Sinocare Boston Consulting Group Matrix

Unlock Strategic Clarity

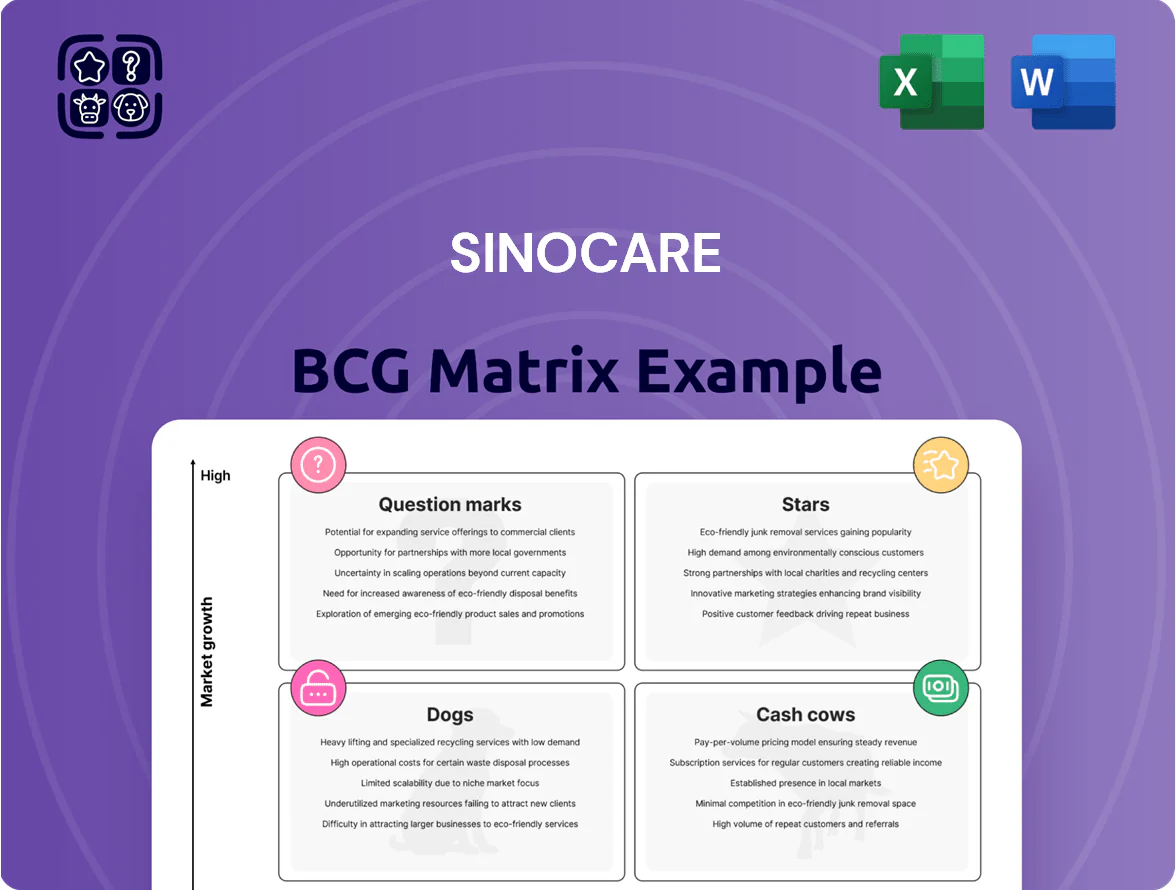

Sinocare’s BCG Matrix preview highlights how its glucose monitoring and diabetes management products compete across growth and market-share axes, hinting at which offerings are potential Stars or Cash Cows and which may be underperforming; this snapshot is ideal for investors and strategists sizing opportunity and risk.

Get the full BCG Matrix report for a quadrant-by-quadrant breakdown, actionable strategic moves, and editable Word plus Excel files—purchase now to shortcut research and make confident product and capital-allocation decisions.

Stars

Continuous Glucose Monitoring Systems

The iCan CGM series is Sinocare’s high-growth flagship, using third-generation sensors to compete in a CGM market growing at ~17% CAGR (2020–25) and valued at ~$12.5B in 2025.

By late 2025, partnerships with A. Menarini Diagnostics have placed iCan in 20+ European jurisdictions, capturing a leading share in the premium segment—estimated 8–12% share in served markets.

iCan drives top-line revenue but demands heavy R&D and marketing spend—Sinocare invested ~RMB 420M in diabetes R&D in 2024—to sustain competitiveness vs. global rivals like Abbott.

Integrated Digital Diabetes Platforms

Sinocare’s Integrated Digital Diabetes Platforms are Stars: SinoGPT AI and the digital management ecosystem shifted the company from device maker to service provider, tapping the market move to data-driven chronic care in hospitals and homes.

By 2025 these platforms cover 4,000+ Chinese hospitals and generated an estimated 28–35% higher ARPU versus devices alone, so Sinocare must keep investing in IoT integration and personalized care to sustain growth.

Multi-Parameter POCT Devices

The Precision Desk Lab and advanced iPOCT units for glucose, uric acid, and ketones are Sinocare’s Stars: in 2025 they captured ~28% share of China’s professional POCT market and drove 42% of Sinocare’s device revenue (¥1.12bn of ¥2.67bn YTD), reflecting fast clinical adoption amid healthcare decentralization.

They produce strong cash inflows but require rapid R&D spend—Sinocare increased iPOCT R&D 34% YoY in 2024–25—keeping these products in the Star quadrant as of end-2025.

Trividia Health International Portfolio

Through the 2023 acquisition of U.S.-based Trividia Health, Sinocare captured a leading share in North American retail glucose monitoring: TRUE brand presence in 55,000+ outlets (Walgreens, CVS) reaches an estimated 4–6 million users, boosting Sinocare’s international revenue—U.S. contributed about 18% of group sales in 2024.

Integration of Chinese R&D with U.S. manufacturing accelerates product pipeline and gross margins, but the segment stays capital-intensive: logistics, FDA/CE compliance and warranty reserves keep capex and OPEX elevated.

- TRUE in 55,000+ outlets

- 4–6M users (est.)

- U.S. ~18% of 2024 sales

- Higher capex for compliance/logistics

Smart Hypertension Monitoring Solutions

Sinocare’s Smart Hypertension Monitoring Solutions, launched under the Biosensing Plus strategy, entered the chronic disease market in 2023 and hit double-digit CAGR adoption, reaching an estimated $24M revenue run-rate by Q4 2025.

Bundling with Sinocare’s diabetes meters and apps raised stickiness: cross-sell lifted ARPU ~28% and drove a 6-point market-share gain vs traditional BP device makers in China by 2025.

To keep momentum, Sinocare must invest in aggressive promotion and channel expansion through 2025; without a 15–20% marketing uplift, leadership vs established med-dev incumbents could slip.

- Revenue run-rate Q4 2025: $24M

- ARPU increase from bundling: ~28%

- Market-share gain vs incumbents: +6 pts (China, 2023–2025)

- Required marketing uplift to secure lead: 15–20%

Sinocare’s flagship suite fuels rapid 2025 growth—CGM, iPOCT, TRUE, Smart BP surge

Sinocare’s Stars (iCan CGM, Integrated Digital Platforms, iPOCT, TRUE, Smart BP) drove rapid growth by 2025: iCan ~8–12% share in served EU markets; CGM market ~$12.5B (2025); iPOCT 28% China share, ¥1.12bn of ¥2.67bn YTD device revenue; TRUE in 55,000+ US outlets (~4–6M users); Smart BP $24M run-rate Q4 2025.

| Product | Key 2025 metrics |

|---|---|

| iCan CGM | 8–12% served-market share; market $12.5B |

| iPOCT | 28% China share; ¥1.12bn device rev |

| TRUE | 55,000+ outlets; 4–6M users |

| Smart BP | $24M run-rate Q4 2025 |

What is included in the product

Comprehensive BCG Matrix review of Sinocare’s portfolio with quadrant strategies, investment priorities, and trend-driven risks/opportunities.

One-page Sinocare BCG Matrix mapping each unit for quick strategic decisions, export-ready for seamless PowerPoint integration.

Cash Cows

Retail Blood Glucose Meters

Sinocare holds ~50% share of China’s retail blood glucose meter market, addressing >140 million people with diabetes in China (IDF 2023 est.), making this a stable, high-volume cash cow.

Low marketing and R&D for mature strip-and-meter sales mean these products produce most free cash flow; in 2024 Sinocare reported ~RMB 1.2 billion operating cash flow, largely from this segment.

Those steady profits fund next-gen CGM and AI projects, covering upfront R&D and pilot production without diluting equity or large debt increases.

Traditional Blood Glucose Test Strips

Test strips are a high-margin, recurring cash cow for Sinocare, driven by millions of installed meters and a 2024 estimated market share around 28% in China’s BGM strip segment; low BGM market growth (~2% CAGR 2023–2028) and strong customer loyalty keep unit economics favorable. The consumables business has minimal capex and SG&A per unit, generating roughly RMB 450–600 million in annual operating cashflow (2024 est.), which funds debt service and fuels 2025–26 international expansion.

Legacy Safe-Accu Product Series

The Legacy Safe-Accu product series sells over 12 million units annually in China, generating high gross margins (estimated 30–35% in 2024) due to scale and optimized supply chains, making it a consistent cash cow for Sinocare.

PTS Diagnostics Lipid Analyzers

The CardioChek family of lipid analyzers, acquired via PTS Diagnostics in 2021, dominates the global point-of-care lipid testing niche with an estimated $85–95M annual revenue run-rate in 2024 and ~18% global market share in handheld analyzers.

Operating in a mature segment, demand from clinics and pharmacies is steady, yielding consistent cash flow but low mid-single-digit growth forecasts (2–4% CAGR to 2028), making it a classic Cash Cow for Sinocare.

It provides reliable international revenue—roughly 12–15% of Sinocare’s FY2024 revenue—and funds expansion in chronic disease management devices and R&D.

- 2024 run-rate $85–95M; ~18% handheld share

- Low growth: 2–4% CAGR to 2028

- Contributes ~12–15% of Sinocare FY2024 revenue

Hospital-Grade Glycemic Management Systems

Sinocare’s hospital-grade glycemic management systems hold ~45% share in China’s inpatient BGM segment (2024), delivering stable annual revenue ~RMB 430m and consistent gross margin ~52%, making them a reliable cash cow for the group.

With basic in-hospital BGM market growth near 3% CAGR (2022–24), these systems need minimal capex to sustain output, freeing cash flow to underwrite admin costs and fund smart-healthcare R&D and platform rollouts.

- 2024 revenue ~RMB 430m; gross margin ~52%

- Domestic inpatient BGM share ~45% (2024)

- Market growth ~3% CAGR (2022–24)

- Low incremental capex; funds smart-health transition

Sinocare’s cash-generating BGM, strips & CardioChek fund CGM/AI global push

Sinocare’s mature BGM meters, strips, hospital systems, and CardioChek deliver steady high-margin cash flow—~RMB 1.2bn operating cash flow (2024 est.), strips ~RMB 450–600m, hospital systems ~RMB 430m, CardioChek $85–95m—funding CGM/AI R&D and 2025–26 international expansion.

| Product | 2024 revenue | Share | Growth |

|---|---|---|---|

| Strips/meters | RMB 450–600m | ~28% (strips China) | ~2% CAGR |

| Hospital BGM | RMB 430m | ~45% (inpatient China) | ~3% CAGR |

| CardioChek | $85–95m | ~18% handheld | 2–4% CAGR |

Preview = Final Product

Sinocare BCG Matrix

The file you're previewing on this page is the final Sinocare BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report designed for clear portfolio analysis.

This preview is the exact same document that will be delivered to your inbox post-purchase, crafted with market-backed insights and formatted for immediate editing, printing, or presenting to stakeholders.

What you see is the authentic BCG Matrix file included with your one-time purchase—professionally designed by strategy experts and ready to plug into business planning, investor decks, or competitive reviews.

There are no mockups or placeholders here; upon buying you’ll unlock the complete, analysis-ready Sinocare BCG Matrix for instant download and deployment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Sinocare’s BCG Matrix preview highlights how its glucose monitoring and diabetes management products compete across growth and market-share axes, hinting at which offerings are potential Stars or Cash Cows and which may be underperforming; this snapshot is ideal for investors and strategists sizing opportunity and risk.

Get the full BCG Matrix report for a quadrant-by-quadrant breakdown, actionable strategic moves, and editable Word plus Excel files—purchase now to shortcut research and make confident product and capital-allocation decisions.

Stars

Continuous Glucose Monitoring Systems

The iCan CGM series is Sinocare’s high-growth flagship, using third-generation sensors to compete in a CGM market growing at ~17% CAGR (2020–25) and valued at ~$12.5B in 2025.

By late 2025, partnerships with A. Menarini Diagnostics have placed iCan in 20+ European jurisdictions, capturing a leading share in the premium segment—estimated 8–12% share in served markets.

iCan drives top-line revenue but demands heavy R&D and marketing spend—Sinocare invested ~RMB 420M in diabetes R&D in 2024—to sustain competitiveness vs. global rivals like Abbott.

Integrated Digital Diabetes Platforms

Sinocare’s Integrated Digital Diabetes Platforms are Stars: SinoGPT AI and the digital management ecosystem shifted the company from device maker to service provider, tapping the market move to data-driven chronic care in hospitals and homes.

By 2025 these platforms cover 4,000+ Chinese hospitals and generated an estimated 28–35% higher ARPU versus devices alone, so Sinocare must keep investing in IoT integration and personalized care to sustain growth.

Multi-Parameter POCT Devices

The Precision Desk Lab and advanced iPOCT units for glucose, uric acid, and ketones are Sinocare’s Stars: in 2025 they captured ~28% share of China’s professional POCT market and drove 42% of Sinocare’s device revenue (¥1.12bn of ¥2.67bn YTD), reflecting fast clinical adoption amid healthcare decentralization.

They produce strong cash inflows but require rapid R&D spend—Sinocare increased iPOCT R&D 34% YoY in 2024–25—keeping these products in the Star quadrant as of end-2025.

Trividia Health International Portfolio

Through the 2023 acquisition of U.S.-based Trividia Health, Sinocare captured a leading share in North American retail glucose monitoring: TRUE brand presence in 55,000+ outlets (Walgreens, CVS) reaches an estimated 4–6 million users, boosting Sinocare’s international revenue—U.S. contributed about 18% of group sales in 2024.

Integration of Chinese R&D with U.S. manufacturing accelerates product pipeline and gross margins, but the segment stays capital-intensive: logistics, FDA/CE compliance and warranty reserves keep capex and OPEX elevated.

- TRUE in 55,000+ outlets

- 4–6M users (est.)

- U.S. ~18% of 2024 sales

- Higher capex for compliance/logistics

Smart Hypertension Monitoring Solutions

Sinocare’s Smart Hypertension Monitoring Solutions, launched under the Biosensing Plus strategy, entered the chronic disease market in 2023 and hit double-digit CAGR adoption, reaching an estimated $24M revenue run-rate by Q4 2025.

Bundling with Sinocare’s diabetes meters and apps raised stickiness: cross-sell lifted ARPU ~28% and drove a 6-point market-share gain vs traditional BP device makers in China by 2025.

To keep momentum, Sinocare must invest in aggressive promotion and channel expansion through 2025; without a 15–20% marketing uplift, leadership vs established med-dev incumbents could slip.

- Revenue run-rate Q4 2025: $24M

- ARPU increase from bundling: ~28%

- Market-share gain vs incumbents: +6 pts (China, 2023–2025)

- Required marketing uplift to secure lead: 15–20%

Sinocare’s flagship suite fuels rapid 2025 growth—CGM, iPOCT, TRUE, Smart BP surge

Sinocare’s Stars (iCan CGM, Integrated Digital Platforms, iPOCT, TRUE, Smart BP) drove rapid growth by 2025: iCan ~8–12% share in served EU markets; CGM market ~$12.5B (2025); iPOCT 28% China share, ¥1.12bn of ¥2.67bn YTD device revenue; TRUE in 55,000+ US outlets (~4–6M users); Smart BP $24M run-rate Q4 2025.

| Product | Key 2025 metrics |

|---|---|

| iCan CGM | 8–12% served-market share; market $12.5B |

| iPOCT | 28% China share; ¥1.12bn device rev |

| TRUE | 55,000+ outlets; 4–6M users |

| Smart BP | $24M run-rate Q4 2025 |

What is included in the product

Comprehensive BCG Matrix review of Sinocare’s portfolio with quadrant strategies, investment priorities, and trend-driven risks/opportunities.

One-page Sinocare BCG Matrix mapping each unit for quick strategic decisions, export-ready for seamless PowerPoint integration.

Cash Cows

Retail Blood Glucose Meters

Sinocare holds ~50% share of China’s retail blood glucose meter market, addressing >140 million people with diabetes in China (IDF 2023 est.), making this a stable, high-volume cash cow.

Low marketing and R&D for mature strip-and-meter sales mean these products produce most free cash flow; in 2024 Sinocare reported ~RMB 1.2 billion operating cash flow, largely from this segment.

Those steady profits fund next-gen CGM and AI projects, covering upfront R&D and pilot production without diluting equity or large debt increases.

Traditional Blood Glucose Test Strips

Test strips are a high-margin, recurring cash cow for Sinocare, driven by millions of installed meters and a 2024 estimated market share around 28% in China’s BGM strip segment; low BGM market growth (~2% CAGR 2023–2028) and strong customer loyalty keep unit economics favorable. The consumables business has minimal capex and SG&A per unit, generating roughly RMB 450–600 million in annual operating cashflow (2024 est.), which funds debt service and fuels 2025–26 international expansion.

Legacy Safe-Accu Product Series

The Legacy Safe-Accu product series sells over 12 million units annually in China, generating high gross margins (estimated 30–35% in 2024) due to scale and optimized supply chains, making it a consistent cash cow for Sinocare.

PTS Diagnostics Lipid Analyzers

The CardioChek family of lipid analyzers, acquired via PTS Diagnostics in 2021, dominates the global point-of-care lipid testing niche with an estimated $85–95M annual revenue run-rate in 2024 and ~18% global market share in handheld analyzers.

Operating in a mature segment, demand from clinics and pharmacies is steady, yielding consistent cash flow but low mid-single-digit growth forecasts (2–4% CAGR to 2028), making it a classic Cash Cow for Sinocare.

It provides reliable international revenue—roughly 12–15% of Sinocare’s FY2024 revenue—and funds expansion in chronic disease management devices and R&D.

- 2024 run-rate $85–95M; ~18% handheld share

- Low growth: 2–4% CAGR to 2028

- Contributes ~12–15% of Sinocare FY2024 revenue

Hospital-Grade Glycemic Management Systems

Sinocare’s hospital-grade glycemic management systems hold ~45% share in China’s inpatient BGM segment (2024), delivering stable annual revenue ~RMB 430m and consistent gross margin ~52%, making them a reliable cash cow for the group.

With basic in-hospital BGM market growth near 3% CAGR (2022–24), these systems need minimal capex to sustain output, freeing cash flow to underwrite admin costs and fund smart-healthcare R&D and platform rollouts.

- 2024 revenue ~RMB 430m; gross margin ~52%

- Domestic inpatient BGM share ~45% (2024)

- Market growth ~3% CAGR (2022–24)

- Low incremental capex; funds smart-health transition

Sinocare’s cash-generating BGM, strips & CardioChek fund CGM/AI global push

Sinocare’s mature BGM meters, strips, hospital systems, and CardioChek deliver steady high-margin cash flow—~RMB 1.2bn operating cash flow (2024 est.), strips ~RMB 450–600m, hospital systems ~RMB 430m, CardioChek $85–95m—funding CGM/AI R&D and 2025–26 international expansion.

| Product | 2024 revenue | Share | Growth |

|---|---|---|---|

| Strips/meters | RMB 450–600m | ~28% (strips China) | ~2% CAGR |

| Hospital BGM | RMB 430m | ~45% (inpatient China) | ~3% CAGR |

| CardioChek | $85–95m | ~18% handheld | 2–4% CAGR |

Preview = Final Product

Sinocare BCG Matrix

The file you're previewing on this page is the final Sinocare BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report designed for clear portfolio analysis.

This preview is the exact same document that will be delivered to your inbox post-purchase, crafted with market-backed insights and formatted for immediate editing, printing, or presenting to stakeholders.

What you see is the authentic BCG Matrix file included with your one-time purchase—professionally designed by strategy experts and ready to plug into business planning, investor decks, or competitive reviews.

There are no mockups or placeholders here; upon buying you’ll unlock the complete, analysis-ready Sinocare BCG Matrix for instant download and deployment.