025 competition for graduates from top 14 law schools kept partner/associate leverage high; average first-year associate starting pay at AmLaw firms hit roughly $215,000 in 2025, pushing Sidley’s labor costs up and creating a high-cost structure to retain prestige and service quality.

Legal technology and AI vendors

Providers of AI-driven legal research and practice-management tools wield growing supplier power as firms rely on these systems for efficiency; the global legal AI market reached $3.7 billion in 2024 and is projected to hit $8.2 billion by 2030, concentrating leverage with a few major vendors.

Large-scale legal language model providers form a concentrated supplier group—OpenAI, Google, and specialized players like Casetext and ROSS—driving pricing and feature roadmaps that affect costs and capabilities.

To stay competitive in data-heavy litigation and transactional work, Sidley Austin must invest in partnerships and integrations; a conservative estimate: enterprise AI licensing and integration could require $10–30 million over three years for a firm of Sidley’s scale.

Real estate and office space providers

For Sidley Austin, landlords in prime hubs (New York, London, Hong Kong) hold moderate bargaining power because premium addresses matter for client meetings and reputation; Midtown Manhattan and Canary Wharf vacancy rates were ~7.5% and 11% in Q4 2024, shaping lease leverage. Hybrid work cut office demand—global office occupancy averaged ~55% in 2024—so supplier power eased versus pre-2020 levels.

Specialized expert witnesses and consultants

Specialized expert witnesses and economic consultants hold strong supplier power for Sidley Austin in complex litigation and regulatory work; a 2024 ALM survey found 62% of Big Law firms reported limited expert availability in key specialties.

Their scarce, case‑critical expertise lets them command high fees—often $500–1,200/hour for top econometricians—making them indispensable to specific practice groups and increasing client cost exposure.

- 62% of firms report limited expert supply

- Top expert rates $500–1,200/hour

- Experts pivotal in high‑stakes outcomes

Accreditation and regulatory bodies

Bar associations and global regulators supply Sidley Austin’s license to operate by setting practice standards and compliance rules; in 2024, ABA model rules influenced 18% of major US firms’ remote-work policies, forcing firm-wide policy changes.

Though not commercial suppliers, their authority to revise ethics requirements or cross-border practice rules compels Sidley to adapt staffing, supervision, and fee arrangements.

This creates a non-negotiable supply-side constraint: regulatory changes can increase compliance costs—estimated at 2–4% of revenue for top 100 firms in 2023—and limit service models.

- License-holder: bar/regulators set standards

- Rule changes force ops shifts

- Compliance costs ~2–4% revenue (2023)

- 18% remote-work policy impact (2024)

Suppliers Squeeze Sidley: Rising lawyer pay, legal‑AI prices, expert rates, and compliance costs

Suppliers wield moderate-to-strong power: elite attorneys push labor costs (AmLaw 1L pay ~$215,000 in 2025), AI/legal‑tech vendors concentrate pricing (legal AI market $3.7B in 2024), expert witnesses command $500–1,200/hr, and regulators force compliance (~2–4% revenue); combined, these raise operating costs and limit pricing flexibility for Sidley Austin.

| Supplier | Key Metric | 2024–25 Data |

|---|---|---|

| Elite attorneys | 1L pay | $215,000 (AmLaw avg, 2025) |

| Legal AI market | Market size | $3.7B (2024) |

| Expert witnesses | Rates | $500–1,200/hr (2024) |

| Regulators | Compliance cost | 2–4% revenue (2023) |

What is included in the product

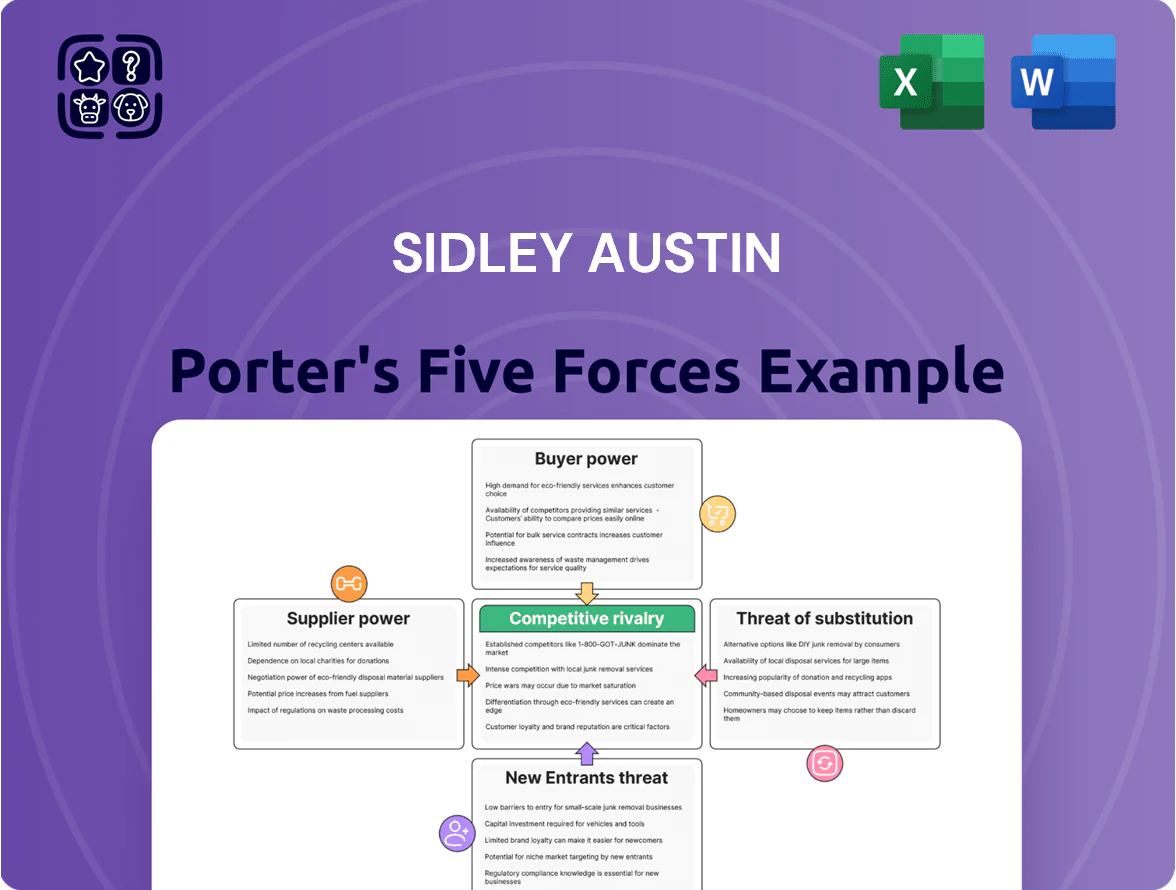

Tailored exclusively for Sidley Austin, this Porter's Five Forces overview uncovers competitive pressures, client bargaining power, supplier dynamics, potential new entrants, and substitutes impacting its profitability and market position.

Sidley Austin Porter's Five Forces one-sheet pinpoints competitive pressures and strategic levers instantly—ideal for rapid decision-making and slide-ready summaries.

Customers Bargaining Power

Concentration of institutional clients

Sidley Austin serves large multinationals and financial firms whose concentrated demand gives them outsized leverage—top 20 clients can account for an estimated 25–40% of revenue in BigLaw peers, so similar dynamics likely apply. These buyers use procurement teams to push alternative fee arrangements (AFAs) over hourly rates; in 2024, 34% of corporate legal spend shifted to AFAs. The firm must prove measurable efficiency and value to retain these clients.

Low switching costs for non-specialized work

While switching mid-litigation is hard, clients freely move general corporate work among elite firms; 2024 Am Law data shows top 100 firms overlap on 68% of corporate deals, so Sidley Austin faces constant poaching pressure.

The abundance of White Shoe and Magic Circle peers forces Sidley to prove superior outcomes; client churn risk rises if win rates drop below firm average—Sidley’s 2023 partner-originated revenue growth was 6.8%, so pricing remains sensitive even for wealthy corporates.

Growth of sophisticated in-house legal teams

By end-2025, roughly 60% of Fortune 500 clients expanded in-house legal teams, letting them handle routine M&A due diligence and contract work and tightly manage outside counsel, per Deloitte 2025 Legal Ops Survey; Sidley Austin faces unbundling as clients retain high-margin strategy and litigation oversight while outsourcing only complex cross-border cases, cutting billable-hours dependency and pressuring fees and margins.

Demand for alternative fee arrangements

Clients increasingly prefer fixed, success, or capped fees over billable hours; 2024 Altman Weil survey found 58% of corporate legal departments use alternative fee arrangements (AFAs), up from 43% in 2019.

This shift gives buyers control of legal spend and transparency, shifting inefficiency risk to Sidley and pressuring margins; AFAs now represent ~20% of large-firm revenue per 2023 ILTA data.

Sidley must upgrade project management, staffing mix, and pricing models to protect realization and predictability while meeting buyer demands.

- 58% of legal depts use AFAs (Altman Weil 2024)

- AFAs ≈20% of large-firm revenue (ILTA 2023)

- Risk shifts to firm; requires tighter project management

Information transparency and performance benchmarking

Information transparency—public win-rate datasets and diversity reports—lets clients compare Sidley Austin’s case outcomes and lawyer utilization against rivals; 2024 ALM data shows top firms’ median litigation win rates varying by 10–15 percentage points, sharpening comparisons.

Clients use data platforms to benchmark Sidley on efficiency and cost-per-matter; procurement teams demand fee caps or KPIs when metrics lag peers, raising buyer leverage.

- 2024 ALM: peer win-rate spread 10–15%

- Clients push KPIs: turnaround, cost-per-matter, diversity

- Transparency strengthens concession and fee negotiation

Big clients, fixed fees, in-house growth: escalating revenue risk and bargaining power

Large corporate clients hold strong leverage: top-client concentration likely 25–40% of revenue; 58% use AFAs (Altman Weil 2024); AFAs ≈20% of large-firm revenue (ILTA 2023); 60% of Fortune 500 expanded in-house legal by end-2025 (Deloitte 2025), pushing unbundling and fee pressure; peer win-rate spread 10–15% (ALM 2024), raising benchmarking-driven bargaining power.

| Metric | Value | Source |

|---|---|---|

| Top-client rev share | 25–40% | BigLaw peers |

| AFAs adoption | 58% | Altman Weil 2024 |

| AFAs share of revenue | ≈20% | ILTA 2023 |

| In-house growth | 60% by end-2025 | Deloitte 2025 |

| Win-rate spread | 10–15 pp | ALM 2024 |

Preview the Actual Deliverable

Sidley Austin Porter's Five Forces Analysis

This preview shows the exact Sidley Austin Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Sidley Austin operates in a highly competitive legal market where client bargaining power, rivalry among elite firms, and regulatory shifts shape profitability; supplier influence and substitutes like boutique specialists add pressure while scale and reputation provide defense. This snapshot highlights key tensions but skips force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to gain a consultant-grade breakdown and actionable insights for strategy or investment.

Suppliers Bargaining Power

Scarcity of elite legal talent

The primary suppliers for Sidley Austin are elite attorneys and specialized legal professionals, and by late 2025 competition for graduates from top 14 law schools kept partner/associate leverage high; average first-year associate starting pay at AmLaw firms hit roughly $215,000 in 2025, pushing Sidley’s labor costs up and creating a high-cost structure to retain prestige and service quality.

Legal technology and AI vendors

Providers of AI-driven legal research and practice-management tools wield growing supplier power as firms rely on these systems for efficiency; the global legal AI market reached $3.7 billion in 2024 and is projected to hit $8.2 billion by 2030, concentrating leverage with a few major vendors.

Large-scale legal language model providers form a concentrated supplier group—OpenAI, Google, and specialized players like Casetext and ROSS—driving pricing and feature roadmaps that affect costs and capabilities.

To stay competitive in data-heavy litigation and transactional work, Sidley Austin must invest in partnerships and integrations; a conservative estimate: enterprise AI licensing and integration could require $10–30 million over three years for a firm of Sidley’s scale.

Real estate and office space providers

For Sidley Austin, landlords in prime hubs (New York, London, Hong Kong) hold moderate bargaining power because premium addresses matter for client meetings and reputation; Midtown Manhattan and Canary Wharf vacancy rates were ~7.5% and 11% in Q4 2024, shaping lease leverage. Hybrid work cut office demand—global office occupancy averaged ~55% in 2024—so supplier power eased versus pre-2020 levels.

Specialized expert witnesses and consultants

Specialized expert witnesses and economic consultants hold strong supplier power for Sidley Austin in complex litigation and regulatory work; a 2024 ALM survey found 62% of Big Law firms reported limited expert availability in key specialties.

Their scarce, case‑critical expertise lets them command high fees—often $500–1,200/hour for top econometricians—making them indispensable to specific practice groups and increasing client cost exposure.

- 62% of firms report limited expert supply

- Top expert rates $500–1,200/hour

- Experts pivotal in high‑stakes outcomes

Accreditation and regulatory bodies

Bar associations and global regulators supply Sidley Austin’s license to operate by setting practice standards and compliance rules; in 2024, ABA model rules influenced 18% of major US firms’ remote-work policies, forcing firm-wide policy changes.

Though not commercial suppliers, their authority to revise ethics requirements or cross-border practice rules compels Sidley to adapt staffing, supervision, and fee arrangements.

This creates a non-negotiable supply-side constraint: regulatory changes can increase compliance costs—estimated at 2–4% of revenue for top 100 firms in 2023—and limit service models.

- License-holder: bar/regulators set standards

- Rule changes force ops shifts

- Compliance costs ~2–4% revenue (2023)

- 18% remote-work policy impact (2024)

Suppliers Squeeze Sidley: Rising lawyer pay, legal‑AI prices, expert rates, and compliance costs

Suppliers wield moderate-to-strong power: elite attorneys push labor costs (AmLaw 1L pay ~$215,000 in 2025), AI/legal‑tech vendors concentrate pricing (legal AI market $3.7B in 2024), expert witnesses command $500–1,200/hr, and regulators force compliance (~2–4% revenue); combined, these raise operating costs and limit pricing flexibility for Sidley Austin.

| Supplier | Key Metric | 2024–25 Data |

|---|---|---|

| Elite attorneys | 1L pay | $215,000 (AmLaw avg, 2025) |

| Legal AI market | Market size | $3.7B (2024) |

| Expert witnesses | Rates | $500–1,200/hr (2024) |

| Regulators | Compliance cost | 2–4% revenue (2023) |

What is included in the product

Tailored exclusively for Sidley Austin, this Porter's Five Forces overview uncovers competitive pressures, client bargaining power, supplier dynamics, potential new entrants, and substitutes impacting its profitability and market position.

Sidley Austin Porter's Five Forces one-sheet pinpoints competitive pressures and strategic levers instantly—ideal for rapid decision-making and slide-ready summaries.

Customers Bargaining Power

Concentration of institutional clients

Sidley Austin serves large multinationals and financial firms whose concentrated demand gives them outsized leverage—top 20 clients can account for an estimated 25–40% of revenue in BigLaw peers, so similar dynamics likely apply. These buyers use procurement teams to push alternative fee arrangements (AFAs) over hourly rates; in 2024, 34% of corporate legal spend shifted to AFAs. The firm must prove measurable efficiency and value to retain these clients.

Low switching costs for non-specialized work

While switching mid-litigation is hard, clients freely move general corporate work among elite firms; 2024 Am Law data shows top 100 firms overlap on 68% of corporate deals, so Sidley Austin faces constant poaching pressure.

The abundance of White Shoe and Magic Circle peers forces Sidley to prove superior outcomes; client churn risk rises if win rates drop below firm average—Sidley’s 2023 partner-originated revenue growth was 6.8%, so pricing remains sensitive even for wealthy corporates.

Growth of sophisticated in-house legal teams

By end-2025, roughly 60% of Fortune 500 clients expanded in-house legal teams, letting them handle routine M&A due diligence and contract work and tightly manage outside counsel, per Deloitte 2025 Legal Ops Survey; Sidley Austin faces unbundling as clients retain high-margin strategy and litigation oversight while outsourcing only complex cross-border cases, cutting billable-hours dependency and pressuring fees and margins.

Demand for alternative fee arrangements

Clients increasingly prefer fixed, success, or capped fees over billable hours; 2024 Altman Weil survey found 58% of corporate legal departments use alternative fee arrangements (AFAs), up from 43% in 2019.

This shift gives buyers control of legal spend and transparency, shifting inefficiency risk to Sidley and pressuring margins; AFAs now represent ~20% of large-firm revenue per 2023 ILTA data.

Sidley must upgrade project management, staffing mix, and pricing models to protect realization and predictability while meeting buyer demands.

- 58% of legal depts use AFAs (Altman Weil 2024)

- AFAs ≈20% of large-firm revenue (ILTA 2023)

- Risk shifts to firm; requires tighter project management

Information transparency and performance benchmarking

Information transparency—public win-rate datasets and diversity reports—lets clients compare Sidley Austin’s case outcomes and lawyer utilization against rivals; 2024 ALM data shows top firms’ median litigation win rates varying by 10–15 percentage points, sharpening comparisons.

Clients use data platforms to benchmark Sidley on efficiency and cost-per-matter; procurement teams demand fee caps or KPIs when metrics lag peers, raising buyer leverage.

- 2024 ALM: peer win-rate spread 10–15%

- Clients push KPIs: turnaround, cost-per-matter, diversity

- Transparency strengthens concession and fee negotiation

Big clients, fixed fees, in-house growth: escalating revenue risk and bargaining power

Large corporate clients hold strong leverage: top-client concentration likely 25–40% of revenue; 58% use AFAs (Altman Weil 2024); AFAs ≈20% of large-firm revenue (ILTA 2023); 60% of Fortune 500 expanded in-house legal by end-2025 (Deloitte 2025), pushing unbundling and fee pressure; peer win-rate spread 10–15% (ALM 2024), raising benchmarking-driven bargaining power.

| Metric | Value | Source |

|---|---|---|

| Top-client rev share | 25–40% | BigLaw peers |

| AFAs adoption | 58% | Altman Weil 2024 |

| AFAs share of revenue | ≈20% | ILTA 2023 |

| In-house growth | 60% by end-2025 | Deloitte 2025 |

| Win-rate spread | 10–15 pp | ALM 2024 |

Preview the Actual Deliverable

Sidley Austin Porter's Five Forces Analysis

This preview shows the exact Sidley Austin Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.