Skyworks Solutions Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

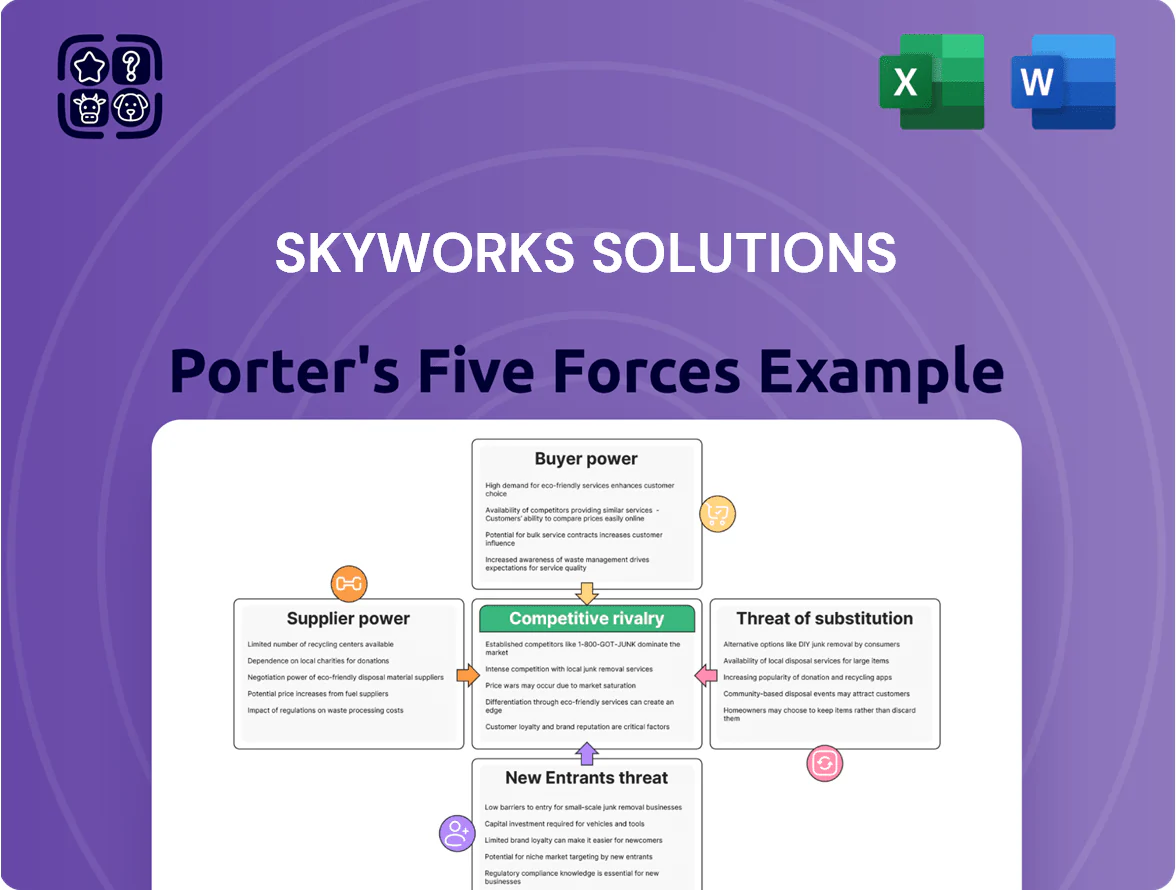

Skyworks Solutions faces intense rivalry from semiconductor peers, strong buyer bargaining from major OEMs, and moderate supplier power due to specialized RF components, while barriers to entry remain high and substitute threats are manageable given its tech moat.

Suppliers Bargaining Power

Dependence on specialized semiconductor foundries

Skyworks depends on external foundries such as TSMC and GlobalFoundries for advanced CMOS wafers; in 2024 roughly 25–35% of its production came from external fabs, concentrating supplier risk.

These foundries command pricing power due to constrained advanced-node capacity and complex process expertise; TSMC’s 2024 capital expenditure was about $36–40 billion, signaling tight supply versus rising demand.

If foundries raise prices or suffer delays, Skyworks has few short-term substitutes, which would compress gross margins (Skyworks’ 2024 gross margin was ~45%) and disrupt delivery schedules.

Sourcing of critical raw materials and substrates

Suppliers of gallium arsenide (GaAs) and specialized piezoelectric substrates are few, giving them moderate bargaining power over Skyworks Solutions; GaAs wafer market had ~USD 2.1 billion revenue in 2024, with top vendors controlling ~60%.

Price moves or allocation shifts can raise Skyworks’ COGS and hurt margins—Skyworks reported gross margin 38.4% in FY2024—while supply disruption could halt production for mobile and automotive RF modules.

High switching costs for manufacturing equipment

Skyworks relies on specialized lithography and test kit from a tiny group—ASML and Applied Materials—whose EUV and advanced etch tools cost $100M+ per system and have 12–36 month lead times, so switching would force massive capital outlays; this dependence raises supplier power for maintenance, spare parts, and node upgrades, and contributed to industry-wide capex concentration where top 3 suppliers control ~70% of advanced tool market in 2024.

Intellectual property and software licensing

Skyworks relies on third-party IP cores and electronic design automation (EDA) tools, with vendors exerting leverage via restrictive licenses and switching costs; industry surveys show EDA and IP licensing can account for 3–6% of semiconductor R&D spend—roughly $40–80 million annually if Skyworks’ 2024 R&D was ~$1.3 billion.

That dependency forces recurring licensing and maintenance fees, limits negotiating room, and ties part of operating budget to vendor terms, raising supplier bargaining power.

- 3–6% of R&D spend on IP/EDA (~$40–80M, based on 2024 R&D $1.3B)

- High switching costs from proprietary ecosystems

- Restrictive contracts limit price/usage flexibility

Consolidation within the global supply chain

The semiconductor supply chain has consolidated: top OSATs (outsourced assembly and test) like ASE Technology, Amkor, and JCET control ~50–60% of global packaging/assembly capacity as of 2025, raising their leverage over chip designers such as Skyworks Solutions.

As OSATs grew via M&A, they can push pricing and lead-time terms; Skyworks now often signs multi-year volume commitments to secure backend capacity across its RF, analog, and mixed-signal product lines.

Long-term contracts shift risk: Skyworks assumes volume and inventory exposure to guarantee priority access during shortages, affecting working capital and margin flexibility.

- Top 3 OSAT share ~40%–60% (2025)

- Multi-year contracts common (3–5 years)

- Increased cost exposure to guaranteed volumes

- Higher bargaining power reduces Skyworks' supplier flexibility

Supplier concentration lifts COGS & margin risk — foundries, toolmakers, OSATs dominate

Suppliers hold moderate-to-high power: leading foundries (TSMC capex $36–40B in 2024) and toolmakers (ASML/Applied control ~70% of advanced tools) constrain capacity; GaAs suppliers and top OSATs (top 3 ~50–60% capacity in 2025) limit alternatives, raising COGS and margin risk (Skyworks gross margin ~38–45% in 2024). Long-term contracts and EDA/IP fees (~$40–80M) increase switching costs.

| Metric | Value |

|---|---|

| TSMC capex 2024 | $36–40B |

| Skyworks gross margin 2024 | ~38–45% |

| GaAs market 2024 | $2.1B (top vendors ~60%) |

| Top OSAT share 2025 | ~50–60% |

| EDA/IP spend est. | $40–80M |

What is included in the product

Tailored Porter's Five Forces analysis for Skyworks Solutions, uncovering competitive intensity, customer and supplier bargaining power, threat of substitutes, and entry barriers to reveal strategic vulnerabilities and growth levers.

One-sheet Porter's Five Forces for Skyworks—quickly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Significant revenue concentration from Apple

About 30% of Skyworks Solutions’ FY2024 revenue came from Apple, giving Apple outsized negotiating power to push prices down and demand strict performance and qualification terms.

That concentration means Apple can pressure Skyworks on margins and lead times; if Apple shifts suppliers or builds in-house RF chips, Skyworks faces a potentially material revenue hit and margin compression.

Price pressure from large smartphone OEMs

Large OEMs like Samsung and Xiaomi buy at scale and face slim device margins—global smartphone ASP fell to about $320 in 2024, so they push suppliers hard.

These buyers routinely pit RF component vendors against each other to shave 5–15% off BOMs for flagship and mid-range models.

Skyworks must fund R&D—R&D was $526m in FY2024—to keep differentiated chips; otherwise it risks volume losses to lower-cost rivals.

Shift toward in-house chip design by tech giants

Large tech firms increasingly design proprietary silicon to boost HW-SW fit; Apple’s 2024 A17 modem move and Google’s Tensor updates cut third-party RF scope. If Apple/Google internalize RF front-ends, Skyworks’ $6.8B addressable RF market (2024 estimate) could shrink materially. Skyworks must shift to higher-value integrated RF systems and software-enabled modules that raise replication cost and keep switching friction high.

Adoption of standardized connectivity modules

In IoT and industrial markets, adoption of standardized off-the-shelf connectivity modules raises customer bargaining power by enabling easy vendor switches based on price and supply; alternative-module shipments grew ~18% YoY in 2024 per industry tracker.

Skyworks defends pricing by targeting high-performance segments—custom RF front-ends and power-efficient ICs—where customers pay premiums; Skyworks reported 2024 adj. gross margin ~47% supporting this focus.

- Standard modules ↑ switchability, pressure on prices

- Alt-module shipments +18% in 2024

- Skyworks targets custom, high-efficiency RF

- 2024 adj. gross margin ~47%

Cyclical demand and inventory management

Customers in automotive and infrastructure place large, lumpy orders tied to cycles; Skyworks saw automotive revenue swing by ~±20% year-over-year in 2023–2024, amplifying order volatility.

When end demand slows, buyers can delay or cancel, forcing Skyworks to hold excess inventory; inventory rose to $1.2bn at end-2024, increasing carrying costs and margin pressure.

To manage this, Skyworks keeps flexible fabs and backlog management; shorter cycle lines and dual-sourcing helped cut lead-time variance by ~30% in 2024.

- Large, lumpy orders linked to macro cycles

- Order cancellations drive excess inventory: $1.2bn end-2024

- Revenue swings ~±20% in auto 2023–24

- Flexible fabs, dual-sourcing, 30% lower lead-time variance

Skyworks faces customer power and internalization risks despite strong margins

Customers wield high bargaining power: Apple drove ~30% of FY2024 revenue, enabling price and spec leverage; large OEMs pushed RF BOM cuts of ~5–15% as smartphone ASP fell to ~$320 in 2024. Skyworks’ R&D spend $526m and adj. gross margin ~47% defend value, but risks rise as Apple/Google internalize RF and alt-module shipments grew ~18% YoY. Inventory hit $1.2bn end-2024; auto revenue swung ~±20% in 2023–24.

| Metric | 2024 |

|---|---|

| Apple revenue share | ~30% |

| R&D | $526m |

| Adj. gross margin | ~47% |

| Smartphone ASP | $320 |

| Alt-module shipments YoY | +18% |

| Inventory | $1.2bn |

| Auto rev volatility | ±20% |

Preview Before You Purchase

Skyworks Solutions Porter's Five Forces Analysis

This preview shows the exact Skyworks Solutions Porter’s Five Forces analysis you'll receive upon purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file you’ll be able to download instantly after payment and use immediately.

You're viewing the final deliverable: a ready-to-use strategic assessment of Skyworks Solutions that matches the purchased document exactly.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Skyworks Solutions faces intense rivalry from semiconductor peers, strong buyer bargaining from major OEMs, and moderate supplier power due to specialized RF components, while barriers to entry remain high and substitute threats are manageable given its tech moat.

Suppliers Bargaining Power

Dependence on specialized semiconductor foundries

Skyworks depends on external foundries such as TSMC and GlobalFoundries for advanced CMOS wafers; in 2024 roughly 25–35% of its production came from external fabs, concentrating supplier risk.

These foundries command pricing power due to constrained advanced-node capacity and complex process expertise; TSMC’s 2024 capital expenditure was about $36–40 billion, signaling tight supply versus rising demand.

If foundries raise prices or suffer delays, Skyworks has few short-term substitutes, which would compress gross margins (Skyworks’ 2024 gross margin was ~45%) and disrupt delivery schedules.

Sourcing of critical raw materials and substrates

Suppliers of gallium arsenide (GaAs) and specialized piezoelectric substrates are few, giving them moderate bargaining power over Skyworks Solutions; GaAs wafer market had ~USD 2.1 billion revenue in 2024, with top vendors controlling ~60%.

Price moves or allocation shifts can raise Skyworks’ COGS and hurt margins—Skyworks reported gross margin 38.4% in FY2024—while supply disruption could halt production for mobile and automotive RF modules.

High switching costs for manufacturing equipment

Skyworks relies on specialized lithography and test kit from a tiny group—ASML and Applied Materials—whose EUV and advanced etch tools cost $100M+ per system and have 12–36 month lead times, so switching would force massive capital outlays; this dependence raises supplier power for maintenance, spare parts, and node upgrades, and contributed to industry-wide capex concentration where top 3 suppliers control ~70% of advanced tool market in 2024.

Intellectual property and software licensing

Skyworks relies on third-party IP cores and electronic design automation (EDA) tools, with vendors exerting leverage via restrictive licenses and switching costs; industry surveys show EDA and IP licensing can account for 3–6% of semiconductor R&D spend—roughly $40–80 million annually if Skyworks’ 2024 R&D was ~$1.3 billion.

That dependency forces recurring licensing and maintenance fees, limits negotiating room, and ties part of operating budget to vendor terms, raising supplier bargaining power.

- 3–6% of R&D spend on IP/EDA (~$40–80M, based on 2024 R&D $1.3B)

- High switching costs from proprietary ecosystems

- Restrictive contracts limit price/usage flexibility

Consolidation within the global supply chain

The semiconductor supply chain has consolidated: top OSATs (outsourced assembly and test) like ASE Technology, Amkor, and JCET control ~50–60% of global packaging/assembly capacity as of 2025, raising their leverage over chip designers such as Skyworks Solutions.

As OSATs grew via M&A, they can push pricing and lead-time terms; Skyworks now often signs multi-year volume commitments to secure backend capacity across its RF, analog, and mixed-signal product lines.

Long-term contracts shift risk: Skyworks assumes volume and inventory exposure to guarantee priority access during shortages, affecting working capital and margin flexibility.

- Top 3 OSAT share ~40%–60% (2025)

- Multi-year contracts common (3–5 years)

- Increased cost exposure to guaranteed volumes

- Higher bargaining power reduces Skyworks' supplier flexibility

Supplier concentration lifts COGS & margin risk — foundries, toolmakers, OSATs dominate

Suppliers hold moderate-to-high power: leading foundries (TSMC capex $36–40B in 2024) and toolmakers (ASML/Applied control ~70% of advanced tools) constrain capacity; GaAs suppliers and top OSATs (top 3 ~50–60% capacity in 2025) limit alternatives, raising COGS and margin risk (Skyworks gross margin ~38–45% in 2024). Long-term contracts and EDA/IP fees (~$40–80M) increase switching costs.

| Metric | Value |

|---|---|

| TSMC capex 2024 | $36–40B |

| Skyworks gross margin 2024 | ~38–45% |

| GaAs market 2024 | $2.1B (top vendors ~60%) |

| Top OSAT share 2025 | ~50–60% |

| EDA/IP spend est. | $40–80M |

What is included in the product

Tailored Porter's Five Forces analysis for Skyworks Solutions, uncovering competitive intensity, customer and supplier bargaining power, threat of substitutes, and entry barriers to reveal strategic vulnerabilities and growth levers.

One-sheet Porter's Five Forces for Skyworks—quickly spot supplier, buyer, and competitive pressures to streamline strategic decisions.

Customers Bargaining Power

Significant revenue concentration from Apple

About 30% of Skyworks Solutions’ FY2024 revenue came from Apple, giving Apple outsized negotiating power to push prices down and demand strict performance and qualification terms.

That concentration means Apple can pressure Skyworks on margins and lead times; if Apple shifts suppliers or builds in-house RF chips, Skyworks faces a potentially material revenue hit and margin compression.

Price pressure from large smartphone OEMs

Large OEMs like Samsung and Xiaomi buy at scale and face slim device margins—global smartphone ASP fell to about $320 in 2024, so they push suppliers hard.

These buyers routinely pit RF component vendors against each other to shave 5–15% off BOMs for flagship and mid-range models.

Skyworks must fund R&D—R&D was $526m in FY2024—to keep differentiated chips; otherwise it risks volume losses to lower-cost rivals.

Shift toward in-house chip design by tech giants

Large tech firms increasingly design proprietary silicon to boost HW-SW fit; Apple’s 2024 A17 modem move and Google’s Tensor updates cut third-party RF scope. If Apple/Google internalize RF front-ends, Skyworks’ $6.8B addressable RF market (2024 estimate) could shrink materially. Skyworks must shift to higher-value integrated RF systems and software-enabled modules that raise replication cost and keep switching friction high.

Adoption of standardized connectivity modules

In IoT and industrial markets, adoption of standardized off-the-shelf connectivity modules raises customer bargaining power by enabling easy vendor switches based on price and supply; alternative-module shipments grew ~18% YoY in 2024 per industry tracker.

Skyworks defends pricing by targeting high-performance segments—custom RF front-ends and power-efficient ICs—where customers pay premiums; Skyworks reported 2024 adj. gross margin ~47% supporting this focus.

- Standard modules ↑ switchability, pressure on prices

- Alt-module shipments +18% in 2024

- Skyworks targets custom, high-efficiency RF

- 2024 adj. gross margin ~47%

Cyclical demand and inventory management

Customers in automotive and infrastructure place large, lumpy orders tied to cycles; Skyworks saw automotive revenue swing by ~±20% year-over-year in 2023–2024, amplifying order volatility.

When end demand slows, buyers can delay or cancel, forcing Skyworks to hold excess inventory; inventory rose to $1.2bn at end-2024, increasing carrying costs and margin pressure.

To manage this, Skyworks keeps flexible fabs and backlog management; shorter cycle lines and dual-sourcing helped cut lead-time variance by ~30% in 2024.

- Large, lumpy orders linked to macro cycles

- Order cancellations drive excess inventory: $1.2bn end-2024

- Revenue swings ~±20% in auto 2023–24

- Flexible fabs, dual-sourcing, 30% lower lead-time variance

Skyworks faces customer power and internalization risks despite strong margins

Customers wield high bargaining power: Apple drove ~30% of FY2024 revenue, enabling price and spec leverage; large OEMs pushed RF BOM cuts of ~5–15% as smartphone ASP fell to ~$320 in 2024. Skyworks’ R&D spend $526m and adj. gross margin ~47% defend value, but risks rise as Apple/Google internalize RF and alt-module shipments grew ~18% YoY. Inventory hit $1.2bn end-2024; auto revenue swung ~±20% in 2023–24.

| Metric | 2024 |

|---|---|

| Apple revenue share | ~30% |

| R&D | $526m |

| Adj. gross margin | ~47% |

| Smartphone ASP | $320 |

| Alt-module shipments YoY | +18% |

| Inventory | $1.2bn |

| Auto rev volatility | ±20% |

Preview Before You Purchase

Skyworks Solutions Porter's Five Forces Analysis

This preview shows the exact Skyworks Solutions Porter’s Five Forces analysis you'll receive upon purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file you’ll be able to download instantly after payment and use immediately.

You're viewing the final deliverable: a ready-to-use strategic assessment of Skyworks Solutions that matches the purchased document exactly.