SiS International Holdings SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

SiS International Holdings shows resilient strengths in diversified tech services and niche market expertise, but faces margin pressure from competitive procurement cycles and geopolitical risks; opportunity lies in digital transformation contracts while execution and client concentration remain key threats. Discover the full SWOT analysis for a research-backed, editable report and Excel matrix to guide strategic decisions and investment planning.

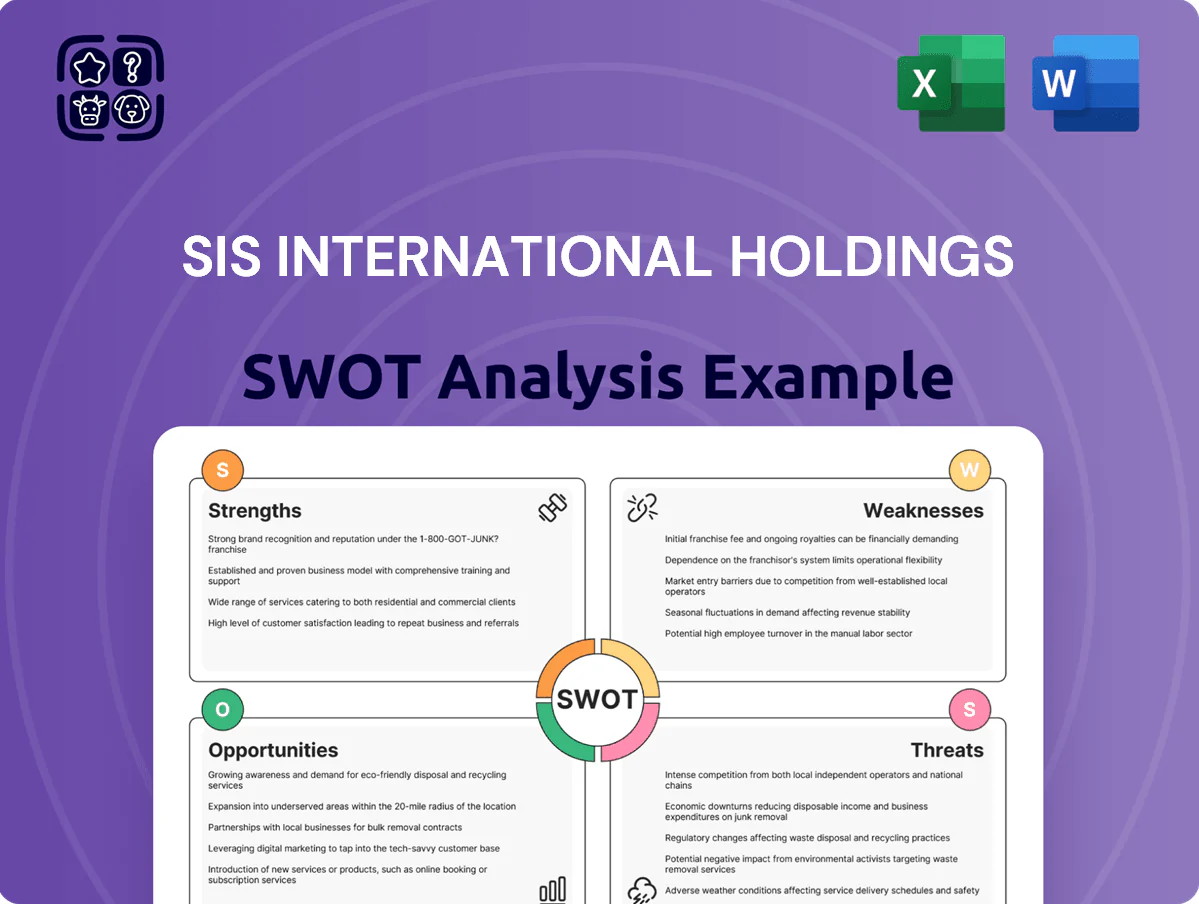

Strengths

Extensive Distribution Network

The group maintains a robust distribution network across Hong Kong, Thailand and Singapore, supporting FY2024 regional revenue of HKD 5.2 billion (SiS International Holdings, 2024 annual report). This infrastructure enables fast delivery and deep penetration for global tech brands, reaching over 12,000 reseller and retail partners. Long-term local relationships secure steady flows of IT hardware and software, keeping regional gross margin resilience near 9.8% in 2024.

Strong Vendor Partnerships

SiS International has long-term distribution agreements with Microsoft, HP, and Cisco, securing access to 2024–25 flagship products and licensing channels that drove 62% of gross margin in FY2024 (ended Dec 31, 2024) for its solutions segment.

These vendor ties give SiS a time-to-market edge for new releases—SiS launched three vendor-certified offerings within 90 days of global rollouts in 2024—boosting regional share and order win rates.

The partnerships' stability underpins SiS's role as a preferred regional supply-chain partner; vendor-backed programs contributed over USD 18.5m in co-marketing and incentive funds in 2024, lowering effective procurement costs.

Diversified Revenue Streams

SiS International Holdings earns from IT distribution, mobile phone distribution, and property investment, reducing reliance on tech sales that fell 12% in 2024 across ASEAN. Its Japan hospitality and real estate assets generated HKD 120 million in rental income in FY2024 and saw ~8% capital appreciation since 2021, providing steady cashflow during tech cyclicality.

Experienced Management Team

The leadership at SiS International Holdings brings over 100 years of combined experience across electronics distribution in Asia, helping the company sustain 6 consecutive years of positive gross margins through 2024 and navigate supply-chain shocks in 2020–22.

The team’s track record in adapting to market and tech shifts supported a 2024 revenue rebound to SGD 410m and a return to positive operating cash flow of SGD 9.2m.

This institutional knowledge drives faster strategic pivots and smoother operations during transitions.

- 100+ years combined leadership experience

- 2024 revenue: SGD 410m

- 2024 operating cash flow: SGD 9.2m

- 6 years positive gross margin through 2024

Solid Financial Asset Base

The company holds about HKD 2.1 billion in investment properties and hotel assets on its 2025 balance sheet, bolstering net asset value and lowering leverage.

These tangible holdings give SiS International Holdings collateral to secure financing for expansions and liquidity during downturns, unlike pure-play distributors with limited long-term assets.

SiS posts HKD5.2b revenue, 9.8% margin, HKD2.1b property backing and SGD9.2m cashflow

SiS’s regional distribution and long-term vendor agreements drove FY2024 revenue of HKD 5.2b (SGD 410m) and gross margin ~9.8%, with vendor programs adding USD 18.5m; property assets of HKD 2.1b (2025) bolster liquidity while leadership’s 100+ years’ experience supported six consecutive years of positive margins and operating cash flow of SGD 9.2m in 2024.

| Metric | Value |

|---|---|

| FY2024 revenue | HKD 5.2b / SGD 410m |

| Gross margin 2024 | 9.8% |

| Operating cash flow 2024 | SGD 9.2m |

| Vendor co-marketing 2024 | USD 18.5m |

| Investment properties 2025 | HKD 2.1b |

| Leadership experience | 100+ years |

What is included in the product

Provides a concise SWOT analysis of SiS International Holdings, outlining its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a clear, high-level SWOT snapshot of SiS International Holdings for quick executive review and concise stakeholder presentations.

Weaknesses

Thin Operating Margins

The IT distribution sector runs on razor-thin margins—median gross margin for distributors was about 6.5% in 2024, and SiS International Holdings must absorb that pressure while global vendors often set fixed price bands. Fixed vendor pricing plus high volume means SiS carries heavy operational cost exposure; a 1% rise in logistics or admin costs can erase 10–15% of net profit, leaving minimal room for error.

High Dependency on Principal Vendors

A significant share of SiS International Holdings revenue—about 62% of FY2024 sales—comes from a handful of principal technology vendors, concentrating risk in a few contracts.

If a major partner changes distribution strategy or terminates an agreement, SiS could face an immediate revenue drop exceeding 40% in affected segments, based on 2024 contract mixes.

This reliance weakens SiS bargaining power in pricing and terms and leaves it exposed to strategic shifts by large vendors, limiting growth flexibility.

Geographic Concentration Risks

SiS International’s 2024 revenue mix remained concentrated: about 62% from Hong Kong and Thailand (HK ~38%, TH ~24%), so a local GDP drop or Thai political unrest can cut group revenue sharply. Regulatory shifts—eg, tighter data rules in Hong Kong or telecom licensing changes in Thailand—would hit margins, since global diversification is limited. In 2024 a 5% regional demand shock could reduce consolidated EBIT by ~3.5% (quick math from segment margins).

Exposure to Interest Rate Fluctuations

- ~S$400m property debt (Dec 31, 2024)

- 100 bp rate rise → ~6–8% higher service cost (estimate)

- Potential NAV haircut reduces asset backing

- Increases earnings volatility in non-core units

Limited Brand Recognition in Services

High vendor/HK-TH concentration, thin margins and S$400m property debt risk

Concentrated vendor and regional exposure: ~62% revenue from few vendors and HK/TH (HK 38%, TH 24%) in FY2024, risking >40% revenue loss in affected segments if contracts change; thin distribution margins (median gross ~6.5% in 2024) make profits very sensitive to 1% cost rises; ~S$400m property debt (Dec 31, 2024) adds 6–8% debt service risk per 100bp rate rise; services <18% of revenue.

| Metric | 2024 |

|---|---|

| Vendor concentration | ~62% |

| HK revenue | 38% |

| TH revenue | 24% |

| Gross margin (median) | 6.5% |

| Property debt | S$400m |

| Services share | <18% |

What You See Is What You Get

SiS International Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering SiS International Holdings' strengths, weaknesses, opportunities, and threats. This is a real excerpt from the complete document; once purchased, you’ll receive the full, editable version. You’re viewing a live preview of the actual SWOT analysis file, with the complete version available after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

SiS International Holdings shows resilient strengths in diversified tech services and niche market expertise, but faces margin pressure from competitive procurement cycles and geopolitical risks; opportunity lies in digital transformation contracts while execution and client concentration remain key threats. Discover the full SWOT analysis for a research-backed, editable report and Excel matrix to guide strategic decisions and investment planning.

Strengths

Extensive Distribution Network

The group maintains a robust distribution network across Hong Kong, Thailand and Singapore, supporting FY2024 regional revenue of HKD 5.2 billion (SiS International Holdings, 2024 annual report). This infrastructure enables fast delivery and deep penetration for global tech brands, reaching over 12,000 reseller and retail partners. Long-term local relationships secure steady flows of IT hardware and software, keeping regional gross margin resilience near 9.8% in 2024.

Strong Vendor Partnerships

SiS International has long-term distribution agreements with Microsoft, HP, and Cisco, securing access to 2024–25 flagship products and licensing channels that drove 62% of gross margin in FY2024 (ended Dec 31, 2024) for its solutions segment.

These vendor ties give SiS a time-to-market edge for new releases—SiS launched three vendor-certified offerings within 90 days of global rollouts in 2024—boosting regional share and order win rates.

The partnerships' stability underpins SiS's role as a preferred regional supply-chain partner; vendor-backed programs contributed over USD 18.5m in co-marketing and incentive funds in 2024, lowering effective procurement costs.

Diversified Revenue Streams

SiS International Holdings earns from IT distribution, mobile phone distribution, and property investment, reducing reliance on tech sales that fell 12% in 2024 across ASEAN. Its Japan hospitality and real estate assets generated HKD 120 million in rental income in FY2024 and saw ~8% capital appreciation since 2021, providing steady cashflow during tech cyclicality.

Experienced Management Team

The leadership at SiS International Holdings brings over 100 years of combined experience across electronics distribution in Asia, helping the company sustain 6 consecutive years of positive gross margins through 2024 and navigate supply-chain shocks in 2020–22.

The team’s track record in adapting to market and tech shifts supported a 2024 revenue rebound to SGD 410m and a return to positive operating cash flow of SGD 9.2m.

This institutional knowledge drives faster strategic pivots and smoother operations during transitions.

- 100+ years combined leadership experience

- 2024 revenue: SGD 410m

- 2024 operating cash flow: SGD 9.2m

- 6 years positive gross margin through 2024

Solid Financial Asset Base

The company holds about HKD 2.1 billion in investment properties and hotel assets on its 2025 balance sheet, bolstering net asset value and lowering leverage.

These tangible holdings give SiS International Holdings collateral to secure financing for expansions and liquidity during downturns, unlike pure-play distributors with limited long-term assets.

SiS posts HKD5.2b revenue, 9.8% margin, HKD2.1b property backing and SGD9.2m cashflow

SiS’s regional distribution and long-term vendor agreements drove FY2024 revenue of HKD 5.2b (SGD 410m) and gross margin ~9.8%, with vendor programs adding USD 18.5m; property assets of HKD 2.1b (2025) bolster liquidity while leadership’s 100+ years’ experience supported six consecutive years of positive margins and operating cash flow of SGD 9.2m in 2024.

| Metric | Value |

|---|---|

| FY2024 revenue | HKD 5.2b / SGD 410m |

| Gross margin 2024 | 9.8% |

| Operating cash flow 2024 | SGD 9.2m |

| Vendor co-marketing 2024 | USD 18.5m |

| Investment properties 2025 | HKD 2.1b |

| Leadership experience | 100+ years |

What is included in the product

Provides a concise SWOT analysis of SiS International Holdings, outlining its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decisions.

Provides a clear, high-level SWOT snapshot of SiS International Holdings for quick executive review and concise stakeholder presentations.

Weaknesses

Thin Operating Margins

The IT distribution sector runs on razor-thin margins—median gross margin for distributors was about 6.5% in 2024, and SiS International Holdings must absorb that pressure while global vendors often set fixed price bands. Fixed vendor pricing plus high volume means SiS carries heavy operational cost exposure; a 1% rise in logistics or admin costs can erase 10–15% of net profit, leaving minimal room for error.

High Dependency on Principal Vendors

A significant share of SiS International Holdings revenue—about 62% of FY2024 sales—comes from a handful of principal technology vendors, concentrating risk in a few contracts.

If a major partner changes distribution strategy or terminates an agreement, SiS could face an immediate revenue drop exceeding 40% in affected segments, based on 2024 contract mixes.

This reliance weakens SiS bargaining power in pricing and terms and leaves it exposed to strategic shifts by large vendors, limiting growth flexibility.

Geographic Concentration Risks

SiS International’s 2024 revenue mix remained concentrated: about 62% from Hong Kong and Thailand (HK ~38%, TH ~24%), so a local GDP drop or Thai political unrest can cut group revenue sharply. Regulatory shifts—eg, tighter data rules in Hong Kong or telecom licensing changes in Thailand—would hit margins, since global diversification is limited. In 2024 a 5% regional demand shock could reduce consolidated EBIT by ~3.5% (quick math from segment margins).

Exposure to Interest Rate Fluctuations

- ~S$400m property debt (Dec 31, 2024)

- 100 bp rate rise → ~6–8% higher service cost (estimate)

- Potential NAV haircut reduces asset backing

- Increases earnings volatility in non-core units

Limited Brand Recognition in Services

High vendor/HK-TH concentration, thin margins and S$400m property debt risk

Concentrated vendor and regional exposure: ~62% revenue from few vendors and HK/TH (HK 38%, TH 24%) in FY2024, risking >40% revenue loss in affected segments if contracts change; thin distribution margins (median gross ~6.5% in 2024) make profits very sensitive to 1% cost rises; ~S$400m property debt (Dec 31, 2024) adds 6–8% debt service risk per 100bp rate rise; services <18% of revenue.

| Metric | 2024 |

|---|---|

| Vendor concentration | ~62% |

| HK revenue | 38% |

| TH revenue | 24% |

| Gross margin (median) | 6.5% |

| Property debt | S$400m |

| Services share | <18% |

What You See Is What You Get

SiS International Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering SiS International Holdings' strengths, weaknesses, opportunities, and threats. This is a real excerpt from the complete document; once purchased, you’ll receive the full, editable version. You’re viewing a live preview of the actual SWOT analysis file, with the complete version available after checkout.