SK PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic trends, and technological innovation are reshaping SK’s strategic outlook with our concise PESTLE snapshot—designed to spark strategic thinking and spotlight risks and opportunities you can act on today; purchase the full PESTLE for a comprehensive, editable analysis and immediate insights tailored for investors, consultants, and executives.

Political factors

Geopolitical tensions and semiconductor trade restrictions

The US–China rivalry hits SK via SK Hynix; US export controls since 2022 and 2023 curbs on EUV-related gear and high-end AI chips constrain supply and sales—SK Hynix reported 2024 capex of KRW 9.2tn amid these limits.

SK must weigh China manufacturing (20–30% revenue exposure in memory markets) against US CHIPS Act incentives—US offers up to $39bn for fabs, influencing SK’s location, tax and subsidy strategy.

South Korean government industrial policy

The South Korean administration treats the K-Semiconductor Belt and green energy as national security priorities, pledging a 510 trillion won semiconductor+future tech fund through 2027 and green industry incentives; SK Inc. wins tax credits and R&D subsidies (e.g., Korea’s 2024 tax breaks for chipmakers, battery R&D grants covering up to 30% of project costs), making alignment with state strategy essential to secure long-term infrastructure and capital support.

Inter-Korean relations and regional stability

Fluctuations in the political climate on the Korean Peninsula remain a systemic risk for Seoul-based conglomerates; 2024 saw 18 major North-South incidents, contributing to a 12% spike in KOSPI volatility during flare-ups.

Any escalation in North Korean military posturing can trigger capital flight and compress SK Inc. valuations—SK holdings fell 6% intra-day during the Oct 2024 tensions.

Investors closely monitor developments: South Korea sovereign CDS widened from 40bps to 72bps in 2024, raising the market risk premium and borrowing costs for SK group firms.

Global energy security and supply chain diplomacy

As a major energy and chemicals player via SK Innovation, SK is exposed to shifts in global energy alliances; 2025 oil price volatility (Brent range $70–95/bbl) and OPEC+ quota changes can swing feedstock costs and refinery margins by several percentage points.

Political instability in the Middle East raises supply risk that can increase input costs—SK reported feedstock cost sensitivity affecting EBITDA margins by ~2–4% in 2024.

SK Inc. pursues resource diplomacy, securing diversified sources for battery metals and LNG; by 2025 it expanded supply agreements covering ~40% of projected battery raw-material needs.

- Exposure to Brent volatility $70–95/bbl (2025)

- Feedstock cost moves impacted EBITDA ~2–4% (2024)

- Supply agreements cover ~40% of battery raw-material needs (2025)

Corporate governance and Chaebol reform pressures

Domestic pressure to boost transparency and minority shareholder protections continues to shape SK Inc.; Korea’s Financial Services Commission proposals in 2024 aimed at tighter disclosure and fair trading affect holding-company oversight and could raise compliance costs by an estimated 2–4% of administrative expenses.

Ongoing legislative moves to reform Chaebol—targeting cross-shareholding and intra-group transactions—force SK to adjust internal deals and succession plans to avoid fines or forced asset divestitures.

Maintaining proactive governance (enhanced boards, independent directors; SK reported 40% independent directors in 2024) is essential to reduce regulatory scrutiny and restore investor confidence after recent activist interventions.

- 2024 FSC proposals tighten disclosure, affecting compliance costs (approx +2–4%)

- Chaebol reforms target cross-shareholdings and intra-group deals

- SK had ~40% independent directors in 2024; governance upgrades reduce scrutiny

US‑China tech clash, CHIPS incentives reshape SK capex; geopolitical risks tighten

US–China tech rivalry, export controls and CHIPS Act incentives reshape SK’s capex and location choices; 2024 SK Hynix capex KRW 9.2tn, US incentives up to $39bn. Domestic policy: 510tn won semiconductor+future tech fund to 2027, 2024 FSC proposals raise compliance ~2–4%. Geopolitical risks: 18 N‑S incidents in 2024, sovereign CDS widened 40→72bps; feedstock cost swing hit EBITDA ~2–4% (2024).

| Metric | 2024/25 |

|---|---|

| SK Hynix capex | KRW 9.2tn (2024) |

| US CHIPS | Up to $39bn |

| K‑tech fund | KRW 510tn to 2027 |

| Sov CDS | 40→72bps (2024) |

What is included in the product

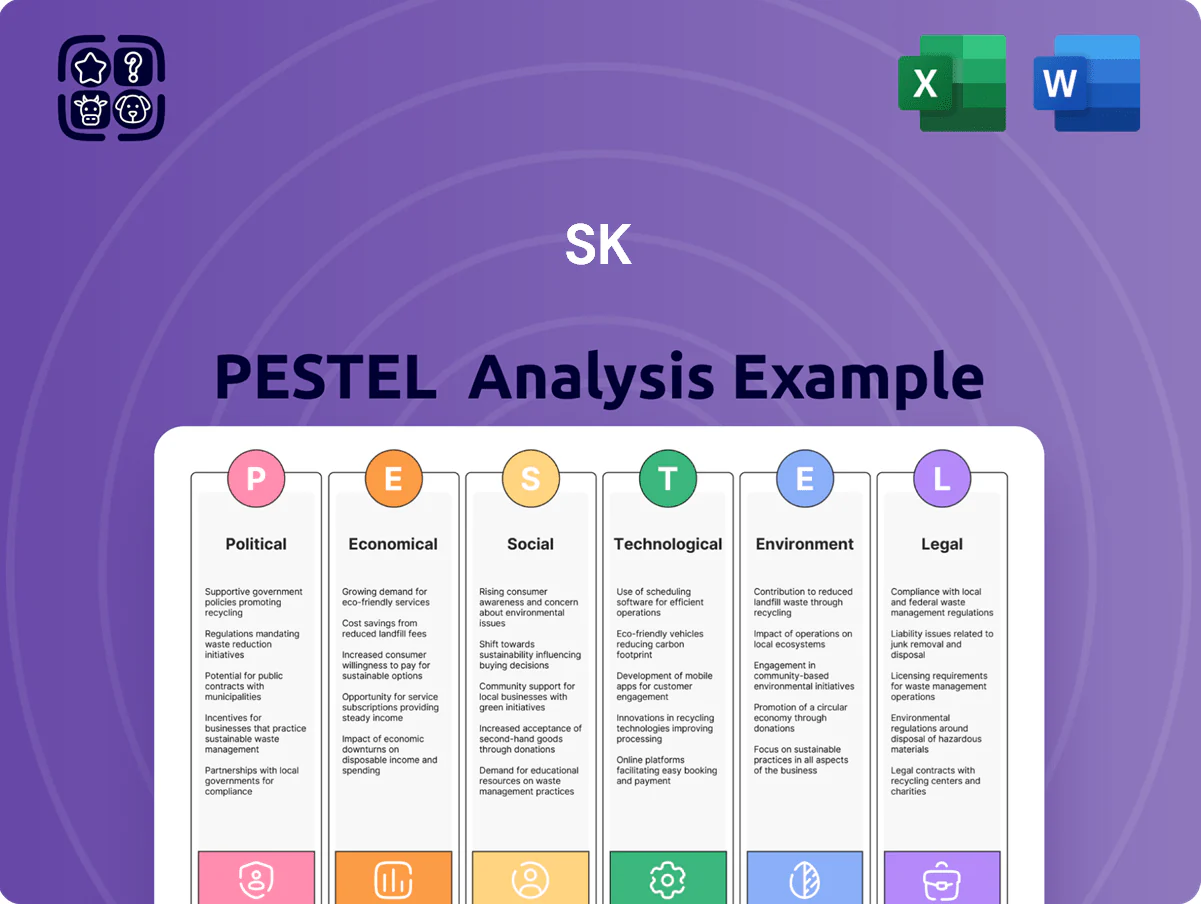

Explores how external macro-environmental factors uniquely affect the SK across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condensed PESTLE summary tailored to SK that highlights key political, economic, social, technological, legal, and environmental drivers for quick inclusion in presentations or strategic briefs.

Economic factors

Global semiconductor market cyclicality

SK Inc.s financials are tightly linked to memory cyclicality; DRAM and NAND swings drove SK hynix revenues to ¥36.9 trillion (2024) and industry ASP declines of ~25% in 2024 cut group dividend payouts materially.

AI server demand buoyed DRAM pricing in H1 2025, but consumer slowdown and oversupply pushed utilisation below 70% in late 2024, pressuring cash flow.

Management uses counter-cyclical capex and inventory cuts—SK hynix reduced 2024 capex ~30% y/y—to smooth income and protect dividend stability.

Interest rate environment and capital allocation

High global interest rates—US Fed funds at 5.25–5.50% and BOK base rate at 3.50% in 2025—raise SK Inc.’s cost of debt, pressuring its leverage-heavy acquisition strategy after net debt rose to about KRW 30 trillion in 2024.

As a holding company, SK’s capacity to fund biotech and hydrogen deals depends on credit market access; rising yields lifted Korea 10-year sovereign yield to ~3.8% in 2025, narrowing borrowing options.

Shifts in Fed and BOK policy materially affect SK Group’s net interest expense—reported interest expense increased ~15% year-over-year in 2024—constraining near-term investment capacity.

Currency exchange rate volatility

As an export-oriented conglomerate, SK Inc. is highly exposed to KRW/USD swings; in 2024 the won weakened ~6% vs. the dollar, which potentially improved export competitiveness but raised imported raw material costs and FX-linked interest expenses.

A weaker KRW raised SK Group’s reported COGS for petrochemical and battery segments—import input shares >40%—and increased USD debt servicing on roughly $8–10bn external liabilities.

Active hedging—FX forwards, options, natural hedges—remains critical to protect operating margins and stabilize 2024–25 EBITDA volatility amid projected KRW downside risks.

Inflationary pressures on operational costs

Persistent inflation in energy (natural gas up ~40% YoY in 2024 in South Korea) and rising labor costs (minimum wage +5.1% in 2024) squeeze SK’s manufacturing margins, lowering EBITDA at some subsidiaries by estimated 2–4 percentage points in 2024.

Passing costs to customers is constrained by competitive sectors where price elasticity risks market-share loss; SK prioritizes efficiency and cost-cutting to protect margins.

- Energy +40% YoY (2024)

- Minimum wage +5.1% (2024)

- EBITDA hit ~2–4 ppt (2024)

Emerging market growth and diversification

SK Inc. targets Southeast Asia and India to diversify from mature markets; ASEAN GDP grew 4.9% in 2024 and India 7.2% in FY2024, offering demand for SK’s digital services and telecom infrastructure investments.

Localized pricing and partnerships are needed as per-capita incomes vary—2024 GDP per capita: Indonesia $4,200, Vietnam $4,100, India $2,600—impacting ARPU and rollout economics.

- ASEAN GDP growth 4.9% (2024) and India 7.2% (FY2024)

- GDP per capita: Indonesia $4,200; Vietnam $4,100; India $2,600 (2024)

- Requires local pricing, partnerships, and tailored investment to hit ARPU targets

SK Inc.: Margin Pressure from Memory Cycles, Rates and FX; ASEAN/India Diversification Eases Risk

SK Inc. faces cyclical memory revenue swings (SK hynix ¥36.9T 2024) and higher funding costs—KRW debt ~30T (2024), BOK 3.50% and Fed 5.25–5.50% (2025)—while FX (KRW −6% vs USD 2024), energy +40% YoY (2024) and wage +5.1% (2024) compress margins; diversification to ASEAN/India (GDP 4.9%/7.2% 2024) offsets demand risk.

| Metric | Value (2024/25) |

|---|---|

| SK hynix Revenue | ¥36.9T (2024) |

| Net debt | KRW ~30T (2024) |

| Fed / BOK rates | 5.25–5.50% / 3.50% (2025) |

| KRW vs USD | −6% (2024) |

| Energy inflation | +40% YoY (2024) |

| Min wage | +5.1% (2024) |

| ASEAN / India GDP | 4.9% / 7.2% (2024) |

Preview Before You Purchase

SK PESTLE Analysis

The preview shown here is the exact SK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without modifications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic trends, and technological innovation are reshaping SK’s strategic outlook with our concise PESTLE snapshot—designed to spark strategic thinking and spotlight risks and opportunities you can act on today; purchase the full PESTLE for a comprehensive, editable analysis and immediate insights tailored for investors, consultants, and executives.

Political factors

Geopolitical tensions and semiconductor trade restrictions

The US–China rivalry hits SK via SK Hynix; US export controls since 2022 and 2023 curbs on EUV-related gear and high-end AI chips constrain supply and sales—SK Hynix reported 2024 capex of KRW 9.2tn amid these limits.

SK must weigh China manufacturing (20–30% revenue exposure in memory markets) against US CHIPS Act incentives—US offers up to $39bn for fabs, influencing SK’s location, tax and subsidy strategy.

South Korean government industrial policy

The South Korean administration treats the K-Semiconductor Belt and green energy as national security priorities, pledging a 510 trillion won semiconductor+future tech fund through 2027 and green industry incentives; SK Inc. wins tax credits and R&D subsidies (e.g., Korea’s 2024 tax breaks for chipmakers, battery R&D grants covering up to 30% of project costs), making alignment with state strategy essential to secure long-term infrastructure and capital support.

Inter-Korean relations and regional stability

Fluctuations in the political climate on the Korean Peninsula remain a systemic risk for Seoul-based conglomerates; 2024 saw 18 major North-South incidents, contributing to a 12% spike in KOSPI volatility during flare-ups.

Any escalation in North Korean military posturing can trigger capital flight and compress SK Inc. valuations—SK holdings fell 6% intra-day during the Oct 2024 tensions.

Investors closely monitor developments: South Korea sovereign CDS widened from 40bps to 72bps in 2024, raising the market risk premium and borrowing costs for SK group firms.

Global energy security and supply chain diplomacy

As a major energy and chemicals player via SK Innovation, SK is exposed to shifts in global energy alliances; 2025 oil price volatility (Brent range $70–95/bbl) and OPEC+ quota changes can swing feedstock costs and refinery margins by several percentage points.

Political instability in the Middle East raises supply risk that can increase input costs—SK reported feedstock cost sensitivity affecting EBITDA margins by ~2–4% in 2024.

SK Inc. pursues resource diplomacy, securing diversified sources for battery metals and LNG; by 2025 it expanded supply agreements covering ~40% of projected battery raw-material needs.

- Exposure to Brent volatility $70–95/bbl (2025)

- Feedstock cost moves impacted EBITDA ~2–4% (2024)

- Supply agreements cover ~40% of battery raw-material needs (2025)

Corporate governance and Chaebol reform pressures

Domestic pressure to boost transparency and minority shareholder protections continues to shape SK Inc.; Korea’s Financial Services Commission proposals in 2024 aimed at tighter disclosure and fair trading affect holding-company oversight and could raise compliance costs by an estimated 2–4% of administrative expenses.

Ongoing legislative moves to reform Chaebol—targeting cross-shareholding and intra-group transactions—force SK to adjust internal deals and succession plans to avoid fines or forced asset divestitures.

Maintaining proactive governance (enhanced boards, independent directors; SK reported 40% independent directors in 2024) is essential to reduce regulatory scrutiny and restore investor confidence after recent activist interventions.

- 2024 FSC proposals tighten disclosure, affecting compliance costs (approx +2–4%)

- Chaebol reforms target cross-shareholdings and intra-group deals

- SK had ~40% independent directors in 2024; governance upgrades reduce scrutiny

US‑China tech clash, CHIPS incentives reshape SK capex; geopolitical risks tighten

US–China tech rivalry, export controls and CHIPS Act incentives reshape SK’s capex and location choices; 2024 SK Hynix capex KRW 9.2tn, US incentives up to $39bn. Domestic policy: 510tn won semiconductor+future tech fund to 2027, 2024 FSC proposals raise compliance ~2–4%. Geopolitical risks: 18 N‑S incidents in 2024, sovereign CDS widened 40→72bps; feedstock cost swing hit EBITDA ~2–4% (2024).

| Metric | 2024/25 |

|---|---|

| SK Hynix capex | KRW 9.2tn (2024) |

| US CHIPS | Up to $39bn |

| K‑tech fund | KRW 510tn to 2027 |

| Sov CDS | 40→72bps (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the SK across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condensed PESTLE summary tailored to SK that highlights key political, economic, social, technological, legal, and environmental drivers for quick inclusion in presentations or strategic briefs.

Economic factors

Global semiconductor market cyclicality

SK Inc.s financials are tightly linked to memory cyclicality; DRAM and NAND swings drove SK hynix revenues to ¥36.9 trillion (2024) and industry ASP declines of ~25% in 2024 cut group dividend payouts materially.

AI server demand buoyed DRAM pricing in H1 2025, but consumer slowdown and oversupply pushed utilisation below 70% in late 2024, pressuring cash flow.

Management uses counter-cyclical capex and inventory cuts—SK hynix reduced 2024 capex ~30% y/y—to smooth income and protect dividend stability.

Interest rate environment and capital allocation

High global interest rates—US Fed funds at 5.25–5.50% and BOK base rate at 3.50% in 2025—raise SK Inc.’s cost of debt, pressuring its leverage-heavy acquisition strategy after net debt rose to about KRW 30 trillion in 2024.

As a holding company, SK’s capacity to fund biotech and hydrogen deals depends on credit market access; rising yields lifted Korea 10-year sovereign yield to ~3.8% in 2025, narrowing borrowing options.

Shifts in Fed and BOK policy materially affect SK Group’s net interest expense—reported interest expense increased ~15% year-over-year in 2024—constraining near-term investment capacity.

Currency exchange rate volatility

As an export-oriented conglomerate, SK Inc. is highly exposed to KRW/USD swings; in 2024 the won weakened ~6% vs. the dollar, which potentially improved export competitiveness but raised imported raw material costs and FX-linked interest expenses.

A weaker KRW raised SK Group’s reported COGS for petrochemical and battery segments—import input shares >40%—and increased USD debt servicing on roughly $8–10bn external liabilities.

Active hedging—FX forwards, options, natural hedges—remains critical to protect operating margins and stabilize 2024–25 EBITDA volatility amid projected KRW downside risks.

Inflationary pressures on operational costs

Persistent inflation in energy (natural gas up ~40% YoY in 2024 in South Korea) and rising labor costs (minimum wage +5.1% in 2024) squeeze SK’s manufacturing margins, lowering EBITDA at some subsidiaries by estimated 2–4 percentage points in 2024.

Passing costs to customers is constrained by competitive sectors where price elasticity risks market-share loss; SK prioritizes efficiency and cost-cutting to protect margins.

- Energy +40% YoY (2024)

- Minimum wage +5.1% (2024)

- EBITDA hit ~2–4 ppt (2024)

Emerging market growth and diversification

SK Inc. targets Southeast Asia and India to diversify from mature markets; ASEAN GDP grew 4.9% in 2024 and India 7.2% in FY2024, offering demand for SK’s digital services and telecom infrastructure investments.

Localized pricing and partnerships are needed as per-capita incomes vary—2024 GDP per capita: Indonesia $4,200, Vietnam $4,100, India $2,600—impacting ARPU and rollout economics.

- ASEAN GDP growth 4.9% (2024) and India 7.2% (FY2024)

- GDP per capita: Indonesia $4,200; Vietnam $4,100; India $2,600 (2024)

- Requires local pricing, partnerships, and tailored investment to hit ARPU targets

SK Inc.: Margin Pressure from Memory Cycles, Rates and FX; ASEAN/India Diversification Eases Risk

SK Inc. faces cyclical memory revenue swings (SK hynix ¥36.9T 2024) and higher funding costs—KRW debt ~30T (2024), BOK 3.50% and Fed 5.25–5.50% (2025)—while FX (KRW −6% vs USD 2024), energy +40% YoY (2024) and wage +5.1% (2024) compress margins; diversification to ASEAN/India (GDP 4.9%/7.2% 2024) offsets demand risk.

| Metric | Value (2024/25) |

|---|---|

| SK hynix Revenue | ¥36.9T (2024) |

| Net debt | KRW ~30T (2024) |

| Fed / BOK rates | 5.25–5.50% / 3.50% (2025) |

| KRW vs USD | −6% (2024) |

| Energy inflation | +40% YoY (2024) |

| Min wage | +5.1% (2024) |

| ASEAN / India GDP | 4.9% / 7.2% (2024) |

Preview Before You Purchase

SK PESTLE Analysis

The preview shown here is the exact SK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without modifications.