Skyworth Porter's Five Forces Analysis

Don't Miss the Bigger Picture

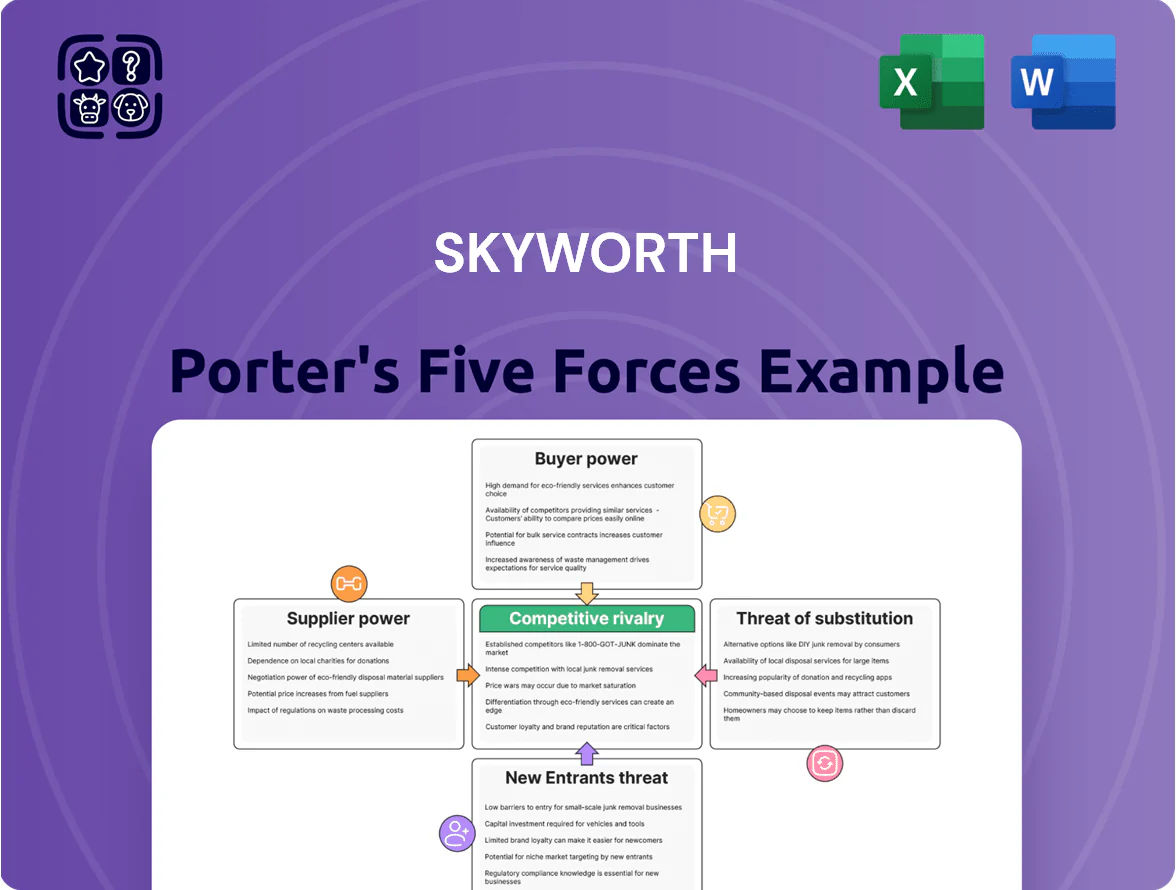

Skyworth faces intense rivalry from global TV and appliance brands, shifting buyer power amid commoditization, and moderate supplier leverage for key components; new entrants and substitutes pose ongoing threats as streaming and smart-home convergence reshape demand.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Skyworth’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Display Panel Manufacturers

The high-end OLED and LCD panel market is concentrated among a few suppliers—BOE Technology Group and LG Display lead with combined capacity >60% for large TV panels in 2025—so Skyworth faces strong supplier power. Panels account for roughly 40–55% of TV BOM (bill of materials), so price swings erode gross margins quickly; a 10% panel price rise cuts gross margin by ~4–5 percentage points. As of late 2025, production delays at any major panel maker have caused TV shipment shortfalls up to 20% in industry reports, directly risking Skyworth’s delivery timelines and margins.

Critical Semiconductor and Chipset Dependency

Skyworth’s move into AI-enabled smart appliances raises dependence on advanced semiconductors, with image-processor and connectivity chips accounting for an estimated 18–25% of BOM (bill of materials) in premium TV and fridge models in 2024.

Specialized suppliers like MediaTek and Qualcomm hold pricing power; spot wafer shortages in 2023 pushed chip prices up 20–35%, squeezing OEM margins.

During 2022–24 geopolitical export curbs, supply constraints lengthened lead times by 30–50%, giving chipmakers leverage to prioritize large clients and demand premium terms.

Raw Material Price Volatility

Vertical Integration Strategy

Skyworth has reduced supplier power by investing in in-house component and display module production, lowering external procurement for key parts to about 35% of inputs in 2024 versus ~50% in 2019, per company filings.

This vertical integration cut exposure to vendor price spikes, improved gross margin by ~1.2 percentage points in FY2024, and raised supply-chain resilience during 2023–24 panel shortages.

- In-house parts = ~35% of inputs (2024)

- Gross margin uplift ≈ +1.2 pp (FY2024)

- Reduced vendor dependency vs 2019 (~50% external)

Logistics and Energy Costs

Suppliers of transportation and energy services significantly affect Skyworth’s landed cost for heavy appliances; average sea freight rates rose 18% in 2025 while bunker fuel surcharges climbed 12% year-on-year.

Greener logistics regulations in 2025 pushed carriers to pass compliance costs—estimated at $25–$40 per TEU—raising per-unit transport for large appliances.

Skyworth faces limited negotiation power because only a few reliable global logistics partners exist, making these cost increases largely non-negotiable.

- Sea freight +18% in 2025

- Bunker surcharges +12% YoY

- Compliance cost $25–$40 per TEU

- Few reliable global carriers → low bargaining power

Supplier dominance: Panels & chips squeeze margins as costs and freight surge

Suppliers have high power: top panel makers (BOE, LGD) hold >60% large-panel capacity (2025), panels are 40–55% of BOM so a 10% panel price rise cuts gross margin ~4–5 pp; chips = 18–25% of BOM with MediaTek/Qualcomm pricing power; in‑house sourcing rose to ~35% (2024) from 50% external (2019), lifting gross margin ~1.2 pp; sea freight +18% (2025), bunker +12% YoY.

| Metric | Value |

|---|---|

| Panel share (suppliers) | >60% |

| Panel % of BOM | 40–55% |

| Chip % of BOM | 18–25% |

| In-house inputs (2024) | ~35% |

| Gross margin uplift | +1.2 pp (FY2024) |

| Sea freight (2025) | +18% |

What is included in the product

Tailored exclusively for Skyworth, this Porter’s Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

Clear, one-sheet Porter’s Five Forces for Skyworth—quickly spot competitive pressures and relieve decision-making friction.

Customers Bargaining Power

Price Sensitivity in Mid-Range Markets

Price sensitivity in mid-range consumer electronics is high: global price elasticity estimates show 1.2–1.6 for TVs and set-top boxes, so a 10% price cut can raise volume ~12–16%. In 2024 Skyworth’s APAC mid-range segment saw average selling price (ASP) fall 6% year-over-year, while online price comparison platforms list >30 competing SKUs within ±10% of Skyworth’s prices, forcing aggressive pricing to protect share.

Low Switching Costs for Consumers

Individual buyers face near-zero financial cost when switching TV or washing machine brands; in 2024 global replacement purchases rose 3.1% while average unit prices fell 2.4%, lowering upgrade friction.

Cross-platform apps and protocols like Wi‑Fi, Matter (2022 standard adoption up 38% in 2024), and Bluetooth mean devices interoperate, cutting ecosystem lock‑in.

That reduced barrier gives customers leverage to demand higher specs and better after‑sales service; 62% of surveyed EU buyers in 2024 cited service quality as a top buying factor.

Dominance of E-commerce Platforms

Large e-commerce giants like Alibaba Group and JD.com wield strong bargaining power over manufacturers; in 2024 Alibaba's Tmall and Taobao accounted for roughly 55% of China online retail GMV and JD.com about 20%, letting platforms dictate shelf visibility and fees.

These platforms can force deep discounts and require participation in big events—Alibaba's Singles Day 2024 promotions drove >100 billion RMB in merchant-supported discounts—pressuring margins.

Skyworth depends on online channels for a majority of domestic TV sales (est. >50% in 2024), so platform terms strongly shape pricing, promotion cadence, and contract leverage.

Demand for Ecosystem Interoperability

Demand for ecosystem interoperability is rising: 68% of global smart-home buyers in 2024 prefer devices compatible with Matter or leading proprietary platforms like Xiaomi and Huawei, so Skyworth risks losing customers if it lacks broad integration.

To retain market share Skyworth must boost software spend—industry peers allocate 8–12% of revenue to R&D for connectivity; falling short will push users to better-integrated brands.

- 68% prefer compatible devices (2024)

- Peers spend 8–12% revenue on connectivity R&D

- Lack of integration risks rapid customer churn

Corporate and OEM Partner Influence

A large share of Skyworths 2024 revenue—about 38% per company filings—comes from B2B OEM/ODM deals where buyers demand high volumes and push margins down, squeezing Skyworths gross margin versus retail lines.

Major corporate clients place bulk orders and can negotiate thin per-unit margins in exchange for scale; losing one big OEM contract could cut manufacturing utilization and revenue by double-digit percentages.

Here’s the quick math: a 10% client loss could lower revenue ~3–6% and drop factory utilization proportionally, raising per-unit costs and hurting margins.

- 2024: ~38% revenue from OEM/ODM

- Bulk orders → lower margins

- Single major contract loss → double-digit utilization hit

- 10% client loss ≈ 3–6% revenue decline

Skyworth under margin pressure: price-sensitive market, platform dominance, and R&D gap

Customers hold strong bargaining power: high price sensitivity (TV/set-top price elasticity 1.2–1.6), APAC ASP down 6% in 2024, and >30 competing SKUs within ±10% of Skyworth pricing. Platforms (Alibaba ~55% GMV, JD.com ~20% in China 2024) and 38% OEM/ODM revenue share force discounts and thin margins; a 10% client loss ≈ 3–6% revenue hit. 68% of buyers want Matter/compatibility; peers spend 8–12% revenue on connectivity R&D.

| Metric | 2024 |

|---|---|

| APAC mid-range ASP change | -6% |

| TV price elasticity | 1.2–1.6 |

| Alibaba share (China online GMV) | ~55% |

| JD.com share | ~20% |

| Revenue from OEM/ODM | ~38% |

| Buyers preferring Matter/compatibility | 68% |

| Peer connectivity R&D spend | 8–12% rev |

Preview the Actual Deliverable

Skyworth Porter's Five Forces Analysis

This preview shows the exact Skyworth Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy.

No mockups, no samples: this is the professionally written, fully formatted analysis file you’ll have instant access to upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Skyworth faces intense rivalry from global TV and appliance brands, shifting buyer power amid commoditization, and moderate supplier leverage for key components; new entrants and substitutes pose ongoing threats as streaming and smart-home convergence reshape demand.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Skyworth’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Display Panel Manufacturers

The high-end OLED and LCD panel market is concentrated among a few suppliers—BOE Technology Group and LG Display lead with combined capacity >60% for large TV panels in 2025—so Skyworth faces strong supplier power. Panels account for roughly 40–55% of TV BOM (bill of materials), so price swings erode gross margins quickly; a 10% panel price rise cuts gross margin by ~4–5 percentage points. As of late 2025, production delays at any major panel maker have caused TV shipment shortfalls up to 20% in industry reports, directly risking Skyworth’s delivery timelines and margins.

Critical Semiconductor and Chipset Dependency

Skyworth’s move into AI-enabled smart appliances raises dependence on advanced semiconductors, with image-processor and connectivity chips accounting for an estimated 18–25% of BOM (bill of materials) in premium TV and fridge models in 2024.

Specialized suppliers like MediaTek and Qualcomm hold pricing power; spot wafer shortages in 2023 pushed chip prices up 20–35%, squeezing OEM margins.

During 2022–24 geopolitical export curbs, supply constraints lengthened lead times by 30–50%, giving chipmakers leverage to prioritize large clients and demand premium terms.

Raw Material Price Volatility

Vertical Integration Strategy

Skyworth has reduced supplier power by investing in in-house component and display module production, lowering external procurement for key parts to about 35% of inputs in 2024 versus ~50% in 2019, per company filings.

This vertical integration cut exposure to vendor price spikes, improved gross margin by ~1.2 percentage points in FY2024, and raised supply-chain resilience during 2023–24 panel shortages.

- In-house parts = ~35% of inputs (2024)

- Gross margin uplift ≈ +1.2 pp (FY2024)

- Reduced vendor dependency vs 2019 (~50% external)

Logistics and Energy Costs

Suppliers of transportation and energy services significantly affect Skyworth’s landed cost for heavy appliances; average sea freight rates rose 18% in 2025 while bunker fuel surcharges climbed 12% year-on-year.

Greener logistics regulations in 2025 pushed carriers to pass compliance costs—estimated at $25–$40 per TEU—raising per-unit transport for large appliances.

Skyworth faces limited negotiation power because only a few reliable global logistics partners exist, making these cost increases largely non-negotiable.

- Sea freight +18% in 2025

- Bunker surcharges +12% YoY

- Compliance cost $25–$40 per TEU

- Few reliable global carriers → low bargaining power

Supplier dominance: Panels & chips squeeze margins as costs and freight surge

Suppliers have high power: top panel makers (BOE, LGD) hold >60% large-panel capacity (2025), panels are 40–55% of BOM so a 10% panel price rise cuts gross margin ~4–5 pp; chips = 18–25% of BOM with MediaTek/Qualcomm pricing power; in‑house sourcing rose to ~35% (2024) from 50% external (2019), lifting gross margin ~1.2 pp; sea freight +18% (2025), bunker +12% YoY.

| Metric | Value |

|---|---|

| Panel share (suppliers) | >60% |

| Panel % of BOM | 40–55% |

| Chip % of BOM | 18–25% |

| In-house inputs (2024) | ~35% |

| Gross margin uplift | +1.2 pp (FY2024) |

| Sea freight (2025) | +18% |

What is included in the product

Tailored exclusively for Skyworth, this Porter’s Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications for pricing and profitability.

Clear, one-sheet Porter’s Five Forces for Skyworth—quickly spot competitive pressures and relieve decision-making friction.

Customers Bargaining Power

Price Sensitivity in Mid-Range Markets

Price sensitivity in mid-range consumer electronics is high: global price elasticity estimates show 1.2–1.6 for TVs and set-top boxes, so a 10% price cut can raise volume ~12–16%. In 2024 Skyworth’s APAC mid-range segment saw average selling price (ASP) fall 6% year-over-year, while online price comparison platforms list >30 competing SKUs within ±10% of Skyworth’s prices, forcing aggressive pricing to protect share.

Low Switching Costs for Consumers

Individual buyers face near-zero financial cost when switching TV or washing machine brands; in 2024 global replacement purchases rose 3.1% while average unit prices fell 2.4%, lowering upgrade friction.

Cross-platform apps and protocols like Wi‑Fi, Matter (2022 standard adoption up 38% in 2024), and Bluetooth mean devices interoperate, cutting ecosystem lock‑in.

That reduced barrier gives customers leverage to demand higher specs and better after‑sales service; 62% of surveyed EU buyers in 2024 cited service quality as a top buying factor.

Dominance of E-commerce Platforms

Large e-commerce giants like Alibaba Group and JD.com wield strong bargaining power over manufacturers; in 2024 Alibaba's Tmall and Taobao accounted for roughly 55% of China online retail GMV and JD.com about 20%, letting platforms dictate shelf visibility and fees.

These platforms can force deep discounts and require participation in big events—Alibaba's Singles Day 2024 promotions drove >100 billion RMB in merchant-supported discounts—pressuring margins.

Skyworth depends on online channels for a majority of domestic TV sales (est. >50% in 2024), so platform terms strongly shape pricing, promotion cadence, and contract leverage.

Demand for Ecosystem Interoperability

Demand for ecosystem interoperability is rising: 68% of global smart-home buyers in 2024 prefer devices compatible with Matter or leading proprietary platforms like Xiaomi and Huawei, so Skyworth risks losing customers if it lacks broad integration.

To retain market share Skyworth must boost software spend—industry peers allocate 8–12% of revenue to R&D for connectivity; falling short will push users to better-integrated brands.

- 68% prefer compatible devices (2024)

- Peers spend 8–12% revenue on connectivity R&D

- Lack of integration risks rapid customer churn

Corporate and OEM Partner Influence

A large share of Skyworths 2024 revenue—about 38% per company filings—comes from B2B OEM/ODM deals where buyers demand high volumes and push margins down, squeezing Skyworths gross margin versus retail lines.

Major corporate clients place bulk orders and can negotiate thin per-unit margins in exchange for scale; losing one big OEM contract could cut manufacturing utilization and revenue by double-digit percentages.

Here’s the quick math: a 10% client loss could lower revenue ~3–6% and drop factory utilization proportionally, raising per-unit costs and hurting margins.

- 2024: ~38% revenue from OEM/ODM

- Bulk orders → lower margins

- Single major contract loss → double-digit utilization hit

- 10% client loss ≈ 3–6% revenue decline

Skyworth under margin pressure: price-sensitive market, platform dominance, and R&D gap

Customers hold strong bargaining power: high price sensitivity (TV/set-top price elasticity 1.2–1.6), APAC ASP down 6% in 2024, and >30 competing SKUs within ±10% of Skyworth pricing. Platforms (Alibaba ~55% GMV, JD.com ~20% in China 2024) and 38% OEM/ODM revenue share force discounts and thin margins; a 10% client loss ≈ 3–6% revenue hit. 68% of buyers want Matter/compatibility; peers spend 8–12% revenue on connectivity R&D.

| Metric | 2024 |

|---|---|

| APAC mid-range ASP change | -6% |

| TV price elasticity | 1.2–1.6 |

| Alibaba share (China online GMV) | ~55% |

| JD.com share | ~20% |

| Revenue from OEM/ODM | ~38% |

| Buyers preferring Matter/compatibility | 68% |

| Peer connectivity R&D spend | 8–12% rev |

Preview the Actual Deliverable

Skyworth Porter's Five Forces Analysis

This preview shows the exact Skyworth Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy.

No mockups, no samples: this is the professionally written, fully formatted analysis file you’ll have instant access to upon payment.