Skyward Specialty Insurance PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE analysis of Skyward Specialty Insurance—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its strategy and risk profile; download the full report for actionable insights, ready-to-use charts, and editable files to inform investments, pitches, or strategic planning.

Political factors

Federal Regulatory Policy Shifts

As of early 2026, federal administrative priorities continue reshaping financial services, with Treasury and federal agencies issuing 12 major guidance updates since 2024 that affect capital adequacy and systemic risk rules relevant to insurers.

Skyward Specialty must adjust to evolving oversight—recent stress-test scenarios raised capital buffer expectations by ~15% for midsize specialty carriers—affecting pricing and product rollout timelines.

Regulatory shifts directly influence market entry: 2025 data show 22% fewer new specialty product filings in states citing federal guidance uncertainty, constraining Skyward’s niche expansion plans.

Infrastructure Spending Initiatives

Government-led infrastructure projects funded through mid-decade legislative cycles—US Bipartisan Infrastructure Law allocations reaching about $1.2 trillion through 2026—directly boost demand for surety and construction insurance, supporting Skyward Specialty’s project-based underwriting.

As a niche commercial insurer, Skyward benefits from sustained public investment in domestic energy and transportation, with $550B earmarked for roads and bridges and billions in grid and ports funding spurring specialty risk placements.

Skyward’s growth in these segments is sensitive to political appetite for continued fiscal expansion; a 10–15% reduction in planned infrastructure spend could materially compress premium volumes in targeted lines.

Geopolitical Influence on Reinsurance

Global political instability drove reinsurer capacity down 12% and pushed retrocession premiums up ~18% in 2024, tightening the market Skyward Specialty relies on for risk transfer; tensions in regions like Eastern Europe and the Middle East have been cited by major brokers as primary drivers. Skyward must continuously monitor geopolitical shifts to preserve underwriting margins and shore up capital, as reduced reinsurance availability can materially stress the balance sheet during systemic events.

State-Level Insurance Commissioner Influence

- 50+ state-level commissioners affect rate approvals

- 12 states updated mandated coverages (2023–2025)

- Skyward active in 30+ state jurisdictions, increasing compliance complexity

Trade Policies and Domestic Manufacturing

Political incentives for domestic manufacturing and near-shoring are boosting U.S. manufacturing investment, with announced reshoring projects exceeding $200 billion in 2024 and manufacturing capex rising ~6% YoY, creating expanded specialty casualty and workers’ comp exposures.

As rhetoric becomes policy—tax credits, CHIPS Act follow-ons, and state incentives—Skyward Specialty targets risks from modernized plants, automation, and supply-chain reconfiguration, aligning underwriting with higher-value industrial accounts.

Skyward’s focus on underserved segments matches an industrial resurgence: specialty casualty rates hardened in 2023–24, with workers’ comp loss trends up ~8% in targeted sectors, presenting premium growth opportunities.

- Reshoring projects >$200B (2024)

- Manufacturing capex +6% YoY (2024)

- Workers’ comp loss trends +8% in targeted industries (2023–24)

- Policy drivers: federal tax credits, CHIPS-related funding, state incentives

Regulatory shock cuts specialty filings 22% as reinsurers trim capacity amid $1.4T build boom

Federal guidance since 2024 raised capital buffer expectations ~15%, reducing new specialty filings by 22% in states citing uncertainty and cutting reinsurer capacity ~12% (retrocession premiums +18%), while $1.2T infrastructure allocations and $200B+ reshoring announce expand construction and manufacturing exposures, with Skyward active in 30+ states facing 50+ commissioners and 12 states' mandated coverage changes (2023–25).

| Metric | Value |

|---|---|

| Capital buffer shift | +15% |

| New filings drop | -22% |

| Reinsurer capacity | -12% |

| Retrocession premiums | +18% |

| Infrastructure funding | $1.2T (through 2026) |

| Reshoring projects | $200B (2024) |

| States with mandated changes | 12 (2023–25) |

| States active | 30+ |

What is included in the product

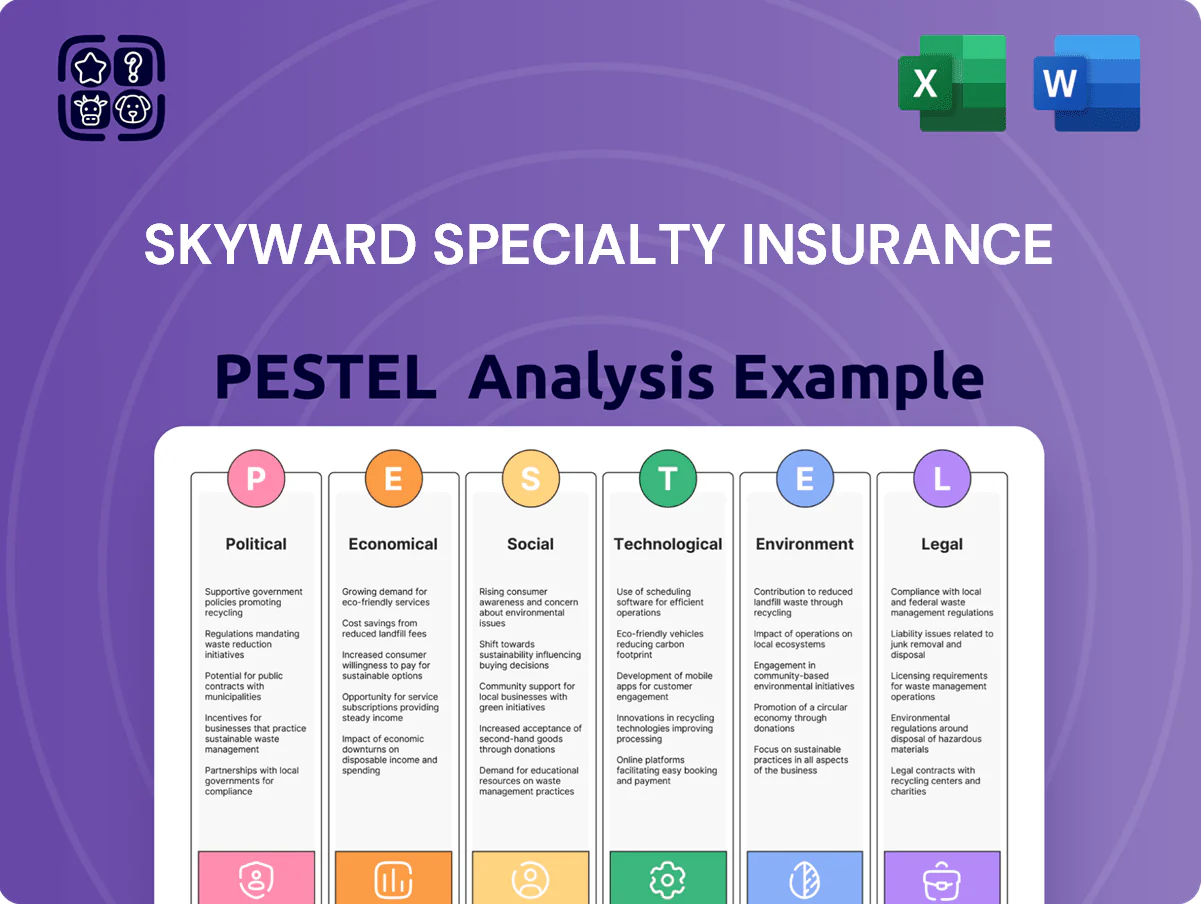

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Skyward Specialty Insurance, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Skyward Specialty Insurance that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment Stability

By end-2025 stabilization of US Treasury yields near 4.5–5.0% has increased Skyward Specialty’s investment income, boosting fixed-income returns and lifting portfolio market values, aiding underwriting margins. Higher sustained rates favor the company’s bond-heavy allocation, reducing reinvestment risk and supporting an estimated 50–100 bps improvement in yield on invested assets year-over-year. However, elevated borrowing costs have slowed capex in energy and construction sectors, softening demand for new specialty policies. Continued rate stability will likely sustain investment tailwinds but keep new premium growth pressured in capital-intensive industries.

Social Inflation and Loss Costs

Social inflation—driven by rising litigation costs and large jury awards—has pushed US commercial liability loss costs up about 35% since 2016, with jury verdicts median size rising 60% from 2015–2023; Skyward Specialty must deploy sophisticated actuarial models and trend assumptions to keep premiums aligned with these elevated claim severities.

Labor Market Dynamics in Niche Sectors

Shortages of skilled workers in construction and trucking—US construction job openings rose to 473,000 in Dec 2024 while trucking vacancy rates hit 6.1% in 2024—raise Skyward Specialty’s exposure as firms hire less-experienced labor, increasing accident frequency and claim severity; insurers saw construction loss ratios climb ~7 percentage points in 2023–24. Skyward must recalibrate underwriting models and pricing to reflect higher workforce-driven operational risk.

Reinsurance Market Pricing Cycles

The reinsurance pricing cycle controls Skyward Specialty’s cost of risk transfer; tightened markets in late 2025 show renewal rate increases of roughly 5–12% in specialty treaty segments, raising ceded cost pressures.

Disciplined pricing forces Skyward to optimize retentions and capital allocation—analysts estimate a 10–15% capital uplift needed to maintain writing capacity at current layers.

Securing favorable treaty terms is critical for growth: constrained reinsurance capacity could limit new specialty line writings by an estimated 8–20% under adverse scenarios.

- Late-2025 specialty treaty rate increases ~5–12%

- Required capital uplift to hold layers ~10–15%

- Potential new-business capacity reduction 8–20% if reinsurance tightens

General Inflationary Pressures

Broad inflation raises replacement costs for property and the medical costs in workers' comp; US CPI rose 3.4% in 2024 and medical services inflation was ~4.1%, increasing claim severity for Skyward Specialty.

Skyward mitigates via inflation guards and quarterly rate reviews across P&C lines; reinsurance and reserve adequacy must be adjusted to reflect a 3–5% annual cost runway.

Persistent inflation risks margin compression, forcing agile pricing, tighter underwriting, and loss-cost escalation monitoring to preserve combined ratios near target.

- US CPI 2024: +3.4%

- Medical services inflation 2024: ~4.1%

- Action: inflation guards, quarterly rate reviews, adjust reserves/reinsurance

Higher yields boost investment income but inflation, reinsurance hikes force 10–15% capital lift

Higher US Treasury yields (~4.5–5.0% end-2025) boosted investment income, improving yields on invested assets by ~50–100 bps, while elevated borrowing costs and tightened reinsurance (treaty rate increases ~5–12%) constrain new specialty premium growth and raise ceded costs; inflation (CPI 2024 +3.4%, medical +4.1%) increases claim severity, requiring 10–15% capital uplift to maintain capacity.

| Metric | Value |

|---|---|

| Treasury yields (eop 2025) | 4.5–5.0% |

| Yield on assets change | +50–100 bps |

| Reinsurance treaty rate change (late-2025) | +5–12% |

| US CPI 2024 | +3.4% |

| Medical inflation 2024 | ~4.1% |

| Estimated capital uplift | 10–15% |

Preview the Actual Deliverable

Skyward Specialty Insurance PESTLE Analysis

The preview shown here is the exact PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for Skyward Specialty Insurance.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE analysis of Skyward Specialty Insurance—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its strategy and risk profile; download the full report for actionable insights, ready-to-use charts, and editable files to inform investments, pitches, or strategic planning.

Political factors

Federal Regulatory Policy Shifts

As of early 2026, federal administrative priorities continue reshaping financial services, with Treasury and federal agencies issuing 12 major guidance updates since 2024 that affect capital adequacy and systemic risk rules relevant to insurers.

Skyward Specialty must adjust to evolving oversight—recent stress-test scenarios raised capital buffer expectations by ~15% for midsize specialty carriers—affecting pricing and product rollout timelines.

Regulatory shifts directly influence market entry: 2025 data show 22% fewer new specialty product filings in states citing federal guidance uncertainty, constraining Skyward’s niche expansion plans.

Infrastructure Spending Initiatives

Government-led infrastructure projects funded through mid-decade legislative cycles—US Bipartisan Infrastructure Law allocations reaching about $1.2 trillion through 2026—directly boost demand for surety and construction insurance, supporting Skyward Specialty’s project-based underwriting.

As a niche commercial insurer, Skyward benefits from sustained public investment in domestic energy and transportation, with $550B earmarked for roads and bridges and billions in grid and ports funding spurring specialty risk placements.

Skyward’s growth in these segments is sensitive to political appetite for continued fiscal expansion; a 10–15% reduction in planned infrastructure spend could materially compress premium volumes in targeted lines.

Geopolitical Influence on Reinsurance

Global political instability drove reinsurer capacity down 12% and pushed retrocession premiums up ~18% in 2024, tightening the market Skyward Specialty relies on for risk transfer; tensions in regions like Eastern Europe and the Middle East have been cited by major brokers as primary drivers. Skyward must continuously monitor geopolitical shifts to preserve underwriting margins and shore up capital, as reduced reinsurance availability can materially stress the balance sheet during systemic events.

State-Level Insurance Commissioner Influence

- 50+ state-level commissioners affect rate approvals

- 12 states updated mandated coverages (2023–2025)

- Skyward active in 30+ state jurisdictions, increasing compliance complexity

Trade Policies and Domestic Manufacturing

Political incentives for domestic manufacturing and near-shoring are boosting U.S. manufacturing investment, with announced reshoring projects exceeding $200 billion in 2024 and manufacturing capex rising ~6% YoY, creating expanded specialty casualty and workers’ comp exposures.

As rhetoric becomes policy—tax credits, CHIPS Act follow-ons, and state incentives—Skyward Specialty targets risks from modernized plants, automation, and supply-chain reconfiguration, aligning underwriting with higher-value industrial accounts.

Skyward’s focus on underserved segments matches an industrial resurgence: specialty casualty rates hardened in 2023–24, with workers’ comp loss trends up ~8% in targeted sectors, presenting premium growth opportunities.

- Reshoring projects >$200B (2024)

- Manufacturing capex +6% YoY (2024)

- Workers’ comp loss trends +8% in targeted industries (2023–24)

- Policy drivers: federal tax credits, CHIPS-related funding, state incentives

Regulatory shock cuts specialty filings 22% as reinsurers trim capacity amid $1.4T build boom

Federal guidance since 2024 raised capital buffer expectations ~15%, reducing new specialty filings by 22% in states citing uncertainty and cutting reinsurer capacity ~12% (retrocession premiums +18%), while $1.2T infrastructure allocations and $200B+ reshoring announce expand construction and manufacturing exposures, with Skyward active in 30+ states facing 50+ commissioners and 12 states' mandated coverage changes (2023–25).

| Metric | Value |

|---|---|

| Capital buffer shift | +15% |

| New filings drop | -22% |

| Reinsurer capacity | -12% |

| Retrocession premiums | +18% |

| Infrastructure funding | $1.2T (through 2026) |

| Reshoring projects | $200B (2024) |

| States with mandated changes | 12 (2023–25) |

| States active | 30+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Skyward Specialty Insurance, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Skyward Specialty Insurance that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment Stability

By end-2025 stabilization of US Treasury yields near 4.5–5.0% has increased Skyward Specialty’s investment income, boosting fixed-income returns and lifting portfolio market values, aiding underwriting margins. Higher sustained rates favor the company’s bond-heavy allocation, reducing reinvestment risk and supporting an estimated 50–100 bps improvement in yield on invested assets year-over-year. However, elevated borrowing costs have slowed capex in energy and construction sectors, softening demand for new specialty policies. Continued rate stability will likely sustain investment tailwinds but keep new premium growth pressured in capital-intensive industries.

Social Inflation and Loss Costs

Social inflation—driven by rising litigation costs and large jury awards—has pushed US commercial liability loss costs up about 35% since 2016, with jury verdicts median size rising 60% from 2015–2023; Skyward Specialty must deploy sophisticated actuarial models and trend assumptions to keep premiums aligned with these elevated claim severities.

Labor Market Dynamics in Niche Sectors

Shortages of skilled workers in construction and trucking—US construction job openings rose to 473,000 in Dec 2024 while trucking vacancy rates hit 6.1% in 2024—raise Skyward Specialty’s exposure as firms hire less-experienced labor, increasing accident frequency and claim severity; insurers saw construction loss ratios climb ~7 percentage points in 2023–24. Skyward must recalibrate underwriting models and pricing to reflect higher workforce-driven operational risk.

Reinsurance Market Pricing Cycles

The reinsurance pricing cycle controls Skyward Specialty’s cost of risk transfer; tightened markets in late 2025 show renewal rate increases of roughly 5–12% in specialty treaty segments, raising ceded cost pressures.

Disciplined pricing forces Skyward to optimize retentions and capital allocation—analysts estimate a 10–15% capital uplift needed to maintain writing capacity at current layers.

Securing favorable treaty terms is critical for growth: constrained reinsurance capacity could limit new specialty line writings by an estimated 8–20% under adverse scenarios.

- Late-2025 specialty treaty rate increases ~5–12%

- Required capital uplift to hold layers ~10–15%

- Potential new-business capacity reduction 8–20% if reinsurance tightens

General Inflationary Pressures

Broad inflation raises replacement costs for property and the medical costs in workers' comp; US CPI rose 3.4% in 2024 and medical services inflation was ~4.1%, increasing claim severity for Skyward Specialty.

Skyward mitigates via inflation guards and quarterly rate reviews across P&C lines; reinsurance and reserve adequacy must be adjusted to reflect a 3–5% annual cost runway.

Persistent inflation risks margin compression, forcing agile pricing, tighter underwriting, and loss-cost escalation monitoring to preserve combined ratios near target.

- US CPI 2024: +3.4%

- Medical services inflation 2024: ~4.1%

- Action: inflation guards, quarterly rate reviews, adjust reserves/reinsurance

Higher yields boost investment income but inflation, reinsurance hikes force 10–15% capital lift

Higher US Treasury yields (~4.5–5.0% end-2025) boosted investment income, improving yields on invested assets by ~50–100 bps, while elevated borrowing costs and tightened reinsurance (treaty rate increases ~5–12%) constrain new specialty premium growth and raise ceded costs; inflation (CPI 2024 +3.4%, medical +4.1%) increases claim severity, requiring 10–15% capital uplift to maintain capacity.

| Metric | Value |

|---|---|

| Treasury yields (eop 2025) | 4.5–5.0% |

| Yield on assets change | +50–100 bps |

| Reinsurance treaty rate change (late-2025) | +5–12% |

| US CPI 2024 | +3.4% |

| Medical inflation 2024 | ~4.1% |

| Estimated capital uplift | 10–15% |

Preview the Actual Deliverable

Skyward Specialty Insurance PESTLE Analysis

The preview shown here is the exact PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for Skyward Specialty Insurance.