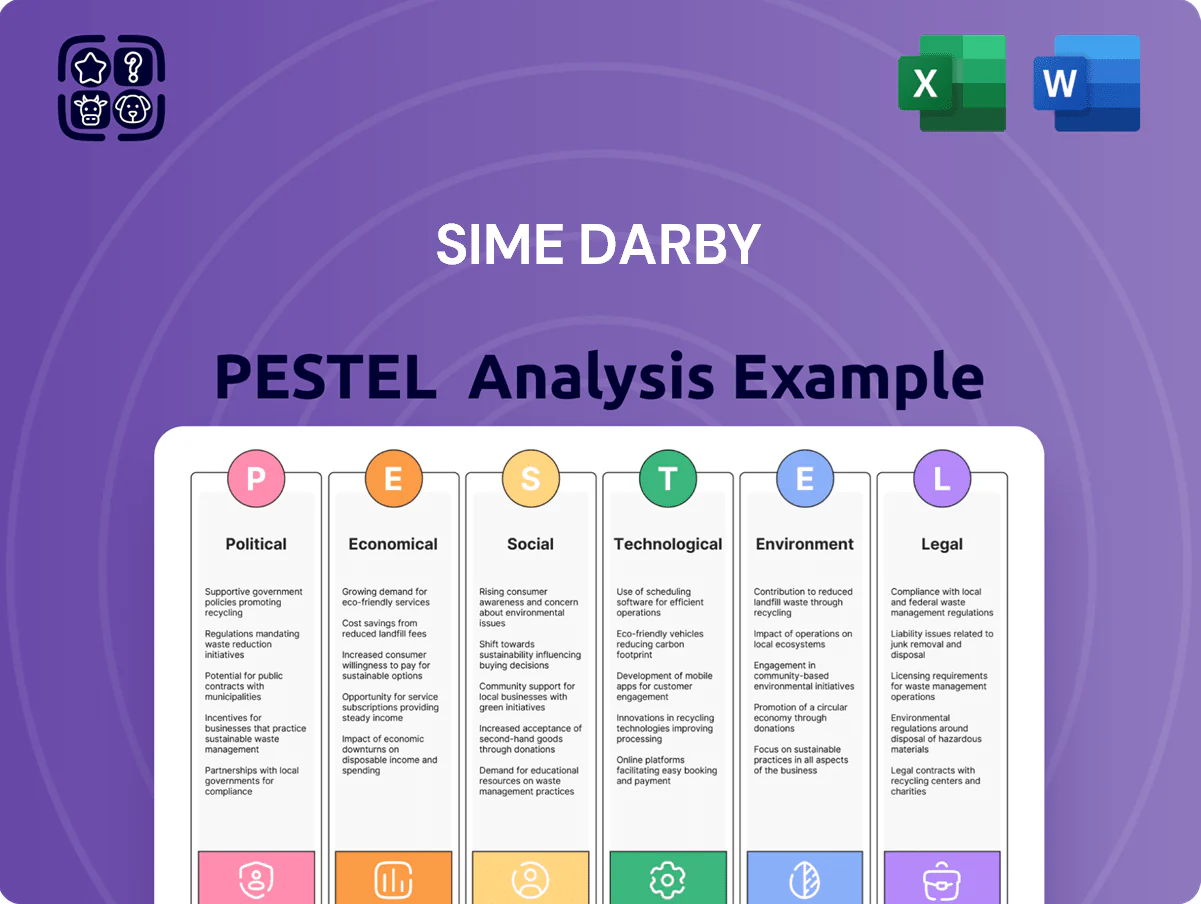

Sime Darby PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of Sime Darby reveals how political shifts, economic pressures, and environmental regulations are reshaping its growth trajectory—critical insight for investors and strategists seeking competitive advantage; download the full report for a detailed breakdown and actionable recommendations you can use immediately.

Political factors

Geopolitical Trade Relations Between China and Australia

Sime Darby Industrial's exposure to Australia hinges on mining demand: China imported 62% of Australia’s iron ore in 2024, and coal exports to China fell 18% year-on-year amid diplomatic strains, directly reducing demand for Caterpillar-class machinery and aftermarket services.

Malaysia National Automotive Policy and EV Incentives

The Malaysian National Automotive Policy (NAP 2020 update toward NAP 2025) targets EV penetration and local value-addition, with government EV incentives including full import duty exemptions and investment tax allowances; Sime Darby Motor gained tax breaks for CKD EV assembly, supporting its FY2024 EV rollout where EVs comprised ~8% of retail sales versus 3% in 2021.

Infrastructure Spending in Key Southeast Asian Markets

Government-led infrastructure projects in Malaysia and Southeast Asia drive demand in Sime Darby’s industrial equipment segment, with ASEAN infrastructure spending projected at US$200–250 billion annually through 2025–2030 and Malaysia’s 2024 Budget allocating RM50.7 billion for infrastructure. Political approvals for major transport and utility projects create a steady pipeline for heavy machinery and engineering services, underpinning order books. Sime Darby’s revenues are thus sensitive to regional fiscal health and shifts in development priorities, with public CAPEX trends directly affecting equipment sales and aftersales.

Regional Stability and Policy Consistency

Operating across 10+ Asia-Pacific markets, Sime Darby faces diverse political risk; e.g., Malaysia, Indonesia, and the Philippines accounted for over 60% of regional revenues in FY2024, amplifying exposure to local instability.

Policy shifts—such as Indonesia’s 2023 mineral export rules and Malaysian foreign-ownership debates—can affect asset valuations and import duty costs, creating operational uncertainty.

Maintaining ties with local authorities and community stakeholders is crucial to safeguard long-term investments and ensure continuity across jurisdictions.

- Exposure: 10+ APAC markets; >60% revenues from Malaysia/Indonesia/Philippines (FY2024)

- Risk triggers: leadership changes, foreign-ownership policy reversals, import duty shifts

- Mitigation: strong local government and community relations to protect assets and operations

Global Trade Protectionism and Tariffs

The rise of protectionism has pushed global tariffs upward; in 2023 global trade-weighted tariffs averaged 3.2% with spikes in key markets, raising import costs for vehicle and component distributors like Sime Darby. As principal distributor for BMW and Caterpillar, Sime Darby faces margin pressure when tariffs or retaliatory duties increase COGS, evidenced by Malaysia’s vehicle import duty variances of 10–30% in recent policy shifts. Strategic plans must model supply-chain shocks and expand local assembly to avoid high duties.

- Global trade-weighted tariffs ~3.2% (2023)

- Malaysia vehicle import duties range ~10–30%

- Higher tariffs → increased COGS, narrower margins for BMW/Caterpillar distribution

- Localized assembly reduces exposure to import duties and supply disruptions

Sime Darby: >60% ASEAN Revenue, Infrastructure Boom vs Trade Tariffs & Vehicle Duties

Political risks shape Sime Darby’s regional revenues: FY2024 >60% from Malaysia/Indonesia/PH; ASEAN capex US$200–250bn pa (2025–30); Malaysia 2024 infrastructure RM50.7bn; China bought 62% of AU iron ore (2024); global trade-weighted tariffs ~3.2% (2023); Malaysia vehicle import duties 10–30% impacting margins.

| Metric | Value |

|---|---|

| FY2024 regional revenue share | >60% |

| ASEAN infra spend | US$200–250bn/yr (2025–30) |

| Malaysia infra 2024 | RM50.7bn |

| China AU iron ore share | 62% (2024) |

| Global tariffs | 3.2% (2023) |

| Malaysia vehicle duties | 10–30% |

What is included in the product

Explores how macro-environmental factors uniquely affect Sime Darby across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify threats, opportunities and scenario-driven strategies; formatted for easy insertion into plans, decks or reports and reflecting regional industry dynamics.

A concise, visually segmented Sime Darby PESTLE summary that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, market positioning, and region-specific implications while allowing space for custom notes.

Economic factors

Commodity Price Volatility Impacting Industrial Demand

The demand for Sime Darby Industrial equipment tracks global commodity prices—coal, gold and iron ore—where a 20% rise in iron ore and 15% in gold during 2024 boosted mining capex, underpinning higher orders for heavy machinery.

High commodity prices in 2024 encouraged fleet renewals and expansion, while a projected 2025 downturn—benchmark iron ore futures down ~12% YTD to Jan 2025—would likely cut clients’ CAPEX and compress Sime Darby Industrial margins.

Currency Exchange Rate Fluctuations

As a multinational conglomerate, Sime Darby faces exposure from MYR volatility versus AUD, CNY and USD; a 10% MYR depreciation vs USD in 2023 raised import costs for vehicles and spare parts by roughly 8–12%, while translation effects trimmed FY2024 overseas EBITDA by about RM250–400m. Significant movements can therefore erode margins, making hedging—forwards, options, and natural hedges—critical to stabilize cash flows and protect the bottom line.

Interest Rate Environments and Financing Costs

The automotive and industrial segments are interest-rate sensitive; a 150 bps rise in Malaysian OPR to 3.25% by late 2025 would increase borrowing costs for Sime Darby and its customers, squeezing margins and slowing premium vehicle demand. Higher rates raise finance costs for construction firms buying heavy equipment, risking a 5–8% volume decline in equipment sales. Sime Darby must offer competitive financing packages and target net debt/EBITDA around 1.0–1.5x to preserve liquidity and credit metrics.

Inflationary Pressures on Operational Costs

Global inflation elevated input costs in 2023–24; Malaysia’s headline CPI peaked near 4.2% in 2023, pushing wages, logistics and commodity prices up and compressing margins across Sime Darby’s diversified segments.

Management faces a trade-off between price increases and volume sensitivity; passing costs risks demand erosion in price-sensitive markets while margins dipped—Sime Darby Plantation reported input cost rises impacting EBIT margins in FY2024.

Prioritising lean operations, tighter supply-chain procurement and fuel-efficient logistics—plus targeted hedging for key commodities—are essential to protect operating profit and cash flow amid persistent inflationary pressures.

- Malaysia CPI ~4.2% (2023) raised labor and logistics costs

- Input-cost-driven margin pressure observed in FY2024 Plantation results

- Mitigation: supply-chain efficiency, lean ops, commodity hedging

Consumer Spending Power in the Premium Segment

The motors division depends on affluent buyers in Malaysia, China and Singapore; Malaysia’s 2024 GDP grew 4.0% while Singapore’s 2024 GDP rose 3.6% and China’s 2024 GDP 5.2%, all affecting premium demand.

Economic slowdowns or rising inequality can shrink luxury car sales—BMW and Porsche volumes fell ~8% in SE Asia in 2023 during softer demand.

Tracking GDP, unemployment and consumer confidence enables Sime Darby to adjust inventory and marketing for the premium segment.

- 2024 GDP: Malaysia 4.0%, China 5.2%, Singapore 3.6%

- Luxury car sales drop ~8% in SE Asia in 2023

- Monitor GDP, employment, consumer confidence to size inventory

Commodity upcycle lifts mining capex as inflation and FX pressure margins, GDP shapes demand

Economic drivers: 2024 commodity upcycle (iron ore +20%, gold +15%) boosted mining capex, yet iron ore futures down ~12% YTD Jan 2025 risks CAPEX cuts; Malaysia CPI ~4.2% (2023) raised input costs; MYR -10% vs USD in 2023 increased import costs ~8–12%; 2024 GDP: MY 4.0%, CN 5.2%, SG 3.6% affecting premium vehicle demand.

| Metric | 2023/2024 |

|---|---|

| Iron ore | +20% (2024) |

| Gold | +15% (2024) |

| MY CPI | 4.2% (2023) |

| MYR vs USD | -10% (2023) |

| GDP MY/CN/SG | 4.0%/5.2%/3.6% (2024) |

Preview the Actual Deliverable

Sime Darby PESTLE Analysis

The preview shown here is the exact Sime Darby PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

The layout, content, and structure visible here are exactly what you’ll download immediately after buying—no placeholders, no teasers, just the final, comprehensive report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of Sime Darby reveals how political shifts, economic pressures, and environmental regulations are reshaping its growth trajectory—critical insight for investors and strategists seeking competitive advantage; download the full report for a detailed breakdown and actionable recommendations you can use immediately.

Political factors

Geopolitical Trade Relations Between China and Australia

Sime Darby Industrial's exposure to Australia hinges on mining demand: China imported 62% of Australia’s iron ore in 2024, and coal exports to China fell 18% year-on-year amid diplomatic strains, directly reducing demand for Caterpillar-class machinery and aftermarket services.

Malaysia National Automotive Policy and EV Incentives

The Malaysian National Automotive Policy (NAP 2020 update toward NAP 2025) targets EV penetration and local value-addition, with government EV incentives including full import duty exemptions and investment tax allowances; Sime Darby Motor gained tax breaks for CKD EV assembly, supporting its FY2024 EV rollout where EVs comprised ~8% of retail sales versus 3% in 2021.

Infrastructure Spending in Key Southeast Asian Markets

Government-led infrastructure projects in Malaysia and Southeast Asia drive demand in Sime Darby’s industrial equipment segment, with ASEAN infrastructure spending projected at US$200–250 billion annually through 2025–2030 and Malaysia’s 2024 Budget allocating RM50.7 billion for infrastructure. Political approvals for major transport and utility projects create a steady pipeline for heavy machinery and engineering services, underpinning order books. Sime Darby’s revenues are thus sensitive to regional fiscal health and shifts in development priorities, with public CAPEX trends directly affecting equipment sales and aftersales.

Regional Stability and Policy Consistency

Operating across 10+ Asia-Pacific markets, Sime Darby faces diverse political risk; e.g., Malaysia, Indonesia, and the Philippines accounted for over 60% of regional revenues in FY2024, amplifying exposure to local instability.

Policy shifts—such as Indonesia’s 2023 mineral export rules and Malaysian foreign-ownership debates—can affect asset valuations and import duty costs, creating operational uncertainty.

Maintaining ties with local authorities and community stakeholders is crucial to safeguard long-term investments and ensure continuity across jurisdictions.

- Exposure: 10+ APAC markets; >60% revenues from Malaysia/Indonesia/Philippines (FY2024)

- Risk triggers: leadership changes, foreign-ownership policy reversals, import duty shifts

- Mitigation: strong local government and community relations to protect assets and operations

Global Trade Protectionism and Tariffs

The rise of protectionism has pushed global tariffs upward; in 2023 global trade-weighted tariffs averaged 3.2% with spikes in key markets, raising import costs for vehicle and component distributors like Sime Darby. As principal distributor for BMW and Caterpillar, Sime Darby faces margin pressure when tariffs or retaliatory duties increase COGS, evidenced by Malaysia’s vehicle import duty variances of 10–30% in recent policy shifts. Strategic plans must model supply-chain shocks and expand local assembly to avoid high duties.

- Global trade-weighted tariffs ~3.2% (2023)

- Malaysia vehicle import duties range ~10–30%

- Higher tariffs → increased COGS, narrower margins for BMW/Caterpillar distribution

- Localized assembly reduces exposure to import duties and supply disruptions

Sime Darby: >60% ASEAN Revenue, Infrastructure Boom vs Trade Tariffs & Vehicle Duties

Political risks shape Sime Darby’s regional revenues: FY2024 >60% from Malaysia/Indonesia/PH; ASEAN capex US$200–250bn pa (2025–30); Malaysia 2024 infrastructure RM50.7bn; China bought 62% of AU iron ore (2024); global trade-weighted tariffs ~3.2% (2023); Malaysia vehicle import duties 10–30% impacting margins.

| Metric | Value |

|---|---|

| FY2024 regional revenue share | >60% |

| ASEAN infra spend | US$200–250bn/yr (2025–30) |

| Malaysia infra 2024 | RM50.7bn |

| China AU iron ore share | 62% (2024) |

| Global tariffs | 3.2% (2023) |

| Malaysia vehicle duties | 10–30% |

What is included in the product

Explores how macro-environmental factors uniquely affect Sime Darby across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify threats, opportunities and scenario-driven strategies; formatted for easy insertion into plans, decks or reports and reflecting regional industry dynamics.

A concise, visually segmented Sime Darby PESTLE summary that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, market positioning, and region-specific implications while allowing space for custom notes.

Economic factors

Commodity Price Volatility Impacting Industrial Demand

The demand for Sime Darby Industrial equipment tracks global commodity prices—coal, gold and iron ore—where a 20% rise in iron ore and 15% in gold during 2024 boosted mining capex, underpinning higher orders for heavy machinery.

High commodity prices in 2024 encouraged fleet renewals and expansion, while a projected 2025 downturn—benchmark iron ore futures down ~12% YTD to Jan 2025—would likely cut clients’ CAPEX and compress Sime Darby Industrial margins.

Currency Exchange Rate Fluctuations

As a multinational conglomerate, Sime Darby faces exposure from MYR volatility versus AUD, CNY and USD; a 10% MYR depreciation vs USD in 2023 raised import costs for vehicles and spare parts by roughly 8–12%, while translation effects trimmed FY2024 overseas EBITDA by about RM250–400m. Significant movements can therefore erode margins, making hedging—forwards, options, and natural hedges—critical to stabilize cash flows and protect the bottom line.

Interest Rate Environments and Financing Costs

The automotive and industrial segments are interest-rate sensitive; a 150 bps rise in Malaysian OPR to 3.25% by late 2025 would increase borrowing costs for Sime Darby and its customers, squeezing margins and slowing premium vehicle demand. Higher rates raise finance costs for construction firms buying heavy equipment, risking a 5–8% volume decline in equipment sales. Sime Darby must offer competitive financing packages and target net debt/EBITDA around 1.0–1.5x to preserve liquidity and credit metrics.

Inflationary Pressures on Operational Costs

Global inflation elevated input costs in 2023–24; Malaysia’s headline CPI peaked near 4.2% in 2023, pushing wages, logistics and commodity prices up and compressing margins across Sime Darby’s diversified segments.

Management faces a trade-off between price increases and volume sensitivity; passing costs risks demand erosion in price-sensitive markets while margins dipped—Sime Darby Plantation reported input cost rises impacting EBIT margins in FY2024.

Prioritising lean operations, tighter supply-chain procurement and fuel-efficient logistics—plus targeted hedging for key commodities—are essential to protect operating profit and cash flow amid persistent inflationary pressures.

- Malaysia CPI ~4.2% (2023) raised labor and logistics costs

- Input-cost-driven margin pressure observed in FY2024 Plantation results

- Mitigation: supply-chain efficiency, lean ops, commodity hedging

Consumer Spending Power in the Premium Segment

The motors division depends on affluent buyers in Malaysia, China and Singapore; Malaysia’s 2024 GDP grew 4.0% while Singapore’s 2024 GDP rose 3.6% and China’s 2024 GDP 5.2%, all affecting premium demand.

Economic slowdowns or rising inequality can shrink luxury car sales—BMW and Porsche volumes fell ~8% in SE Asia in 2023 during softer demand.

Tracking GDP, unemployment and consumer confidence enables Sime Darby to adjust inventory and marketing for the premium segment.

- 2024 GDP: Malaysia 4.0%, China 5.2%, Singapore 3.6%

- Luxury car sales drop ~8% in SE Asia in 2023

- Monitor GDP, employment, consumer confidence to size inventory

Commodity upcycle lifts mining capex as inflation and FX pressure margins, GDP shapes demand

Economic drivers: 2024 commodity upcycle (iron ore +20%, gold +15%) boosted mining capex, yet iron ore futures down ~12% YTD Jan 2025 risks CAPEX cuts; Malaysia CPI ~4.2% (2023) raised input costs; MYR -10% vs USD in 2023 increased import costs ~8–12%; 2024 GDP: MY 4.0%, CN 5.2%, SG 3.6% affecting premium vehicle demand.

| Metric | 2023/2024 |

|---|---|

| Iron ore | +20% (2024) |

| Gold | +15% (2024) |

| MY CPI | 4.2% (2023) |

| MYR vs USD | -10% (2023) |

| GDP MY/CN/SG | 4.0%/5.2%/3.6% (2024) |

Preview the Actual Deliverable

Sime Darby PESTLE Analysis

The preview shown here is the exact Sime Darby PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

The layout, content, and structure visible here are exactly what you’ll download immediately after buying—no placeholders, no teasers, just the final, comprehensive report.