Sinch PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, market economics, and rapid tech innovation are reshaping Sinch’s strategic outlook in our concise PESTLE snapshot—designed for investors and strategists who need clarity fast.

Our full PESTLE delivers granular analysis of political risks, consumer trends, and legal exposures that could impact revenue and valuation—perfect for due diligence or strategy sessions.

Buy the complete report to access editable insights, actionable risk forecasts, and competitive implications you can use immediately.

Political factors

Data Sovereignty Policies

As global pushes for digital sovereignty grow, Sinch faces fragmented laws on data residency—over 90 countries had data localization requirements by 2024—forcing localized infrastructure spend and partner deals to host customer data regionally.

Investing in local data centers or regional cloud providers adds capex and opex pressure; Sinch reported 2024 revenue of SEK 19.3bn, making targeted infrastructure allocations a material strategic cost.

Noncompliance risks include market exclusions and fines; several countries tightened rules in 2023–25, threatening access to high-growth APAC and EMEA markets if Sinch fails to align.

Geopolitical Trade Relations

Ongoing trade tensions between the US, EU and China—with global tariffs rising 8% on average for tech goods since 2021—disrupt hardware supply chains and cross-border digital service flows, impacting Sinch’s SMPP gateway deployments and device provisioning.

Sinch faces risks from sanctions or export controls that could restrict messaging to specific markets; in 2024 messaging revenues concentrated 62% in Americas+EMEA heighten exposure to regional policy shifts.

As a neutral Swedish company, Sinch’s EU base and diversified carrier agreements help mitigate geopolitical friction, supporting continuity amid escalating trade policy volatility.

Government Digital Transformation

Many governments accelerated public-service digitization during 2020–2024, with global e‑government development index rising 6% and public digital services spend estimated at $400 billion in 2024, creating demand for secure mobile comms; Sinch, with 2024 revenue of SEK 16.6 billion (~$1.6B) and strong messaging/security capabilities, is well‑positioned for citizen engagement, emergency alerts, and ID verification contracts; however, securing such deals requires rigorous political vetting, compliance, and high transparency standards.

Taxation of Digital Services

Implementation of OECD/G20 global minimum tax (15%) and country-level digital service taxes raises Sinch’s effective tax rate risk, potentially reducing 2024 adjusted EBITDA margin (26.1% in 2023) if passthroughs fail.

Political moves to tax multinationals more aggressively force Sinch to revise financial planning, restructuring and transfer pricing; 2024 tax provisions rose by an estimated mid-single-digit million SEK across peers.

Navigating these policies is critical to preserve investor confidence and support stable free cash flow (Sinch reported SEK 1.8bn FCF in 2023).

- Global minimum tax: 15% OECD/G20 standard; increases headline tax exposure

- Country DSTs: fragmented levies add compliance and potential double taxation

- Impact: pressure on EBITDA margin and FCF; necessitates tax planning and corporate adjustments

Regulatory Lobbying and Influence

Sinch actively lobbies telecom regulators on messaging standards and spam prevention, leveraging its 2024 revenue of SEK 22.6 billion to fund compliance and advocacy efforts.

EU political stability and harmonized digital rules enable Sinch to push standards internationally, affecting markets that account for over 60% of its ARR.

Shaping future telecom legislation is a strategic asset that can protect margins and support Sinch’s market share in the $100+ billion CPaaS sector.

- 2024 revenue SEK 22.6bn; >60% ARR from EU/regulated markets

- CPaaS total addressable market >$100bn

- Lobbying strengthens compliance, anti-spam policy influence

Regulatory fragmentation and taxes squeeze Sinch—rising localization costs erode FCF/EBITDA

Political fragmentation (90+ data localization laws by 2024) forces Sinch to localize infrastructure; 2024 revenue cited between SEK 19.3–22.6bn with ~60% ARR in regulated markets, raising capex/opex and compliance costs. OECD 15% global minimum tax and DSTs elevate effective tax risk, pressuring EBITDA/FCF (2023 EBITDA margin 26.1%, FCF SEK 1.8bn). Lobbying mitigates regulatory threats.

| Metric | Value |

|---|---|

| Data localization laws | 90+ |

| 2024 revenue | SEK 19.3–22.6bn |

| EU/regulated ARR | >60% |

| 2023 EBITDA margin | 26.1% |

| 2023 FCF | SEK 1.8bn |

What is included in the product

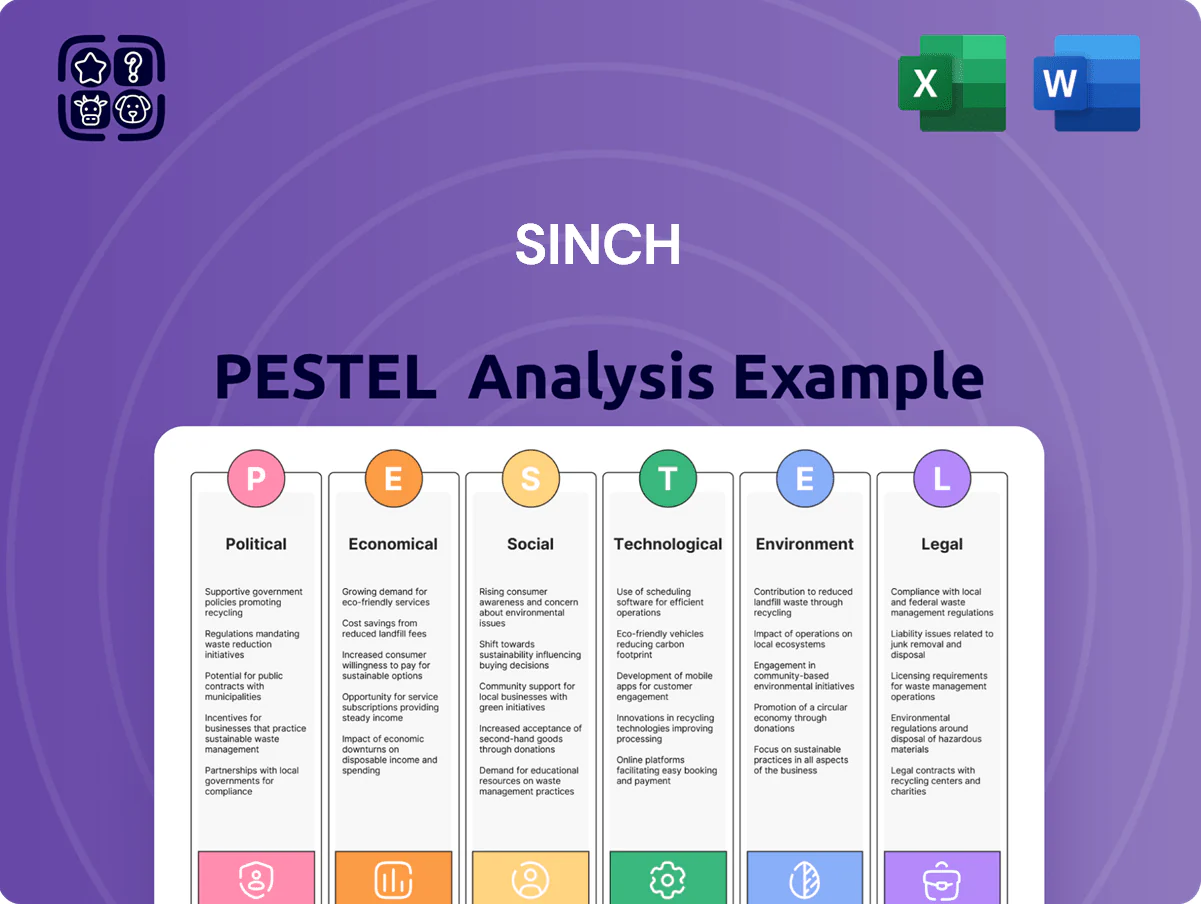

Explores how macro-environmental factors uniquely affect Sinch across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Sinch PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning during planning sessions.

Economic factors

Interest Rate Volatility

The macroeconomic environment of late 2025 remains shaped by central bank policies: the ECB deposit rate sat at 4.0% and the Fed funds target near 5.25% in Q4 2025, keeping interest-rate volatility elevated. For growth-focused Sinch, higher rates increase cost of debt and discount rates, lowering NPV of future cash flows and pressuring valuations. Elevated borrowing costs can deter M&A, while rate stabilization would enable refinancing and more aggressive expansion.

Currency Exchange Fluctuations

Operating in 60+ countries exposes Sinch to material transactional and translational FX risk; with 2024 revenue ~SEK 34.2bn and roughly 40–50% earned in USD/EUR, a 5% SEK strengthening could cut reported revenue by ~1.6–2.0% and compress margins similarly. Volatility in USD/SEK and EUR/SEK drove +/-6–8% quarterly EPS swings in 2023–2024, making hedging programs and localized pricing crucial to protect margins.

Global Inflationary Pressures

Persistent global inflation raised cloud and energy costs; Sinch reported gross margin pressure in 2024 as energy and bandwidth costs rose amid 6.8% global CPI (2024 OECD), squeezing telecoms and platform operators' margins.

Higher labor costs inflated R&D and support expenses; Sinch’s 2024 reported operating expenses grew ~9% YoY, while many enterprise clients faced reduced purchasing power, with US real wages still below 2019 levels.

Sinch can pass some costs via price adjustments, but prolonged inflation risks client cuts to marketing and engagement spend; automation and efficiency initiatives—e.g., platform consolidation—are critical to sustain EBITDA margins near 2024 levels.

Emerging Market Growth

Emerging market growth in Latin America and Southeast Asia offers Sinch a large addressable market as mobile connections exceed 1.2 billion in LATAM and 1.9 billion in SEA by 2025; rapid smartphone adoption and a projected middle‑class expansion (~100 million new consumers in SEA by 2030) drive higher demand for SMS and WhatsApp business messaging.

Sinch’s market capture hinges on local GDP stability—LATAM GDP growth ~2.3% (2024) and SEA ~4.5% (2024)—and regulatory, currency, and infrastructure risks that can accelerate or constrain revenue growth.

- LATAM mobile users >1.2B (2025 est.)

- SEA mobile users >1.9B (2025 est.)

- SEA middle class +~100M by 2030

- LATAM GDP growth ~2.3% (2024), SEA ~4.5% (2024)

Enterprise Spending Trends

Enterprise spending cycles drive Sinch revenue mix: during 2023–2025 slowdown signals, IDC noted global IT spending growth fell to about 3% in 2023, pushing firms to favor essential SMS/voice over omnichannel suites, likely compressing ASPs for Sinch.

When GDP growth rebounds—IMF projected 3.0% global growth in 2024—enterprises accelerate AI-driven CX adoption, benefiting Sinch’s cloud messaging and CPaaS upsell potential.

- 3% global IT spend growth in 2023 (IDC)

- IMF 2024 global GDP ~3.0%

- Downturns shift mix to core SMS/voice, lowering ASPs

- Growth favors AI/omnichannel upsells for Sinch

Higher rates, FX hit and rising costs squeeze Sinch margins despite emerging-market growth

Higher global rates (ECB 4.0%, Fed ~5.25% in Q4 2025) raise Sinch’s discount rates and borrowing costs, pressuring valuations; FX exposure (40–50% USD/EUR; 5% SEK strengthening → ~1.6–2.0% revenue hit) and inflation-driven cloud/energy/labor cost rises compressed 2024 margins; emerging markets (LATAM users >1.2B, SEA >1.9B; GDP LATAM ~2.3%, SEA ~4.5% in 2024) offer growth but carry currency and regulatory risk.

| Metric | Value |

|---|---|

| 2024 Revenue | ~SEK 34.2bn |

| USD/EUR share | 40–50% |

| FX sensitivity | 5% SEK ↑ → −1.6–2.0% rev |

| ECB / Fed (Q4 2025) | 4.0% / ~5.25% |

| LATAM / SEA users (2025) | >1.2B / >1.9B |

| GDP growth (2024) | LATAM ~2.3%, SEA ~4.5% |

Preview Before You Purchase

Sinch PESTLE Analysis

The preview shown here is the exact Sinch PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, market economics, and rapid tech innovation are reshaping Sinch’s strategic outlook in our concise PESTLE snapshot—designed for investors and strategists who need clarity fast.

Our full PESTLE delivers granular analysis of political risks, consumer trends, and legal exposures that could impact revenue and valuation—perfect for due diligence or strategy sessions.

Buy the complete report to access editable insights, actionable risk forecasts, and competitive implications you can use immediately.

Political factors

Data Sovereignty Policies

As global pushes for digital sovereignty grow, Sinch faces fragmented laws on data residency—over 90 countries had data localization requirements by 2024—forcing localized infrastructure spend and partner deals to host customer data regionally.

Investing in local data centers or regional cloud providers adds capex and opex pressure; Sinch reported 2024 revenue of SEK 19.3bn, making targeted infrastructure allocations a material strategic cost.

Noncompliance risks include market exclusions and fines; several countries tightened rules in 2023–25, threatening access to high-growth APAC and EMEA markets if Sinch fails to align.

Geopolitical Trade Relations

Ongoing trade tensions between the US, EU and China—with global tariffs rising 8% on average for tech goods since 2021—disrupt hardware supply chains and cross-border digital service flows, impacting Sinch’s SMPP gateway deployments and device provisioning.

Sinch faces risks from sanctions or export controls that could restrict messaging to specific markets; in 2024 messaging revenues concentrated 62% in Americas+EMEA heighten exposure to regional policy shifts.

As a neutral Swedish company, Sinch’s EU base and diversified carrier agreements help mitigate geopolitical friction, supporting continuity amid escalating trade policy volatility.

Government Digital Transformation

Many governments accelerated public-service digitization during 2020–2024, with global e‑government development index rising 6% and public digital services spend estimated at $400 billion in 2024, creating demand for secure mobile comms; Sinch, with 2024 revenue of SEK 16.6 billion (~$1.6B) and strong messaging/security capabilities, is well‑positioned for citizen engagement, emergency alerts, and ID verification contracts; however, securing such deals requires rigorous political vetting, compliance, and high transparency standards.

Taxation of Digital Services

Implementation of OECD/G20 global minimum tax (15%) and country-level digital service taxes raises Sinch’s effective tax rate risk, potentially reducing 2024 adjusted EBITDA margin (26.1% in 2023) if passthroughs fail.

Political moves to tax multinationals more aggressively force Sinch to revise financial planning, restructuring and transfer pricing; 2024 tax provisions rose by an estimated mid-single-digit million SEK across peers.

Navigating these policies is critical to preserve investor confidence and support stable free cash flow (Sinch reported SEK 1.8bn FCF in 2023).

- Global minimum tax: 15% OECD/G20 standard; increases headline tax exposure

- Country DSTs: fragmented levies add compliance and potential double taxation

- Impact: pressure on EBITDA margin and FCF; necessitates tax planning and corporate adjustments

Regulatory Lobbying and Influence

Sinch actively lobbies telecom regulators on messaging standards and spam prevention, leveraging its 2024 revenue of SEK 22.6 billion to fund compliance and advocacy efforts.

EU political stability and harmonized digital rules enable Sinch to push standards internationally, affecting markets that account for over 60% of its ARR.

Shaping future telecom legislation is a strategic asset that can protect margins and support Sinch’s market share in the $100+ billion CPaaS sector.

- 2024 revenue SEK 22.6bn; >60% ARR from EU/regulated markets

- CPaaS total addressable market >$100bn

- Lobbying strengthens compliance, anti-spam policy influence

Regulatory fragmentation and taxes squeeze Sinch—rising localization costs erode FCF/EBITDA

Political fragmentation (90+ data localization laws by 2024) forces Sinch to localize infrastructure; 2024 revenue cited between SEK 19.3–22.6bn with ~60% ARR in regulated markets, raising capex/opex and compliance costs. OECD 15% global minimum tax and DSTs elevate effective tax risk, pressuring EBITDA/FCF (2023 EBITDA margin 26.1%, FCF SEK 1.8bn). Lobbying mitigates regulatory threats.

| Metric | Value |

|---|---|

| Data localization laws | 90+ |

| 2024 revenue | SEK 19.3–22.6bn |

| EU/regulated ARR | >60% |

| 2023 EBITDA margin | 26.1% |

| 2023 FCF | SEK 1.8bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Sinch across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Sinch PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning during planning sessions.

Economic factors

Interest Rate Volatility

The macroeconomic environment of late 2025 remains shaped by central bank policies: the ECB deposit rate sat at 4.0% and the Fed funds target near 5.25% in Q4 2025, keeping interest-rate volatility elevated. For growth-focused Sinch, higher rates increase cost of debt and discount rates, lowering NPV of future cash flows and pressuring valuations. Elevated borrowing costs can deter M&A, while rate stabilization would enable refinancing and more aggressive expansion.

Currency Exchange Fluctuations

Operating in 60+ countries exposes Sinch to material transactional and translational FX risk; with 2024 revenue ~SEK 34.2bn and roughly 40–50% earned in USD/EUR, a 5% SEK strengthening could cut reported revenue by ~1.6–2.0% and compress margins similarly. Volatility in USD/SEK and EUR/SEK drove +/-6–8% quarterly EPS swings in 2023–2024, making hedging programs and localized pricing crucial to protect margins.

Global Inflationary Pressures

Persistent global inflation raised cloud and energy costs; Sinch reported gross margin pressure in 2024 as energy and bandwidth costs rose amid 6.8% global CPI (2024 OECD), squeezing telecoms and platform operators' margins.

Higher labor costs inflated R&D and support expenses; Sinch’s 2024 reported operating expenses grew ~9% YoY, while many enterprise clients faced reduced purchasing power, with US real wages still below 2019 levels.

Sinch can pass some costs via price adjustments, but prolonged inflation risks client cuts to marketing and engagement spend; automation and efficiency initiatives—e.g., platform consolidation—are critical to sustain EBITDA margins near 2024 levels.

Emerging Market Growth

Emerging market growth in Latin America and Southeast Asia offers Sinch a large addressable market as mobile connections exceed 1.2 billion in LATAM and 1.9 billion in SEA by 2025; rapid smartphone adoption and a projected middle‑class expansion (~100 million new consumers in SEA by 2030) drive higher demand for SMS and WhatsApp business messaging.

Sinch’s market capture hinges on local GDP stability—LATAM GDP growth ~2.3% (2024) and SEA ~4.5% (2024)—and regulatory, currency, and infrastructure risks that can accelerate or constrain revenue growth.

- LATAM mobile users >1.2B (2025 est.)

- SEA mobile users >1.9B (2025 est.)

- SEA middle class +~100M by 2030

- LATAM GDP growth ~2.3% (2024), SEA ~4.5% (2024)

Enterprise Spending Trends

Enterprise spending cycles drive Sinch revenue mix: during 2023–2025 slowdown signals, IDC noted global IT spending growth fell to about 3% in 2023, pushing firms to favor essential SMS/voice over omnichannel suites, likely compressing ASPs for Sinch.

When GDP growth rebounds—IMF projected 3.0% global growth in 2024—enterprises accelerate AI-driven CX adoption, benefiting Sinch’s cloud messaging and CPaaS upsell potential.

- 3% global IT spend growth in 2023 (IDC)

- IMF 2024 global GDP ~3.0%

- Downturns shift mix to core SMS/voice, lowering ASPs

- Growth favors AI/omnichannel upsells for Sinch

Higher rates, FX hit and rising costs squeeze Sinch margins despite emerging-market growth

Higher global rates (ECB 4.0%, Fed ~5.25% in Q4 2025) raise Sinch’s discount rates and borrowing costs, pressuring valuations; FX exposure (40–50% USD/EUR; 5% SEK strengthening → ~1.6–2.0% revenue hit) and inflation-driven cloud/energy/labor cost rises compressed 2024 margins; emerging markets (LATAM users >1.2B, SEA >1.9B; GDP LATAM ~2.3%, SEA ~4.5% in 2024) offer growth but carry currency and regulatory risk.

| Metric | Value |

|---|---|

| 2024 Revenue | ~SEK 34.2bn |

| USD/EUR share | 40–50% |

| FX sensitivity | 5% SEK ↑ → −1.6–2.0% rev |

| ECB / Fed (Q4 2025) | 4.0% / ~5.25% |

| LATAM / SEA users (2025) | >1.2B / >1.9B |

| GDP growth (2024) | LATAM ~2.3%, SEA ~4.5% |

Preview Before You Purchase

Sinch PESTLE Analysis

The preview shown here is the exact Sinch PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use immediately.