Simplex Infrastructures SWOT Analysis

Your Strategic Toolkit Starts Here

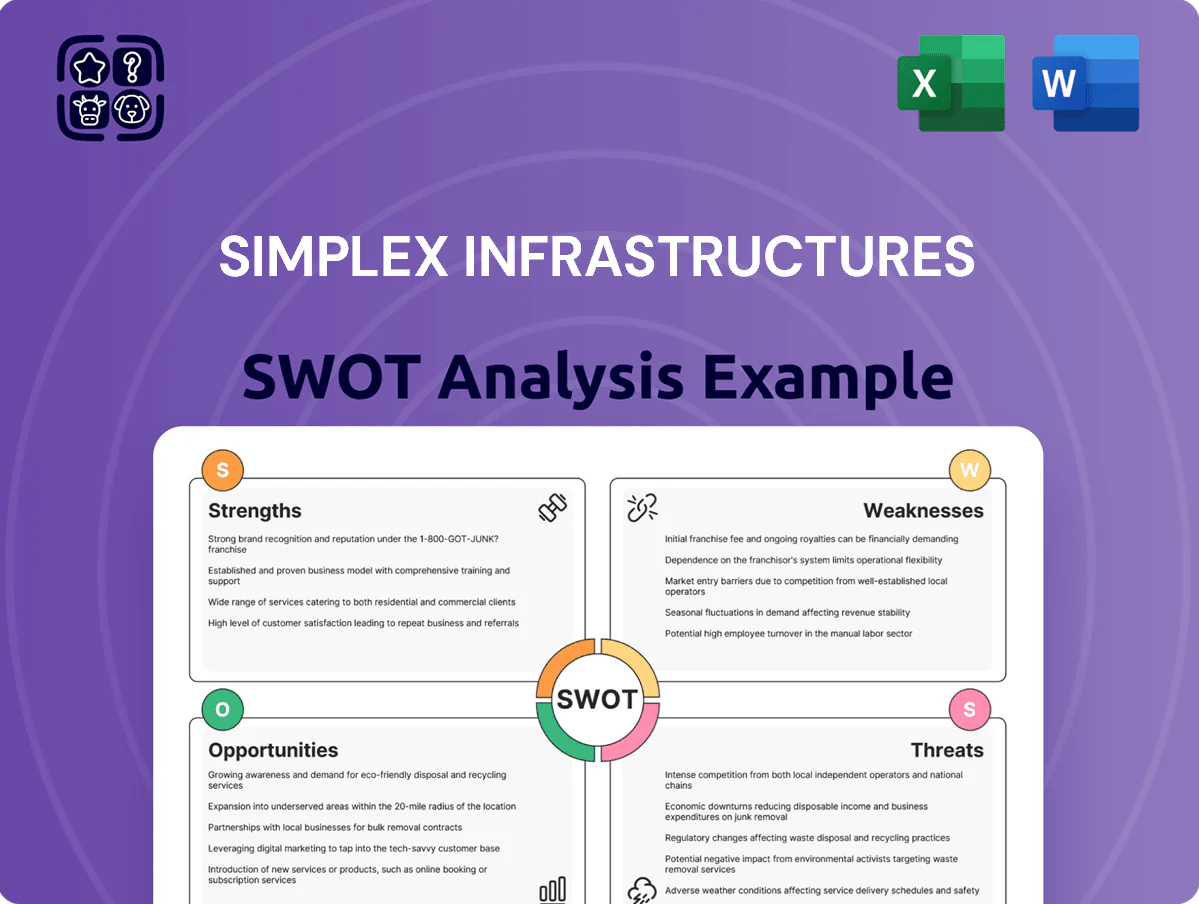

Simplex Infrastructures possesses notable strengths in its diversified project portfolio and established market presence, but faces challenges from intense competition and fluctuating project timelines. Understanding these internal capabilities and external market dynamics is crucial for strategic planning.

Want the full story behind Simplex Infrastructures' strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Diverse Sectoral Expertise

Simplex Infrastructures boasts a remarkably diverse sectoral expertise, a significant strength that underpins its resilience and growth potential. The company's extensive portfolio covers a wide array of critical infrastructure segments, including buildings, industrial plants, power generation and transmission, urban development, marine projects, and transportation networks.

This broad sectoral reach is a key differentiator, mitigating risks associated with downturns in any single industry. For instance, in the fiscal year ending March 31, 2023, Simplex's order book reflected this diversification, with significant contributions from both building and transport infrastructure projects, showcasing its ability to secure business across varied economic cycles.

The company's proven track record in executing complex and challenging projects, such as the construction of elevated flyovers, modern airport terminals, and major bridges, further highlights its comprehensive capabilities. This depth of experience across different project types allows Simplex to adapt to evolving market demands and leverage opportunities in India's rapidly expanding infrastructure landscape.

Established Market Presence and Experience

Simplex Infrastructures boasts a deep-rooted presence in India's construction sector, built over decades. This extensive history translates into a robust brand reputation and a proven track record of successfully managing complex projects from start to finish.

The company's experience is underscored by its completion of numerous high-profile contracts, often earning commendation certificates from satisfied clients. For instance, in FY2023, Simplex reported a revenue of INR 3,368 crore, demonstrating its substantial operational scale and market engagement.

Public and Private Sector Client Base

Simplex Infrastructures' ability to serve both public and private sector clients is a significant strength, offering a diversified revenue base. This dual focus helps cushion the company against sector-specific downturns. For instance, in the fiscal year ending March 31, 2023, Simplex's order book demonstrated a healthy mix of government contracts and private sector projects, allowing for consistent project flow and revenue generation.

Operational Efficiency in Specific Areas

Simplex Infrastructures has demonstrated pockets of operational strength, notably in managing its Cash Conversion Cycle. This efficiency in converting working capital into cash is a vital asset, particularly within the often cash-intensive construction industry. For instance, as of the fiscal year ending March 31, 2024, the company's Cash Conversion Cycle was reported at 95 days, an improvement from 102 days in the previous year, signaling better working capital management.

This operational proficiency translates into tangible benefits:

- Improved Liquidity Management: A shorter cycle means cash is tied up for less time, enhancing the company's ability to meet short-term obligations.

- Reduced Working Capital Needs: Efficient conversion lowers the amount of capital required to fund day-to-day operations.

- Enhanced Financial Flexibility: Better cash flow generation provides greater capacity for reinvestment or debt reduction.

- Competitive Advantage: In an industry where cash flow is king, this operational strength can set Simplex apart from less efficient competitors.

Focus on Core Competencies

Simplex Infrastructures' vision centers on maintaining its leadership in foundation technology and general civil engineering. This dedicated focus on core competencies allows the company to harness deep specialized knowledge and extensive experience.

By concentrating on these niche areas within the construction sector, Simplex can cultivate significant competitive advantages. For instance, in the fiscal year ending March 31, 2023, Simplex Infrastructures reported revenue of INR 2,514.5 crore, with a substantial portion likely attributable to its specialized engineering and construction services.

- Leadership in Foundation Technology: Reinforces specialized expertise and market positioning.

- General Civil Engineering Strength: Leverages broad capabilities for diverse project needs.

- Competitive Advantage: Niche focus allows for deeper skill development and efficiency.

- Market Recognition: Sustained leadership implies strong client trust and project execution.

Simplex: Diversified Expertise & Operational Strength Powering Infrastructure

Simplex Infrastructures' diversified sectoral expertise is a significant advantage, allowing it to navigate different market conditions. Its broad portfolio, spanning buildings, industrial plants, power, and transportation, mitigates risks associated with any single sector's performance. This breadth was evident in its order book for the fiscal year ending March 31, 2023, which showed strong contributions from both building and transport infrastructure.

The company's proven track record in executing complex projects, such as elevated flyovers and airport terminals, demonstrates its comprehensive capabilities. This deep experience across various project types enables Simplex to adapt to evolving market demands and capitalize on India's infrastructure growth. For the fiscal year ending March 31, 2023, Simplex reported revenues of INR 3,368 crore, reflecting its substantial operational scale.

Simplex's ability to serve both public and private sector clients provides a diversified revenue base, enhancing its resilience against sector-specific downturns. The fiscal year ending March 31, 2023, saw a healthy mix of government and private projects in its order book, ensuring consistent project flow.

The company exhibits operational strength in managing its Cash Conversion Cycle, a critical factor in the construction industry. As of March 31, 2024, the cycle was 95 days, an improvement from 102 days in the prior year, indicating better working capital management and enhanced financial flexibility.

| Metric | FY Ending March 31, 2023 | FY Ending March 31, 2024 |

|---|---|---|

| Total Revenue (INR Crore) | 3,368 | Not Publicly Disclosed Yet |

| Cash Conversion Cycle (Days) | 102 | 95 |

What is included in the product

Delivers a strategic overview of Simplex Infrastructures’s internal and external business factors, highlighting its strengths, weaknesses, opportunities, and threats.

Offers a clear, actionable framework to identify and address Simplex Infrastructures' critical vulnerabilities and capitalize on its unique strengths.

Weaknesses

Significant Financial Losses and Declining Revenue

Simplex Infrastructures has faced considerable financial headwinds, marked by significant net losses and a pronounced downturn in revenue. For instance, the company experienced a substantial 73.53% decrease in net profit during the fourth quarter of the 2024-2025 fiscal year.

This financial strain is further evidenced by a 21.85% decline in sales for the same quarter. The company's revenue trajectory has been a consistent concern, showing a concerning compound annual growth rate (CAGR) of -23.4% over the last five years, highlighting a persistent struggle to maintain sales momentum.

Poor Liquidity and Debt Servicing Delays

Simplex Infrastructures faces significant challenges with its liquidity, resulting in persistent delays in meeting its debt obligations. This financial strain is a major concern for stakeholders.

Credit rating agencies have flagged Simplex Infrastructures by placing it under 'Issuer Not Cooperating' categories. This designation stems from a lack of sufficient information and ongoing defaults, underscoring the company's precarious financial health.

High Debt-to-Equity Ratio and Interest Costs

Simplex Infrastructures' high Debt-to-Equity ratio, reportedly around 2.2x as of March 2024, highlights a substantial reliance on borrowed funds. This leverage magnifies financial risk, particularly as interest expenses continue to climb, impacting profitability and cash flow availability.

Negative Profitability Ratios

Simplex Infrastructures faces significant challenges with its profitability, as evidenced by consistently weak key metrics. Over the last three years, the company has reported a concerning Return on Equity (ROE) of -58.53% and a Return on Capital Employed (ROCE) of -0.55%. These figures highlight a struggle to generate adequate returns for shareholders and efficiently utilize its capital base.

Further compounding these issues, the company's EBITDA margin has remained low, signaling difficulties in translating revenue into operational profits. This low margin suggests that operational costs are consuming a substantial portion of earnings, hindering the company's ability to cover its expenses and reinvest in growth.

- Poor Profitability: Negative ROE (-58.53%) and ROCE (-0.55%) over the past three years indicate weak financial performance.

- Low EBITDA Margin: Challenges in generating sufficient operating profits are evident from the consistently low EBITDA margin.

- Capital Inefficiency: The negative ROCE points to issues in effectively employing capital to generate returns.

Challenges in Recovering Client Dues

Simplex Infrastructures faces significant hurdles in collecting payments from its clients, a situation that has notably strained its liquidity. These delays, especially from government entities, directly impede the company's ability to manage its cash flow effectively. This directly impacts its capacity to meet its financial commitments, including debt servicing, creating a challenging financial environment.

The company's financial health is further complicated by these recovery delays. For instance, as of the fiscal year ending March 31, 2023, Simplex Infrastructures reported a substantial increase in its trade receivables. This rise, coupled with slow collection cycles, highlights the persistent nature of this weakness.

- Delayed Client Payments: Significant delays in receiving payments from clients, particularly government agencies, are a primary concern.

- Liquidity Strain: These payment delays directly contribute to a stretched liquidity position for the company.

- Impact on Debt Servicing: The inability to collect dues promptly hinders the company's ability to service its existing debt obligations.

- Trade Receivables Growth: An increase in trade receivables, as observed in recent financial reports, underscores the severity of the collection issue.

Infrastructure company faces severe profitability and liquidity issues

Simplex Infrastructures grapples with persistent profitability issues, reflected in a stark -58.53% Return on Equity and a -0.55% Return on Capital Employed over the last three years. This indicates a significant struggle to generate value for shareholders and efficiently utilize its capital base.

The company's operational efficiency is also hampered by a low EBITDA margin, suggesting that operating costs are disproportionately high relative to revenue, thereby limiting its capacity for reinvestment and debt coverage.

Furthermore, Simplex Infrastructures faces substantial liquidity challenges stemming from prolonged delays in client payments, particularly from government entities, which directly impacts its ability to meet financial obligations and service its debt.

These collection delays are further evidenced by a significant increase in trade receivables, as reported for the fiscal year ending March 31, 2023, underscoring the ongoing severity of this operational weakness.

| Financial Metric | Value | Period |

|---|---|---|

| Return on Equity (ROE) | -58.53% | Last 3 Years |

| Return on Capital Employed (ROCE) | -0.55% | Last 3 Years |

| EBITDA Margin | Low | Consistent Concern |

| Trade Receivables | Increased | FY Ending March 31, 2023 |

Preview Before You Purchase

Simplex Infrastructures SWOT Analysis

This preview reflects the real document you'll receive—professional, structured, and ready to use. You're viewing an actual excerpt from the complete Simplex Infrastructures SWOT analysis. Once purchased, you'll gain access to the full, detailed report, providing a comprehensive understanding of the company's strategic position.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Simplex Infrastructures possesses notable strengths in its diversified project portfolio and established market presence, but faces challenges from intense competition and fluctuating project timelines. Understanding these internal capabilities and external market dynamics is crucial for strategic planning.

Want the full story behind Simplex Infrastructures' strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Diverse Sectoral Expertise

Simplex Infrastructures boasts a remarkably diverse sectoral expertise, a significant strength that underpins its resilience and growth potential. The company's extensive portfolio covers a wide array of critical infrastructure segments, including buildings, industrial plants, power generation and transmission, urban development, marine projects, and transportation networks.

This broad sectoral reach is a key differentiator, mitigating risks associated with downturns in any single industry. For instance, in the fiscal year ending March 31, 2023, Simplex's order book reflected this diversification, with significant contributions from both building and transport infrastructure projects, showcasing its ability to secure business across varied economic cycles.

The company's proven track record in executing complex and challenging projects, such as the construction of elevated flyovers, modern airport terminals, and major bridges, further highlights its comprehensive capabilities. This depth of experience across different project types allows Simplex to adapt to evolving market demands and leverage opportunities in India's rapidly expanding infrastructure landscape.

Established Market Presence and Experience

Simplex Infrastructures boasts a deep-rooted presence in India's construction sector, built over decades. This extensive history translates into a robust brand reputation and a proven track record of successfully managing complex projects from start to finish.

The company's experience is underscored by its completion of numerous high-profile contracts, often earning commendation certificates from satisfied clients. For instance, in FY2023, Simplex reported a revenue of INR 3,368 crore, demonstrating its substantial operational scale and market engagement.

Public and Private Sector Client Base

Simplex Infrastructures' ability to serve both public and private sector clients is a significant strength, offering a diversified revenue base. This dual focus helps cushion the company against sector-specific downturns. For instance, in the fiscal year ending March 31, 2023, Simplex's order book demonstrated a healthy mix of government contracts and private sector projects, allowing for consistent project flow and revenue generation.

Operational Efficiency in Specific Areas

Simplex Infrastructures has demonstrated pockets of operational strength, notably in managing its Cash Conversion Cycle. This efficiency in converting working capital into cash is a vital asset, particularly within the often cash-intensive construction industry. For instance, as of the fiscal year ending March 31, 2024, the company's Cash Conversion Cycle was reported at 95 days, an improvement from 102 days in the previous year, signaling better working capital management.

This operational proficiency translates into tangible benefits:

- Improved Liquidity Management: A shorter cycle means cash is tied up for less time, enhancing the company's ability to meet short-term obligations.

- Reduced Working Capital Needs: Efficient conversion lowers the amount of capital required to fund day-to-day operations.

- Enhanced Financial Flexibility: Better cash flow generation provides greater capacity for reinvestment or debt reduction.

- Competitive Advantage: In an industry where cash flow is king, this operational strength can set Simplex apart from less efficient competitors.

Focus on Core Competencies

Simplex Infrastructures' vision centers on maintaining its leadership in foundation technology and general civil engineering. This dedicated focus on core competencies allows the company to harness deep specialized knowledge and extensive experience.

By concentrating on these niche areas within the construction sector, Simplex can cultivate significant competitive advantages. For instance, in the fiscal year ending March 31, 2023, Simplex Infrastructures reported revenue of INR 2,514.5 crore, with a substantial portion likely attributable to its specialized engineering and construction services.

- Leadership in Foundation Technology: Reinforces specialized expertise and market positioning.

- General Civil Engineering Strength: Leverages broad capabilities for diverse project needs.

- Competitive Advantage: Niche focus allows for deeper skill development and efficiency.

- Market Recognition: Sustained leadership implies strong client trust and project execution.

Simplex: Diversified Expertise & Operational Strength Powering Infrastructure

Simplex Infrastructures' diversified sectoral expertise is a significant advantage, allowing it to navigate different market conditions. Its broad portfolio, spanning buildings, industrial plants, power, and transportation, mitigates risks associated with any single sector's performance. This breadth was evident in its order book for the fiscal year ending March 31, 2023, which showed strong contributions from both building and transport infrastructure.

The company's proven track record in executing complex projects, such as elevated flyovers and airport terminals, demonstrates its comprehensive capabilities. This deep experience across various project types enables Simplex to adapt to evolving market demands and capitalize on India's infrastructure growth. For the fiscal year ending March 31, 2023, Simplex reported revenues of INR 3,368 crore, reflecting its substantial operational scale.

Simplex's ability to serve both public and private sector clients provides a diversified revenue base, enhancing its resilience against sector-specific downturns. The fiscal year ending March 31, 2023, saw a healthy mix of government and private projects in its order book, ensuring consistent project flow.

The company exhibits operational strength in managing its Cash Conversion Cycle, a critical factor in the construction industry. As of March 31, 2024, the cycle was 95 days, an improvement from 102 days in the prior year, indicating better working capital management and enhanced financial flexibility.

| Metric | FY Ending March 31, 2023 | FY Ending March 31, 2024 |

|---|---|---|

| Total Revenue (INR Crore) | 3,368 | Not Publicly Disclosed Yet |

| Cash Conversion Cycle (Days) | 102 | 95 |

What is included in the product

Delivers a strategic overview of Simplex Infrastructures’s internal and external business factors, highlighting its strengths, weaknesses, opportunities, and threats.

Offers a clear, actionable framework to identify and address Simplex Infrastructures' critical vulnerabilities and capitalize on its unique strengths.

Weaknesses

Significant Financial Losses and Declining Revenue

Simplex Infrastructures has faced considerable financial headwinds, marked by significant net losses and a pronounced downturn in revenue. For instance, the company experienced a substantial 73.53% decrease in net profit during the fourth quarter of the 2024-2025 fiscal year.

This financial strain is further evidenced by a 21.85% decline in sales for the same quarter. The company's revenue trajectory has been a consistent concern, showing a concerning compound annual growth rate (CAGR) of -23.4% over the last five years, highlighting a persistent struggle to maintain sales momentum.

Poor Liquidity and Debt Servicing Delays

Simplex Infrastructures faces significant challenges with its liquidity, resulting in persistent delays in meeting its debt obligations. This financial strain is a major concern for stakeholders.

Credit rating agencies have flagged Simplex Infrastructures by placing it under 'Issuer Not Cooperating' categories. This designation stems from a lack of sufficient information and ongoing defaults, underscoring the company's precarious financial health.

High Debt-to-Equity Ratio and Interest Costs

Simplex Infrastructures' high Debt-to-Equity ratio, reportedly around 2.2x as of March 2024, highlights a substantial reliance on borrowed funds. This leverage magnifies financial risk, particularly as interest expenses continue to climb, impacting profitability and cash flow availability.

Negative Profitability Ratios

Simplex Infrastructures faces significant challenges with its profitability, as evidenced by consistently weak key metrics. Over the last three years, the company has reported a concerning Return on Equity (ROE) of -58.53% and a Return on Capital Employed (ROCE) of -0.55%. These figures highlight a struggle to generate adequate returns for shareholders and efficiently utilize its capital base.

Further compounding these issues, the company's EBITDA margin has remained low, signaling difficulties in translating revenue into operational profits. This low margin suggests that operational costs are consuming a substantial portion of earnings, hindering the company's ability to cover its expenses and reinvest in growth.

- Poor Profitability: Negative ROE (-58.53%) and ROCE (-0.55%) over the past three years indicate weak financial performance.

- Low EBITDA Margin: Challenges in generating sufficient operating profits are evident from the consistently low EBITDA margin.

- Capital Inefficiency: The negative ROCE points to issues in effectively employing capital to generate returns.

Challenges in Recovering Client Dues

Simplex Infrastructures faces significant hurdles in collecting payments from its clients, a situation that has notably strained its liquidity. These delays, especially from government entities, directly impede the company's ability to manage its cash flow effectively. This directly impacts its capacity to meet its financial commitments, including debt servicing, creating a challenging financial environment.

The company's financial health is further complicated by these recovery delays. For instance, as of the fiscal year ending March 31, 2023, Simplex Infrastructures reported a substantial increase in its trade receivables. This rise, coupled with slow collection cycles, highlights the persistent nature of this weakness.

- Delayed Client Payments: Significant delays in receiving payments from clients, particularly government agencies, are a primary concern.

- Liquidity Strain: These payment delays directly contribute to a stretched liquidity position for the company.

- Impact on Debt Servicing: The inability to collect dues promptly hinders the company's ability to service its existing debt obligations.

- Trade Receivables Growth: An increase in trade receivables, as observed in recent financial reports, underscores the severity of the collection issue.

Infrastructure company faces severe profitability and liquidity issues

Simplex Infrastructures grapples with persistent profitability issues, reflected in a stark -58.53% Return on Equity and a -0.55% Return on Capital Employed over the last three years. This indicates a significant struggle to generate value for shareholders and efficiently utilize its capital base.

The company's operational efficiency is also hampered by a low EBITDA margin, suggesting that operating costs are disproportionately high relative to revenue, thereby limiting its capacity for reinvestment and debt coverage.

Furthermore, Simplex Infrastructures faces substantial liquidity challenges stemming from prolonged delays in client payments, particularly from government entities, which directly impacts its ability to meet financial obligations and service its debt.

These collection delays are further evidenced by a significant increase in trade receivables, as reported for the fiscal year ending March 31, 2023, underscoring the ongoing severity of this operational weakness.

| Financial Metric | Value | Period |

|---|---|---|

| Return on Equity (ROE) | -58.53% | Last 3 Years |

| Return on Capital Employed (ROCE) | -0.55% | Last 3 Years |

| EBITDA Margin | Low | Consistent Concern |

| Trade Receivables | Increased | FY Ending March 31, 2023 |

Preview Before You Purchase

Simplex Infrastructures SWOT Analysis

This preview reflects the real document you'll receive—professional, structured, and ready to use. You're viewing an actual excerpt from the complete Simplex Infrastructures SWOT analysis. Once purchased, you'll gain access to the full, detailed report, providing a comprehensive understanding of the company's strategic position.