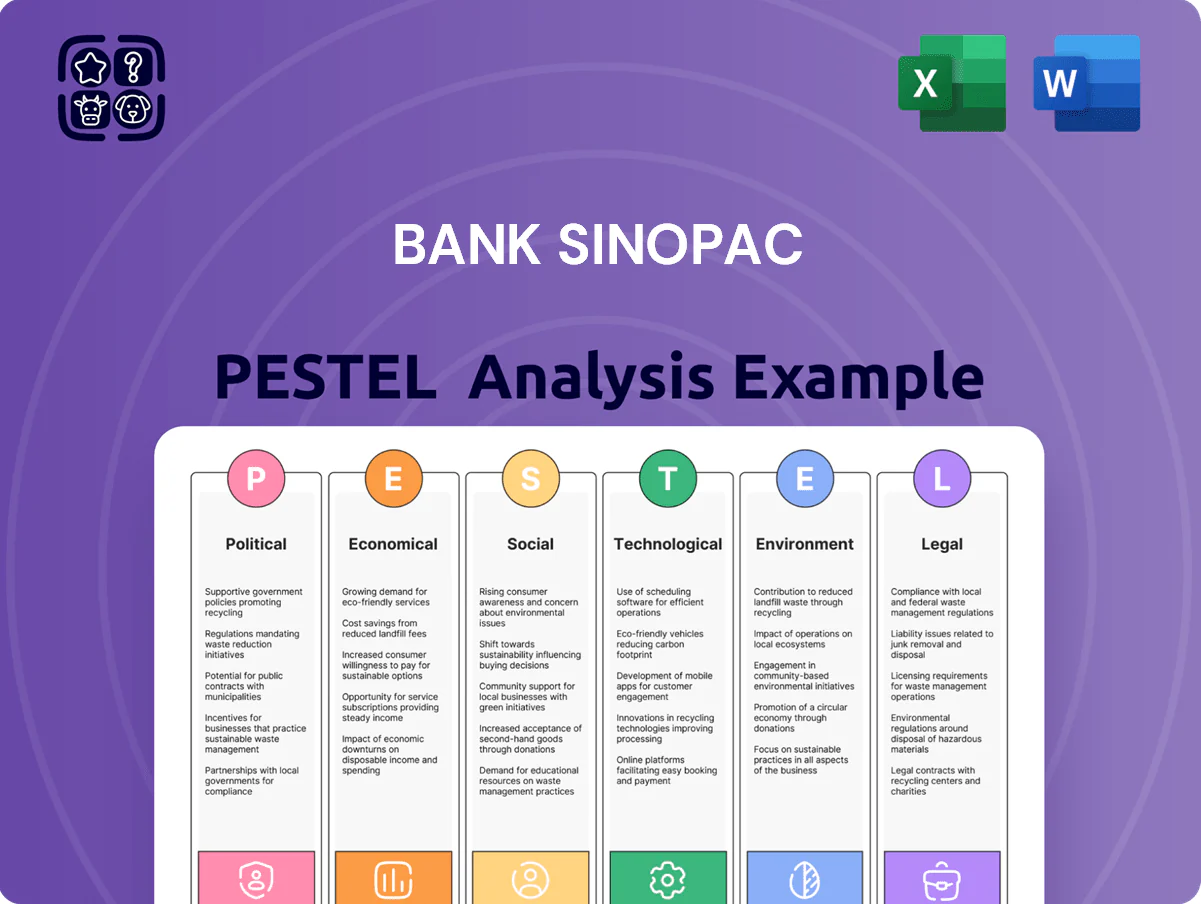

Bank SinoPac PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how regulatory shifts, economic cycles, and digital innovation are reshaping Bank SinoPac’s strategic outlook—our PESTLE Analysis translates these external forces into actionable implications for investors and managers. Purchase the full report to access exhaustive, ready-to-use insights and forecasts that will strengthen your decisions and save research time.

Political factors

Cross-Strait Geopolitical Tensions

The Taiwan–Mainland China relationship is a key political risk for Bank SinoPac, as ~60% of its 2024 revenue-generating operations are Taiwan-focused and cross-strait flows drive ~25% of its corporate loan syndication volume.

Escalation in tensions can spur market volatility—Taiwan TAIEX dropped 12% during 2022 regional shocks—reducing investor confidence and cutting cross-border transaction volumes that comprised 18% of fee income in 2023.

Management must monitor diplomatic developments, given that 2024 export controls and occasional trade restrictions between Taipei and Beijing have led to tightened compliance costs, raising regional regulatory risk and potential credit-impairment exposure.

Financial Supervision Commission Policy

The Financial Supervision Commission in Taiwan tightened bank capital rules, raising CET1 expectations toward 10.5% industry-wide and boosting governance audits; regulators fined banks NT$3.2bn in 2024–2025 for compliance lapses.

Support for New Southbound Policy

Taiwan’s New Southbound Policy incentivizes banks to enter Southeast Asia to cut overreliance on Greater China; Taipei allocated NT$100bn in 2024 trade-financing support to promote such expansion. Bank SinoPac used subsidies and tax breaks to open branches/partnerships in Vietnam and Thailand, lifting its Southeast Asia loan book to about 6% of total loans by 2025 (from 2.1% in 2020).

Political Stability and Governance

The internal political stability of Taiwan, reflected in a 2024 World Bank Worldwide Governance IndicatorRanking of 74/100 for political stability, shapes regulatory predictability and long-term reform implementation affecting Bank SinoPac's strategy.

A stable legislature lets the bank project tax and compliance costs more accurately; Taiwan's corporate tax rate remained at 20% in 2024, aiding multi-year forecasting.

Election-driven shifts can reprioritize spending and fiscal policy rapidly—Bank SinoPac must adjust to policy swings that could alter credit demand or sovereign risk premia.

- 2024 political stability index: 74/100

- Taiwan corporate tax rate: 20% (2024)

- Election cycles can change fiscal priorities, impacting credit demand and compliance costs

International Trade Agreements

Taiwan’s exclusion from some regional trade blocs raises corporate banking demand at Bank SinoPac as exporters—which accounted for about 35% of Taiwan’s GDP in 2023—seek alternative financing and hedging solutions to remain competitive.

Ongoing political pushes for high‑standard trade agreements force the bank to upgrade trade finance products to comply with global norms; Taiwan’s merchandise exports reached US$423.5 billion in 2024, amplifying this need.

Such agreements shape cross‑border capital flows and the health of export sectors that comprise a large share of Bank SinoPac’s corporate loan book, with manufacturing loans representing roughly 28% of corporate lending in 2024.

- 35% of GDP from exporters (2023)

- Merchandise exports US$423.5B (2024)

- Manufacturing loans ~28% of corporate lending (2024)

Cross‑strait risk dominates: 60% Taiwan revenue, rising compliance & SEA expansion

Cross‑strait tensions remain the principal political risk—~60% of 2024 revenue operations are Taiwan‑focused and ~25% of corporate syndications are driven by cross‑strait flows; market shocks (TAIEX −12% in 2022) and 2024 export controls raised compliance costs and credit risk. Regulators pushed CET1 toward 10.5%; Taiwan political stability index 74/100 (2024); New Southbound support raised SEA loans to ~6% by 2025.

| Metric | Value |

|---|---|

| Taiwan revenue focus (2024) | ~60% |

| Cross‑strait corp. syndication | ~25% |

| TAIEX shock (2022) | −12% |

| CET1 target (2024) | ~10.5% |

| Political stability (2024) | 74/100 |

| SEA loan share (2025) | ~6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bank SinoPac across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Bank SinoPac that’s easy to drop into presentations or share across teams, helping quickly align stakeholders on external risks and market positioning while allowing note additions for local/regional context.

Economic factors

Monetary Policy and Interest Rates

The Central Bank of Taiwan's rate moves were pivotal to Bank SinoPac's NIM, with policy rates rising to 1.875% by Dec 2025 from 0.875% in 2023, pressuring funding costs while lending yields lagged. By end-2025 SinoPac reported a NIM near 1.35% as it navigated stabilizing inflation and volatile global cycles. Active loan-to-deposit management—LDR around 78% in 2025—balanced return optimization and regulatory liquidity buffers.

Taiwan GDP Growth Trends

The Taiwanese economy, powered by a 2024 GDP growth of 2.3% and a 2025 IMF-projected stabilization near 2.5%, hinges on semiconductor and tech exports that drive corporate credit and consumer loan demand.

As growth stabilizes in 2025, Bank SinoPac sees uneven demand across sectors—stronger in ICT and electronics, softer in traditional manufacturing and retail—impacting loan origination mix.

The bank adjusts risk appetite and capital allocation using Central Bank forecasts and BSP data, tilting exposure toward high-growth tech exporters and related supply-chain financing.

Inflation and Consumer Purchasing Power

Persistent inflation in Taiwan—CPI rose 2.9% in 2024 and averaged ~2.6% in 2023–24—erodes consumer purchasing power, raising cost of living and pressure on household debt, which can increase non-performing loans for Bank SinoPac.

Bank SinoPac closely monitors these indicators to recalibrate retail deposit rates, credit card rewards and underwriting standards, having tightened credit lines by ~5% in high-risk segments in 2024.

Balancing competitive saver yields (market deposit rates climbed ~1.2 percentage points in 2024) with manageable loan terms is critical to sustain margins while containing consumer credit stress.

Exchange Rate Volatility

As a major international banker, Bank SinoPac is exposed to NTD volatility versus USD, JPY and CNY; NTD moved about 3.8% versus USD in 2024, amplifying translation risk for its foreign-currency assets (NT$ billions) and affecting trade finance pricing.

Currency swings raise clients' transaction costs and counterparty credit risk; in 2024 the bank reported expanded FX volumes and strengthened hedging, with derivatives usage up ~12% year-on-year to mitigate P&L volatility.

- NTD vs USD volatility ~3.8% in 2024

- Derivatives hedging use +12% YoY

- Higher FX-related transaction costs for trade clients

- Robust FX services central to risk management

Global Supply Chain Shifts

The reorganization of global supply chains, especially in tech, raises demand for corporate lending as 42% of Taiwanese electronics firms planned relocation or supplier diversification in 2023, creating opportunities for Bank SinoPac to offer capex and working-capital financing for factory moves and supplier onboarding.

Bank SinoPac must speed credit assessments and risk models to underwrite cross-border exposures and currency, logistics, and tariff risks amid supply-chain shifts.

- 42% of Taiwanese electronics firms planned relocation/diversification in 2023

- Demand for capex and working-capital loans rises with reshoring/nearshoring

- Requires faster, geography-aware credit and FX risk models

Higher rates cut NIM to ~1.35%; tech-led loan demand offsets FX hedging gains

Rising policy rates to 1.875% by Dec 2025 cut NIM to ~1.35% as funding costs outpaced lending yields; LDR ~78% in 2025. Taiwan GDP ~2.3% in 2024, ~2.5% in 2025 supports tech-led corporate loan demand; CPI ~2.9% in 2024 pressures household debt and NPL risk. NTD volatility ~3.8% vs USD (2024) and +12% YoY derivatives hedging increased FX service revenue.

| Metric | 2024 | 2025 |

|---|---|---|

| GDP growth | 2.3% | ~2.5% |

| CPI | 2.9% | ~2.6% avg |

| Policy rate | 0.875% | 1.875% |

| NIM (SinoPac) | — | ~1.35% |

| LDR | — | ~78% |

| NTD vs USD vol | ~3.8% | — |

| Derivatives hedging | +12% YoY | — |

Same Document Delivered

Bank SinoPac PESTLE Analysis

The preview shown here is the exact Bank SinoPac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are exactly what you’ll download immediately after payment.

Everything displayed is part of the final product, providing a complete PESTLE assessment you can apply straightaway.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how regulatory shifts, economic cycles, and digital innovation are reshaping Bank SinoPac’s strategic outlook—our PESTLE Analysis translates these external forces into actionable implications for investors and managers. Purchase the full report to access exhaustive, ready-to-use insights and forecasts that will strengthen your decisions and save research time.

Political factors

Cross-Strait Geopolitical Tensions

The Taiwan–Mainland China relationship is a key political risk for Bank SinoPac, as ~60% of its 2024 revenue-generating operations are Taiwan-focused and cross-strait flows drive ~25% of its corporate loan syndication volume.

Escalation in tensions can spur market volatility—Taiwan TAIEX dropped 12% during 2022 regional shocks—reducing investor confidence and cutting cross-border transaction volumes that comprised 18% of fee income in 2023.

Management must monitor diplomatic developments, given that 2024 export controls and occasional trade restrictions between Taipei and Beijing have led to tightened compliance costs, raising regional regulatory risk and potential credit-impairment exposure.

Financial Supervision Commission Policy

The Financial Supervision Commission in Taiwan tightened bank capital rules, raising CET1 expectations toward 10.5% industry-wide and boosting governance audits; regulators fined banks NT$3.2bn in 2024–2025 for compliance lapses.

Support for New Southbound Policy

Taiwan’s New Southbound Policy incentivizes banks to enter Southeast Asia to cut overreliance on Greater China; Taipei allocated NT$100bn in 2024 trade-financing support to promote such expansion. Bank SinoPac used subsidies and tax breaks to open branches/partnerships in Vietnam and Thailand, lifting its Southeast Asia loan book to about 6% of total loans by 2025 (from 2.1% in 2020).

Political Stability and Governance

The internal political stability of Taiwan, reflected in a 2024 World Bank Worldwide Governance IndicatorRanking of 74/100 for political stability, shapes regulatory predictability and long-term reform implementation affecting Bank SinoPac's strategy.

A stable legislature lets the bank project tax and compliance costs more accurately; Taiwan's corporate tax rate remained at 20% in 2024, aiding multi-year forecasting.

Election-driven shifts can reprioritize spending and fiscal policy rapidly—Bank SinoPac must adjust to policy swings that could alter credit demand or sovereign risk premia.

- 2024 political stability index: 74/100

- Taiwan corporate tax rate: 20% (2024)

- Election cycles can change fiscal priorities, impacting credit demand and compliance costs

International Trade Agreements

Taiwan’s exclusion from some regional trade blocs raises corporate banking demand at Bank SinoPac as exporters—which accounted for about 35% of Taiwan’s GDP in 2023—seek alternative financing and hedging solutions to remain competitive.

Ongoing political pushes for high‑standard trade agreements force the bank to upgrade trade finance products to comply with global norms; Taiwan’s merchandise exports reached US$423.5 billion in 2024, amplifying this need.

Such agreements shape cross‑border capital flows and the health of export sectors that comprise a large share of Bank SinoPac’s corporate loan book, with manufacturing loans representing roughly 28% of corporate lending in 2024.

- 35% of GDP from exporters (2023)

- Merchandise exports US$423.5B (2024)

- Manufacturing loans ~28% of corporate lending (2024)

Cross‑strait risk dominates: 60% Taiwan revenue, rising compliance & SEA expansion

Cross‑strait tensions remain the principal political risk—~60% of 2024 revenue operations are Taiwan‑focused and ~25% of corporate syndications are driven by cross‑strait flows; market shocks (TAIEX −12% in 2022) and 2024 export controls raised compliance costs and credit risk. Regulators pushed CET1 toward 10.5%; Taiwan political stability index 74/100 (2024); New Southbound support raised SEA loans to ~6% by 2025.

| Metric | Value |

|---|---|

| Taiwan revenue focus (2024) | ~60% |

| Cross‑strait corp. syndication | ~25% |

| TAIEX shock (2022) | −12% |

| CET1 target (2024) | ~10.5% |

| Political stability (2024) | 74/100 |

| SEA loan share (2025) | ~6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bank SinoPac across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Bank SinoPac that’s easy to drop into presentations or share across teams, helping quickly align stakeholders on external risks and market positioning while allowing note additions for local/regional context.

Economic factors

Monetary Policy and Interest Rates

The Central Bank of Taiwan's rate moves were pivotal to Bank SinoPac's NIM, with policy rates rising to 1.875% by Dec 2025 from 0.875% in 2023, pressuring funding costs while lending yields lagged. By end-2025 SinoPac reported a NIM near 1.35% as it navigated stabilizing inflation and volatile global cycles. Active loan-to-deposit management—LDR around 78% in 2025—balanced return optimization and regulatory liquidity buffers.

Taiwan GDP Growth Trends

The Taiwanese economy, powered by a 2024 GDP growth of 2.3% and a 2025 IMF-projected stabilization near 2.5%, hinges on semiconductor and tech exports that drive corporate credit and consumer loan demand.

As growth stabilizes in 2025, Bank SinoPac sees uneven demand across sectors—stronger in ICT and electronics, softer in traditional manufacturing and retail—impacting loan origination mix.

The bank adjusts risk appetite and capital allocation using Central Bank forecasts and BSP data, tilting exposure toward high-growth tech exporters and related supply-chain financing.

Inflation and Consumer Purchasing Power

Persistent inflation in Taiwan—CPI rose 2.9% in 2024 and averaged ~2.6% in 2023–24—erodes consumer purchasing power, raising cost of living and pressure on household debt, which can increase non-performing loans for Bank SinoPac.

Bank SinoPac closely monitors these indicators to recalibrate retail deposit rates, credit card rewards and underwriting standards, having tightened credit lines by ~5% in high-risk segments in 2024.

Balancing competitive saver yields (market deposit rates climbed ~1.2 percentage points in 2024) with manageable loan terms is critical to sustain margins while containing consumer credit stress.

Exchange Rate Volatility

As a major international banker, Bank SinoPac is exposed to NTD volatility versus USD, JPY and CNY; NTD moved about 3.8% versus USD in 2024, amplifying translation risk for its foreign-currency assets (NT$ billions) and affecting trade finance pricing.

Currency swings raise clients' transaction costs and counterparty credit risk; in 2024 the bank reported expanded FX volumes and strengthened hedging, with derivatives usage up ~12% year-on-year to mitigate P&L volatility.

- NTD vs USD volatility ~3.8% in 2024

- Derivatives hedging use +12% YoY

- Higher FX-related transaction costs for trade clients

- Robust FX services central to risk management

Global Supply Chain Shifts

The reorganization of global supply chains, especially in tech, raises demand for corporate lending as 42% of Taiwanese electronics firms planned relocation or supplier diversification in 2023, creating opportunities for Bank SinoPac to offer capex and working-capital financing for factory moves and supplier onboarding.

Bank SinoPac must speed credit assessments and risk models to underwrite cross-border exposures and currency, logistics, and tariff risks amid supply-chain shifts.

- 42% of Taiwanese electronics firms planned relocation/diversification in 2023

- Demand for capex and working-capital loans rises with reshoring/nearshoring

- Requires faster, geography-aware credit and FX risk models

Higher rates cut NIM to ~1.35%; tech-led loan demand offsets FX hedging gains

Rising policy rates to 1.875% by Dec 2025 cut NIM to ~1.35% as funding costs outpaced lending yields; LDR ~78% in 2025. Taiwan GDP ~2.3% in 2024, ~2.5% in 2025 supports tech-led corporate loan demand; CPI ~2.9% in 2024 pressures household debt and NPL risk. NTD volatility ~3.8% vs USD (2024) and +12% YoY derivatives hedging increased FX service revenue.

| Metric | 2024 | 2025 |

|---|---|---|

| GDP growth | 2.3% | ~2.5% |

| CPI | 2.9% | ~2.6% avg |

| Policy rate | 0.875% | 1.875% |

| NIM (SinoPac) | — | ~1.35% |

| LDR | — | ~78% |

| NTD vs USD vol | ~3.8% | — |

| Derivatives hedging | +12% YoY | — |

Same Document Delivered

Bank SinoPac PESTLE Analysis

The preview shown here is the exact Bank SinoPac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are exactly what you’ll download immediately after payment.

Everything displayed is part of the final product, providing a complete PESTLE assessment you can apply straightaway.