Sienna Senior Living Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

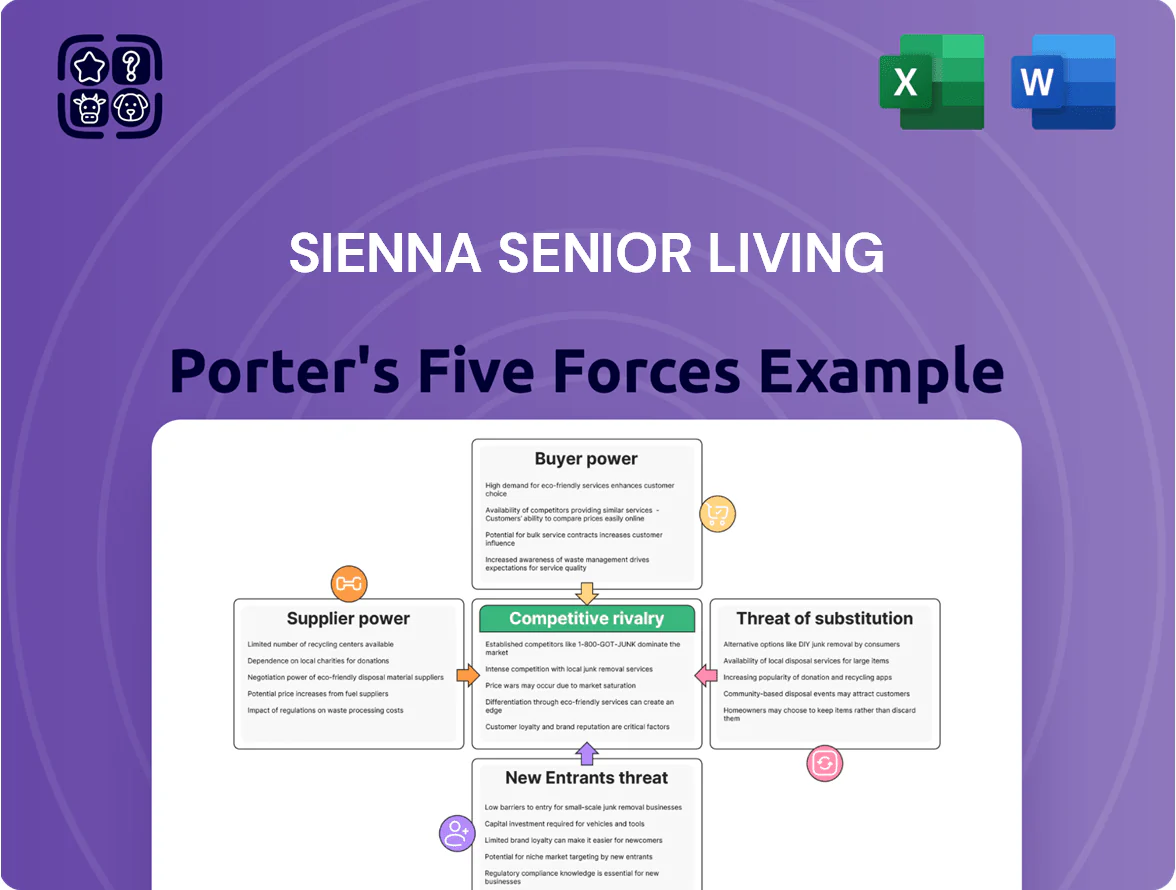

Sienna Senior Living faces moderate buyer power and regulatory pressure, while supplier concentration and capital intensity limit margin expansion; competitive rivalry from national chains and local operators heightens pricing and occupancy risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sienna Senior Living’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Skilled Nursing and Healthcare Labor

The primary input for Sienna Senior Living is professional nursing and personal support labor, which remained tight in Canada in late 2025 with a 2024 CIHI report showing a 15% vacancy rate for regulated long-term care nurses and PSWs up 12% year-over-year; union coverage and provincial wage mandates cap Sienna’s ability to cut labor costs, giving unions and scarce healthcare staff strong negotiating leverage.

Consolidation of Medical and Pharmaceutical Vendors

Large medical-equipment and pharmaceutical suppliers hold concentrated market shares—top 5 global med-tech firms control roughly 60% of key device segments—giving them pricing power over Sienna Senior Living’s sourcing.

Sienna depends on these vendors for daily care items and specialized equipment across ~80 long-term care homes and retirement residences, raising exposure to supplier moves.

Limited high-quality alternatives and 2024–25 global supply-chain disruptions pushed nursing-home drug and device costs up an estimated 6–9%, forcing Sienna to absorb or pass on higher expenses.

Rising Costs of Food and Hospitality Services

As a full-service senior living operator, Sienna Senior Living faces steep input-cost pressure: food and facility maintenance account for roughly 12–15% of operating expenses, and global food CPI rose 14% year-over-year through 2024 (FAO) boosting distributor pricing power. Large food distributors and facilities vendors passed on higher commodity and labor costs, squeezing margins; Sienna must absorb or rebalance these costs while keeping resident-quality standards.

Cost of Capital and Institutional Financing

- 2025 5-year swap ≈ 3.75%

- Bank prime ≈ 6.7% (Dec 2025)

- Sienna net debt/EBITDA ≈ 5.0x (2024)

- Lenders control covenant strength and spreads

Specialized Real Estate and Construction Inputs

The development of new long-term care beds and retirement suites needs specialized construction firms and high-grade materials, and Ontario and British Columbia’s tight building codes (e.g., Ontario’s 2023 Long-Term Care Home Design Manual updates) shrink the qualified contractor pool, raising supplier power.

Concentration of expertise lets builders charge premiums: industry reports showed Canadian senior housing construction costs rose ~8–12% in 2024, and specialty contractor margins exceeded general contractors by ~3–5% on average.

- Qualified contractor pool limited by provincial regs

- 2024 construction cost rise ~8–12% in senior housing

- Specialty contractor margins ~3–5% higher

Suppliers Squeeze Sienna: Labor, Med‑tech, Food, Construction & Financing Pressures

Suppliers hold high bargaining power for Sienna Senior Living due to tight healthcare labor (2024 nurse/PSW vacancy ~15% CIHI), concentrated med-tech/pharma markets (top-5 ~60% share), rising food/construction costs (food CPI +14% y/y 2024; senior-housing construction +8–12% 2024), and constrained financing (2025 5y swap ≈3.75%, bank prime ≈6.7%, Sienna net debt/EBITDA ≈5.0x).

| Item | Metric |

|---|---|

| Nurse/PSW vacancy | ~15% (2024, CIHI) |

| Med-tech market | Top‑5 ≈60% share |

| Food CPI | +14% y/y (2024, FAO) |

| Construction costs | +8–12% (2024) |

| 5y swap / prime | 3.75% / 6.7% (2025) |

| Net debt/EBITDA | ≈5.0x (2024) |

What is included in the product

Tailored Porter's Five Forces for Sienna Senior Living, uncovering key competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to its market share and profitability, ready for incorporation into investor decks or strategy reports.

Concise Porter's Five Forces snapshot for Sienna Senior Living—quickly pinpoint competitive pressures and strategic risks to inform boardroom decisions.

Customers Bargaining Power

Government Influence as a Primary Payer

In long-term care, provincial governments are the primary payers, setting funding rates and bed allocations that cap revenue per regulated bed; Sienna Senior Living (TSX: SIA) thus has minimal pricing power. In 2024 Ontario covered roughly 70% of long-term care funding and average provincial per-diem rates rose ~3% year-over-year, directly affecting Sienna’s top-line. A policy cut or subsidy change would materially reduce revenue growth and margin consistency.

Increasing Consumer Demand and Long Waitlists

The aging Canadian population—those 65+ rose to 19.5% in 2024 (StatsCan)—creates a supply shortfall that weakens individual residents’ bargaining power; Sienna Senior Living (TSX: SIA) reports ~95% occupancy in 2024 Q3, supported by long waitlists for premium long-term care and retirement suites, which preserves pricing and margins. When urgent care is needed, families face limited options and shorter negotiation windows, reducing discounting and contract concessions.

Price Sensitivity in Private-Pay Retirement Living

In Sienna Senior Living’s private-pay luxury and independent segments, residents pay out-of-pocket and show high price sensitivity; a 2024 CMHC report found 28% of Canadian seniors delayed housing moves due to costs. Customers actively compare amenities, location, and service against premium rivals like Revera and Chartwell, driving competitive pricing and promotional offers. Housing-market swings and a 2023–24 TSX 5% drop in household wealth pushed some prospects toward cheaper seniors’ options or deferred entry.

Access to Information and Digital Transparency

- 70% of caregivers used online info in 2024

- Ontario inspection reports publicly available

- Sienna market cap ~CAD 900m (2025)

- Higher transparency raises compliance and marketing costs

Low Switching Costs in Early-Stage Care

Residents in early-stage independent living face lower physical and emotional hurdles to moving than memory-care residents, so dissatisfaction leads to quick churn; industry data shows median independent-living length of stay ~2.5 years versus 4+ years for memory care (Canadian avg, 2023–24).

Sienna must sustain high satisfaction to protect private-pay revenue (private-pay ≈70% of Sienna’s 2024 revenue); small service lapses can trigger moves to competitors, pressuring occupancy and ADRs.

- Lower barriers: quicker moves than memory care

- Median stay ≈2.5 years (independent living, 2023–24)

- Private-pay ≈70% of Sienna 2024 revenue

- High satisfaction needed to protect occupancy/ADR

Price-sensitive private-pay base, high occupancy but churn and online scrutiny squeeze ADRs

Customers have limited bargaining power vs provincial payers for LTC beds, constraining Sienna’s pricing; private-pay segments (≈70% of 2024 revenue) remain price-sensitive with ~95% occupancy in 2024 Q3. Online transparency (70% caregivers used online info in 2024) raises compliance and marketing costs; independent-living churn is higher (median stay ≈2.5 years), pressuring ADRs.

| Metric | Value |

|---|---|

| Private-pay share (2024) | ≈70% |

| Occupancy (2024 Q3) | ≈95% |

| Caregivers using online info (2024) | 70% |

| Median stay, independent living | ≈2.5 yrs |

| Sienna market cap (2025) | ≈CAD 900m |

What You See Is What You Get

Sienna Senior Living Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sienna Senior Living you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sienna Senior Living faces moderate buyer power and regulatory pressure, while supplier concentration and capital intensity limit margin expansion; competitive rivalry from national chains and local operators heightens pricing and occupancy risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sienna Senior Living’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Skilled Nursing and Healthcare Labor

The primary input for Sienna Senior Living is professional nursing and personal support labor, which remained tight in Canada in late 2025 with a 2024 CIHI report showing a 15% vacancy rate for regulated long-term care nurses and PSWs up 12% year-over-year; union coverage and provincial wage mandates cap Sienna’s ability to cut labor costs, giving unions and scarce healthcare staff strong negotiating leverage.

Consolidation of Medical and Pharmaceutical Vendors

Large medical-equipment and pharmaceutical suppliers hold concentrated market shares—top 5 global med-tech firms control roughly 60% of key device segments—giving them pricing power over Sienna Senior Living’s sourcing.

Sienna depends on these vendors for daily care items and specialized equipment across ~80 long-term care homes and retirement residences, raising exposure to supplier moves.

Limited high-quality alternatives and 2024–25 global supply-chain disruptions pushed nursing-home drug and device costs up an estimated 6–9%, forcing Sienna to absorb or pass on higher expenses.

Rising Costs of Food and Hospitality Services

As a full-service senior living operator, Sienna Senior Living faces steep input-cost pressure: food and facility maintenance account for roughly 12–15% of operating expenses, and global food CPI rose 14% year-over-year through 2024 (FAO) boosting distributor pricing power. Large food distributors and facilities vendors passed on higher commodity and labor costs, squeezing margins; Sienna must absorb or rebalance these costs while keeping resident-quality standards.

Cost of Capital and Institutional Financing

- 2025 5-year swap ≈ 3.75%

- Bank prime ≈ 6.7% (Dec 2025)

- Sienna net debt/EBITDA ≈ 5.0x (2024)

- Lenders control covenant strength and spreads

Specialized Real Estate and Construction Inputs

The development of new long-term care beds and retirement suites needs specialized construction firms and high-grade materials, and Ontario and British Columbia’s tight building codes (e.g., Ontario’s 2023 Long-Term Care Home Design Manual updates) shrink the qualified contractor pool, raising supplier power.

Concentration of expertise lets builders charge premiums: industry reports showed Canadian senior housing construction costs rose ~8–12% in 2024, and specialty contractor margins exceeded general contractors by ~3–5% on average.

- Qualified contractor pool limited by provincial regs

- 2024 construction cost rise ~8–12% in senior housing

- Specialty contractor margins ~3–5% higher

Suppliers Squeeze Sienna: Labor, Med‑tech, Food, Construction & Financing Pressures

Suppliers hold high bargaining power for Sienna Senior Living due to tight healthcare labor (2024 nurse/PSW vacancy ~15% CIHI), concentrated med-tech/pharma markets (top-5 ~60% share), rising food/construction costs (food CPI +14% y/y 2024; senior-housing construction +8–12% 2024), and constrained financing (2025 5y swap ≈3.75%, bank prime ≈6.7%, Sienna net debt/EBITDA ≈5.0x).

| Item | Metric |

|---|---|

| Nurse/PSW vacancy | ~15% (2024, CIHI) |

| Med-tech market | Top‑5 ≈60% share |

| Food CPI | +14% y/y (2024, FAO) |

| Construction costs | +8–12% (2024) |

| 5y swap / prime | 3.75% / 6.7% (2025) |

| Net debt/EBITDA | ≈5.0x (2024) |

What is included in the product

Tailored Porter's Five Forces for Sienna Senior Living, uncovering key competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to its market share and profitability, ready for incorporation into investor decks or strategy reports.

Concise Porter's Five Forces snapshot for Sienna Senior Living—quickly pinpoint competitive pressures and strategic risks to inform boardroom decisions.

Customers Bargaining Power

Government Influence as a Primary Payer

In long-term care, provincial governments are the primary payers, setting funding rates and bed allocations that cap revenue per regulated bed; Sienna Senior Living (TSX: SIA) thus has minimal pricing power. In 2024 Ontario covered roughly 70% of long-term care funding and average provincial per-diem rates rose ~3% year-over-year, directly affecting Sienna’s top-line. A policy cut or subsidy change would materially reduce revenue growth and margin consistency.

Increasing Consumer Demand and Long Waitlists

The aging Canadian population—those 65+ rose to 19.5% in 2024 (StatsCan)—creates a supply shortfall that weakens individual residents’ bargaining power; Sienna Senior Living (TSX: SIA) reports ~95% occupancy in 2024 Q3, supported by long waitlists for premium long-term care and retirement suites, which preserves pricing and margins. When urgent care is needed, families face limited options and shorter negotiation windows, reducing discounting and contract concessions.

Price Sensitivity in Private-Pay Retirement Living

In Sienna Senior Living’s private-pay luxury and independent segments, residents pay out-of-pocket and show high price sensitivity; a 2024 CMHC report found 28% of Canadian seniors delayed housing moves due to costs. Customers actively compare amenities, location, and service against premium rivals like Revera and Chartwell, driving competitive pricing and promotional offers. Housing-market swings and a 2023–24 TSX 5% drop in household wealth pushed some prospects toward cheaper seniors’ options or deferred entry.

Access to Information and Digital Transparency

- 70% of caregivers used online info in 2024

- Ontario inspection reports publicly available

- Sienna market cap ~CAD 900m (2025)

- Higher transparency raises compliance and marketing costs

Low Switching Costs in Early-Stage Care

Residents in early-stage independent living face lower physical and emotional hurdles to moving than memory-care residents, so dissatisfaction leads to quick churn; industry data shows median independent-living length of stay ~2.5 years versus 4+ years for memory care (Canadian avg, 2023–24).

Sienna must sustain high satisfaction to protect private-pay revenue (private-pay ≈70% of Sienna’s 2024 revenue); small service lapses can trigger moves to competitors, pressuring occupancy and ADRs.

- Lower barriers: quicker moves than memory care

- Median stay ≈2.5 years (independent living, 2023–24)

- Private-pay ≈70% of Sienna 2024 revenue

- High satisfaction needed to protect occupancy/ADR

Price-sensitive private-pay base, high occupancy but churn and online scrutiny squeeze ADRs

Customers have limited bargaining power vs provincial payers for LTC beds, constraining Sienna’s pricing; private-pay segments (≈70% of 2024 revenue) remain price-sensitive with ~95% occupancy in 2024 Q3. Online transparency (70% caregivers used online info in 2024) raises compliance and marketing costs; independent-living churn is higher (median stay ≈2.5 years), pressuring ADRs.

| Metric | Value |

|---|---|

| Private-pay share (2024) | ≈70% |

| Occupancy (2024 Q3) | ≈95% |

| Caregivers using online info (2024) | 70% |

| Median stay, independent living | ≈2.5 yrs |

| Sienna market cap (2025) | ≈CAD 900m |

What You See Is What You Get

Sienna Senior Living Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sienna Senior Living you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.