Sisram Medical Porter's Five Forces Analysis

Don't Miss the Bigger Picture

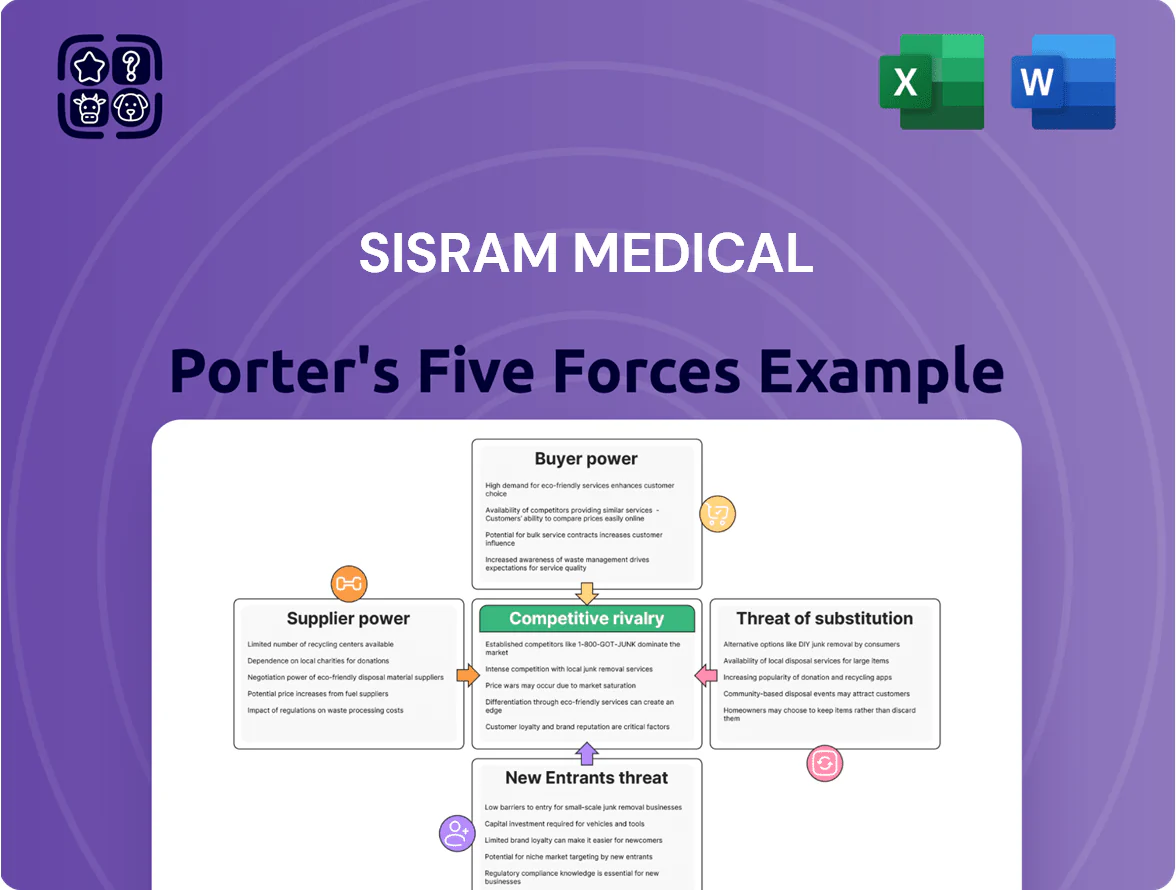

Sisram Medical faces moderate supplier leverage, intense competitive rivalry among device and service providers, and a rising threat from innovative substitutes and new entrants in aesthetic medicine, with buyer power amplified by channel consolidation and price sensitivity.

Suppliers Bargaining Power

Specialized component dependency

Sisram Medical depends on high-precision optical fibers, laser diodes, and specialized electronics for its energy-based devices; these parts are niche: about 70–80% of medical-grade laser sub-assemblies come from fewer than 10 certified global vendors as of 2025.

Basic components are commoditized, but the limited supplier pool gives moderate bargaining power—supply disruptions could delay production and affect quality, risking revenue dips given 2024 device gross margins around 48%.

Regulatory compliance of the supply chain

Suppliers in the medical aesthetic industry must meet strict international standards like ISO 13485, which shrinks the supplier base and raises bargaining power for compliant vendors.

For Sisram Medical, this concentration means fewer alternatives and higher switching costs, pushing supplier leverage in pricing and lead times.

By end-2025, demand for sustainable, ethically sourced components—used in ~18–25% of device BOMs per recent industry surveys—further narrows viable partners, increasing their negotiation leverage.

Integration with Fosun Pharma ecosystem

As a Fosun Pharma subsidiary, Sisram Medical taps into the parent’s global procurement network—Fosun Pharma reported RMB 120.4 billion in 2024 revenue, boosting buying scale and supplier leverage. This scale cuts supplier power: bulk contracts and group-level framework agreements lower input costs and improve payment and lead-time terms. During 2020–2024 supply shocks, Fosun’s priority allocation helped Sisram maintain >95% fulfilment on key laser components. That priority and scale let Sisram secure preferential pricing and faster delivery.

Switching costs for technical hardware

The technical complexity of Sisram’s Alma devices makes switching suppliers for critical components costly: re-engineering and fresh regulatory filings (e.g., FDA 510(k) or EU MDR) can take 6–18 months and cost $0.5–$3M per device variant, giving existing suppliers measurable leverage.

As a result, Sisram favors multi-year, collaborative contracts with key tech partners, reducing supply disruption risk and capex for redesigns; long-term deals often cover 60–80% of critical-component spend.

- 6–18 months typical re-certification delay

- $0.5–$3M estimated redesign/regulatory cost

- 60–80% of critical-component spend under long-term contracts

Geographic concentration of raw materials

The sourcing of rare earths and specialized minerals for Sisram Medical’s laser devices is heavily concentrated in Asia, notably China, which supplied about 60–70% of global rare earth oxides in 2024; that geographic concentration lets regional suppliers and policy shifts drive price and availability swings.

Suppliers’ influence rose after China’s export quota changes in 2022–2023 and export duty guidance in 2024, so Sisram must hedge procurement and diversify contracts to keep cost of goods sold stable through end-2025 amid commodity volatility.

- China supplied ~65% of rare earth oxides in 2024

- Price volatility: +22% peak-to-trough for key minerals in 2024

- Mitigation: diversify suppliers, long-term contracts, strategic inventory

Supplier power high despite Fosun scale—supply concentration, switching costs risk COGS

Suppliers hold moderate-to-high power: 70–80% of laser sub-assemblies from <10 vendors (2025), China supplied ~65% of rare earths (2024), and device gross margin ~48% (2024), so disruptions raise COGS risk. Fosun scale (RMB 120.4bn revenue, 2024) cuts supplier power; long-term contracts cover 60–80% of critical spend, while switching costs (6–18 months, $0.5–$3M) maintain supplier leverage.

| Metric | Value |

|---|---|

| Laser vendors concentration | 70–80% from <10 |

| Rare earths supply (China) | ~65% (2024) |

| Device gross margin | ~48% (2024) |

| Fosun Pharma revenue | RMB 120.4bn (2024) |

| Switching cost | 6–18m; $0.5–$3M |

| Long-term contract coverage | 60–80% |

What is included in the product

Tailored Five Forces analysis for Sisram Medical that uncovers competitive intensity, buyer/supplier power, threat of entrants and substitutes, and identifies disruptive trends and entry barriers affecting its profitability.

Concise Porter's Five Forces snapshot for Sisram Medical—quickly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

High switching costs for practitioners

Medical practices invest heavily in Sisram’s platforms—Soprano or Harmony—often spending $50k–$200k per device and 40–80 training hours per staff member, creating high switching costs. Once integrated, clinics face downtime, retraining, and capital write-offs, so switching to competitors is rarely economical. This lock-in lowers customer bargaining power and lets Sisram keep stable consumable margins (20–35% gross) and service fees. What this hides: small clinics still push back on bulk pricing.

Brand recognition and patient demand

Alma brand recognition drives patient demand: surveys show 48% of aesthetic patients in 2024 requested specific device brands, with Alma among the top three, pushing clinics to stock Sisram technology to stay competitive.

Because patients often choose treatments, clinics have reduced bargaining power; Sisram reported 2024 device revenues up 22%, indicating pricing resilience despite buyer concentration.

Fragmentation of the global clinic market

The majority of Sisram Medical’s customers are independent med spas, dermatologists, and small plastic surgery practices; this fragmentation means single buyers rarely exceed 1–2% of Sisram’s revenue, so they lack volume leverage to force discounts.

Large corporate aesthetic groups grew ~18% CAGR 2019–2024 but still account for under 20% of global clinic revenues, keeping pricing power with manufacturers like Sisram.

Essential nature of after-sales support

Customers depend on Sisram for technical support, software updates, and proprietary consumables, creating high switching costs; in 2024 Sisram’s service revenue made up ~28% of medical segment sales, reinforcing recurring dependence.

This ongoing service tie shifts bargaining power to Sisram because clinics risk costly downtime—average device downtime loss ~USD 2,400/day for aesthetic clinics—so they keep using certified parts and service.

- Service revenue ~28% of medical sales (2024)

- Avg downtime cost ~USD 2,400/day

- Certification required for warranty and compliance

Access to financing and leasing models

By 2025 Sisram Medical expanded flexible financing and leasing, cutting upfront costs and boosting device adoption by ~35% versus 2022, widening the practitioner pool but lowering buyer bargaining as clinics tie to Sisram’s contract terms.

Leases commonly run 36–60 months and include service agreements that lock in maintenance revenue (estimated 20–30% of contract value), increasing vendor dependence and reducing customer exit options.

- Adoption +35% vs 2022

- Typical lease 36–60 months

- Service revenue 20–30% of contracts

- Higher switching costs, lower buyer power

Sisram’s pricing power: high capex, costly downtime & recurring 20–35% consumable margins

Sisram faces low customer bargaining power: high device capex (USD 50k–200k), 40–80 training hours, service revenue ~28% of medical sales (2024), leases (36–60 months) boosted adoption +35% vs 2022, and avg downtime cost ~USD 2,400/day—so clinics accept premiums and recurring consumable margins (20–35%).

| Metric | Value (2024/2025) |

|---|---|

| Device price | USD 50k–200k |

| Training | 40–80 hours |

| Service rev | ~28% medical sales |

| Adoption vs 2022 | +35% |

| Lease term | 36–60 months |

| Downtime cost | ~USD 2,400/day |

| Consumable margin | 20–35% |

Preview the Actual Deliverable

Sisram Medical Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sisram Medical you'll receive upon purchase—no placeholders or mockups; the full, professionally formatted document is ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Sisram Medical faces moderate supplier leverage, intense competitive rivalry among device and service providers, and a rising threat from innovative substitutes and new entrants in aesthetic medicine, with buyer power amplified by channel consolidation and price sensitivity.

Suppliers Bargaining Power

Specialized component dependency

Sisram Medical depends on high-precision optical fibers, laser diodes, and specialized electronics for its energy-based devices; these parts are niche: about 70–80% of medical-grade laser sub-assemblies come from fewer than 10 certified global vendors as of 2025.

Basic components are commoditized, but the limited supplier pool gives moderate bargaining power—supply disruptions could delay production and affect quality, risking revenue dips given 2024 device gross margins around 48%.

Regulatory compliance of the supply chain

Suppliers in the medical aesthetic industry must meet strict international standards like ISO 13485, which shrinks the supplier base and raises bargaining power for compliant vendors.

For Sisram Medical, this concentration means fewer alternatives and higher switching costs, pushing supplier leverage in pricing and lead times.

By end-2025, demand for sustainable, ethically sourced components—used in ~18–25% of device BOMs per recent industry surveys—further narrows viable partners, increasing their negotiation leverage.

Integration with Fosun Pharma ecosystem

As a Fosun Pharma subsidiary, Sisram Medical taps into the parent’s global procurement network—Fosun Pharma reported RMB 120.4 billion in 2024 revenue, boosting buying scale and supplier leverage. This scale cuts supplier power: bulk contracts and group-level framework agreements lower input costs and improve payment and lead-time terms. During 2020–2024 supply shocks, Fosun’s priority allocation helped Sisram maintain >95% fulfilment on key laser components. That priority and scale let Sisram secure preferential pricing and faster delivery.

Switching costs for technical hardware

The technical complexity of Sisram’s Alma devices makes switching suppliers for critical components costly: re-engineering and fresh regulatory filings (e.g., FDA 510(k) or EU MDR) can take 6–18 months and cost $0.5–$3M per device variant, giving existing suppliers measurable leverage.

As a result, Sisram favors multi-year, collaborative contracts with key tech partners, reducing supply disruption risk and capex for redesigns; long-term deals often cover 60–80% of critical-component spend.

- 6–18 months typical re-certification delay

- $0.5–$3M estimated redesign/regulatory cost

- 60–80% of critical-component spend under long-term contracts

Geographic concentration of raw materials

The sourcing of rare earths and specialized minerals for Sisram Medical’s laser devices is heavily concentrated in Asia, notably China, which supplied about 60–70% of global rare earth oxides in 2024; that geographic concentration lets regional suppliers and policy shifts drive price and availability swings.

Suppliers’ influence rose after China’s export quota changes in 2022–2023 and export duty guidance in 2024, so Sisram must hedge procurement and diversify contracts to keep cost of goods sold stable through end-2025 amid commodity volatility.

- China supplied ~65% of rare earth oxides in 2024

- Price volatility: +22% peak-to-trough for key minerals in 2024

- Mitigation: diversify suppliers, long-term contracts, strategic inventory

Supplier power high despite Fosun scale—supply concentration, switching costs risk COGS

Suppliers hold moderate-to-high power: 70–80% of laser sub-assemblies from <10 vendors (2025), China supplied ~65% of rare earths (2024), and device gross margin ~48% (2024), so disruptions raise COGS risk. Fosun scale (RMB 120.4bn revenue, 2024) cuts supplier power; long-term contracts cover 60–80% of critical spend, while switching costs (6–18 months, $0.5–$3M) maintain supplier leverage.

| Metric | Value |

|---|---|

| Laser vendors concentration | 70–80% from <10 |

| Rare earths supply (China) | ~65% (2024) |

| Device gross margin | ~48% (2024) |

| Fosun Pharma revenue | RMB 120.4bn (2024) |

| Switching cost | 6–18m; $0.5–$3M |

| Long-term contract coverage | 60–80% |

What is included in the product

Tailored Five Forces analysis for Sisram Medical that uncovers competitive intensity, buyer/supplier power, threat of entrants and substitutes, and identifies disruptive trends and entry barriers affecting its profitability.

Concise Porter's Five Forces snapshot for Sisram Medical—quickly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

High switching costs for practitioners

Medical practices invest heavily in Sisram’s platforms—Soprano or Harmony—often spending $50k–$200k per device and 40–80 training hours per staff member, creating high switching costs. Once integrated, clinics face downtime, retraining, and capital write-offs, so switching to competitors is rarely economical. This lock-in lowers customer bargaining power and lets Sisram keep stable consumable margins (20–35% gross) and service fees. What this hides: small clinics still push back on bulk pricing.

Brand recognition and patient demand

Alma brand recognition drives patient demand: surveys show 48% of aesthetic patients in 2024 requested specific device brands, with Alma among the top three, pushing clinics to stock Sisram technology to stay competitive.

Because patients often choose treatments, clinics have reduced bargaining power; Sisram reported 2024 device revenues up 22%, indicating pricing resilience despite buyer concentration.

Fragmentation of the global clinic market

The majority of Sisram Medical’s customers are independent med spas, dermatologists, and small plastic surgery practices; this fragmentation means single buyers rarely exceed 1–2% of Sisram’s revenue, so they lack volume leverage to force discounts.

Large corporate aesthetic groups grew ~18% CAGR 2019–2024 but still account for under 20% of global clinic revenues, keeping pricing power with manufacturers like Sisram.

Essential nature of after-sales support

Customers depend on Sisram for technical support, software updates, and proprietary consumables, creating high switching costs; in 2024 Sisram’s service revenue made up ~28% of medical segment sales, reinforcing recurring dependence.

This ongoing service tie shifts bargaining power to Sisram because clinics risk costly downtime—average device downtime loss ~USD 2,400/day for aesthetic clinics—so they keep using certified parts and service.

- Service revenue ~28% of medical sales (2024)

- Avg downtime cost ~USD 2,400/day

- Certification required for warranty and compliance

Access to financing and leasing models

By 2025 Sisram Medical expanded flexible financing and leasing, cutting upfront costs and boosting device adoption by ~35% versus 2022, widening the practitioner pool but lowering buyer bargaining as clinics tie to Sisram’s contract terms.

Leases commonly run 36–60 months and include service agreements that lock in maintenance revenue (estimated 20–30% of contract value), increasing vendor dependence and reducing customer exit options.

- Adoption +35% vs 2022

- Typical lease 36–60 months

- Service revenue 20–30% of contracts

- Higher switching costs, lower buyer power

Sisram’s pricing power: high capex, costly downtime & recurring 20–35% consumable margins

Sisram faces low customer bargaining power: high device capex (USD 50k–200k), 40–80 training hours, service revenue ~28% of medical sales (2024), leases (36–60 months) boosted adoption +35% vs 2022, and avg downtime cost ~USD 2,400/day—so clinics accept premiums and recurring consumable margins (20–35%).

| Metric | Value (2024/2025) |

|---|---|

| Device price | USD 50k–200k |

| Training | 40–80 hours |

| Service rev | ~28% medical sales |

| Adoption vs 2022 | +35% |

| Lease term | 36–60 months |

| Downtime cost | ~USD 2,400/day |

| Consumable margin | 20–35% |

Preview the Actual Deliverable

Sisram Medical Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sisram Medical you'll receive upon purchase—no placeholders or mockups; the full, professionally formatted document is ready for immediate download and use.