Skadden, Arps, Slate, Meagher & Flom Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

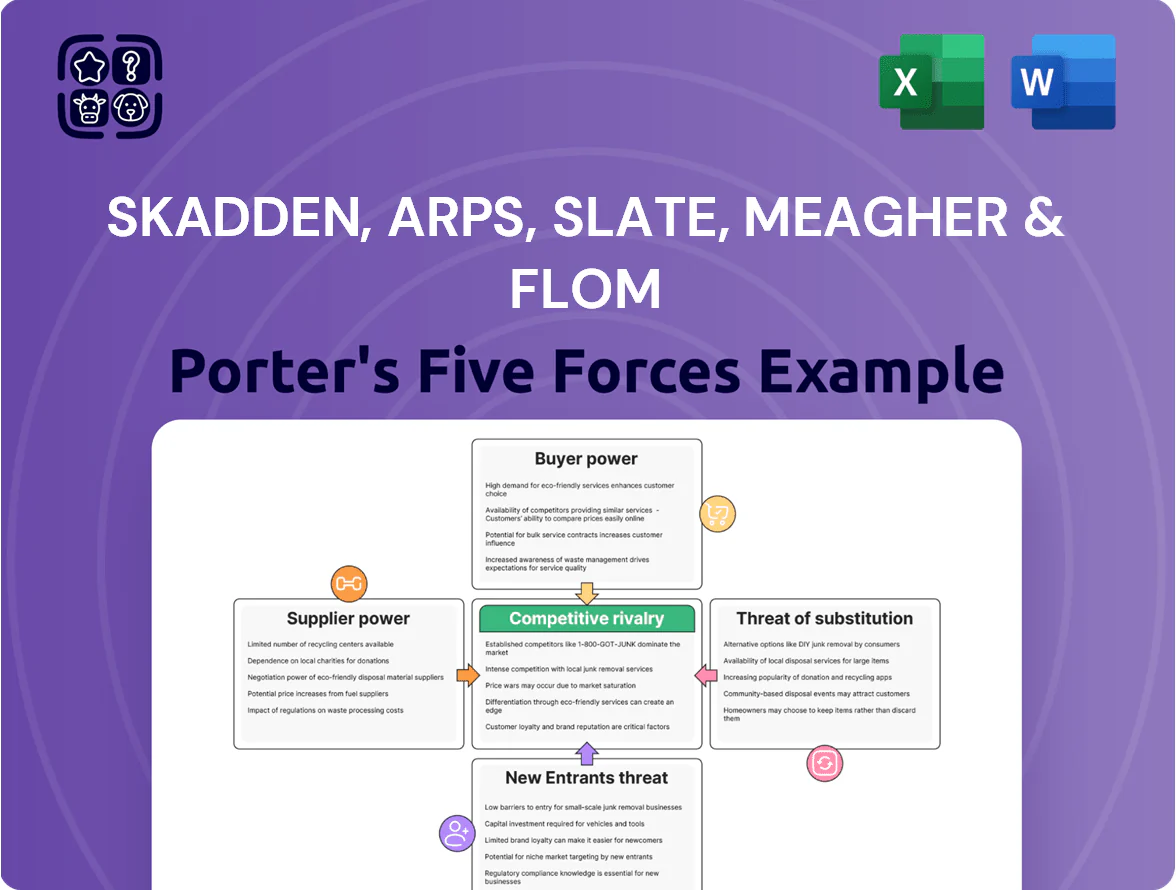

Skadden, Arps faces intense rivalry among elite global law firms, strong buyer power from corporate clients, and moderate supplier influence from specialized legal talent, while regulatory shifts and alternative legal service providers pose notable threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Skadden, Arps, Slate, Meagher & Flom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Elite Legal Talent Acquisition

Suppliers are elite law graduates and lateral partners who command top pay; in 2025 BigLaw starting salaries hit 215,000 USD and partner laterals often get multi-year guarantees exceeding 1–3 million USD, giving suppliers strong leverage.

Skadden must match lockstep or offer merit pay and signing bonuses—recent lateral buyouts averaged 500–1,200k USD—to avoid exits to rivals like Wachtell or Cravath.

Specialized Legal Technology Providers

Suppliers of AI research and e-discovery tools now wield more power as firms depend on them for speed and scale; in 2024 legal AI spend across large firms rose ~28% to an estimated $1.2bn, boosting vendor leverage. Skadden leans on these platforms to process terabytes of documents in major deals and litigations, so vendor uptime and feature roadmaps matter. High switching costs—integration, training, and license migration often >$5m for top-tier suites—further increase supplier bargaining power.

Premium Office Real Estate

Maintaining offices in New York, London and Hong Kong forces Skadden to absorb premium rents—Manhattan Class A rents averaged $110/sq ft in 2025 Q4, West End London £95/sq ft and Central Hong Kong HK$1200/sq ft—giving landlords strong leverage from scarce trophy addresses; Skadden’s prestige and client access tie it to these locations, reducing its bargaining power and creating predictable lease cost exposure that limits rent-driven flexibility.

Professional Liability Insurers

For Skadden, Arps, Slate, Meagher & Flom, malpractice and liability insurance is a major cost driver given multi-billion-dollar M&A and global litigation exposure; industry-wide D&O and professional liability premium rates rose ~20–30% from 2020–2024, pressuring large-firm budgets.

A small group of insurers can underwrite these risks, creating supplier concentration that lets carriers impose stricter terms, higher retentions, and selective capacity, reducing Skadden’s bargaining power.

Expert Witness and Consulting Networks

Complex litigation at Skadden demands world-class subject-matter experts and economic consultants whose niche skills are scarce, giving suppliers high bargaining power; top expert witness rates average $500–1,200/hour in 2024, and large cases often spend $1–5M on expert fees.

Skadden sustains favorable client outcomes by keeping long-term relationships, pre-engagement retainer agreements, and co-billing arrangements to mitigate cost and availability risks.

- Experts scarce → high supplier power

- Typical expert fees: $500–1,200/hour (2024)

- Big cases: $1–5M on experts

- Mitigation: retainers, co-billing, preferred panels

Suppliers Tighten Grip: Talent, AI Spend & Insurance Drive Costs Skyward

Suppliers (elite lawyers, lateral partners, AI/e-discovery vendors, insurers, expert witnesses, landlords) exert high bargaining power due to scarce talent, rising BigLaw pay (2025 starting $215,000; lateral buyouts $500–1,200k), legal-AI spend (~$1.2bn in 2024, +28%), insurance premiums +20–30% (2020–24), and high switching costs (tool integration >$5m, expert fees $500–1,200/hr).

| Supplier | Key metric |

|---|---|

| Starting salary | $215,000 (2025) |

| Lateral buyouts | $500–1,200k |

| Legal-AI spend | $1.2bn (2024, +28%) |

| Insurance rise | +20–30% (2020–24) |

What is included in the product

Tailored Porter's Five Forces analysis for Skadden, Arps, Slate, Meagher & Flom that uncovers competitive drivers, client bargaining power, supplier influence, threat of new entrants and substitutes, plus strategic vulnerabilities and protective barriers affecting its market position.

One-sheet Porter's Five Forces for Skadden—rapidly assess competitive pressure across client markets, talent poaching, regulatory threats, billing power, and substitute legal services to streamline strategic decisions.

Customers Bargaining Power

Concentration of Institutional Clients

Skadden’s revenue heavily depends on major corporations and banks; in 2024 top 50 clients likely accounted for an estimated 30–40% of revenue, giving those institutional buyers strong bargaining power.

These sophisticated clients can push for discounted hourly rates or alternative fee arrangements; surveys in 2023 showed 58% of large corporates demanded AFAs for big matters.

Because clients can shift large portfolios of work, Skadden faces sizable leverage at renewals, raising margin pressure and forcing flexible pricing to retain business.

Shift Toward Alternative Fee Structures

By late 2025 many corporate clients shifted from billable hours to fixed-fee or success-based pricing, with surveys showing 42% of Fortune 500 legal budgets using alternative fees in 2024–25. This trend forces Skadden to increase transparency and efficiency in staffing, matter planning, and e-billing to protect margins. Clients leverage buying power to demand fee risk-sharing—sometimes tying 10–30% of fees to case outcomes—pressuring the firm’s revenue volatility and cash flow predictability.

Internalization of Legal Services

Many corporate clients have grown in-house legal teams; by 2024 58% of S&P 500 companies reported handling more routine M&A and compliance work internally, cutting demand for external counsel to only high-stakes matters.

That shift makes clients highly selective and price-sensitive: 2023/24 surveys show 42% of general counsel negotiate fees even with elite firms like Skadden, pressing alternative fee arrangements for bet-the-company deals.

Low Switching Costs Between Elite Firms

- Clients keep 3–5 elite firms (2024)

- Multiple bids on >$1bn deals

- Skadden partner rate ≈ $1,300/hr (2024)

- Low contractual lock-ins increases leverage

Client Demand for ESG and Diversity Compliance

Institutional buyers — pension funds, asset managers, and sovereign wealth funds — now demand ESG and diversity data; a 2024 McKinsey report found 72% of institutional clients consider supplier DEI a deal factor, forcing Skadden to expand non-legal reporting teams and compliance systems.

Clients use $billions in legal spend as leverage; missing ESG/diversity targets risks losing major accounts and up to an estimated 10–20% revenue exposure in worst-case client churn scenarios.

- 72% of institutional clients weigh DEI (McKinsey 2024)

Skadden's top clients command 30–40% revenue, driving AFAs, fee pressure, and churn risk

Major clients likely drove ~30–40% of Skadden revenue in 2024, giving them strong leverage to demand AFAs (58% of large corporates in 2023), fee caps, and outcome-linked fees (10–30%), compressed partner rates (~$1,300/hr in 2024), and selective work as in-house teams handled 58% of routine tasks; ESG/DEI demands (72% institutional weight in 2024) add churn risk (10–20% revenue exposure).

| Metric | Value |

|---|---|

| Top-50 client revenue share (2024) | 30–40% |

| AFAs demanded (2023) | 58% |

| Partner rate (2024) | ~$1,300/hr |

| In-house handling (S&P500, 2024) | 58% |

| ESG/DEI weight (institutional, 2024) | 72% |

| Potential churn exposure | 10–20% |

Same Document Delivered

Skadden, Arps, Slate, Meagher & Flom Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Skadden, Arps, Slate, Meagher & Flom you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Skadden, Arps faces intense rivalry among elite global law firms, strong buyer power from corporate clients, and moderate supplier influence from specialized legal talent, while regulatory shifts and alternative legal service providers pose notable threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Skadden, Arps, Slate, Meagher & Flom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Elite Legal Talent Acquisition

Suppliers are elite law graduates and lateral partners who command top pay; in 2025 BigLaw starting salaries hit 215,000 USD and partner laterals often get multi-year guarantees exceeding 1–3 million USD, giving suppliers strong leverage.

Skadden must match lockstep or offer merit pay and signing bonuses—recent lateral buyouts averaged 500–1,200k USD—to avoid exits to rivals like Wachtell or Cravath.

Specialized Legal Technology Providers

Suppliers of AI research and e-discovery tools now wield more power as firms depend on them for speed and scale; in 2024 legal AI spend across large firms rose ~28% to an estimated $1.2bn, boosting vendor leverage. Skadden leans on these platforms to process terabytes of documents in major deals and litigations, so vendor uptime and feature roadmaps matter. High switching costs—integration, training, and license migration often >$5m for top-tier suites—further increase supplier bargaining power.

Premium Office Real Estate

Maintaining offices in New York, London and Hong Kong forces Skadden to absorb premium rents—Manhattan Class A rents averaged $110/sq ft in 2025 Q4, West End London £95/sq ft and Central Hong Kong HK$1200/sq ft—giving landlords strong leverage from scarce trophy addresses; Skadden’s prestige and client access tie it to these locations, reducing its bargaining power and creating predictable lease cost exposure that limits rent-driven flexibility.

Professional Liability Insurers

For Skadden, Arps, Slate, Meagher & Flom, malpractice and liability insurance is a major cost driver given multi-billion-dollar M&A and global litigation exposure; industry-wide D&O and professional liability premium rates rose ~20–30% from 2020–2024, pressuring large-firm budgets.

A small group of insurers can underwrite these risks, creating supplier concentration that lets carriers impose stricter terms, higher retentions, and selective capacity, reducing Skadden’s bargaining power.

Expert Witness and Consulting Networks

Complex litigation at Skadden demands world-class subject-matter experts and economic consultants whose niche skills are scarce, giving suppliers high bargaining power; top expert witness rates average $500–1,200/hour in 2024, and large cases often spend $1–5M on expert fees.

Skadden sustains favorable client outcomes by keeping long-term relationships, pre-engagement retainer agreements, and co-billing arrangements to mitigate cost and availability risks.

- Experts scarce → high supplier power

- Typical expert fees: $500–1,200/hour (2024)

- Big cases: $1–5M on experts

- Mitigation: retainers, co-billing, preferred panels

Suppliers Tighten Grip: Talent, AI Spend & Insurance Drive Costs Skyward

Suppliers (elite lawyers, lateral partners, AI/e-discovery vendors, insurers, expert witnesses, landlords) exert high bargaining power due to scarce talent, rising BigLaw pay (2025 starting $215,000; lateral buyouts $500–1,200k), legal-AI spend (~$1.2bn in 2024, +28%), insurance premiums +20–30% (2020–24), and high switching costs (tool integration >$5m, expert fees $500–1,200/hr).

| Supplier | Key metric |

|---|---|

| Starting salary | $215,000 (2025) |

| Lateral buyouts | $500–1,200k |

| Legal-AI spend | $1.2bn (2024, +28%) |

| Insurance rise | +20–30% (2020–24) |

What is included in the product

Tailored Porter's Five Forces analysis for Skadden, Arps, Slate, Meagher & Flom that uncovers competitive drivers, client bargaining power, supplier influence, threat of new entrants and substitutes, plus strategic vulnerabilities and protective barriers affecting its market position.

One-sheet Porter's Five Forces for Skadden—rapidly assess competitive pressure across client markets, talent poaching, regulatory threats, billing power, and substitute legal services to streamline strategic decisions.

Customers Bargaining Power

Concentration of Institutional Clients

Skadden’s revenue heavily depends on major corporations and banks; in 2024 top 50 clients likely accounted for an estimated 30–40% of revenue, giving those institutional buyers strong bargaining power.

These sophisticated clients can push for discounted hourly rates or alternative fee arrangements; surveys in 2023 showed 58% of large corporates demanded AFAs for big matters.

Because clients can shift large portfolios of work, Skadden faces sizable leverage at renewals, raising margin pressure and forcing flexible pricing to retain business.

Shift Toward Alternative Fee Structures

By late 2025 many corporate clients shifted from billable hours to fixed-fee or success-based pricing, with surveys showing 42% of Fortune 500 legal budgets using alternative fees in 2024–25. This trend forces Skadden to increase transparency and efficiency in staffing, matter planning, and e-billing to protect margins. Clients leverage buying power to demand fee risk-sharing—sometimes tying 10–30% of fees to case outcomes—pressuring the firm’s revenue volatility and cash flow predictability.

Internalization of Legal Services

Many corporate clients have grown in-house legal teams; by 2024 58% of S&P 500 companies reported handling more routine M&A and compliance work internally, cutting demand for external counsel to only high-stakes matters.

That shift makes clients highly selective and price-sensitive: 2023/24 surveys show 42% of general counsel negotiate fees even with elite firms like Skadden, pressing alternative fee arrangements for bet-the-company deals.

Low Switching Costs Between Elite Firms

- Clients keep 3–5 elite firms (2024)

- Multiple bids on >$1bn deals

- Skadden partner rate ≈ $1,300/hr (2024)

- Low contractual lock-ins increases leverage

Client Demand for ESG and Diversity Compliance

Institutional buyers — pension funds, asset managers, and sovereign wealth funds — now demand ESG and diversity data; a 2024 McKinsey report found 72% of institutional clients consider supplier DEI a deal factor, forcing Skadden to expand non-legal reporting teams and compliance systems.

Clients use $billions in legal spend as leverage; missing ESG/diversity targets risks losing major accounts and up to an estimated 10–20% revenue exposure in worst-case client churn scenarios.

- 72% of institutional clients weigh DEI (McKinsey 2024)

Skadden's top clients command 30–40% revenue, driving AFAs, fee pressure, and churn risk

Major clients likely drove ~30–40% of Skadden revenue in 2024, giving them strong leverage to demand AFAs (58% of large corporates in 2023), fee caps, and outcome-linked fees (10–30%), compressed partner rates (~$1,300/hr in 2024), and selective work as in-house teams handled 58% of routine tasks; ESG/DEI demands (72% institutional weight in 2024) add churn risk (10–20% revenue exposure).

| Metric | Value |

|---|---|

| Top-50 client revenue share (2024) | 30–40% |

| AFAs demanded (2023) | 58% |

| Partner rate (2024) | ~$1,300/hr |

| In-house handling (S&P500, 2024) | 58% |

| ESG/DEI weight (institutional, 2024) | 72% |

| Potential churn exposure | 10–20% |

Same Document Delivered

Skadden, Arps, Slate, Meagher & Flom Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Skadden, Arps, Slate, Meagher & Flom you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.