Bank SinoPac Business Model Canvas

Bank SinoPac Business Model Canvas: Download Editable Blueprint for Strategy & Investment

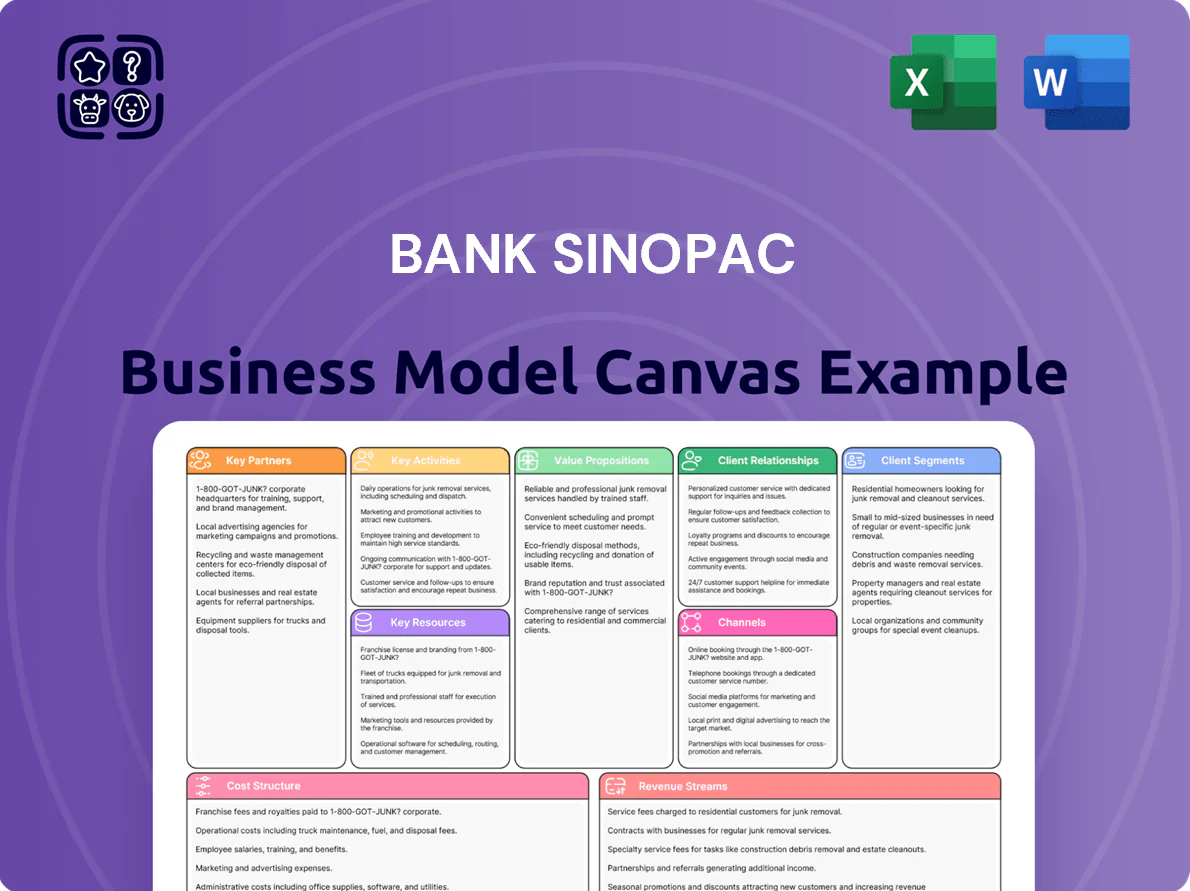

Unlock the full strategic blueprint behind Bank SinoPac’s business model with our complete Business Model Canvas—detailing value propositions, customer segments, key activities, and revenue streams to inform investment and strategy decisions; download the editable Word and Excel files to benchmark, adapt, and act on proven banking strategies.

Partnerships

SinoPac Financial Holdings

As a primary subsidiary of SinoPac Financial Holdings, Bank SinoPac taps a cross-selling ecosystem across securities and insurance, driving ~18% of 2024 fee income from group referrals and lowering customer acquisition cost by an estimated 22%. Shared admin functions cut overheads—group-level expense ratio fell to 42% in 2024—improving capital efficiency and enabling integrated financial packages (bank+securities+insurance) that standalone rivals rarely match.

Fintech and Technology Providers

The bank partners with leading fintechs to speed digital transformation, deploying AI credit-scoring models that cut default prediction error by ~15% and rolling out blockchain trade finance pilots that reduced settlement times from 5 days to 24 hours in 2024.

Global Payment Networks

Partnerships with Visa and Mastercard give Bank SinoPac global transaction reach, supporting over 200 countries and access to a combined merchant network processing trillions annually; in 2024 global card transaction volume exceeded $10.9 trillion, enabling SinoPac’s retail and corporate clients seamless cross-border payments.

Insurance and Asset Managers

Bank SinoPac partners with third-party insurers and global asset managers to broaden its wealth management offerings, generating commission income via bancassurance and advisory fees; in 2024 bancassurance revenue rose ~12% y/y to NT$2.1 billion, helping AUM-linked fees reach NT$4.3 billion.

These ties secure exclusive fund access and tailored solutions for HNW clients, preserving competitiveness as HNW segment AUM grew 9% in 2024 to NT$180 billion.

- NT$2.1B bancassurance revenue (2024)

- NT$4.3B AUM fees (2024)

- HNW AUM NT$180B, +9% (2024)

- Exclusive fund deals boost client retention

Government and Regulatory Agencies

Continuous engagement with the Financial Supervisory Commission and regional regulators keeps Bank SinoPac aligned with evolving capital requirements—Taiwan banks faced a 2024 CET1 trend toward 12–13% regulatory buffers, so close dialogue reduces regulatory shortfall risk.

These partnerships include participation in government-backed lending schemes—Bank SinoPac reported underwriting NT$18.3 billion in SME and green loans under public programs in 2024—and help secure licenses and cross-border operating approvals.

- Regular regulator meetings to monitor CET1 and liquidity ratios

- NT$18.3 billion SME/green loans via government schemes in 2024

- Collaboration aids licensing and cross-jurisdiction compliance

Bank SinoPac cuts costs 22%, boosts fees via referrals to 18% and grows HNW AUM

Bank SinoPac leverages group synergies, fintech and card networks to cut acquisition cost ~22%, drive ~18% of 2024 fee income from referrals, and lift bancassurance/AUM fees (NT$2.1B/NT$4.3B) while underwriting NT$18.3B in public SME/green loans and growing HNW AUM to NT$180B (+9%).

| Metric | 2024 |

|---|---|

| Referral fee share | ~18% |

| Acq. cost reduction | ~22% |

| Bancassurance rev | NT$2.1B |

| AUM fees | NT$4.3B |

| HNW AUM | NT$180B (+9%) |

| Public loans underwritten | NT$18.3B |

What is included in the product

A concise, investor-ready Business Model Canvas for Bank SinoPac that maps customer segments, channels, value propositions, revenue streams, key activities, partners, resources, cost structure, and governance, with integrated SWOT and competitive analysis to reflect real-world operations and strategic priorities for presentations and decision-making.

Concise one-page Business Model Canvas for Bank SinoPac that condenses strategy into an editable, shareable snapshot—ideal for boardrooms, team collaboration, and quick comparative analysis.

Activities

Financial Product Development

Bank SinoPac develops mortgages, green bonds, and structured investment vehicles, using quarterly market research to adapt to Taiwan's 2025 household mortgage growth of 3.2% and a 2024-25 policy rate rise to 1.75%. By launching a NT$15 billion green bond program in 2024 and tailoring products for retail savers and corporate clients, the bank aligns offerings with shifting demand and rate volatility.

Risk Management and Mitigation

A core activity is rigorous assessment of credit, market, and operational risks to protect the balance sheet; Bank SinoPac reported NPL ratio of 0.36% and CET1 ratio of 12.4% as of 2025, reflecting this focus. Advanced data analytics monitor loan portfolios and flag early-warning signals—machine-learning models reduced delinquency prediction lag by 40% in 2024. Effective risk management keeps the bank compliant with Basel III capital adequacy and preserves credit ratings.

Digital Platform Enhancement

Bank SinoPac allocates ~NT$1.8bn annually to Dawho app and digital channels, funding cybersecurity upgrades (ISO 27001-aligned), UI/UX redesigns, and RPA-driven wealth tools that raised digital AUM by 22% in 2024; ongoing platform investment aims to cut cost-to-serve by 18% and lower branch transactions 35% by 2026.

Corporate Advisory and Lending

The bank provides tailored financing and strategic advisory to SMEs and corporates, underwriting debt, arranging M&A deals, and managing trade finance; in 2024 Bank SinoPac reported NT$45 billion in corporate loan originations and NT$2.1 billion in advisory fees, driving steady interest income and fee growth.

- NT$45B corporate loans (2024)

- NT$2.1B advisory fees (2024)

- M&A and trade finance-led relationship revenue

ESG and Sustainability Initiatives

Bank SinoPac embeds ESG into strategy by auditing its loan portfolio carbon intensity—2024 internal review found 18% of financed emissions concentrated in energy and transport—and by funding NT$3.2 billion in green loans and community financial-literacy programs in 2024.

By prioritizing sustainable finance, the bank meets global investor ESG benchmarks and reduces long-term climate and regulatory risk, targeting a 25% reduction in portfolio carbon intensity by 2030.

- 2024 green loan volume: NT$3.2 billion

- 2024 portfolio emissions concentration: 18% in energy/transport

- 2030 carbon-intensity target: −25%

- Community programs funded: NT$200 million (2024)

Bank SinoPac: Strong risk controls, digital push and NT$3.2B green lending

Bank SinoPac develops mortgages, green bonds, SME financing, and digital wealth tools, backing risk control (NPL 0.36%, CET1 12.4% in 2025) and ESG (NT$3.2B green loans, 18% financed emissions in 2024). Quarterly market research and NT$1.8B digital spend drive product shifts; 2024 corporate loans NT$45B, advisory fees NT$2.1B.

| Metric | 2024/25 |

|---|---|

| NPL ratio | 0.36% (2025) |

| CET1 | 12.4% (2025) |

| Green loans | NT$3.2B (2024) |

| Corp loans | NT$45B (2024) |

| Digital spend | NT$1.8B pa |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank SinoPac Business Model Canvas you will receive—no mockups or samples. Upon purchase, you'll get this exact file in full, ready-to-edit Word and Excel formats, with all sections and content included. What you see is what you’ll own, formatted for immediate use in presentations, analysis, or strategy work.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank SinoPac Business Model Canvas: Download Editable Blueprint for Strategy & Investment

Unlock the full strategic blueprint behind Bank SinoPac’s business model with our complete Business Model Canvas—detailing value propositions, customer segments, key activities, and revenue streams to inform investment and strategy decisions; download the editable Word and Excel files to benchmark, adapt, and act on proven banking strategies.

Partnerships

SinoPac Financial Holdings

As a primary subsidiary of SinoPac Financial Holdings, Bank SinoPac taps a cross-selling ecosystem across securities and insurance, driving ~18% of 2024 fee income from group referrals and lowering customer acquisition cost by an estimated 22%. Shared admin functions cut overheads—group-level expense ratio fell to 42% in 2024—improving capital efficiency and enabling integrated financial packages (bank+securities+insurance) that standalone rivals rarely match.

Fintech and Technology Providers

The bank partners with leading fintechs to speed digital transformation, deploying AI credit-scoring models that cut default prediction error by ~15% and rolling out blockchain trade finance pilots that reduced settlement times from 5 days to 24 hours in 2024.

Global Payment Networks

Partnerships with Visa and Mastercard give Bank SinoPac global transaction reach, supporting over 200 countries and access to a combined merchant network processing trillions annually; in 2024 global card transaction volume exceeded $10.9 trillion, enabling SinoPac’s retail and corporate clients seamless cross-border payments.

Insurance and Asset Managers

Bank SinoPac partners with third-party insurers and global asset managers to broaden its wealth management offerings, generating commission income via bancassurance and advisory fees; in 2024 bancassurance revenue rose ~12% y/y to NT$2.1 billion, helping AUM-linked fees reach NT$4.3 billion.

These ties secure exclusive fund access and tailored solutions for HNW clients, preserving competitiveness as HNW segment AUM grew 9% in 2024 to NT$180 billion.

- NT$2.1B bancassurance revenue (2024)

- NT$4.3B AUM fees (2024)

- HNW AUM NT$180B, +9% (2024)

- Exclusive fund deals boost client retention

Government and Regulatory Agencies

Continuous engagement with the Financial Supervisory Commission and regional regulators keeps Bank SinoPac aligned with evolving capital requirements—Taiwan banks faced a 2024 CET1 trend toward 12–13% regulatory buffers, so close dialogue reduces regulatory shortfall risk.

These partnerships include participation in government-backed lending schemes—Bank SinoPac reported underwriting NT$18.3 billion in SME and green loans under public programs in 2024—and help secure licenses and cross-border operating approvals.

- Regular regulator meetings to monitor CET1 and liquidity ratios

- NT$18.3 billion SME/green loans via government schemes in 2024

- Collaboration aids licensing and cross-jurisdiction compliance

Bank SinoPac cuts costs 22%, boosts fees via referrals to 18% and grows HNW AUM

Bank SinoPac leverages group synergies, fintech and card networks to cut acquisition cost ~22%, drive ~18% of 2024 fee income from referrals, and lift bancassurance/AUM fees (NT$2.1B/NT$4.3B) while underwriting NT$18.3B in public SME/green loans and growing HNW AUM to NT$180B (+9%).

| Metric | 2024 |

|---|---|

| Referral fee share | ~18% |

| Acq. cost reduction | ~22% |

| Bancassurance rev | NT$2.1B |

| AUM fees | NT$4.3B |

| HNW AUM | NT$180B (+9%) |

| Public loans underwritten | NT$18.3B |

What is included in the product

A concise, investor-ready Business Model Canvas for Bank SinoPac that maps customer segments, channels, value propositions, revenue streams, key activities, partners, resources, cost structure, and governance, with integrated SWOT and competitive analysis to reflect real-world operations and strategic priorities for presentations and decision-making.

Concise one-page Business Model Canvas for Bank SinoPac that condenses strategy into an editable, shareable snapshot—ideal for boardrooms, team collaboration, and quick comparative analysis.

Activities

Financial Product Development

Bank SinoPac develops mortgages, green bonds, and structured investment vehicles, using quarterly market research to adapt to Taiwan's 2025 household mortgage growth of 3.2% and a 2024-25 policy rate rise to 1.75%. By launching a NT$15 billion green bond program in 2024 and tailoring products for retail savers and corporate clients, the bank aligns offerings with shifting demand and rate volatility.

Risk Management and Mitigation

A core activity is rigorous assessment of credit, market, and operational risks to protect the balance sheet; Bank SinoPac reported NPL ratio of 0.36% and CET1 ratio of 12.4% as of 2025, reflecting this focus. Advanced data analytics monitor loan portfolios and flag early-warning signals—machine-learning models reduced delinquency prediction lag by 40% in 2024. Effective risk management keeps the bank compliant with Basel III capital adequacy and preserves credit ratings.

Digital Platform Enhancement

Bank SinoPac allocates ~NT$1.8bn annually to Dawho app and digital channels, funding cybersecurity upgrades (ISO 27001-aligned), UI/UX redesigns, and RPA-driven wealth tools that raised digital AUM by 22% in 2024; ongoing platform investment aims to cut cost-to-serve by 18% and lower branch transactions 35% by 2026.

Corporate Advisory and Lending

The bank provides tailored financing and strategic advisory to SMEs and corporates, underwriting debt, arranging M&A deals, and managing trade finance; in 2024 Bank SinoPac reported NT$45 billion in corporate loan originations and NT$2.1 billion in advisory fees, driving steady interest income and fee growth.

- NT$45B corporate loans (2024)

- NT$2.1B advisory fees (2024)

- M&A and trade finance-led relationship revenue

ESG and Sustainability Initiatives

Bank SinoPac embeds ESG into strategy by auditing its loan portfolio carbon intensity—2024 internal review found 18% of financed emissions concentrated in energy and transport—and by funding NT$3.2 billion in green loans and community financial-literacy programs in 2024.

By prioritizing sustainable finance, the bank meets global investor ESG benchmarks and reduces long-term climate and regulatory risk, targeting a 25% reduction in portfolio carbon intensity by 2030.

- 2024 green loan volume: NT$3.2 billion

- 2024 portfolio emissions concentration: 18% in energy/transport

- 2030 carbon-intensity target: −25%

- Community programs funded: NT$200 million (2024)

Bank SinoPac: Strong risk controls, digital push and NT$3.2B green lending

Bank SinoPac develops mortgages, green bonds, SME financing, and digital wealth tools, backing risk control (NPL 0.36%, CET1 12.4% in 2025) and ESG (NT$3.2B green loans, 18% financed emissions in 2024). Quarterly market research and NT$1.8B digital spend drive product shifts; 2024 corporate loans NT$45B, advisory fees NT$2.1B.

| Metric | 2024/25 |

|---|---|

| NPL ratio | 0.36% (2025) |

| CET1 | 12.4% (2025) |

| Green loans | NT$3.2B (2024) |

| Corp loans | NT$45B (2024) |

| Digital spend | NT$1.8B pa |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank SinoPac Business Model Canvas you will receive—no mockups or samples. Upon purchase, you'll get this exact file in full, ready-to-edit Word and Excel formats, with all sections and content included. What you see is what you’ll own, formatted for immediate use in presentations, analysis, or strategy work.