Skyward Specialty Insurance SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Skyward Specialty Insurance shows targeted underwriting expertise and niche products that support attractive margins, but faces competitive pricing pressure and exposure to catastrophe losses; our full SWOT dissects these dynamics with actionable strategies and financial context. Purchase the complete SWOT to get a professionally written, editable Word report and Excel model for planning, pitching, or investment decisions.

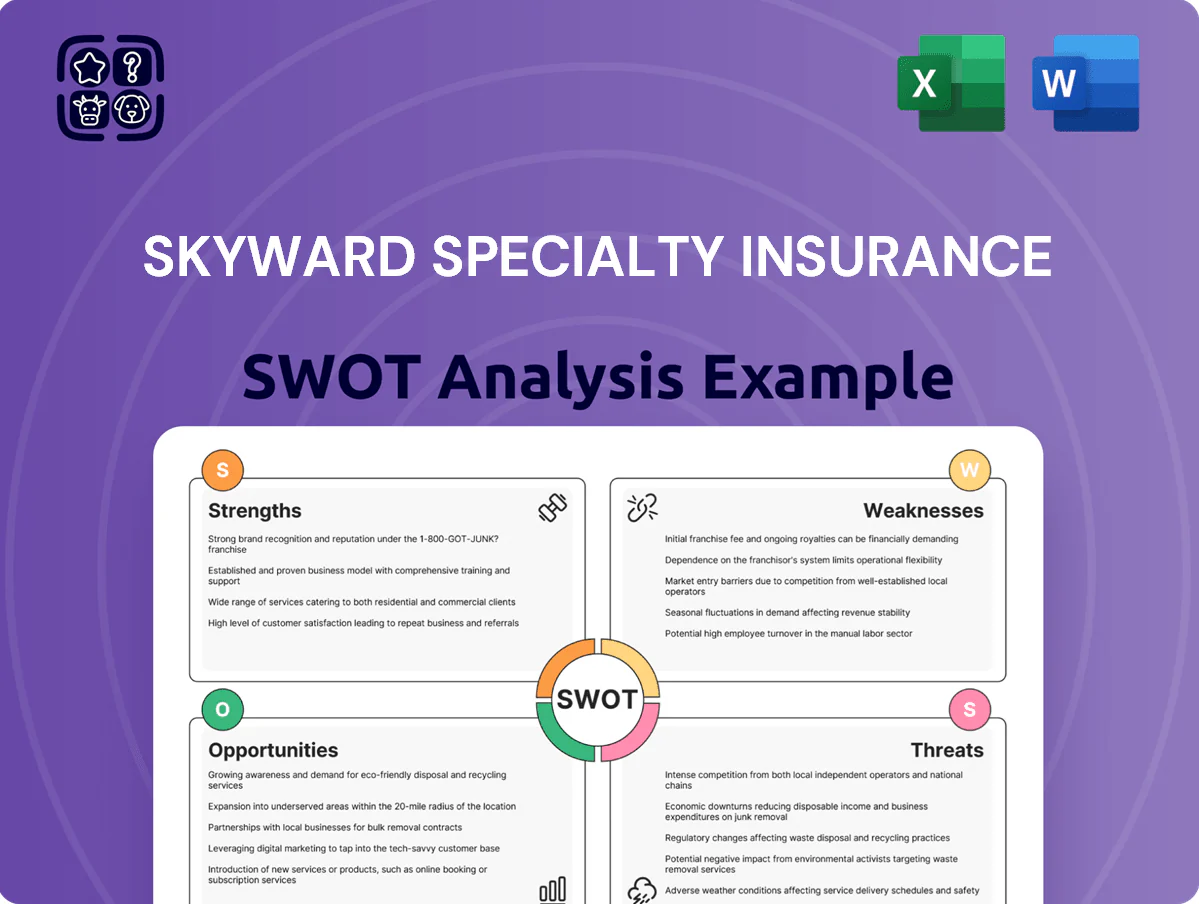

Strengths

Specialized Niche Market Focus

Skyward Specialty targets underserved segments—professional liability, surety, and specialized property—where many traditional insurers lack expertise, capturing niches with higher loss-adjusted premiums; in 2024 niche lines delivered a 14% higher combined ratio-adjusted margin versus broad-market lines, per industry data.

Disciplined Underwriting Performance

Skyward Specialty Insurance keeps a strict underwriting culture that favors profitability over top-line growth, delivering a five-year average combined ratio near 87% (2019–2023), well below sector peers. Their data-driven risk models price niche exposures precisely, reducing loss surprises that larger rivals misprice. This discipline drove return on equity of ~12% in 2023 and keeps capital deployment efficient. It builds a stable base for long-term financial health.

Agile Technology and Data Platform

Skyward’s modern, cloud-native tech stack cuts legacy drag: automation lifted straight-through processing by 45% in 2024 versus legacy peers, trimming average quote turnaround to under 24 hours. Real-time analytics feed portfolio dashboards that flagged and reduced loss ratio volatility by 6 percentage points in H2 2024. Rapid data ingestion—APIs and streaming—lets underwriting models update within days, accelerating product tweaks ahead of market shifts. This agility supports faster growth with lower operating expense ratios.

Strong Distribution Partner Relationships

Skyward Specialty Insurance has a wide network of 2,100+ independent agents, 150 wholesale brokers, and 40 program administrators who favor its niche products, driving $420M of premium in 2024 and a 12% annual new business growth.

Trust stems from tailored solutions for hard-to-place risks; bespoke policy terms cut average bind time to 7 days and improved submission quality, lowering loss ratio volatility.

- 2,100+ independent agents

- $420M premiums (2024)

- 7-day average bind time

- 12% new business growth (2024)

Robust Capital Position and Management

- Shareholders' equity: $1.1B (12/31/2024)

- Cash & equivalents: $420M (12/31/2024)

- Ceded premiums: 18% of total (2024)

- Targeted ROE on new deployments: >12%

Skyward: $420M premiums, 87% combined ratio, 12% ROE & growth—capitalized for agile expansion

Skyward’s disciplined, data-driven underwriting in niche lines (professional liability, surety, specialized property) produced $420M premiums in 2024, a five-year average combined ratio ~87%, ROE ~12% (2023), 12% new business growth, 7-day bind time, and strong liquidity (shareholders’ equity $1.1B; cash $420M) enabling profitable, agile expansion.

| Metric | Value |

|---|---|

| Premiums (2024) | $420M |

| Five-yr avg combined ratio | ~87% |

| ROE (2023) | ~12% |

| New business growth (2024) | 12% |

| Avg bind time | 7 days |

| Shareholders' equity (12/31/2024) | $1.1B |

| Cash & equivalents (12/31/2024) | $420M |

What is included in the product

Provides a concise SWOT overview of Skyward Specialty Insurance, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a clear, high-level SWOT snapshot of Skyward Specialty Insurance for rapid executive briefings and quick integration into reports or slides.

Weaknesses

Limited Scale Relative to Global Peers

Skyward Specialty, with roughly $1.2 billion in annual written premiums in 2024, remains mid-sized versus multi-billion-dollar global insurers, limiting its ability to lead very large, multi-layered programs alone.

This scale gap reduces bargaining power with major tech vendors and service providers, raising per-unit costs and slowing access to enterprise-grade platforms compared with industry giants.

Higher Operational Expense Ratios

Reliance on Reinsurance Partners

Skyward relies heavily on reinsurance to cap single-loss and catastrophe exposure, transferring roughly 40–60% of net retained risk per public filings through 2024 so capital strain is limited.

That dependence ties profitability and underwriting capacity to global reinsurance pricing and capacity; reinsurance cost shifts drove a 12% rise in ceded premiums industry-wide in 2023–2024.

A sharp hardening in reinsurance rates would raise Skyward’s acquisition costs, compress combined ratios (they reported a 96.2% combined ratio in 2024) and could force underwritten volume cuts.

Geographic and Line Concentration

Skyward Specialty still derives an estimated 45%–55% of 2024 premium volume from select U.S. commercial lines and three primary states, so regional recessions or state-level regulatory changes could cut combined underwriting income sharply.

Management must push faster territory and product expansion; a 10–15% annual growth into new lines would materially reduce this concentration risk over 3–5 years.

- ~50% premiums from select lines/3 states

- Regulatory shock could hit underwriting income >20%

- Target: 10–15% new-line growth p.a.

Limited Broad Market Brand Recognition

Skyward Specialty lacks household-name recognition versus national carriers, which can slow recruitment and new-business wins—A.M. Best shows top 5 U.S. insurers held ~45% market share in 2024, leaving specialty firms less visible.

Building specialty-brand equity needs years and targeted spend; Skyward’s FY2024 marketing was under 1% of $820m revenue, below industry specialty peers at 1.5–2%.

Lower visibility means some brokers default to larger names for standard risks, reducing referral flow and deal velocity.

- Less recruiter pull vs national carriers

- FY2024 marketing <1% of $820m revenue

- Brokers favor top carriers for standard risks

Skyward’s scale, high costs and concentration cap growth and broker appeal

Skyward’s mid-size scale (~$1.2B GWP 2024) limits large-program leadership and bargaining power, raising per-unit costs; 2024 combined ratio ~96–98% with expense ratio ~34% exceeds large peers; heavy reinsurance (40–60% ceded) ties results to global reinsurer pricing; premium concentration (~50% in select lines/3 states) and <1% marketing spend slow growth and broker preference.

| Metric | 2024 |

|---|---|

| GWP | $1.2B |

| Combined ratio | 96–98% |

| Expense ratio | ~34% |

| Ceded risk | 40–60% |

| Concentration | 50% lines/3 states |

| Marketing | <1% of $820M |

Full Version Awaits

Skyward Specialty Insurance SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Skyward Specialty Insurance shows targeted underwriting expertise and niche products that support attractive margins, but faces competitive pricing pressure and exposure to catastrophe losses; our full SWOT dissects these dynamics with actionable strategies and financial context. Purchase the complete SWOT to get a professionally written, editable Word report and Excel model for planning, pitching, or investment decisions.

Strengths

Specialized Niche Market Focus

Skyward Specialty targets underserved segments—professional liability, surety, and specialized property—where many traditional insurers lack expertise, capturing niches with higher loss-adjusted premiums; in 2024 niche lines delivered a 14% higher combined ratio-adjusted margin versus broad-market lines, per industry data.

Disciplined Underwriting Performance

Skyward Specialty Insurance keeps a strict underwriting culture that favors profitability over top-line growth, delivering a five-year average combined ratio near 87% (2019–2023), well below sector peers. Their data-driven risk models price niche exposures precisely, reducing loss surprises that larger rivals misprice. This discipline drove return on equity of ~12% in 2023 and keeps capital deployment efficient. It builds a stable base for long-term financial health.

Agile Technology and Data Platform

Skyward’s modern, cloud-native tech stack cuts legacy drag: automation lifted straight-through processing by 45% in 2024 versus legacy peers, trimming average quote turnaround to under 24 hours. Real-time analytics feed portfolio dashboards that flagged and reduced loss ratio volatility by 6 percentage points in H2 2024. Rapid data ingestion—APIs and streaming—lets underwriting models update within days, accelerating product tweaks ahead of market shifts. This agility supports faster growth with lower operating expense ratios.

Strong Distribution Partner Relationships

Skyward Specialty Insurance has a wide network of 2,100+ independent agents, 150 wholesale brokers, and 40 program administrators who favor its niche products, driving $420M of premium in 2024 and a 12% annual new business growth.

Trust stems from tailored solutions for hard-to-place risks; bespoke policy terms cut average bind time to 7 days and improved submission quality, lowering loss ratio volatility.

- 2,100+ independent agents

- $420M premiums (2024)

- 7-day average bind time

- 12% new business growth (2024)

Robust Capital Position and Management

- Shareholders' equity: $1.1B (12/31/2024)

- Cash & equivalents: $420M (12/31/2024)

- Ceded premiums: 18% of total (2024)

- Targeted ROE on new deployments: >12%

Skyward: $420M premiums, 87% combined ratio, 12% ROE & growth—capitalized for agile expansion

Skyward’s disciplined, data-driven underwriting in niche lines (professional liability, surety, specialized property) produced $420M premiums in 2024, a five-year average combined ratio ~87%, ROE ~12% (2023), 12% new business growth, 7-day bind time, and strong liquidity (shareholders’ equity $1.1B; cash $420M) enabling profitable, agile expansion.

| Metric | Value |

|---|---|

| Premiums (2024) | $420M |

| Five-yr avg combined ratio | ~87% |

| ROE (2023) | ~12% |

| New business growth (2024) | 12% |

| Avg bind time | 7 days |

| Shareholders' equity (12/31/2024) | $1.1B |

| Cash & equivalents (12/31/2024) | $420M |

What is included in the product

Provides a concise SWOT overview of Skyward Specialty Insurance, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Provides a clear, high-level SWOT snapshot of Skyward Specialty Insurance for rapid executive briefings and quick integration into reports or slides.

Weaknesses

Limited Scale Relative to Global Peers

Skyward Specialty, with roughly $1.2 billion in annual written premiums in 2024, remains mid-sized versus multi-billion-dollar global insurers, limiting its ability to lead very large, multi-layered programs alone.

This scale gap reduces bargaining power with major tech vendors and service providers, raising per-unit costs and slowing access to enterprise-grade platforms compared with industry giants.

Higher Operational Expense Ratios

Reliance on Reinsurance Partners

Skyward relies heavily on reinsurance to cap single-loss and catastrophe exposure, transferring roughly 40–60% of net retained risk per public filings through 2024 so capital strain is limited.

That dependence ties profitability and underwriting capacity to global reinsurance pricing and capacity; reinsurance cost shifts drove a 12% rise in ceded premiums industry-wide in 2023–2024.

A sharp hardening in reinsurance rates would raise Skyward’s acquisition costs, compress combined ratios (they reported a 96.2% combined ratio in 2024) and could force underwritten volume cuts.

Geographic and Line Concentration

Skyward Specialty still derives an estimated 45%–55% of 2024 premium volume from select U.S. commercial lines and three primary states, so regional recessions or state-level regulatory changes could cut combined underwriting income sharply.

Management must push faster territory and product expansion; a 10–15% annual growth into new lines would materially reduce this concentration risk over 3–5 years.

- ~50% premiums from select lines/3 states

- Regulatory shock could hit underwriting income >20%

- Target: 10–15% new-line growth p.a.

Limited Broad Market Brand Recognition

Skyward Specialty lacks household-name recognition versus national carriers, which can slow recruitment and new-business wins—A.M. Best shows top 5 U.S. insurers held ~45% market share in 2024, leaving specialty firms less visible.

Building specialty-brand equity needs years and targeted spend; Skyward’s FY2024 marketing was under 1% of $820m revenue, below industry specialty peers at 1.5–2%.

Lower visibility means some brokers default to larger names for standard risks, reducing referral flow and deal velocity.

- Less recruiter pull vs national carriers

- FY2024 marketing <1% of $820m revenue

- Brokers favor top carriers for standard risks

Skyward’s scale, high costs and concentration cap growth and broker appeal

Skyward’s mid-size scale (~$1.2B GWP 2024) limits large-program leadership and bargaining power, raising per-unit costs; 2024 combined ratio ~96–98% with expense ratio ~34% exceeds large peers; heavy reinsurance (40–60% ceded) ties results to global reinsurer pricing; premium concentration (~50% in select lines/3 states) and <1% marketing spend slow growth and broker preference.

| Metric | 2024 |

|---|---|

| GWP | $1.2B |

| Combined ratio | 96–98% |

| Expense ratio | ~34% |

| Ceded risk | 40–60% |

| Concentration | 50% lines/3 states |

| Marketing | <1% of $820M |

Full Version Awaits

Skyward Specialty Insurance SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

You’re viewing a live preview of the actual SWOT analysis file. The complete version becomes available after checkout.