Shanghai Kehua Bio-engineering Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

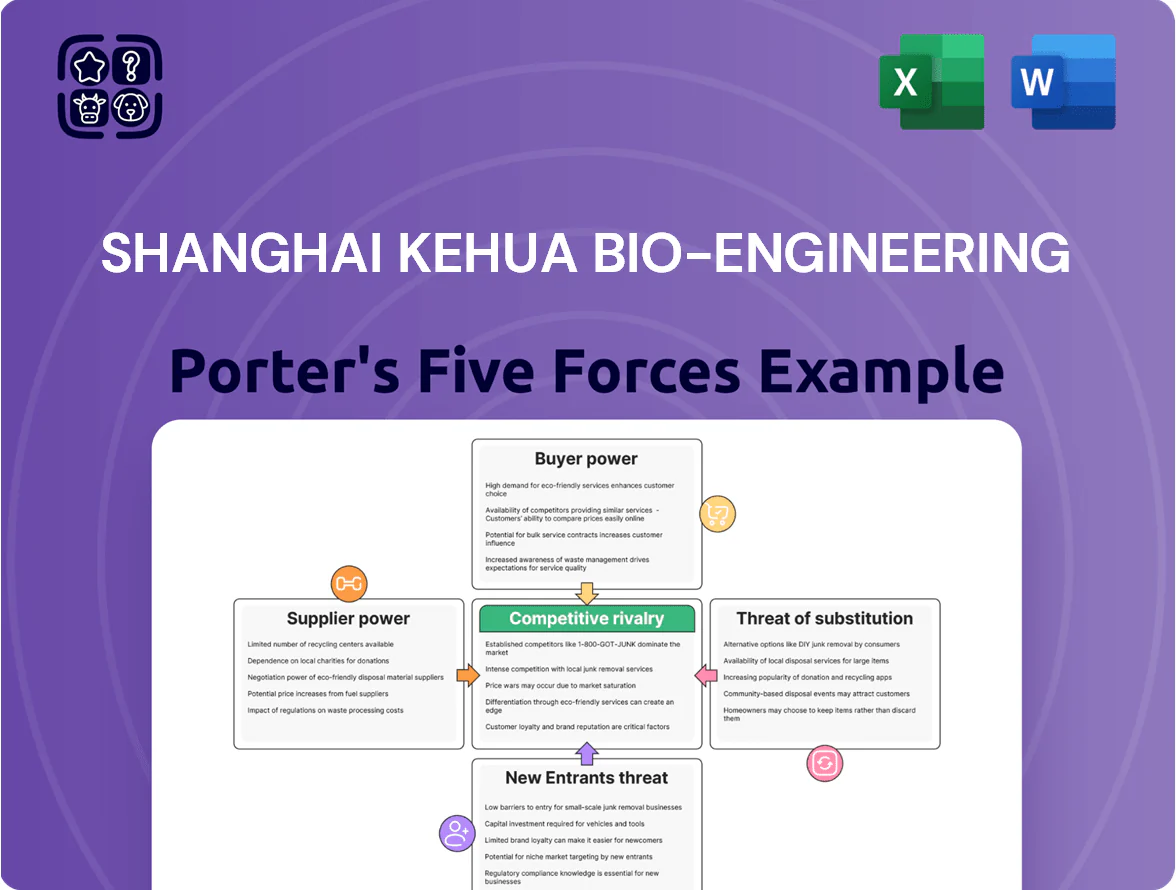

Shanghai Kehua Bio-engineering faces moderate supplier power and high regulatory scrutiny, while buyer power and rivalry intensify amid pricing pressure and innovation cycles; barriers to entry are notable but niche biotech startups pose targeted threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Kehua Bio-engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Shanghai Kehua Bio-engineering depends on high-purity antigens and enzymes from global suppliers—about 60–70% of its critical reagent spend in 2024—so supplier influence is material. Domestic suppliers rose to ~35% market share in 2024, but switching needs months of validation and can trigger CFDA/NMPA re-filing, raising costs ~10–15% and delaying revenue recognition. That makes supplier power moderate but strategically significant.

Advanced Instrumentation Component Sourcing

The manufacturing of automated diagnostic instruments relies on precise optical and electronic parts made by few specialized firms, giving suppliers pricing and delivery leverage; industry data shows the top 5 global precision optics suppliers control ~60% of market share as of 2025.

Supplier Concentration in Biotech

The upstream market for critical diagnostic inputs is dominated by a few global biotech giants—Thermo Fisher Scientific, Danaher, and Roche together held about 45% of the global reagents and consumables market in 2024—reducing alternative suppliers for specialized reagents used in blood screening and tumor marker assays.

This concentration raises supply-chain risk for Shanghai Kehua Bio-engineering: a 10–20% price rise or a strategic shift by a dominant supplier could raise COGS by roughly 3–6 percentage points, given reagent costs represented ~18% of product costs in 2024.

Technological Proprietary Inputs

Proprietary reagents and biomarkers used in molecular diagnostics are often patent‑protected by third‑party suppliers, locking Shanghai Kehua Bio-engineering into higher input costs and licensing fees; for example, global assay reagent royalties average 8–12% of product price in 2024, raising COGS for new molecular lines.

Replacing these inputs needs major R&D or licensing—Kehua would face multi‑year development and likely $5–15M per assay to validate substitutes—so supplier leverage intensifies as molecular revenue grows.

- Patents raise switching cost and licensing fees (8–12% typical royalty, 2024)

- Substitute development ≈ $5–15M and 12–24 months per assay

- Dependency strongest for high‑growth molecular products

Rising Costs of Specialized Labor

Suppliers of specialized research services and high-tech equipment face 12–18% higher average salaries for biotechnologists and engineers in Shanghai from 2020–2024, pushing service fees up 8–12% for diagnostic firms like Shanghai Kehua Bio-engineering.

As automation adoption rises—estimated 22% capex growth in biotech manufacturing 2021–2024—reliance on these suppliers increases, concentrating supplier power and raising switching costs for diagnostics firms.

- Salary increase: 12–18% (2020–2024)

- Service fee pass-through: +8–12%

- Biotech automation capex growth: ~22% (2021–2024)

High supplier leverage: concentrated reagents, costly switches raise COGS vulnerability

Suppliers hold moderate-to-high power: critical reagents made up ~60–70% of reagent spend in 2024, top 3 suppliers held ~45% global share (2024), and switching costs (validation, NMPA re-filing) add ~10–15% to costs; COGS sensitivity: a 10–20% input price rise would raise COGS ~3–6 pts. Substitution R&D ~ $5–15M and 12–24 months per assay, royalties 8–12% (2024).

| Metric | Value |

|---|---|

| Reagent spend concentration (2024) | 60–70% |

| Top 3 suppliers market share (2024) | ≈45% |

| Switching cost impact | +10–15% cost, 12–24m delay |

| Substitute R&D per assay | $5–15M |

| Royalty range (2024) | 8–12% |

| COGS sensitivity | +3–6 pts if input +10–20% |

What is included in the product

Tailored exclusively for Shanghai Kehua Bio-engineering, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Shanghai Kehua Bio-engineering—instantly highlights supplier, buyer, competitor, entrant, and substitute pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Centralized Government Procurement Policies

The Chinese Volume-Based Procurement (VBP) centralizes buying for public hospitals, shifting pricing power to state health authorities; in 2024 VBP covered over 50% of hospital procurements and cut diagnostics prices by 20–40% in pilot categories. Shanghai Kehua must compete on thin margins to win large tenders, where single contracts can represent 30–60% of annual public-sales for a product line.

Hospital System Consolidation

Hospital system consolidation in China has raised buyer power: by 2024 over 60% of tertiary hospitals belonged to regional clusters that centralize procurement, pushing Shanghai Kehua Bio-engineering to compete on bundled offers for reagents, instruments, and service to win contracts.

Low Switching Costs for Reagents

Diagnostic instruments cost millions up front, but 70–80% of lifecycle revenue comes from reagents, so buyers push for open-system compatibility and lower reagent prices; in China, hospitals switching to cheaper reagents cut supplier margins by 5–15% in 2024 according to industry reports. Commoditization of common infectious-disease assays (e.g., PCR panels) and competitors offering 10–30% cheaper or more accurate reagents increase buyer leverage, forcing frequent price concessions.

Demand for Integrated Diagnostic Value

Modern clinical labs now demand integrated diagnostic value: products plus digital data integration and 24/7 rapid technical support, not standalone reagents or instruments.

Customers leverage these service needs in negotiations—global IVD service contracts grew 14% in 2024, so buyers press for bundled pricing and SLAs to lower total cost of ownership.

Shanghai Kehua must keep enhancing cloud interfaces, remote diagnostics, and training to justify premium pricing in a buyer-centric market; otherwise margin pressure rises.

- Service-led deals rose 14% in 2024

- Buyers seek SLAs, data integration, 24/7 support

- Kehua needs cloud, remote diag, training to protect margins

Information Transparency in Healthcare

Rising digital transparency in diagnostics—price databases and performance registries—lets hospital procurement compare Shanghai Kehua Bio-engineering to peers; a 2024 IQVIA report showed 28% of Chinese hospitals use online price benchmarking, cutting information asymmetry and boosting buyer leverage.

That shifts negotiations toward demonstrated clinical utility; Kehua must prove superior outcomes or workflow gains to command premium over lower-cost rivals.

Buyers' VBP grip slashes prices 20–40%—Kehua pivots to bundled outcomes, cloud & SLAs

Buyers hold strong leverage: 2024 VBP covered >50% hospital spend and cut prices 20–40%; 60% of tertiary hospitals in clusters centralize procurement; reagents drive 70–80% lifecycle revenue so buyers extract 5–15% margin cuts; service-led contracts rose 14% and 28% of hospitals use price benchmarking (IQVIA 2024), forcing Kehua to sell bundled outcomes, cloud, and SLAs to protect margins.

| Metric | 2024 |

|---|---|

| VBP hospital spend | >50% |

| Tertiary hospital clusters | 60% |

| Reagent share of lifecycle rev | 70–80% |

| Price cuts from VBP | 20–40% |

| Service-led contract growth | 14% |

| Hospitals using benchmarking | 28% |

Full Version Awaits

Shanghai Kehua Bio-engineering Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Shanghai Kehua Bio-engineering you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use. The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights tailored to industry specifics. Once you buy, you’ll get this exact file for immediate download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Shanghai Kehua Bio-engineering faces moderate supplier power and high regulatory scrutiny, while buyer power and rivalry intensify amid pricing pressure and innovation cycles; barriers to entry are notable but niche biotech startups pose targeted threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Kehua Bio-engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Shanghai Kehua Bio-engineering depends on high-purity antigens and enzymes from global suppliers—about 60–70% of its critical reagent spend in 2024—so supplier influence is material. Domestic suppliers rose to ~35% market share in 2024, but switching needs months of validation and can trigger CFDA/NMPA re-filing, raising costs ~10–15% and delaying revenue recognition. That makes supplier power moderate but strategically significant.

Advanced Instrumentation Component Sourcing

The manufacturing of automated diagnostic instruments relies on precise optical and electronic parts made by few specialized firms, giving suppliers pricing and delivery leverage; industry data shows the top 5 global precision optics suppliers control ~60% of market share as of 2025.

Supplier Concentration in Biotech

The upstream market for critical diagnostic inputs is dominated by a few global biotech giants—Thermo Fisher Scientific, Danaher, and Roche together held about 45% of the global reagents and consumables market in 2024—reducing alternative suppliers for specialized reagents used in blood screening and tumor marker assays.

This concentration raises supply-chain risk for Shanghai Kehua Bio-engineering: a 10–20% price rise or a strategic shift by a dominant supplier could raise COGS by roughly 3–6 percentage points, given reagent costs represented ~18% of product costs in 2024.

Technological Proprietary Inputs

Proprietary reagents and biomarkers used in molecular diagnostics are often patent‑protected by third‑party suppliers, locking Shanghai Kehua Bio-engineering into higher input costs and licensing fees; for example, global assay reagent royalties average 8–12% of product price in 2024, raising COGS for new molecular lines.

Replacing these inputs needs major R&D or licensing—Kehua would face multi‑year development and likely $5–15M per assay to validate substitutes—so supplier leverage intensifies as molecular revenue grows.

- Patents raise switching cost and licensing fees (8–12% typical royalty, 2024)

- Substitute development ≈ $5–15M and 12–24 months per assay

- Dependency strongest for high‑growth molecular products

Rising Costs of Specialized Labor

Suppliers of specialized research services and high-tech equipment face 12–18% higher average salaries for biotechnologists and engineers in Shanghai from 2020–2024, pushing service fees up 8–12% for diagnostic firms like Shanghai Kehua Bio-engineering.

As automation adoption rises—estimated 22% capex growth in biotech manufacturing 2021–2024—reliance on these suppliers increases, concentrating supplier power and raising switching costs for diagnostics firms.

- Salary increase: 12–18% (2020–2024)

- Service fee pass-through: +8–12%

- Biotech automation capex growth: ~22% (2021–2024)

High supplier leverage: concentrated reagents, costly switches raise COGS vulnerability

Suppliers hold moderate-to-high power: critical reagents made up ~60–70% of reagent spend in 2024, top 3 suppliers held ~45% global share (2024), and switching costs (validation, NMPA re-filing) add ~10–15% to costs; COGS sensitivity: a 10–20% input price rise would raise COGS ~3–6 pts. Substitution R&D ~ $5–15M and 12–24 months per assay, royalties 8–12% (2024).

| Metric | Value |

|---|---|

| Reagent spend concentration (2024) | 60–70% |

| Top 3 suppliers market share (2024) | ≈45% |

| Switching cost impact | +10–15% cost, 12–24m delay |

| Substitute R&D per assay | $5–15M |

| Royalty range (2024) | 8–12% |

| COGS sensitivity | +3–6 pts if input +10–20% |

What is included in the product

Tailored exclusively for Shanghai Kehua Bio-engineering, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Shanghai Kehua Bio-engineering—instantly highlights supplier, buyer, competitor, entrant, and substitute pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Centralized Government Procurement Policies

The Chinese Volume-Based Procurement (VBP) centralizes buying for public hospitals, shifting pricing power to state health authorities; in 2024 VBP covered over 50% of hospital procurements and cut diagnostics prices by 20–40% in pilot categories. Shanghai Kehua must compete on thin margins to win large tenders, where single contracts can represent 30–60% of annual public-sales for a product line.

Hospital System Consolidation

Hospital system consolidation in China has raised buyer power: by 2024 over 60% of tertiary hospitals belonged to regional clusters that centralize procurement, pushing Shanghai Kehua Bio-engineering to compete on bundled offers for reagents, instruments, and service to win contracts.

Low Switching Costs for Reagents

Diagnostic instruments cost millions up front, but 70–80% of lifecycle revenue comes from reagents, so buyers push for open-system compatibility and lower reagent prices; in China, hospitals switching to cheaper reagents cut supplier margins by 5–15% in 2024 according to industry reports. Commoditization of common infectious-disease assays (e.g., PCR panels) and competitors offering 10–30% cheaper or more accurate reagents increase buyer leverage, forcing frequent price concessions.

Demand for Integrated Diagnostic Value

Modern clinical labs now demand integrated diagnostic value: products plus digital data integration and 24/7 rapid technical support, not standalone reagents or instruments.

Customers leverage these service needs in negotiations—global IVD service contracts grew 14% in 2024, so buyers press for bundled pricing and SLAs to lower total cost of ownership.

Shanghai Kehua must keep enhancing cloud interfaces, remote diagnostics, and training to justify premium pricing in a buyer-centric market; otherwise margin pressure rises.

- Service-led deals rose 14% in 2024

- Buyers seek SLAs, data integration, 24/7 support

- Kehua needs cloud, remote diag, training to protect margins

Information Transparency in Healthcare

Rising digital transparency in diagnostics—price databases and performance registries—lets hospital procurement compare Shanghai Kehua Bio-engineering to peers; a 2024 IQVIA report showed 28% of Chinese hospitals use online price benchmarking, cutting information asymmetry and boosting buyer leverage.

That shifts negotiations toward demonstrated clinical utility; Kehua must prove superior outcomes or workflow gains to command premium over lower-cost rivals.

Buyers' VBP grip slashes prices 20–40%—Kehua pivots to bundled outcomes, cloud & SLAs

Buyers hold strong leverage: 2024 VBP covered >50% hospital spend and cut prices 20–40%; 60% of tertiary hospitals in clusters centralize procurement; reagents drive 70–80% lifecycle revenue so buyers extract 5–15% margin cuts; service-led contracts rose 14% and 28% of hospitals use price benchmarking (IQVIA 2024), forcing Kehua to sell bundled outcomes, cloud, and SLAs to protect margins.

| Metric | 2024 |

|---|---|

| VBP hospital spend | >50% |

| Tertiary hospital clusters | 60% |

| Reagent share of lifecycle rev | 70–80% |

| Price cuts from VBP | 20–40% |

| Service-led contract growth | 14% |

| Hospitals using benchmarking | 28% |

Full Version Awaits

Shanghai Kehua Bio-engineering Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Shanghai Kehua Bio-engineering you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use. The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights tailored to industry specifics. Once you buy, you’ll get this exact file for immediate download.