Sino Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

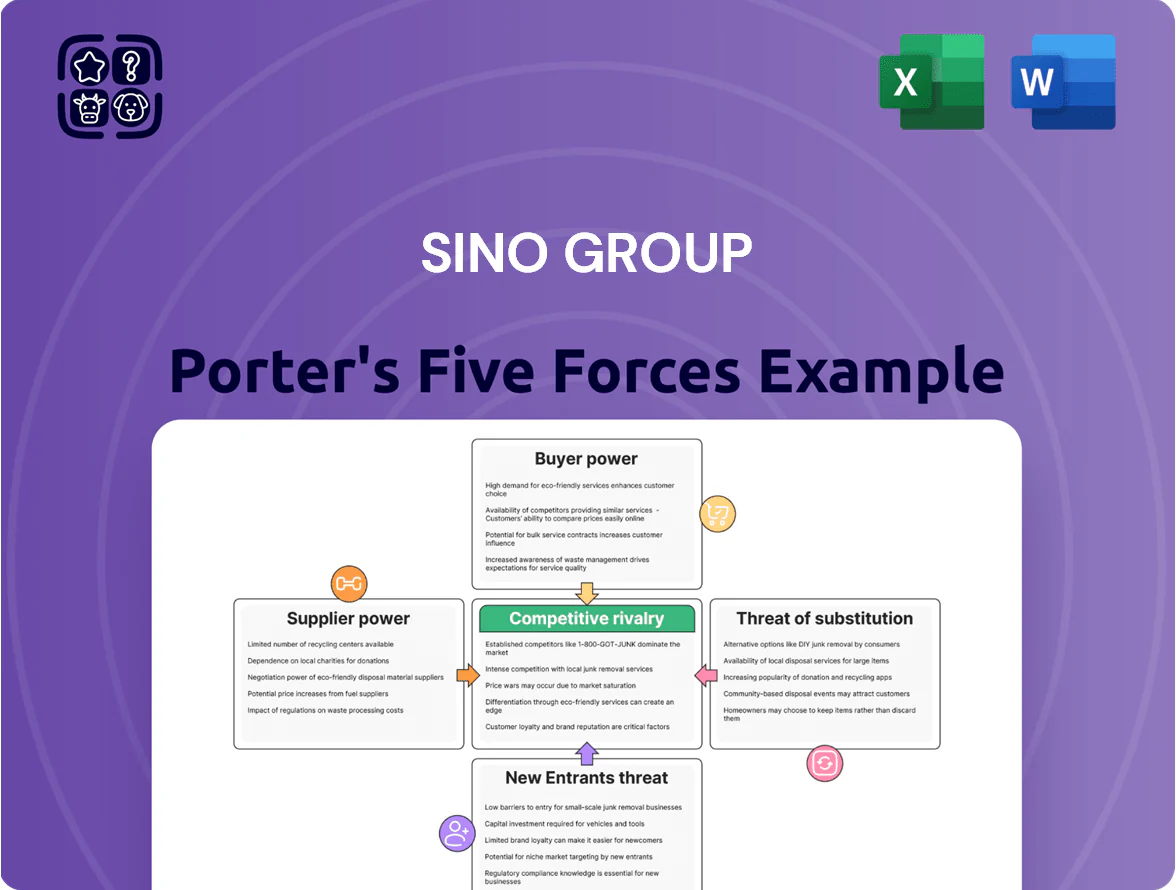

Sino Group faces moderate buyer power and regulatory headwinds, while high capital intensity and established local rivals limit new entrants and intensify rivalry; supplier leverage and substitution risks remain manageable but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sino Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Land Supply

The Hong Kong Government remains the main land supplier, running auctions and tenders that set market price; in 2025 it released 120 hectares in the Northern Metropolis, easing pressure slightly but keeping control.

Prime urban land scarcity keeps supplier pricing power high: Hong Kong residential land prices averaged HKD 18,500/sq ft in 2024, so land costs keep Sino Group’s margins under pressure.

Sino must budget higher acquisition costs—land bids often consume 30–40% of project value—affecting its development pipeline and long-term returns.

Construction Labor Shortages

The 2025 Hong Kong construction sector reports a 15–20% shortfall in skilled workers versus demand, pushing average site wages up about 22% year-on-year and boosting unions and specialist contractors' bargaining leverage over developers like Sino Group.

Sino Group has scaled modular integrated construction and automation, cutting on-site labour hours by an estimated 30% on pilot projects in 2024–25 to blunt supplier power.

Still, higher labour costs remain a persistent fixed drag, increasing development unit costs by roughly 8–12% across residential and commercial projects in 2025.

Specialized Architectural and Engineering Services

Sino Group depends on a narrow set of top-tier international architectural and engineering firms for high-end luxury and green projects, giving suppliers strong bargaining power through unique design expertise and brand prestige.

By 2025, ESG rules tightened and certified green consultants grew scarce; industry reports show demand up ~35% vs 2020, letting these specialists charge 15–30% premium fees to secure LEED/BEAM Plus/BREEAM compliance.

Raw Material Price Volatility

Raw material costs for steel, cement and glass swing with global supply chains and geopolitics; Sino Group can negotiate on volume but remains a price-taker—HKD construction steel rebar rose ~18% in 2024 and global cement prices climbed ~9% that year.

By late 2025 demand for low-carbon materials cut the supplier pool; certified green concrete and low‑carbon glass suppliers command 10–25% price premia, giving those suppliers added bargaining leverage in procurement.

- Steel rebar +18% in 2024

- Cement +9% in 2024

- Green-material price premia 10–25% (late 2025)

- Sino: volume leverage, still price-taker

Technology and PropTech Infrastructure

As Sino Group adds smart-home and AI property-management systems, it relies on specialized vendors whose proprietary software creates high switching costs; Gartner estimated global proptech spend hit US$30.6bn in 2024, concentrating power with platform owners.

Sino’s venture arm (invested ~HK$450m in proptech by 2025) reduces some vendor risk, but dominant cloud and IoT providers still drive core infrastructure costs and contract terms, keeping supplier bargaining power high.

- High vendor dependence from integrated smart systems

- Proprietary platforms = high switching costs

- Gartner: US$30.6bn proptech spend (2024)

- Sino VC ~HK$450m in proptech by 2025

- Big cloud/IoT providers control core infra pricing

Suppliers Dictate Costs: Land, Labour & Materials Surge; Sino Cuts Hours but Remains Price-Taker

Suppliers hold high bargaining power: government land control keeps prices elevated (HKD 18,500/sq ft avg 2024; 120 ha released in 2025), labour shortfall lifts wages ~22% (2025), materials rose—steel +18% (2024), cement +9% (2024)—and green materials demand premiums 10–25% (late 2025); Sino offsets via modular build (-30% site hours) and HK$450m proptech VC but remains price-taker.

| Metric | Value |

|---|---|

| Land price (2024) | HKD 18,500/sq ft |

| Land released (2025) | 120 ha |

| Wage rise (2025) | ~22% |

| Steel (2024) | +18% |

| Cement (2024) | +9% |

| Green premia (late 2025) | 10–25% |

| Modular hours cut | -30% |

| Proptech VC (by 2025) | HK$450m |

What is included in the product

Tailored Porter's Five Forces for Sino Group, uncovering competitive pressures, buyer/supplier power, substitution risks, and entry barriers to assess strategic positioning and profitability drivers.

Compact Porter's Five Forces snapshot for Sino Group—quickly pinpoint competitive pressures and strategic reliefs to inform investment decisions.

Customers Bargaining Power

Residential Buyer Price Sensitivity

By end-2025 Hong Kong residential buyers are highly selective after prolonged rate volatility and weak GDP growth; transactions fell 18% year-on-year to ~38,000 units in 2025, shifting bargaining power to customers.

Buyers demand higher-quality finishes and amenities at existing price points, forcing Sino Group to offer competitive financing and incentives; new-home unsold stock reached ~12,000 units in mid-2025, boosting buyer leverage via the secondary market.

Commercial Tenant Leverage in Office Sectors

The Hong Kong office market, especially Kowloon East, still shows high vacancy—about 14.8% citywide and near 18% in Kowloon East by Q4 2025—giving corporate tenants strong bargaining power. Tenants now extract longer rent-free periods (commonly 6–12 months) and flexible lease clauses, pressuring effective rents down by 5–12% year-on-year. Sino Group must invest in asset enhancement and top-tier property management to retain high-value tenants with many relocation options. Hybrid work has cut peak demand, shifting supply-demand balance decisively toward tenants.

Retail Tenant Demands for Revenue Sharing

Retailers increasingly prefer turnover leases; by 2024 about 28% of Hong Kong mall agreements moved to revenue-sharing to limit retailer risk, boosting tenant leverage over Sino Group.

Revenue-share deals make Sino Group co‑risk bearer, reducing fixed income predictability—mall rental volatility rose ~6% YoY in 2023 when turnover clauses expanded.

Experiential retail pushes tenants to demand marketing funding and digital integration; top tenants now seek co‑marketing budgets equal to 3–5% of turnover.

Sino’s skill in curating exclusive tenant mixes and driving footfall (average mall NOI growth 2021–24: ~4.2% annually) is vital to retain negotiation leverage.

Hotel Guest Expectations and Digital Transparency

Hotel guests now see real-time prices and reviews via OTAs and meta-search: global OTA share reached ~60% of online bookings in 2024, raising switching rates and price sensitivity.

By 2025 guests can instantly compare substitutes across Greater China and ASEAN leisure corridors, so Sino Group must boost service quality and targeted loyalty to cut churn.

Higher guest power means dynamic pricing erodes margins; loyalty programs and standout F&B or wellness offerings can raise retention and RevPAR.

- OTA/meta share ~60% (2024)

- Real-time reviews driving switches

- High regional substitute availability

- Focus: service, loyalty, unique amenities

Institutional Investor Influence

Institutional investors in Sino Group’s investment-property and REIT activities demand high transparency and strong ESG (environmental, social, governance) performance, pushing capital toward developers meeting strict sustainability criteria.

By 2025, studies show ESG-linked financing can change cost of capital by up to 50 basis points, so non-financial metrics now materially affect valuation and indirect investor power over management.

Sino must align operations and reporting with these expectations to retain favorable valuations and REIT investor demand.

- ESG-linked cost of capital impact: ~50 bps (2025)

- Institutional demand: higher transparency + sustainability

- Investor influence: redirects capital, shapes strategy

- Action: align operations, improve ESG reporting

Customers Drive Pressure on Sino Group: Sales Slide, High Vacancy & ESG Cost Hits

Customers hold strong bargaining power across Sino Group’s segments in 2025: residential transactions down 18% to ~38,000 units; unsold stock ~12,000; office vacancy HK ~14.8% (Kowloon East ~18%); rent-free periods 6–12 months; mall revenue-share ~28%; OTA share ~60%; ESG-linked financing impacts cost of capital ~50 bps.

| Metric | 2025/2024 |

|---|---|

| Resi transactions | ~38,000 (-18% YoY) |

| Unsold stock | ~12,000 units |

| Office vacancy | HK 14.8%; Kowloon E ~18% |

| Mall rev-share | ~28% |

| OTA share | ~60% (2024) |

| ESG cost impact | ~50 bps |

Preview Before You Purchase

Sino Group Porter's Five Forces Analysis

This preview shows the exact Sino Group Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're looking at the actual, final deliverable—fully ready for immediate use with clear insights into competitive rivalry, buyer/supplier power, entry threats, and substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Sino Group faces moderate buyer power and regulatory headwinds, while high capital intensity and established local rivals limit new entrants and intensify rivalry; supplier leverage and substitution risks remain manageable but evolving. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sino Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Land Supply

The Hong Kong Government remains the main land supplier, running auctions and tenders that set market price; in 2025 it released 120 hectares in the Northern Metropolis, easing pressure slightly but keeping control.

Prime urban land scarcity keeps supplier pricing power high: Hong Kong residential land prices averaged HKD 18,500/sq ft in 2024, so land costs keep Sino Group’s margins under pressure.

Sino must budget higher acquisition costs—land bids often consume 30–40% of project value—affecting its development pipeline and long-term returns.

Construction Labor Shortages

The 2025 Hong Kong construction sector reports a 15–20% shortfall in skilled workers versus demand, pushing average site wages up about 22% year-on-year and boosting unions and specialist contractors' bargaining leverage over developers like Sino Group.

Sino Group has scaled modular integrated construction and automation, cutting on-site labour hours by an estimated 30% on pilot projects in 2024–25 to blunt supplier power.

Still, higher labour costs remain a persistent fixed drag, increasing development unit costs by roughly 8–12% across residential and commercial projects in 2025.

Specialized Architectural and Engineering Services

Sino Group depends on a narrow set of top-tier international architectural and engineering firms for high-end luxury and green projects, giving suppliers strong bargaining power through unique design expertise and brand prestige.

By 2025, ESG rules tightened and certified green consultants grew scarce; industry reports show demand up ~35% vs 2020, letting these specialists charge 15–30% premium fees to secure LEED/BEAM Plus/BREEAM compliance.

Raw Material Price Volatility

Raw material costs for steel, cement and glass swing with global supply chains and geopolitics; Sino Group can negotiate on volume but remains a price-taker—HKD construction steel rebar rose ~18% in 2024 and global cement prices climbed ~9% that year.

By late 2025 demand for low-carbon materials cut the supplier pool; certified green concrete and low‑carbon glass suppliers command 10–25% price premia, giving those suppliers added bargaining leverage in procurement.

- Steel rebar +18% in 2024

- Cement +9% in 2024

- Green-material price premia 10–25% (late 2025)

- Sino: volume leverage, still price-taker

Technology and PropTech Infrastructure

As Sino Group adds smart-home and AI property-management systems, it relies on specialized vendors whose proprietary software creates high switching costs; Gartner estimated global proptech spend hit US$30.6bn in 2024, concentrating power with platform owners.

Sino’s venture arm (invested ~HK$450m in proptech by 2025) reduces some vendor risk, but dominant cloud and IoT providers still drive core infrastructure costs and contract terms, keeping supplier bargaining power high.

- High vendor dependence from integrated smart systems

- Proprietary platforms = high switching costs

- Gartner: US$30.6bn proptech spend (2024)

- Sino VC ~HK$450m in proptech by 2025

- Big cloud/IoT providers control core infra pricing

Suppliers Dictate Costs: Land, Labour & Materials Surge; Sino Cuts Hours but Remains Price-Taker

Suppliers hold high bargaining power: government land control keeps prices elevated (HKD 18,500/sq ft avg 2024; 120 ha released in 2025), labour shortfall lifts wages ~22% (2025), materials rose—steel +18% (2024), cement +9% (2024)—and green materials demand premiums 10–25% (late 2025); Sino offsets via modular build (-30% site hours) and HK$450m proptech VC but remains price-taker.

| Metric | Value |

|---|---|

| Land price (2024) | HKD 18,500/sq ft |

| Land released (2025) | 120 ha |

| Wage rise (2025) | ~22% |

| Steel (2024) | +18% |

| Cement (2024) | +9% |

| Green premia (late 2025) | 10–25% |

| Modular hours cut | -30% |

| Proptech VC (by 2025) | HK$450m |

What is included in the product

Tailored Porter's Five Forces for Sino Group, uncovering competitive pressures, buyer/supplier power, substitution risks, and entry barriers to assess strategic positioning and profitability drivers.

Compact Porter's Five Forces snapshot for Sino Group—quickly pinpoint competitive pressures and strategic reliefs to inform investment decisions.

Customers Bargaining Power

Residential Buyer Price Sensitivity

By end-2025 Hong Kong residential buyers are highly selective after prolonged rate volatility and weak GDP growth; transactions fell 18% year-on-year to ~38,000 units in 2025, shifting bargaining power to customers.

Buyers demand higher-quality finishes and amenities at existing price points, forcing Sino Group to offer competitive financing and incentives; new-home unsold stock reached ~12,000 units in mid-2025, boosting buyer leverage via the secondary market.

Commercial Tenant Leverage in Office Sectors

The Hong Kong office market, especially Kowloon East, still shows high vacancy—about 14.8% citywide and near 18% in Kowloon East by Q4 2025—giving corporate tenants strong bargaining power. Tenants now extract longer rent-free periods (commonly 6–12 months) and flexible lease clauses, pressuring effective rents down by 5–12% year-on-year. Sino Group must invest in asset enhancement and top-tier property management to retain high-value tenants with many relocation options. Hybrid work has cut peak demand, shifting supply-demand balance decisively toward tenants.

Retail Tenant Demands for Revenue Sharing

Retailers increasingly prefer turnover leases; by 2024 about 28% of Hong Kong mall agreements moved to revenue-sharing to limit retailer risk, boosting tenant leverage over Sino Group.

Revenue-share deals make Sino Group co‑risk bearer, reducing fixed income predictability—mall rental volatility rose ~6% YoY in 2023 when turnover clauses expanded.

Experiential retail pushes tenants to demand marketing funding and digital integration; top tenants now seek co‑marketing budgets equal to 3–5% of turnover.

Sino’s skill in curating exclusive tenant mixes and driving footfall (average mall NOI growth 2021–24: ~4.2% annually) is vital to retain negotiation leverage.

Hotel Guest Expectations and Digital Transparency

Hotel guests now see real-time prices and reviews via OTAs and meta-search: global OTA share reached ~60% of online bookings in 2024, raising switching rates and price sensitivity.

By 2025 guests can instantly compare substitutes across Greater China and ASEAN leisure corridors, so Sino Group must boost service quality and targeted loyalty to cut churn.

Higher guest power means dynamic pricing erodes margins; loyalty programs and standout F&B or wellness offerings can raise retention and RevPAR.

- OTA/meta share ~60% (2024)

- Real-time reviews driving switches

- High regional substitute availability

- Focus: service, loyalty, unique amenities

Institutional Investor Influence

Institutional investors in Sino Group’s investment-property and REIT activities demand high transparency and strong ESG (environmental, social, governance) performance, pushing capital toward developers meeting strict sustainability criteria.

By 2025, studies show ESG-linked financing can change cost of capital by up to 50 basis points, so non-financial metrics now materially affect valuation and indirect investor power over management.

Sino must align operations and reporting with these expectations to retain favorable valuations and REIT investor demand.

- ESG-linked cost of capital impact: ~50 bps (2025)

- Institutional demand: higher transparency + sustainability

- Investor influence: redirects capital, shapes strategy

- Action: align operations, improve ESG reporting

Customers Drive Pressure on Sino Group: Sales Slide, High Vacancy & ESG Cost Hits

Customers hold strong bargaining power across Sino Group’s segments in 2025: residential transactions down 18% to ~38,000 units; unsold stock ~12,000; office vacancy HK ~14.8% (Kowloon East ~18%); rent-free periods 6–12 months; mall revenue-share ~28%; OTA share ~60%; ESG-linked financing impacts cost of capital ~50 bps.

| Metric | 2025/2024 |

|---|---|

| Resi transactions | ~38,000 (-18% YoY) |

| Unsold stock | ~12,000 units |

| Office vacancy | HK 14.8%; Kowloon E ~18% |

| Mall rev-share | ~28% |

| OTA share | ~60% (2024) |

| ESG cost impact | ~50 bps |

Preview Before You Purchase

Sino Group Porter's Five Forces Analysis

This preview shows the exact Sino Group Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're looking at the actual, final deliverable—fully ready for immediate use with clear insights into competitive rivalry, buyer/supplier power, entry threats, and substitutes.