Sinotrans Ltd. PESTLE Analysis

Your Competitive Advantage Starts with This Report

Understand how political shifts, trade policies, and technological advances shape Sinotrans Ltd.'s logistics dominance—our concise PESTLE snapshot highlights risks and growth levers you need to know. Ideal for investors and strategists, the full PESTLE delivers granular, actionable intelligence and editable charts to power decisions. Purchase now to access the complete analysis and stay ahead of industry headwinds.

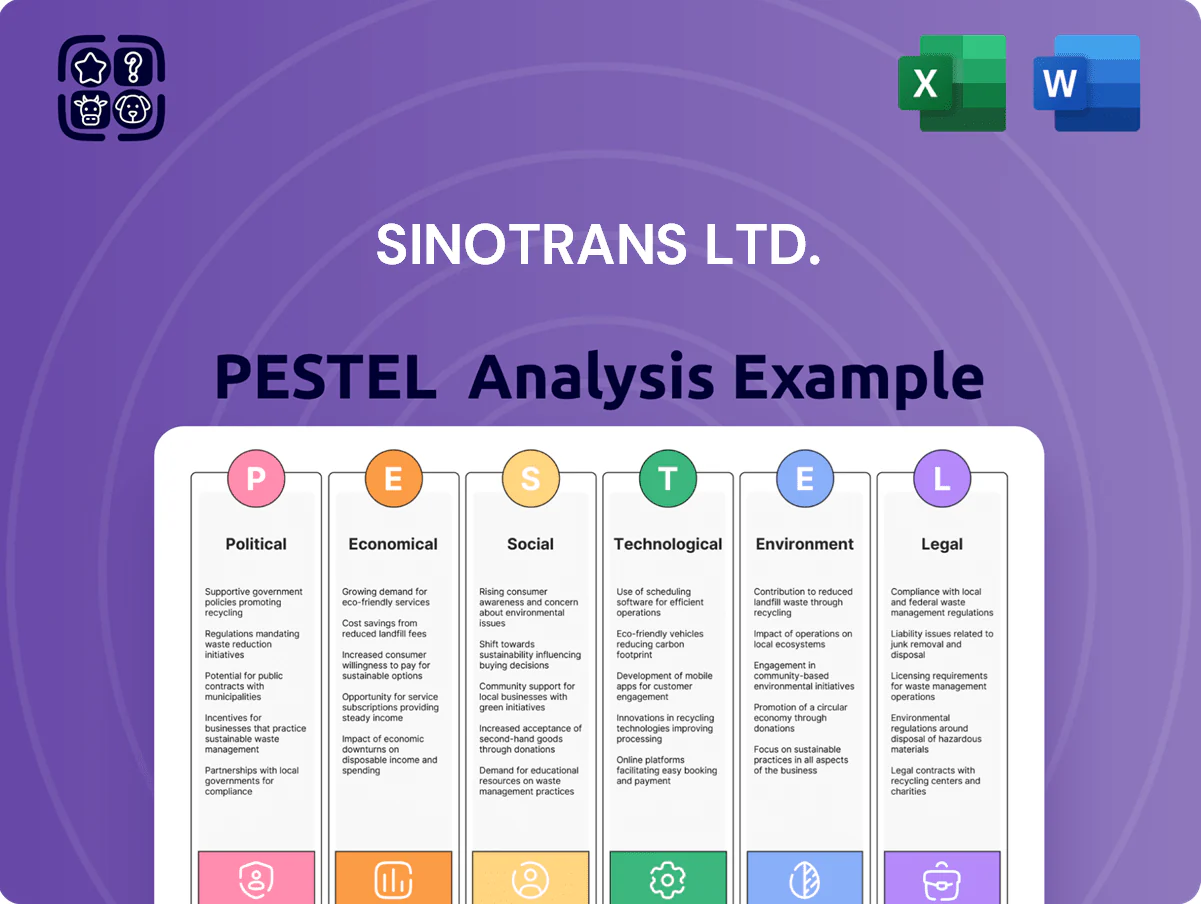

Political factors

Belt and Road Initiative integration

Sinotrans remains a pivotal Belt and Road player, leveraging state-backed support to expand in Eurasia and Africa; government-linked contracts accounted for about 42% of its international logistics revenue in FY2024 (HKD basis), and pipeline projects signed through late 2025 exceed USD 3.1 billion. Strategic infrastructure investments and diplomatic ties streamline cross-border operations, securing repeat high-value contracts for multimodal and port services across 15 BRI countries.

Geopolitical trade tensions

Ongoing trade friction between China and Western economies, notably the US and EU, raises volatility for international freight; US-China tariffs and EU export controls helped reduce China-US container volumes by about 7% in 2023 vs 2022, pressuring Sinotrans’ transpacific revenue streams.

Changing tariff structures and sanctions force frequent route and contract adjustments, with Asia-Europe container throughput down ~4% in 2024 YTD, impacting Sinotrans’ cargo mix and pricing power.

Sinotrans’ capacity to offer alternative routings and multi-modal solutions—rail via China-Europe corridors, feedering, and nearshoring logistics—was key in 2024 where diversified services contributed roughly 28% of logistics revenue, helping mitigate political risk.

State-owned enterprise reform policies

As a subsidiary of China Merchants Group, Sinotrans faces intensified state-owned enterprise reforms aimed at boosting ROE and capital efficiency; Beijing’s 2023–2025 SOE guidelines targeted a 10–15% rise in SOE capital returns, pressuring Sinotrans toward leaner operations. Recent mandates emphasize market-oriented competitiveness while protecting strategic logistics assets, pushing greater transparency—Sinotrans reported a 2024 revenue of RMB 78.4 billion and is streamlining assets to improve margins for both state and private investors.

Regional Comprehensive Economic Partnership impact

The RCEP, covering 30% of global GDP and 2.3 billion people, lowers tariffs and streamlines customs across 15 Asia-Pacific members, creating expanded routes for Sinotrans Ltd.; intra-RCEP trade rose 7.1% in 2023, offering measurable volume upside for freight and logistics revenue.

Sinotrans is reallocating capital to expand warehousing capacity by targeting a 12–15% increase in regional distribution footprint through 2025, aiming to capture higher-margin intra-regional flows as supply chains regionalize.

- RCEP = 30% global GDP, 2.3B people

- Intra-RCEP trade +7.1% in 2023

- Sinotrans targeting 12–15% warehousing footprint growth by 2025

National security and data sovereignty

By 2025 Chinese data security laws (Cybersecurity Law updates and Data Security Law enforcement) force Sinotrans to localize sensitive logistics data; non-compliance risks fines up to 10% of annual revenue and business suspension—material given Sinotrans 2024 revenue of RMB 74.6 billion (≈USD 10.8bn).

Sinotrans must balance compliance with cross-border data flows for global partners, requiring investments in secure gateways and legal teams to avoid bottlenecks in its international digital logistics services.

- 2024 revenue: RMB 74.6bn

- Potential fines: up to 10% revenue

- Requires data localization, secure gateways, legal staffing

Sinotrans: 42% state-backed intl revenue, BRI $3.1bn+, RCEP boost; data fines risk

State backing drives 42% of Sinotrans’ international logistics revenue (FY2024 HKD), BRI contracts >USD 3.1bn through 2025, RCEP boosted intra-regional trade +7.1% (2023), SOE reform targets +10–15% ROE pressuring efficiency; 2024 revenue RMB 74.6–78.4bn, data-localization fines up to 10% revenue require CAPEX for secure gateways and legal compliance.

| Metric | Value |

|---|---|

| State-linked intl revenue share (FY2024) | 42% |

| BRI pipeline thru 2025 | USD 3.1bn+ |

| Intra-RCEP trade change (2023) | +7.1% |

| 2024 revenue | RMB 74.6–78.4bn |

| Potential data fines | Up to 10% revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sinotrans Ltd. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific context.

A concise, easily shareable Sinotrans Ltd. PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick alignment in meetings or presentations.

Economic factors

Global trade volume fluctuations

The health of Sinotrans is tightly linked to global trade volumes, which grew unevenly to an estimated 3.5% in 2024 and slowed to ~2.1% in 2025 as OECD consumer demand softened; weaker activity in the US and EU trimmed freight volumes, pressuring forwarding revenue. Economic slowdowns in key markets reduce spot rates and utilization, while Sinotrans shifts capacity toward Southeast Asia and Latin America—regions posting 2024–25 trade growth above 4%—to capture higher-demand corridors.

Fuel price and energy cost volatility

Energy costs are a major operational expense for Sinotrans, with fuel accounting for roughly 12–15% of total operating costs in 2024 for its trucking and shipping segments. Global oil price volatility—Brent averaging about $86/barrel in 2024 after spiking past $110 in 2022–23 due to OPEC+ cuts and geopolitical conflicts—directly compresses margins. Sinotrans applies fuel surcharges and uses hedging—fuel derivatives covered about 20% of consumption in 2024—to mitigate risks, but sudden price spikes still create quarterly profit pressure.

Currency exchange rate sensitivity

As a global logistics provider, Sinotrans records revenues and costs in multiple currencies, exposing it to RMB/USD volatility; the RMB moved about 5% against the USD in 2024, amplifying margin risk on cross-border freight. Large swings can dent the competitiveness of Chinese exports and raise international operating costs—Sinotrans reported FX losses of CNY 210 million in H1 2025. Robust treasury management and hedging (forwards/options) are therefore critical to protect earnings.

Inflationary pressures on labor and operations

Persistent inflation across China, Southeast Asia and Europe pushed labor costs up 6-8% y/y in 2024 and raised warehouse rents by ~10% in key hubs, squeezing Sinotrans margins as maintenance and fuel costs rose; management reported CNY 200–300 million incremental operating pressure in 2024.

Passing costs risks market share loss to lower-cost carriers, so Sinotrans is accelerating automation and process optimization—capex on tech rose ~18% in 2024—to offset rising overhead.

- Labor +6–8% y/y (2024)

- Warehouse rents +~10% in major hubs (2024)

- Estimated CNY 200–300m incremental operating pressure (2024)

- Tech capex +18% to drive automation (2024)

Interest rate environment and capital expenditure

China's 1-year loan prime rate at 3.55% (Dec 2025) and global US Fed funds near 5.25–5.50% raise Sinotrans' average borrowing costs, potentially slowing fleet modernization and warehouse CAPEX given capital intensity.

Lower rates historically enabled rapid expansion; maintaining a conservative debt-to-equity (Sinotrans' 2024 adjusted gearing ~0.42) preserves creditworthiness for future issuance.

- Higher rates → higher cost of debt, CAPEX delays

- Lower rates → enables aggressive fleet/warehouse expansion

- Target gearing ~0.4–0.5 to protect credit profile

Global trade cools, costs climb: fuel, wages & rents squeeze margins as rates stay high

Global trade slowed to ~2.1% in 2025 after 3.5% in 2024, pressuring freight rates; fuel ~12–15% of costs, Brent avg $86/bbl (2024); RMB moved ~5% vs USD (2024); labor +6–8% y/y and warehouse rents +10% (2024), tech capex +18%; LPR 1yr 3.55% (Dec 2025), Fed funds ~5.25–5.50%, adjusted gearing ~0.42 (2024).

| Metric | Value |

|---|---|

| Global trade growth | 3.5% (2024); 2.1% (2025) |

| Brent | $86/bbl (2024) |

| Fuel % costs | 12–15% (2024) |

| RMB vs USD | ~5% move (2024) |

| Labor / rents | +6–8% / +10% (2024) |

| Tech capex | +18% (2024) |

| Rates | LPR 1yr 3.55% (Dec 2025); Fed 5.25–5.50% |

| Gearing | ~0.42 (2024) |

Same Document Delivered

Sinotrans Ltd. PESTLE Analysis

The preview shown here is the exact Sinotrans Ltd. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible here are identical to the downloadable file you’ll get immediately after payment.

What you see is the finished product—comprehensive analysis delivered exactly as displayed, with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Understand how political shifts, trade policies, and technological advances shape Sinotrans Ltd.'s logistics dominance—our concise PESTLE snapshot highlights risks and growth levers you need to know. Ideal for investors and strategists, the full PESTLE delivers granular, actionable intelligence and editable charts to power decisions. Purchase now to access the complete analysis and stay ahead of industry headwinds.

Political factors

Belt and Road Initiative integration

Sinotrans remains a pivotal Belt and Road player, leveraging state-backed support to expand in Eurasia and Africa; government-linked contracts accounted for about 42% of its international logistics revenue in FY2024 (HKD basis), and pipeline projects signed through late 2025 exceed USD 3.1 billion. Strategic infrastructure investments and diplomatic ties streamline cross-border operations, securing repeat high-value contracts for multimodal and port services across 15 BRI countries.

Geopolitical trade tensions

Ongoing trade friction between China and Western economies, notably the US and EU, raises volatility for international freight; US-China tariffs and EU export controls helped reduce China-US container volumes by about 7% in 2023 vs 2022, pressuring Sinotrans’ transpacific revenue streams.

Changing tariff structures and sanctions force frequent route and contract adjustments, with Asia-Europe container throughput down ~4% in 2024 YTD, impacting Sinotrans’ cargo mix and pricing power.

Sinotrans’ capacity to offer alternative routings and multi-modal solutions—rail via China-Europe corridors, feedering, and nearshoring logistics—was key in 2024 where diversified services contributed roughly 28% of logistics revenue, helping mitigate political risk.

State-owned enterprise reform policies

As a subsidiary of China Merchants Group, Sinotrans faces intensified state-owned enterprise reforms aimed at boosting ROE and capital efficiency; Beijing’s 2023–2025 SOE guidelines targeted a 10–15% rise in SOE capital returns, pressuring Sinotrans toward leaner operations. Recent mandates emphasize market-oriented competitiveness while protecting strategic logistics assets, pushing greater transparency—Sinotrans reported a 2024 revenue of RMB 78.4 billion and is streamlining assets to improve margins for both state and private investors.

Regional Comprehensive Economic Partnership impact

The RCEP, covering 30% of global GDP and 2.3 billion people, lowers tariffs and streamlines customs across 15 Asia-Pacific members, creating expanded routes for Sinotrans Ltd.; intra-RCEP trade rose 7.1% in 2023, offering measurable volume upside for freight and logistics revenue.

Sinotrans is reallocating capital to expand warehousing capacity by targeting a 12–15% increase in regional distribution footprint through 2025, aiming to capture higher-margin intra-regional flows as supply chains regionalize.

- RCEP = 30% global GDP, 2.3B people

- Intra-RCEP trade +7.1% in 2023

- Sinotrans targeting 12–15% warehousing footprint growth by 2025

National security and data sovereignty

By 2025 Chinese data security laws (Cybersecurity Law updates and Data Security Law enforcement) force Sinotrans to localize sensitive logistics data; non-compliance risks fines up to 10% of annual revenue and business suspension—material given Sinotrans 2024 revenue of RMB 74.6 billion (≈USD 10.8bn).

Sinotrans must balance compliance with cross-border data flows for global partners, requiring investments in secure gateways and legal teams to avoid bottlenecks in its international digital logistics services.

- 2024 revenue: RMB 74.6bn

- Potential fines: up to 10% revenue

- Requires data localization, secure gateways, legal staffing

Sinotrans: 42% state-backed intl revenue, BRI $3.1bn+, RCEP boost; data fines risk

State backing drives 42% of Sinotrans’ international logistics revenue (FY2024 HKD), BRI contracts >USD 3.1bn through 2025, RCEP boosted intra-regional trade +7.1% (2023), SOE reform targets +10–15% ROE pressuring efficiency; 2024 revenue RMB 74.6–78.4bn, data-localization fines up to 10% revenue require CAPEX for secure gateways and legal compliance.

| Metric | Value |

|---|---|

| State-linked intl revenue share (FY2024) | 42% |

| BRI pipeline thru 2025 | USD 3.1bn+ |

| Intra-RCEP trade change (2023) | +7.1% |

| 2024 revenue | RMB 74.6–78.4bn |

| Potential data fines | Up to 10% revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sinotrans Ltd. across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific context.

A concise, easily shareable Sinotrans Ltd. PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick alignment in meetings or presentations.

Economic factors

Global trade volume fluctuations

The health of Sinotrans is tightly linked to global trade volumes, which grew unevenly to an estimated 3.5% in 2024 and slowed to ~2.1% in 2025 as OECD consumer demand softened; weaker activity in the US and EU trimmed freight volumes, pressuring forwarding revenue. Economic slowdowns in key markets reduce spot rates and utilization, while Sinotrans shifts capacity toward Southeast Asia and Latin America—regions posting 2024–25 trade growth above 4%—to capture higher-demand corridors.

Fuel price and energy cost volatility

Energy costs are a major operational expense for Sinotrans, with fuel accounting for roughly 12–15% of total operating costs in 2024 for its trucking and shipping segments. Global oil price volatility—Brent averaging about $86/barrel in 2024 after spiking past $110 in 2022–23 due to OPEC+ cuts and geopolitical conflicts—directly compresses margins. Sinotrans applies fuel surcharges and uses hedging—fuel derivatives covered about 20% of consumption in 2024—to mitigate risks, but sudden price spikes still create quarterly profit pressure.

Currency exchange rate sensitivity

As a global logistics provider, Sinotrans records revenues and costs in multiple currencies, exposing it to RMB/USD volatility; the RMB moved about 5% against the USD in 2024, amplifying margin risk on cross-border freight. Large swings can dent the competitiveness of Chinese exports and raise international operating costs—Sinotrans reported FX losses of CNY 210 million in H1 2025. Robust treasury management and hedging (forwards/options) are therefore critical to protect earnings.

Inflationary pressures on labor and operations

Persistent inflation across China, Southeast Asia and Europe pushed labor costs up 6-8% y/y in 2024 and raised warehouse rents by ~10% in key hubs, squeezing Sinotrans margins as maintenance and fuel costs rose; management reported CNY 200–300 million incremental operating pressure in 2024.

Passing costs risks market share loss to lower-cost carriers, so Sinotrans is accelerating automation and process optimization—capex on tech rose ~18% in 2024—to offset rising overhead.

- Labor +6–8% y/y (2024)

- Warehouse rents +~10% in major hubs (2024)

- Estimated CNY 200–300m incremental operating pressure (2024)

- Tech capex +18% to drive automation (2024)

Interest rate environment and capital expenditure

China's 1-year loan prime rate at 3.55% (Dec 2025) and global US Fed funds near 5.25–5.50% raise Sinotrans' average borrowing costs, potentially slowing fleet modernization and warehouse CAPEX given capital intensity.

Lower rates historically enabled rapid expansion; maintaining a conservative debt-to-equity (Sinotrans' 2024 adjusted gearing ~0.42) preserves creditworthiness for future issuance.

- Higher rates → higher cost of debt, CAPEX delays

- Lower rates → enables aggressive fleet/warehouse expansion

- Target gearing ~0.4–0.5 to protect credit profile

Global trade cools, costs climb: fuel, wages & rents squeeze margins as rates stay high

Global trade slowed to ~2.1% in 2025 after 3.5% in 2024, pressuring freight rates; fuel ~12–15% of costs, Brent avg $86/bbl (2024); RMB moved ~5% vs USD (2024); labor +6–8% y/y and warehouse rents +10% (2024), tech capex +18%; LPR 1yr 3.55% (Dec 2025), Fed funds ~5.25–5.50%, adjusted gearing ~0.42 (2024).

| Metric | Value |

|---|---|

| Global trade growth | 3.5% (2024); 2.1% (2025) |

| Brent | $86/bbl (2024) |

| Fuel % costs | 12–15% (2024) |

| RMB vs USD | ~5% move (2024) |

| Labor / rents | +6–8% / +10% (2024) |

| Tech capex | +18% (2024) |

| Rates | LPR 1yr 3.55% (Dec 2025); Fed 5.25–5.50% |

| Gearing | ~0.42 (2024) |

Same Document Delivered

Sinotrans Ltd. PESTLE Analysis

The preview shown here is the exact Sinotrans Ltd. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible here are identical to the downloadable file you’ll get immediately after payment.

What you see is the finished product—comprehensive analysis delivered exactly as displayed, with no surprises.