SiteMinder Porter's Five Forces Analysis

Don't Miss the Bigger Picture

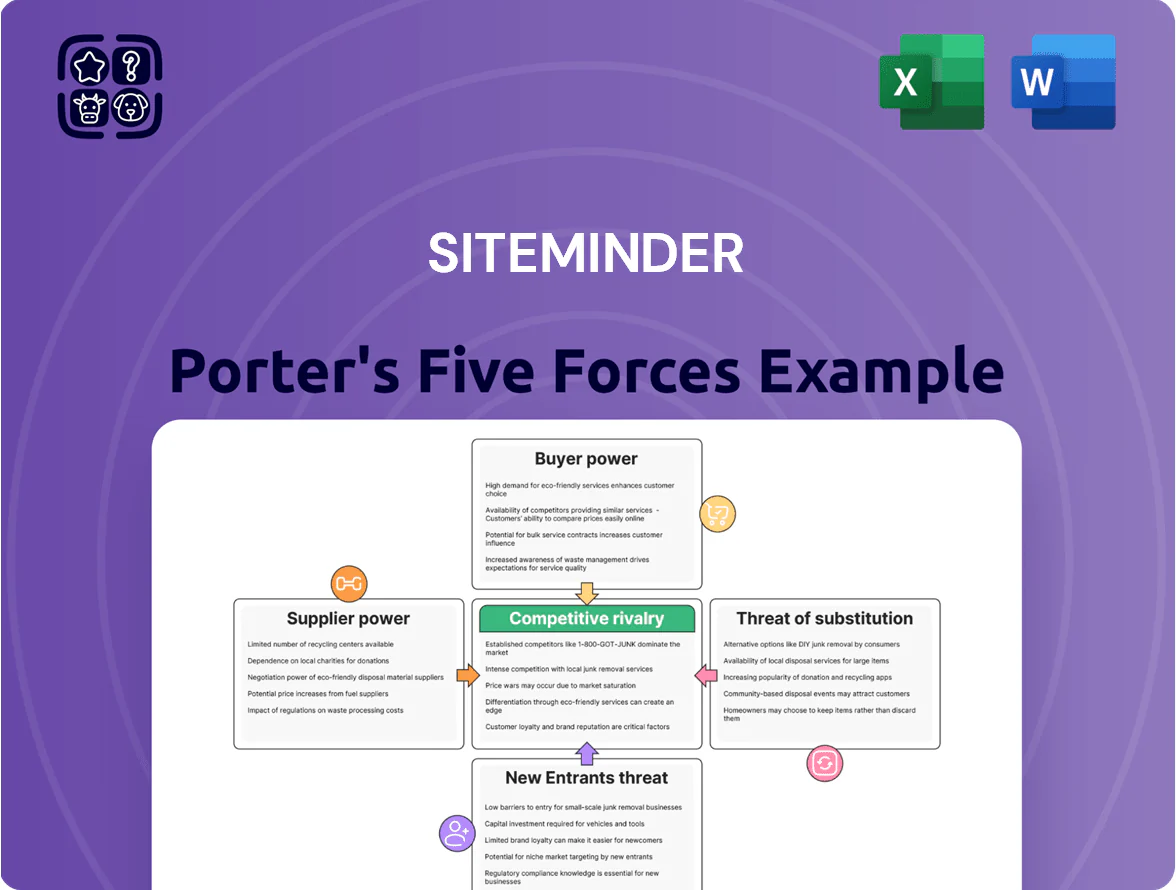

SiteMinder faces intense rivalry from large channel managers and PMS providers, moderate buyer power as hotels seek integrated solutions, and manageable supplier power given scalable cloud infrastructure; threats from new entrants and substitutes hinge on distribution shifts and direct bookings trends. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SiteMinder’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

SiteMinder depends on AWS and Google Cloud for its global platform; together AWS (34% cloud IaaS market share in 2024) and Google Cloud (12%) limit SiteMinder’s pricing leverage, raising supplier power. Standardized APIs and container tech make migration possible—Shop around: rehosting could cut costs by ~10–25% but requires months and multi-million-dollar engineering effort for a platform of SiteMinder’s scale (~100k hotels connected).

Global Distribution Systems and OTAs

Online Travel Agencies (OTAs) and Global Distribution Systems (GDS) supply inventory reach and connectivity; Booking Holdings and Expedia Group together controlled ~70% of global OTA gross bookings in 2023, giving them leverage over API standards and fee terms.

SiteMinder streamlines hotel integrations to these platforms, but must sustain partner agreements and technical compliance or face reduced distribution for its 35,000+ hotel customers and lower ARR growth.

Specialized Software Developers

The global market for cloud-SaaS engineers grew 12% in 2024, tightening supply; SiteMinder depends on these specialists to run its booking platform and launch features, so turnover hurts R&D velocity and revenue cadence.

High demand gives developers bargaining power: in 2024 median senior cloud engineer pay rose to about US$150k–180k in key markets, pushing SiteMinder to compete on pay, equity, and remote policies to retain talent.

Payment Gateway Providers

SiteMinder integrates with third-party payment processors to run its booking engine; these banks and fintechs wield leverage via regulatory compliance demands and set transaction fees SiteMinder largely must accept, pushing margins. In 2024 global card-processing fees averaged 1.3–2.5% per transaction and chargeback rates rose to ~0.7%, so fee hikes or service disruptions immediately raise costs and customer prices.

- Integrations create dependency on processors

- Avg fees 1.3–2.5% (2024)

- Chargeback ~0.7% (2024)

- Regulatory shifts can force rapid changes

Data and Analytics Providers

SiteMinder uses external feeds for market intelligence and local insights, and suppliers of niche hospitality data gain leverage when their datasets are unique and critical to booking-rate or pricing features.

High-quality, real-time data costs remain a steady operating expense—enterprise data subscriptions can run $200k–$1.2M annually for comparable SaaS platforms in 2024, pressuring margins.

Loss of a key data provider would raise switching costs and time-to-market, giving suppliers bargaining power over price and delivery.

- Unique data = high supplier power

- Real-time feeds cost $200k–$1.2M/yr

- Switching raises time-to-market

Suppliers wield outsized leverage—cloud, OTAs, payments, talent and data drive costs

Suppliers (cloud IaaS, OTAs/GDS, payments, data, talent) hold meaningful leverage: AWS 34%/Google 12% IaaS (2024), Booking+Expedia ~70% OTA bookings (2023), card fees 1.3–2.5% (2024), chargebacks ~0.7% (2024), senior cloud pay US$150–180k (2024), data feeds US$200k–1.2M/yr—switching costs and compliance raise SiteMinder’s supplier power.

| Supplier | Key metric |

|---|---|

| Cloud IaaS | AWS 34% / GCP 12% (2024) |

| OTAs/GDS | Booking+Expedia ~70% (2023) |

| Payments | Fees 1.3–2.5%; chargebacks 0.7% (2024) |

| Talent | Senior cloud pay US$150–180k (2024) |

| Data | Feeds US$200k–1.2M/yr (2024) |

What is included in the product

Concise Porter's Five Forces assessment for SiteMinder, highlighting competitive intensity, customer and supplier bargaining power, entry barriers, and substitution risks with targeted strategic implications.

A concise Porter’s Five Forces one-sheet tailored to SiteMinder—quickly assess competitive pressure and prioritize strategies to protect pricing and distribution.

Customers Bargaining Power

Fragmented Hotel Market

The majority of SiteMinder’s customers are small-to-medium independent hotels and boutique chains, which made up roughly 72% of its hotel customers as of FY2024; no single client accounted for more than 0.5% of revenue, limiting individual negotiating clout. This fragmentation lowers customers’ bargaining power, letting SiteMinder maintain relatively stable subscription pricing across the segment—average ARPU (average revenue per user) rose 6% in 2024. As a result, price concessions are uncommon, and churn effects are diluted across a large base of ~35,000 properties.

High Switching Costs

Once a hotel links SiteMinder to its PMS and 400+ distribution channels, switching rivals is complex and risky: hotels report 12–18% booking downtime in migrations and average retraining costs of US$3,200 per property, creating a sticky ecosystem; potential data loss and integration rewrites raise project costs by 20–40%, so this technical lock-in cuts customers’ bargaining power sharply.

Value Proposition and ROI

Hotels depend more on digital distribution to hit occupancy; global OTAs drove 45% of bookings in 2024 and direct channel tech reduced commission leakage by ~10%. SiteMinder shows clients average 12–18% booking growth and a 30–40% cut in manual channel management time, so hotels treat its platform as essential. That shifts bargaining power toward SiteMinder, since hoteliers often pay for performance over marginal price savings.

Availability of Alternative Platforms

While switching platforms is operationally hard, buyers have real choices: over 200 channel managers and 400+ property management systems (PMS) in the market as of 2025, so many hotels compare options before purchase.

Larger groups leverage scale to negotiate enterprise deals; SiteMinder faces pressure to offer bespoke SLAs and volume discounts to win contracts.

This competitive landscape forces SiteMinder to stay price-competitive and rapidly add features; SiteMinder reported 2024 revenue of AUD 114m, so customer acquisition matters for growth.

- 200+ channel managers available (2025)

- 400+ PMS options (2025)

- SiteMinder 2024 revenue AUD 114m

- Large chains negotiate bespoke/volume pricing

Price Sensitivity in Hospitality

The hospitality sector works on thin margins—global average hotel profit margins ran about 10% in 2024—so customers are highly price-sensitive to subscription hikes, since a 5–10% fee rise can push properties into loss.

Individual buyer power is low, but collective sentiment or a 2025 downturn (IMF growth forecasts cut by 0.3pp) could force SiteMinder to cut prices or add flexible tiers.

Hotels compare subscription costs to commission savings: direct-booking lift of 5–12% (industry studies 2023–24) often underpins ROI for channel manager spend.

- Thin margins: ~10% hotel profit (2024)

- Price sensitivity: 5–10% fee impact

- Downdturn risk: IMF 2025 growth cuts

- Direct-booking lift: 5–12% ROI

SME-heavy base boosts stickiness via ROI and lock-in, but fierce market choice pressures pricing

Customers mostly SMEs (~72% of SiteMinder’s base in FY2024) so individual power is low; no client >0.5% revenue. Technical lock-in (12–18% migration downtime; ~US$3,200 retrain cost) and measurable ROI (12–18% booking lift; direct-booking +5–12%) raise stickiness, but 200+ channel managers and 400+ PMS options (2025) plus large-chain volume bargaining keep pressure on price.

| Metric | Value |

|---|---|

| SME share (FY2024) | 72% |

| SiteMinder rev (2024) | AUD 114m |

| Migration downtime | 12–18% |

| Retrain cost | US$3,200 |

| Booking lift | 12–18% |

| Market choices (2025) | 200+ channel mgrs, 400+ PMS |

Preview Before You Purchase

SiteMinder Porter's Five Forces Analysis

This preview shows the exact SiteMinder Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the complete, professionally formatted file you'll be able to download and use the moment you buy, with the full assessment and insights ready for application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

SiteMinder faces intense rivalry from large channel managers and PMS providers, moderate buyer power as hotels seek integrated solutions, and manageable supplier power given scalable cloud infrastructure; threats from new entrants and substitutes hinge on distribution shifts and direct bookings trends. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SiteMinder’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

SiteMinder depends on AWS and Google Cloud for its global platform; together AWS (34% cloud IaaS market share in 2024) and Google Cloud (12%) limit SiteMinder’s pricing leverage, raising supplier power. Standardized APIs and container tech make migration possible—Shop around: rehosting could cut costs by ~10–25% but requires months and multi-million-dollar engineering effort for a platform of SiteMinder’s scale (~100k hotels connected).

Global Distribution Systems and OTAs

Online Travel Agencies (OTAs) and Global Distribution Systems (GDS) supply inventory reach and connectivity; Booking Holdings and Expedia Group together controlled ~70% of global OTA gross bookings in 2023, giving them leverage over API standards and fee terms.

SiteMinder streamlines hotel integrations to these platforms, but must sustain partner agreements and technical compliance or face reduced distribution for its 35,000+ hotel customers and lower ARR growth.

Specialized Software Developers

The global market for cloud-SaaS engineers grew 12% in 2024, tightening supply; SiteMinder depends on these specialists to run its booking platform and launch features, so turnover hurts R&D velocity and revenue cadence.

High demand gives developers bargaining power: in 2024 median senior cloud engineer pay rose to about US$150k–180k in key markets, pushing SiteMinder to compete on pay, equity, and remote policies to retain talent.

Payment Gateway Providers

SiteMinder integrates with third-party payment processors to run its booking engine; these banks and fintechs wield leverage via regulatory compliance demands and set transaction fees SiteMinder largely must accept, pushing margins. In 2024 global card-processing fees averaged 1.3–2.5% per transaction and chargeback rates rose to ~0.7%, so fee hikes or service disruptions immediately raise costs and customer prices.

- Integrations create dependency on processors

- Avg fees 1.3–2.5% (2024)

- Chargeback ~0.7% (2024)

- Regulatory shifts can force rapid changes

Data and Analytics Providers

SiteMinder uses external feeds for market intelligence and local insights, and suppliers of niche hospitality data gain leverage when their datasets are unique and critical to booking-rate or pricing features.

High-quality, real-time data costs remain a steady operating expense—enterprise data subscriptions can run $200k–$1.2M annually for comparable SaaS platforms in 2024, pressuring margins.

Loss of a key data provider would raise switching costs and time-to-market, giving suppliers bargaining power over price and delivery.

- Unique data = high supplier power

- Real-time feeds cost $200k–$1.2M/yr

- Switching raises time-to-market

Suppliers wield outsized leverage—cloud, OTAs, payments, talent and data drive costs

Suppliers (cloud IaaS, OTAs/GDS, payments, data, talent) hold meaningful leverage: AWS 34%/Google 12% IaaS (2024), Booking+Expedia ~70% OTA bookings (2023), card fees 1.3–2.5% (2024), chargebacks ~0.7% (2024), senior cloud pay US$150–180k (2024), data feeds US$200k–1.2M/yr—switching costs and compliance raise SiteMinder’s supplier power.

| Supplier | Key metric |

|---|---|

| Cloud IaaS | AWS 34% / GCP 12% (2024) |

| OTAs/GDS | Booking+Expedia ~70% (2023) |

| Payments | Fees 1.3–2.5%; chargebacks 0.7% (2024) |

| Talent | Senior cloud pay US$150–180k (2024) |

| Data | Feeds US$200k–1.2M/yr (2024) |

What is included in the product

Concise Porter's Five Forces assessment for SiteMinder, highlighting competitive intensity, customer and supplier bargaining power, entry barriers, and substitution risks with targeted strategic implications.

A concise Porter’s Five Forces one-sheet tailored to SiteMinder—quickly assess competitive pressure and prioritize strategies to protect pricing and distribution.

Customers Bargaining Power

Fragmented Hotel Market

The majority of SiteMinder’s customers are small-to-medium independent hotels and boutique chains, which made up roughly 72% of its hotel customers as of FY2024; no single client accounted for more than 0.5% of revenue, limiting individual negotiating clout. This fragmentation lowers customers’ bargaining power, letting SiteMinder maintain relatively stable subscription pricing across the segment—average ARPU (average revenue per user) rose 6% in 2024. As a result, price concessions are uncommon, and churn effects are diluted across a large base of ~35,000 properties.

High Switching Costs

Once a hotel links SiteMinder to its PMS and 400+ distribution channels, switching rivals is complex and risky: hotels report 12–18% booking downtime in migrations and average retraining costs of US$3,200 per property, creating a sticky ecosystem; potential data loss and integration rewrites raise project costs by 20–40%, so this technical lock-in cuts customers’ bargaining power sharply.

Value Proposition and ROI

Hotels depend more on digital distribution to hit occupancy; global OTAs drove 45% of bookings in 2024 and direct channel tech reduced commission leakage by ~10%. SiteMinder shows clients average 12–18% booking growth and a 30–40% cut in manual channel management time, so hotels treat its platform as essential. That shifts bargaining power toward SiteMinder, since hoteliers often pay for performance over marginal price savings.

Availability of Alternative Platforms

While switching platforms is operationally hard, buyers have real choices: over 200 channel managers and 400+ property management systems (PMS) in the market as of 2025, so many hotels compare options before purchase.

Larger groups leverage scale to negotiate enterprise deals; SiteMinder faces pressure to offer bespoke SLAs and volume discounts to win contracts.

This competitive landscape forces SiteMinder to stay price-competitive and rapidly add features; SiteMinder reported 2024 revenue of AUD 114m, so customer acquisition matters for growth.

- 200+ channel managers available (2025)

- 400+ PMS options (2025)

- SiteMinder 2024 revenue AUD 114m

- Large chains negotiate bespoke/volume pricing

Price Sensitivity in Hospitality

The hospitality sector works on thin margins—global average hotel profit margins ran about 10% in 2024—so customers are highly price-sensitive to subscription hikes, since a 5–10% fee rise can push properties into loss.

Individual buyer power is low, but collective sentiment or a 2025 downturn (IMF growth forecasts cut by 0.3pp) could force SiteMinder to cut prices or add flexible tiers.

Hotels compare subscription costs to commission savings: direct-booking lift of 5–12% (industry studies 2023–24) often underpins ROI for channel manager spend.

- Thin margins: ~10% hotel profit (2024)

- Price sensitivity: 5–10% fee impact

- Downdturn risk: IMF 2025 growth cuts

- Direct-booking lift: 5–12% ROI

SME-heavy base boosts stickiness via ROI and lock-in, but fierce market choice pressures pricing

Customers mostly SMEs (~72% of SiteMinder’s base in FY2024) so individual power is low; no client >0.5% revenue. Technical lock-in (12–18% migration downtime; ~US$3,200 retrain cost) and measurable ROI (12–18% booking lift; direct-booking +5–12%) raise stickiness, but 200+ channel managers and 400+ PMS options (2025) plus large-chain volume bargaining keep pressure on price.

| Metric | Value |

|---|---|

| SME share (FY2024) | 72% |

| SiteMinder rev (2024) | AUD 114m |

| Migration downtime | 12–18% |

| Retrain cost | US$3,200 |

| Booking lift | 12–18% |

| Market choices (2025) | 200+ channel mgrs, 400+ PMS |

Preview Before You Purchase

SiteMinder Porter's Five Forces Analysis

This preview shows the exact SiteMinder Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the complete, professionally formatted file you'll be able to download and use the moment you buy, with the full assessment and insights ready for application.