Skyworks Solutions Boston Consulting Group Matrix

Actionable Strategy Starts Here

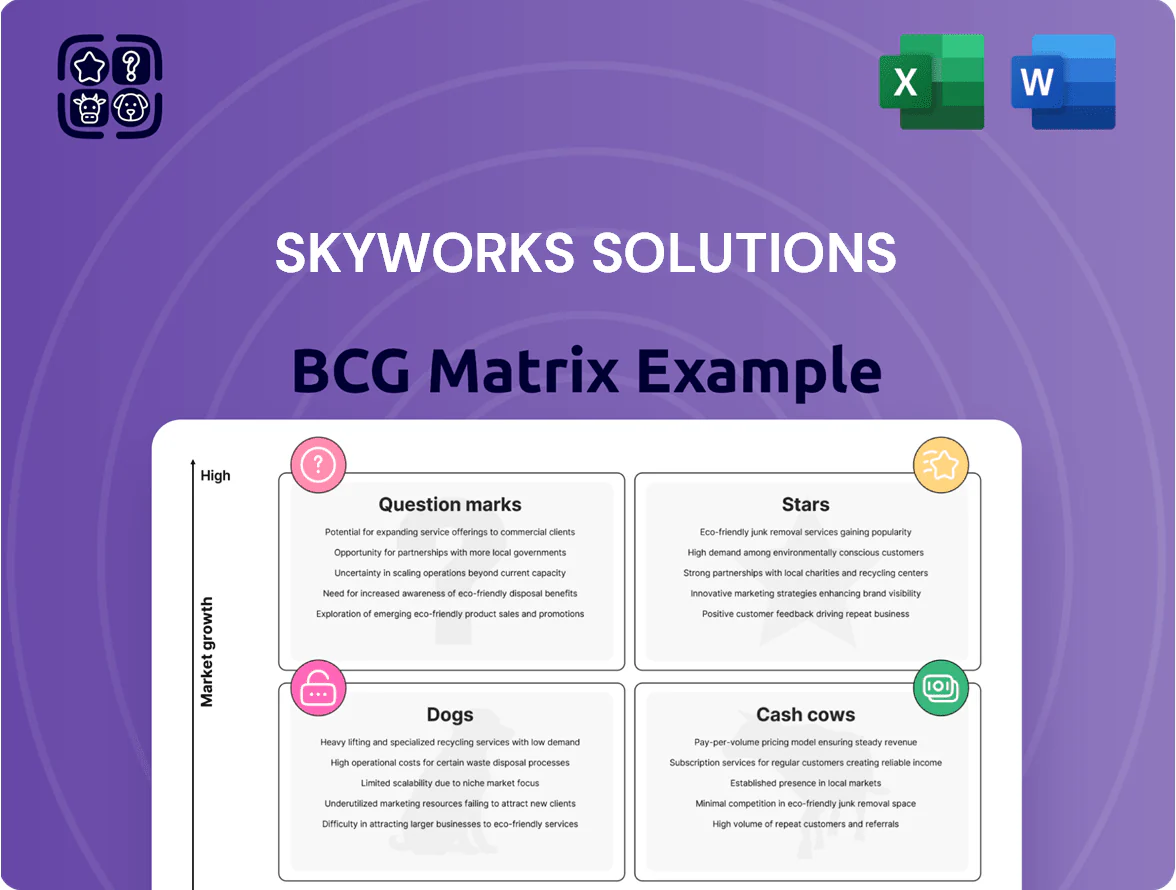

Skyworks Solutions sits at the intersection of high-growth wireless markets and mature connectivity segments; our BCG Matrix preview highlights which product lines act as Stars—driving future growth—and which behave like Cash Cows or Question Marks amid 5G and IoT trends. The full BCG Matrix delivers quadrant-by-quadrant placements, data-backed strategic moves, and capital-allocation guidance to optimize portfolio returns. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that speeds decision-making and execution.

Stars

5G Advanced and RedCap RF Modules

Skyworks remains a dominant leader in the 5G Advanced and Reduced Capability (RedCap) RF module transition, holding an estimated 40–45% share of premium smartphone RF front-end modules in late 2025 while RedCap adoption rises toward 30% of new IoT and mid-tier handset designs.

The modules drive high-margin revenue growth—Skyworks reported RF segment sales of $2.1 billion in FY 2024 and guided increased 2025 R&D to about $450 million to support integrated solutions versus rivals Qorvo and Broadcom.

Heavy R and D spend is required to meet evolving carrier specs and spectral efficiency gains; Skyworks’ 20%+ gross margin on these modules funds advanced carrier aggregation and power amplifier innovations to defend share as mid-tier penetration expands.

Automotive Connectivity and V2X Systems

Skyworks’ automotive connectivity and V2X systems are a rising star: vehicle modules grew at high double-digit rates through 2025, with Skyworks reporting automotive revenue up ~32% YoY to about $1.1B in FY2025 driven by safety and infotainment demand.

Skyworks holds leading share in V2X communication ICs and modules, but rapid EV and AV innovation demands ongoing capital reinvestment—R&D and capex for automotive rose ~28% and 22% respectively in 2024–25.

Once niche, this segment is becoming a core pillar, contributing roughly 18% of company revenue by FY2025 and positioned for continued high-growth if Skyworks keeps pace on integration and certification cycles.

Wi-Fi 7 Integrated Solutions

As Wi‑Fi 7 (IEEE 802.11be) nears mass adoption, Skyworks Solutions holds a leading share in high‑performance routers and access points, powering low‑latency, multi‑Gbps connectivity for spatial computing and 8K streaming; home networking market value is projected to hit ~$45B by 2028 (Grand View Research, 2025).

Advanced Power Management for Mobile

Skyworks Solutions leverages RF expertise to capture ~20–25% share in mobile power-management ICs, addressing high-speed 5G and AI loads that cut battery life by 15–30% per feature set since 2023.

Their analog PMICs optimize voltage regulators and RF front-ends, lifting device efficiency by ~10%—keeping Skyworks as a preferred supplier for flagship OEMs and supporting FY2024 revenue mix where RF+PMICs drove ~40% of segment sales.

- RF-driven PMIC share ~20–25%

- AI features reduce battery life 15–30%

- PMIC efficiency gains ~10%

- RF+PMICs ~40% of FY2024 segment sales

Infrastructure and Small Cell Amplifiers

Skyworks’ Infrastructure and Small Cell Amplifiers sit in a high-growth 5G densification market, with global small cell shipments forecasted to grow ~18% CAGR to 2028 (Omdia 2025); Skyworks supplies high-performance PA and MIMO RF front-ends essential for dense, private enterprise and RAN deployments.

Skyworks holds a leading share in RAN components, capturing macro-to-small-cell migration; strong OEM contracts and a 2025 telecom equipment spend rebound support sustained demand for its specialized chips.

High capital intensity for fab and testing raises barriers; however, robust orders from global telco vendors and private network projects, plus Skyworks’ 2024 revenue exposure to infrastructure (>20%), offset capex risk.

- Market growth: ~18% CAGR to 2028 (Omdia 2025)

- Skyworks infra revenue >20% of 2024 sales

- High-capex barriers reduce competition

- Strong OEM/RAN share drives recurring demand

Skyworks: 5G RF, Auto V2X & PMICs Powering High‑Growth, Margin‑Rich Leadership

Skyworks’ Stars: 5G/RedCap RF modules (40–45% premium smartphone share by late 2025), automotive V2X (FY2025 auto rev ~$1.1B, +32% YoY), Wi‑Fi7/router share, PMICs (20–25% RF‑PMIC share) and infrastructure PAs (infra >20% 2024 revenue) — high growth, strong margins, heavy R&D/capex to defend leadership.

| Segment | 2024–25 |

|---|---|

| RF modules | 40–45% share |

| Automotive | $1.1B, +32% |

| PMICs | 20–25% share |

| Infra | >20% rev |

What is included in the product

BCG Matrix review of Skyworks: quadrant-by-quadrant product analysis with strategic invest/hold/divest guidance and trend-based risks/opportunities.

One-page Skyworks BCG Matrix placing each segment in a quadrant for quick strategic clarity.

Cash Cows

Legacy 4G LTE RF Components

Skyworks’ Legacy 4G LTE RF components remain cash cows: global 4G device shipments were ~1.8 billion units in 2024, and Skyworks holds a leading share in RF front-end for LTE, generating steady revenue—about $1.2B of FY2024 gross profit tied to mature products—while R&D and marketing needs are minimal.

These SKUs run on fully depreciated fabs, lifting gross margins to the mid-40s%; the free cash flow supports investment in 6G research and satellite RF programs, with cash from legacy lines funding a sizable portion of Skyworks’ $400–500M annual strategic tech spend.

Standard Analog and Discrete Components

Skyworks’ standard analog and discrete components—switches, attenuators, diodes—are core building blocks across industrial, automotive, and consumer electronics, holding high market share that management estimates contributes roughly 30–35% of 2025 revenue.

With mature tech and stable end markets, these product lines need minimal maintenance capex (around 3–4% of segment revenue) and deliver predictable gross margins near 40%.

They generate steady free cash flow that underpins Skyworks’ dividend (annualized $0.80 per share in 2025) and sizable share buybacks totaling $1.2B authorized in 2025.

Aerospace and Defense RF Solutions

The aerospace and defense RF segment delivers steady, multi-year contracts for Skyworks (ticker: SWKS), supporting roughly 12–15% of 2025 revenue and typical gross margins above 40%, so it behaves like a cash cow.

High technical barriers, strict qualification cycles, and a mature market give Skyworks a leadership edge and predictable demand, letting the firm extract cash with minimal incremental capex.

Revenue growth here runs low-to-mid single digits annually, insulating margins from smartphone cyclicality and cutting revenue volatility versus the consumer RF business.

Industrial IoT Connectivity

Industrial IoT connectivity—smart meters, factory automation, logistics tracking—provides stable demand and generated roughly $420M in Skyworks Solutions revenue in 2024, making it a reliable cash cow.

Skyworks’ deep, mature wireless portfolio (Wi‑Fi, BLE, NB‑IoT) is widely adopted across industry; protocols’ low growth shifts competition to reliability, helping maintain a ~30% industrial market share.

That stability lets Skyworks allocate R&D and capital toward higher‑growth areas while preserving strong gross margins from industrial products.

- 2024 industrial revenue ≈ $420M

- Approx. 30% industrial market share

- Focus: reliability over rapid innovation

- Funds redirected to speculative growth areas

Smartphone Filter Technology

Skyworks’ smartphone filter tech (SAW/BAW) is a cash cow: market matured, Skyworks holds a significant, stable share, and filters are standard in every handset; IDC reported global smartphone shipments ~1.2B in 2024, supporting steady volume.

Complex tech but optimized manufacturing yields high gross margins—Skyworks reported 2024 gross margin ~45%—and replacement cycles drive recurring revenue and predictable free cash flow.

- Essential in every handset

- Optimized production = high margins (~45% 2024)

- Stable market share, mature demand

- ~1.2B smartphones shipped in 2024 = steady volume

Skyworks’ steady RF cash engine: $1.2B legacy profit funds 6G, satellite bets

Skyworks’ mature RF portfolio (4G LTE, SAW/BAW filters, analog discretes, aerospace/industrial) generated steady cash: FY2024 gross profit ≈ $1.2B; 2024 industrial revenue ≈ $420M; gross margins ~40–45%; funds ~ $400–500M annual R&D and $1.2B buyback auth. These lines yield low single‑digit growth and predictable free cash flow, funding 6G and satellite programs.

| Metric | Value (2024/2025) |

|---|---|

| Gross profit (legacy) | $1.2B (2024) |

| Industrial rev | $420M (2024) |

| Gross margin | 40–45% |

| R&D spend | $400–500M (annual) |

| Buyback auth | $1.2B (2025) |

What You’re Viewing Is Included

Skyworks Solutions BCG Matrix

The file you're previewing on this page is the final Skyworks Solutions BCG Matrix you'll receive after purchase—no watermarks, no demo elements—just a fully formatted, strategy-ready report built for professional use and clear decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Skyworks Solutions sits at the intersection of high-growth wireless markets and mature connectivity segments; our BCG Matrix preview highlights which product lines act as Stars—driving future growth—and which behave like Cash Cows or Question Marks amid 5G and IoT trends. The full BCG Matrix delivers quadrant-by-quadrant placements, data-backed strategic moves, and capital-allocation guidance to optimize portfolio returns. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that speeds decision-making and execution.

Stars

5G Advanced and RedCap RF Modules

Skyworks remains a dominant leader in the 5G Advanced and Reduced Capability (RedCap) RF module transition, holding an estimated 40–45% share of premium smartphone RF front-end modules in late 2025 while RedCap adoption rises toward 30% of new IoT and mid-tier handset designs.

The modules drive high-margin revenue growth—Skyworks reported RF segment sales of $2.1 billion in FY 2024 and guided increased 2025 R&D to about $450 million to support integrated solutions versus rivals Qorvo and Broadcom.

Heavy R and D spend is required to meet evolving carrier specs and spectral efficiency gains; Skyworks’ 20%+ gross margin on these modules funds advanced carrier aggregation and power amplifier innovations to defend share as mid-tier penetration expands.

Automotive Connectivity and V2X Systems

Skyworks’ automotive connectivity and V2X systems are a rising star: vehicle modules grew at high double-digit rates through 2025, with Skyworks reporting automotive revenue up ~32% YoY to about $1.1B in FY2025 driven by safety and infotainment demand.

Skyworks holds leading share in V2X communication ICs and modules, but rapid EV and AV innovation demands ongoing capital reinvestment—R&D and capex for automotive rose ~28% and 22% respectively in 2024–25.

Once niche, this segment is becoming a core pillar, contributing roughly 18% of company revenue by FY2025 and positioned for continued high-growth if Skyworks keeps pace on integration and certification cycles.

Wi-Fi 7 Integrated Solutions

As Wi‑Fi 7 (IEEE 802.11be) nears mass adoption, Skyworks Solutions holds a leading share in high‑performance routers and access points, powering low‑latency, multi‑Gbps connectivity for spatial computing and 8K streaming; home networking market value is projected to hit ~$45B by 2028 (Grand View Research, 2025).

Advanced Power Management for Mobile

Skyworks Solutions leverages RF expertise to capture ~20–25% share in mobile power-management ICs, addressing high-speed 5G and AI loads that cut battery life by 15–30% per feature set since 2023.

Their analog PMICs optimize voltage regulators and RF front-ends, lifting device efficiency by ~10%—keeping Skyworks as a preferred supplier for flagship OEMs and supporting FY2024 revenue mix where RF+PMICs drove ~40% of segment sales.

- RF-driven PMIC share ~20–25%

- AI features reduce battery life 15–30%

- PMIC efficiency gains ~10%

- RF+PMICs ~40% of FY2024 segment sales

Infrastructure and Small Cell Amplifiers

Skyworks’ Infrastructure and Small Cell Amplifiers sit in a high-growth 5G densification market, with global small cell shipments forecasted to grow ~18% CAGR to 2028 (Omdia 2025); Skyworks supplies high-performance PA and MIMO RF front-ends essential for dense, private enterprise and RAN deployments.

Skyworks holds a leading share in RAN components, capturing macro-to-small-cell migration; strong OEM contracts and a 2025 telecom equipment spend rebound support sustained demand for its specialized chips.

High capital intensity for fab and testing raises barriers; however, robust orders from global telco vendors and private network projects, plus Skyworks’ 2024 revenue exposure to infrastructure (>20%), offset capex risk.

- Market growth: ~18% CAGR to 2028 (Omdia 2025)

- Skyworks infra revenue >20% of 2024 sales

- High-capex barriers reduce competition

- Strong OEM/RAN share drives recurring demand

Skyworks: 5G RF, Auto V2X & PMICs Powering High‑Growth, Margin‑Rich Leadership

Skyworks’ Stars: 5G/RedCap RF modules (40–45% premium smartphone share by late 2025), automotive V2X (FY2025 auto rev ~$1.1B, +32% YoY), Wi‑Fi7/router share, PMICs (20–25% RF‑PMIC share) and infrastructure PAs (infra >20% 2024 revenue) — high growth, strong margins, heavy R&D/capex to defend leadership.

| Segment | 2024–25 |

|---|---|

| RF modules | 40–45% share |

| Automotive | $1.1B, +32% |

| PMICs | 20–25% share |

| Infra | >20% rev |

What is included in the product

BCG Matrix review of Skyworks: quadrant-by-quadrant product analysis with strategic invest/hold/divest guidance and trend-based risks/opportunities.

One-page Skyworks BCG Matrix placing each segment in a quadrant for quick strategic clarity.

Cash Cows

Legacy 4G LTE RF Components

Skyworks’ Legacy 4G LTE RF components remain cash cows: global 4G device shipments were ~1.8 billion units in 2024, and Skyworks holds a leading share in RF front-end for LTE, generating steady revenue—about $1.2B of FY2024 gross profit tied to mature products—while R&D and marketing needs are minimal.

These SKUs run on fully depreciated fabs, lifting gross margins to the mid-40s%; the free cash flow supports investment in 6G research and satellite RF programs, with cash from legacy lines funding a sizable portion of Skyworks’ $400–500M annual strategic tech spend.

Standard Analog and Discrete Components

Skyworks’ standard analog and discrete components—switches, attenuators, diodes—are core building blocks across industrial, automotive, and consumer electronics, holding high market share that management estimates contributes roughly 30–35% of 2025 revenue.

With mature tech and stable end markets, these product lines need minimal maintenance capex (around 3–4% of segment revenue) and deliver predictable gross margins near 40%.

They generate steady free cash flow that underpins Skyworks’ dividend (annualized $0.80 per share in 2025) and sizable share buybacks totaling $1.2B authorized in 2025.

Aerospace and Defense RF Solutions

The aerospace and defense RF segment delivers steady, multi-year contracts for Skyworks (ticker: SWKS), supporting roughly 12–15% of 2025 revenue and typical gross margins above 40%, so it behaves like a cash cow.

High technical barriers, strict qualification cycles, and a mature market give Skyworks a leadership edge and predictable demand, letting the firm extract cash with minimal incremental capex.

Revenue growth here runs low-to-mid single digits annually, insulating margins from smartphone cyclicality and cutting revenue volatility versus the consumer RF business.

Industrial IoT Connectivity

Industrial IoT connectivity—smart meters, factory automation, logistics tracking—provides stable demand and generated roughly $420M in Skyworks Solutions revenue in 2024, making it a reliable cash cow.

Skyworks’ deep, mature wireless portfolio (Wi‑Fi, BLE, NB‑IoT) is widely adopted across industry; protocols’ low growth shifts competition to reliability, helping maintain a ~30% industrial market share.

That stability lets Skyworks allocate R&D and capital toward higher‑growth areas while preserving strong gross margins from industrial products.

- 2024 industrial revenue ≈ $420M

- Approx. 30% industrial market share

- Focus: reliability over rapid innovation

- Funds redirected to speculative growth areas

Smartphone Filter Technology

Skyworks’ smartphone filter tech (SAW/BAW) is a cash cow: market matured, Skyworks holds a significant, stable share, and filters are standard in every handset; IDC reported global smartphone shipments ~1.2B in 2024, supporting steady volume.

Complex tech but optimized manufacturing yields high gross margins—Skyworks reported 2024 gross margin ~45%—and replacement cycles drive recurring revenue and predictable free cash flow.

- Essential in every handset

- Optimized production = high margins (~45% 2024)

- Stable market share, mature demand

- ~1.2B smartphones shipped in 2024 = steady volume

Skyworks’ steady RF cash engine: $1.2B legacy profit funds 6G, satellite bets

Skyworks’ mature RF portfolio (4G LTE, SAW/BAW filters, analog discretes, aerospace/industrial) generated steady cash: FY2024 gross profit ≈ $1.2B; 2024 industrial revenue ≈ $420M; gross margins ~40–45%; funds ~ $400–500M annual R&D and $1.2B buyback auth. These lines yield low single‑digit growth and predictable free cash flow, funding 6G and satellite programs.

| Metric | Value (2024/2025) |

|---|---|

| Gross profit (legacy) | $1.2B (2024) |

| Industrial rev | $420M (2024) |

| Gross margin | 40–45% |

| R&D spend | $400–500M (annual) |

| Buyback auth | $1.2B (2025) |

What You’re Viewing Is Included

Skyworks Solutions BCG Matrix

The file you're previewing on this page is the final Skyworks Solutions BCG Matrix you'll receive after purchase—no watermarks, no demo elements—just a fully formatted, strategy-ready report built for professional use and clear decision-making.