SJM Holdings PESTLE Analysis

Your Shortcut to Market Insight Starts Here

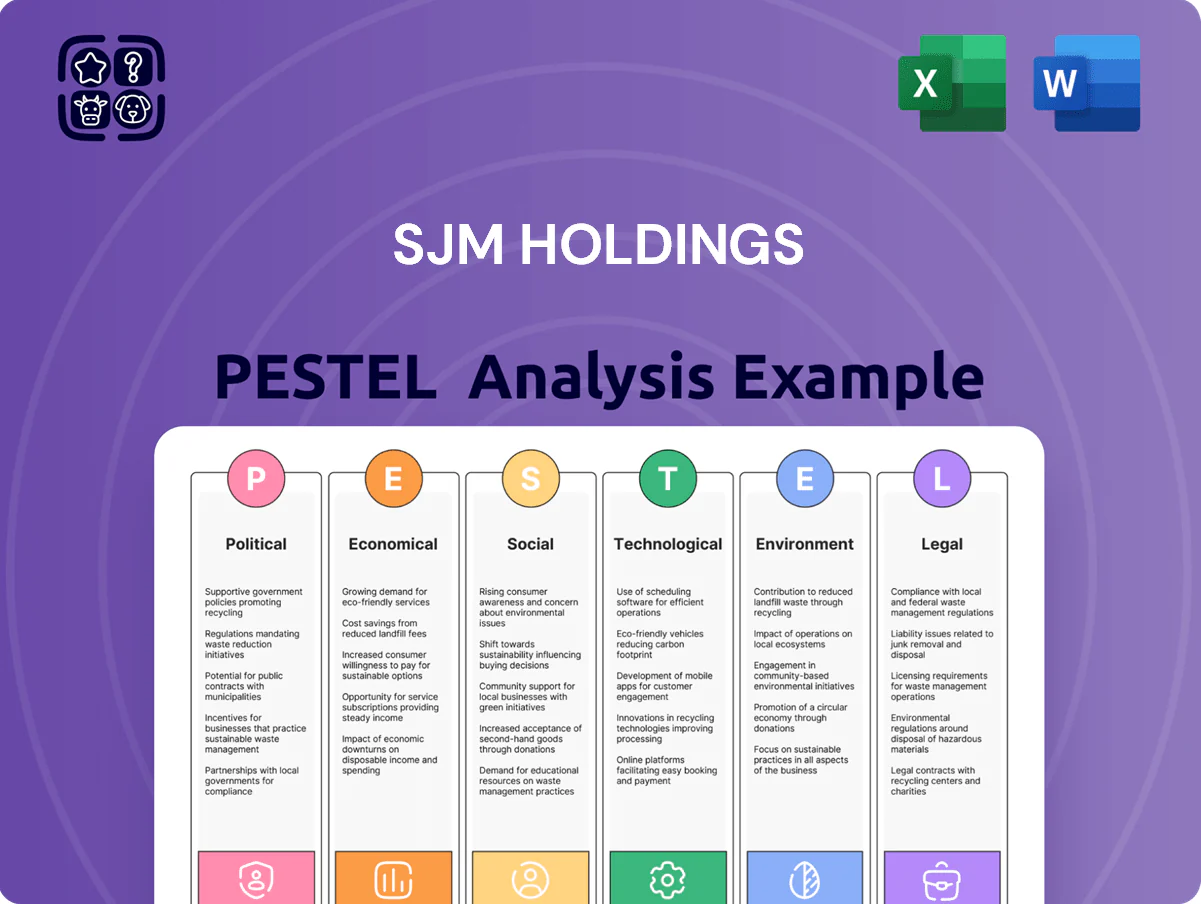

Understand how regulatory shifts, tourism trends, and technological adoption are reshaping SJM Holdings’ growth prospects—our concise PESTLE highlights the external forces that matter most to investors and strategists. Purchase the full analysis for a detailed, ready-to-use report with actionable insights to inform investment decisions and strategic planning.

Political factors

Macau Government Concession Oversight

SJM Holdings operates under a ten-year Macau gaming concession that began in 2023 and remains a key political anchor through 2025; regulators require strict adherence to milestones and investment commitments—SJM pledged HKD 36 billion in capital works and diversification projects as part of its concession terms. The government’s oversight ties license security to meeting redevelopment timelines and local job targets, forcing SJM to align with Macau’s push for economic stability and reduced reliance on pure gaming revenue.

Beijing Central Government Influence

Beijing’s visa controls and anti-corruption drives dictate Macau capital and visitor flows; Macau visitation fell 28% y/y in 2023 and VIP turnover remained volatile, pressuring SJM’s revenue mix.

By late 2025 Beijing’s national security and financial-integrity emphasis tightened compliance costs—Macau gaming operator fines and compliance spending rose; SJM reported higher regulatory provisioning in 2024–25.

Mainland policy shifts on cross-border gambling enforcement directly hit VIP and premium-mass income—VIP rolling chip volumes contracted materially, reducing SJM’s high-margin segment exposure.

Geopolitical Tensions and Trade Relations

Ongoing China-West tensions, especially with the US, create headwinds for Macau’s gaming industry; SJM Holdings, with 2024 revenue around MOP 20.3 billion, faces heightened investor risk premia and volatile ADR flows tied to geopolitical sentiment.

Escalations can prompt travel restrictions—China outbound tourist growth slowed to 12% in 2024 vs pre-COVID levels—which would hit SJM’s VIP and mass segments given Macau’s 2024 visitor arrivals of 23.4 million.

Capital controls or sanctions could reduce international liquidity and deter cross-border investment into Macau gaming, pressuring SJM’s access to overseas funding and impacting its ability to refinance maturing debt.

Greater Bay Area Integration Policy

The Chinese government’s Greater Bay Area integration is a core political driver shaping SJM’s long-term planning, with Beijing allocating over CNY 1.2 trillion to GBA infrastructure projects through 2025 to boost connectivity among Macau, Hong Kong and Guangdong.

Policies improving cross-border transport—Hong Kong–Zhuhai–Macau Bridge handling 6.5 million vehicles since 2018 and planned high-speed links—support SJM’s need to position Grand Lisboa Palace to capture rising intra-GBA visitor flows.

- SJM must align capital expenditure with GBA timelines

- Target uplift: incremental visitor growth 5–8% annually from regional integration

- Opportunity: higher mass-market footfall and cross-border MICE demand

Public Policy on Economic Diversification

The Macau government under its 1+4 strategy has pressured operators to boost non-gaming revenue; SJM must raise leisure, MICE and cultural investment—SJM reported non-gaming revenue at about 11% of total in 2023, below peers averaging ~25% (2023 HK filings).

Regulators expect heavy capex: SJM’s 2024–25 redevelopment and MICE commitments could exceed HKD 10+ billion to comply; shortfalls risk political friction and negative mid-term concession reviews.

- SJM non-gaming revenue ~11% (2023)

- Peer non-gaming average ~25% (2023)

- Estimated required capex HKD 10+ billion (2024–25)

- Failure risks: political friction, adverse concession review

SJM tied to HKD36bn concession, MOP20.3bn revenue; non-gaming lags peers

Macau concession (2023–33) ties SJM to HKD 36bn commitments; 2024 revenue MOP 20.3bn, visitors 23.4m (2024). VIP volatility: 2023 visitation -28% y/y; non-gaming 11% (2023) vs peers 25%. GBA funding CNY 1.2tn to 2025; estimated capex HKD 10+bn (2024–25); rising compliance costs increased provisions in 2024–25.

| Metric | Value |

|---|---|

| 2024 revenue | MOP 20.3bn |

| Visitors (2024) | 23.4m |

| Non-gaming (SJM 2023) | 11% |

| Peer non-gaming (2023) | ~25% |

| Concession commits | HKD 36bn |

| Est capex (2024–25) | HKD 10+bn |

What is included in the product

Explores how macro-environmental forces uniquely affect SJM Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory data to identify risks and opportunities.

A concise, visually segmented PESTLE summary for SJM Holdings that streamlines stakeholder briefings and can be dropped into presentations or planning packs for quick alignment across teams.

Economic factors

Post-Pandemic Consumption Trends

By end-2025 Macau GDP recovered to about 95% of 2019 levels and tourist arrivals reached ~22 million (2024), yet spend-per-visitor declined as the average spender shifted to value-driven purchasing; SJM must adjust offerings and pricing to capture lower-yield volume. The VIP segment remains structurally smaller—VIP gaming revenue fell to ~18% of Macau gross gaming revenue in 2024 vs ~40% pre-2014—raising reliance on mass market and non-gaming. SJM’s topline now tracks Chinese middle-class discretionary income and domestic consumption trends, with household consumption contributing over 50% of China GDP in 2024, making local demand sensitivity critical to forecasts.

Interest Rate Environment and Debt Servicing

The global rise in benchmark rates—US Fed funds at 5.25–5.50% in 2024 and Hong Kong/HKMA tracking higher rates—raises SJM Holdings’ cost of capital, pressuring servicing of its reported HKD 24.8 billion net debt (FY2023). Following heavy CapEx for Grand Lisboa Palace, SJM is focused on deleveraging; a 100–200bp uptick in borrowing costs would materially widen interest expense and compress EBITDA margins. Elevated rates could constrain free cash flow for further property upgrades and limit dividend capacity, making liquidity management and refinancing terms critical.

Inflationary Pressures on Operational Costs

Rising labor, energy and import costs are squeezing SJM’s resort margins; Macau wage inflation in hospitality rose about 6–8% YoY in 2024 amid specialist staff shortages, while electricity tariffs increased c.5% and fuel import prices added further input costs.

Currency Fluctuations and Capital Controls

The Macau pataca is pegged to the Hong Kong dollar, linking SJM’s pricing exposure to HKD-CNY movements; in 2024 the yuan weakened ~3.5% vs USD, increasing travel costs for mainland gamblers paying in CNY and lowering discretionary visits.

China’s capital controls persist—Q1 2025 outbound direct investment fell 12% YoY—constraining high-roller liquidity and limiting SJM’s addressable VIP market.

- Pataca-HKD peg ties Macau pricing to HKD-CNY FX shifts

- 2024 CNY ~3.5% weaker vs USD raised travel costs

- Q1 2025 outbound investment down 12% YoY, tightening VIP liquidity

Regional Competition in Southeast Asia

SJM faces rising competition as Japan, Thailand and the Philippines expand integrated resorts; Japan reported ¥1.3 trillion in IR-related investment approvals by 2024 and Thailand hosted over 40 new large-scale tourism projects in 2023–24, diverting high-value players from Macau.

These jurisdictions target the same regional tourists and premium mass segments that generated Macau gross gaming revenue of MOP 136.4 billion in 2023, so SJM must sharpen pricing, loyalty and non-gaming amenities to preserve market share.

- Japan ¥1.3 trillion IR approvals (2024)

- Macau GGR MOP 136.4 billion (2023)

- Thailand 40+ large tourism projects (2023–24)

- Need: differentiated pricing, loyalty, non-gaming amenities

Macau rebounds toward 2019 GDP, tourism up but VIPs, spending, and debt pose risks

Macau GDP ~95% of 2019 by end-2025; 2024 tourist arrivals ~22m but spend-per-visitor down; VIP share ~18% of GGR (2024) vs ~40% pre-2014, increasing reliance on mass/non-gaming; SJM net debt HKD 24.8bn (FY2023) with rates 5.25–5.50% (US Fed 2024) raising borrowing costs; CNY ~3.5% weaker vs USD (2024), Q1 2025 outbound investment -12% YoY.

| Metric | Value |

|---|---|

| Macau GDP (vs 2019) | ~95% (end-2025) |

| Tourist arrivals | ~22m (2024) |

| VIP share of GGR | ~18% (2024) |

| SJM net debt | HKD 24.8bn (FY2023) |

| Fed funds | 5.25–5.50% (2024) |

| CNY vs USD | -3.5% (2024) |

| Outbound investment Q1 | -12% YoY (Q1 2025) |

Same Document Delivered

SJM Holdings PESTLE Analysis

The preview shown here is the exact SJM Holdings PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure displayed match the final file available for immediate download, with no placeholders or edits required.

What you see is the finished, professionally structured analysis you’ll own after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Understand how regulatory shifts, tourism trends, and technological adoption are reshaping SJM Holdings’ growth prospects—our concise PESTLE highlights the external forces that matter most to investors and strategists. Purchase the full analysis for a detailed, ready-to-use report with actionable insights to inform investment decisions and strategic planning.

Political factors

Macau Government Concession Oversight

SJM Holdings operates under a ten-year Macau gaming concession that began in 2023 and remains a key political anchor through 2025; regulators require strict adherence to milestones and investment commitments—SJM pledged HKD 36 billion in capital works and diversification projects as part of its concession terms. The government’s oversight ties license security to meeting redevelopment timelines and local job targets, forcing SJM to align with Macau’s push for economic stability and reduced reliance on pure gaming revenue.

Beijing Central Government Influence

Beijing’s visa controls and anti-corruption drives dictate Macau capital and visitor flows; Macau visitation fell 28% y/y in 2023 and VIP turnover remained volatile, pressuring SJM’s revenue mix.

By late 2025 Beijing’s national security and financial-integrity emphasis tightened compliance costs—Macau gaming operator fines and compliance spending rose; SJM reported higher regulatory provisioning in 2024–25.

Mainland policy shifts on cross-border gambling enforcement directly hit VIP and premium-mass income—VIP rolling chip volumes contracted materially, reducing SJM’s high-margin segment exposure.

Geopolitical Tensions and Trade Relations

Ongoing China-West tensions, especially with the US, create headwinds for Macau’s gaming industry; SJM Holdings, with 2024 revenue around MOP 20.3 billion, faces heightened investor risk premia and volatile ADR flows tied to geopolitical sentiment.

Escalations can prompt travel restrictions—China outbound tourist growth slowed to 12% in 2024 vs pre-COVID levels—which would hit SJM’s VIP and mass segments given Macau’s 2024 visitor arrivals of 23.4 million.

Capital controls or sanctions could reduce international liquidity and deter cross-border investment into Macau gaming, pressuring SJM’s access to overseas funding and impacting its ability to refinance maturing debt.

Greater Bay Area Integration Policy

The Chinese government’s Greater Bay Area integration is a core political driver shaping SJM’s long-term planning, with Beijing allocating over CNY 1.2 trillion to GBA infrastructure projects through 2025 to boost connectivity among Macau, Hong Kong and Guangdong.

Policies improving cross-border transport—Hong Kong–Zhuhai–Macau Bridge handling 6.5 million vehicles since 2018 and planned high-speed links—support SJM’s need to position Grand Lisboa Palace to capture rising intra-GBA visitor flows.

- SJM must align capital expenditure with GBA timelines

- Target uplift: incremental visitor growth 5–8% annually from regional integration

- Opportunity: higher mass-market footfall and cross-border MICE demand

Public Policy on Economic Diversification

The Macau government under its 1+4 strategy has pressured operators to boost non-gaming revenue; SJM must raise leisure, MICE and cultural investment—SJM reported non-gaming revenue at about 11% of total in 2023, below peers averaging ~25% (2023 HK filings).

Regulators expect heavy capex: SJM’s 2024–25 redevelopment and MICE commitments could exceed HKD 10+ billion to comply; shortfalls risk political friction and negative mid-term concession reviews.

- SJM non-gaming revenue ~11% (2023)

- Peer non-gaming average ~25% (2023)

- Estimated required capex HKD 10+ billion (2024–25)

- Failure risks: political friction, adverse concession review

SJM tied to HKD36bn concession, MOP20.3bn revenue; non-gaming lags peers

Macau concession (2023–33) ties SJM to HKD 36bn commitments; 2024 revenue MOP 20.3bn, visitors 23.4m (2024). VIP volatility: 2023 visitation -28% y/y; non-gaming 11% (2023) vs peers 25%. GBA funding CNY 1.2tn to 2025; estimated capex HKD 10+bn (2024–25); rising compliance costs increased provisions in 2024–25.

| Metric | Value |

|---|---|

| 2024 revenue | MOP 20.3bn |

| Visitors (2024) | 23.4m |

| Non-gaming (SJM 2023) | 11% |

| Peer non-gaming (2023) | ~25% |

| Concession commits | HKD 36bn |

| Est capex (2024–25) | HKD 10+bn |

What is included in the product

Explores how macro-environmental forces uniquely affect SJM Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory data to identify risks and opportunities.

A concise, visually segmented PESTLE summary for SJM Holdings that streamlines stakeholder briefings and can be dropped into presentations or planning packs for quick alignment across teams.

Economic factors

Post-Pandemic Consumption Trends

By end-2025 Macau GDP recovered to about 95% of 2019 levels and tourist arrivals reached ~22 million (2024), yet spend-per-visitor declined as the average spender shifted to value-driven purchasing; SJM must adjust offerings and pricing to capture lower-yield volume. The VIP segment remains structurally smaller—VIP gaming revenue fell to ~18% of Macau gross gaming revenue in 2024 vs ~40% pre-2014—raising reliance on mass market and non-gaming. SJM’s topline now tracks Chinese middle-class discretionary income and domestic consumption trends, with household consumption contributing over 50% of China GDP in 2024, making local demand sensitivity critical to forecasts.

Interest Rate Environment and Debt Servicing

The global rise in benchmark rates—US Fed funds at 5.25–5.50% in 2024 and Hong Kong/HKMA tracking higher rates—raises SJM Holdings’ cost of capital, pressuring servicing of its reported HKD 24.8 billion net debt (FY2023). Following heavy CapEx for Grand Lisboa Palace, SJM is focused on deleveraging; a 100–200bp uptick in borrowing costs would materially widen interest expense and compress EBITDA margins. Elevated rates could constrain free cash flow for further property upgrades and limit dividend capacity, making liquidity management and refinancing terms critical.

Inflationary Pressures on Operational Costs

Rising labor, energy and import costs are squeezing SJM’s resort margins; Macau wage inflation in hospitality rose about 6–8% YoY in 2024 amid specialist staff shortages, while electricity tariffs increased c.5% and fuel import prices added further input costs.

Currency Fluctuations and Capital Controls

The Macau pataca is pegged to the Hong Kong dollar, linking SJM’s pricing exposure to HKD-CNY movements; in 2024 the yuan weakened ~3.5% vs USD, increasing travel costs for mainland gamblers paying in CNY and lowering discretionary visits.

China’s capital controls persist—Q1 2025 outbound direct investment fell 12% YoY—constraining high-roller liquidity and limiting SJM’s addressable VIP market.

- Pataca-HKD peg ties Macau pricing to HKD-CNY FX shifts

- 2024 CNY ~3.5% weaker vs USD raised travel costs

- Q1 2025 outbound investment down 12% YoY, tightening VIP liquidity

Regional Competition in Southeast Asia

SJM faces rising competition as Japan, Thailand and the Philippines expand integrated resorts; Japan reported ¥1.3 trillion in IR-related investment approvals by 2024 and Thailand hosted over 40 new large-scale tourism projects in 2023–24, diverting high-value players from Macau.

These jurisdictions target the same regional tourists and premium mass segments that generated Macau gross gaming revenue of MOP 136.4 billion in 2023, so SJM must sharpen pricing, loyalty and non-gaming amenities to preserve market share.

- Japan ¥1.3 trillion IR approvals (2024)

- Macau GGR MOP 136.4 billion (2023)

- Thailand 40+ large tourism projects (2023–24)

- Need: differentiated pricing, loyalty, non-gaming amenities

Macau rebounds toward 2019 GDP, tourism up but VIPs, spending, and debt pose risks

Macau GDP ~95% of 2019 by end-2025; 2024 tourist arrivals ~22m but spend-per-visitor down; VIP share ~18% of GGR (2024) vs ~40% pre-2014, increasing reliance on mass/non-gaming; SJM net debt HKD 24.8bn (FY2023) with rates 5.25–5.50% (US Fed 2024) raising borrowing costs; CNY ~3.5% weaker vs USD (2024), Q1 2025 outbound investment -12% YoY.

| Metric | Value |

|---|---|

| Macau GDP (vs 2019) | ~95% (end-2025) |

| Tourist arrivals | ~22m (2024) |

| VIP share of GGR | ~18% (2024) |

| SJM net debt | HKD 24.8bn (FY2023) |

| Fed funds | 5.25–5.50% (2024) |

| CNY vs USD | -3.5% (2024) |

| Outbound investment Q1 | -12% YoY (Q1 2025) |

Same Document Delivered

SJM Holdings PESTLE Analysis

The preview shown here is the exact SJM Holdings PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure displayed match the final file available for immediate download, with no placeholders or edits required.

What you see is the finished, professionally structured analysis you’ll own after checkout.