Skyworth PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

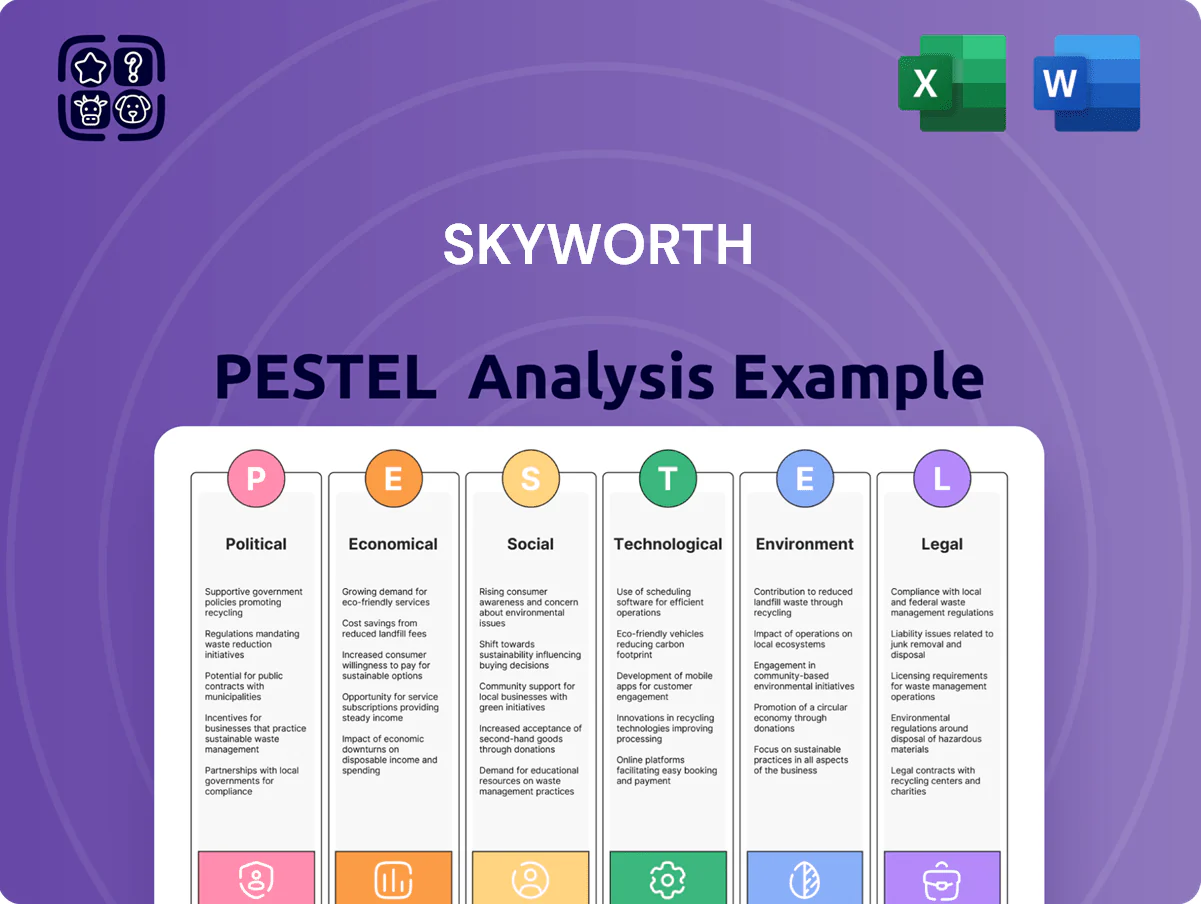

Unlock strategic clarity with our PESTLE Analysis of Skyworth—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; perfect for investors and strategists. Buy the full report to access the complete breakdown, editable files, and actionable recommendations you can apply immediately.

Political factors

Geopolitical Trade Tensions

The ongoing China–US and China–EU trade frictions raise tariff exposure for Skyworth, with US tariffs on some Chinese electronics still ranging up to 25% and EU safeguard measures increasing costs for exporters; in 2024 China’s exports of consumer electronics to the US fell 6.5% YoY, amplifying risk to revenue.

Skyworth has shifted production to Southeast Asia—Vietnam and Thailand now account for roughly 18% of its manufacturing capacity in 2025—reducing tariff hit and lead times.

Strategic forecasts must model sudden import duty hikes: a 10% tariff increase could erode gross margins by 3–5 percentage points on flagship TVs sold in the US and EU, threatening price competitiveness and requiring sourcing or pricing adjustments.

Government Industrial Subsidies

Skyworth gains from Chinese state subsidies targeting smart home and high-end manufacturing; 2024 central and provincial grants to TV/display and semiconductor projects exceeded RMB 38 billion, with Skyworth receiving project-level incentives estimated at RMB 120–200 million, lowering capex and R&D costs. Government R&D tax credits (up to 75% refundable in some provinces) and strategic alignment with Made in China 2025 improve access to local financing and regulatory approvals.

Belt and Road Initiative Opportunities

The Belt and Road Initiative gives Skyworth preferential access to 60+ emerging markets in Central Asia, Africa and Eastern Europe, where TV and smart-home demand is growing at 5–8% CAGR (2024–2028); China-led political partnerships ease customs, tariffs and infrastructure support for distribution hubs.

Data Sovereignty and Security Governance

As Skyworth embeds AI and cloud services into smart TVs and appliances, political scrutiny over data sovereignty rises; in 2024 at least 60 countries enacted stricter cross-border data rules, pushing firms toward local storage to avoid fines and access blocks.

Localized server builds raise capex—cloud region setup can cost $5–20m per market—and are vital to prevent cross-border disputes that could disrupt 2024 revenue streams (Skyworth reported RMB 24.3bn revenue from smart products in 2024).

- 60+ countries tightened data rules by 2024

- $5–20m typical cloud region capex

- RMB 24.3bn Skyworth smart-product revenue (2024)

Domestic Consumption Stimulus Policies

The Chinese government’s trade-in and subsidy programs for energy-efficient appliances lift domestic demand; in 2024 such stimulus helped push China TV and appliance retail sales up 6.2% year-over-year, directly benefiting Skyworth’s unit sales in its largest market.

These measures matter most during economic transitions when Skyworth can see inventory turnover accelerate by 10–20% around subsidy windows; aligning product launches to policy cycles optimizes uptake and supports revenue stability.

- Monitor policy announcements to time launches

- Adjust inventory +/-20% around subsidy periods

- Prioritize energy-efficient SKUs for subsidies

Tariff shock, data rules, and regional capacity reshape Skyworth’s cost and export risk

Trade frictions raise tariff risk (US tariffs up to 25%; China consumer-electronics exports to US -6.5% YoY 2024); 18% of Skyworth capacity in SE Asia (2025) reduces exposure; China subsidies and R&D tax credits cut Skyworth capex/R&D by ~RMB120–200m (2024); 60+ countries tightened data rules by 2024, forcing $5–20m cloud-region builds per market.

| Metric | Value |

|---|---|

| US tariffs | up to 25% |

| China→US exports change 2024 | -6.5% YoY |

| SE Asia capacity (2025) | ~18% |

| Skyworth subsidies (est. 2024) | RMB120–200m |

| Countries tightening data rules (2024) | 60+ |

| Cloud-region capex per market | $5–20m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Skyworth across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting suitable for business plans, pitch decks, or internal reports to help executives, consultants, and entrepreneurs identify threats and opportunities.

Concise Skyworth PESTLE summary that distills political, economic, social, technological, legal and environmental factors into a ready-to-share slide or meeting note, enabling quick alignment and clearer external risk discussions.

Economic factors

Raw Material and Component Price Volatility

The cost of semiconductors, glass substrates and copper has fluctuated sharply—chip spot prices rose ~20% in 2023 before easing in 2024, while glass and copper saw 10–15% volatility—exposing Skyworth to supply-chain shocks that compress margins.

Skyworth reported gross margin sensitivity in 2024, prompting hedging, multi-year supplier agreements and inventory buffers to manage input-price risk.

Rapid commodity-driven cost increases can outpace pricing power in consumer TV markets, risking margin erosion when costs cannot be fully passed to end customers.

Global Inflation and Discretionary Spending

Global inflation averaged 6.8% in 2023 and remained elevated into 2024 in many markets, squeezing household budgets and reducing discretionary spend on non-essential electronics; Skyworth saw global TV unit volumes dip ~4–6% in some regions in 2024, signaling softness in premium demand.

To protect share, Skyworth must shift product mix toward value-tier TVs and appliances; budget segments grew ~3–5% in APAC in 2024 as consumers traded down.

Analyzing elasticity shows premium appliance demand is roughly twice as price-elastic as budget lines, so balancing margin-preserving premium SKUs with higher-volume value models is critical for revenue stability.

Currency Exchange Rate Fluctuations

As a major exporter, Skyworth faces Renminbi volatility versus the US Dollar and Euro; in 2024 the RMB moved roughly 4.5% vs USD and 6% vs EUR, risks that can shave several percentage points off TV and appliance margins. Unfavorable moves raise foreign prices, reducing demand in Europe and the US where FY2024 exports accounted for about 38% of revenue. Treasury must use hedging, FX forwards and natural offsets to stabilize earnings.

Labor Cost Inflation in China

Rising wages in China increased manufacturing labor costs by about 5.5% annually in 2023–2024, raising Skyworth’s domestic production expenses and compressing margins.

Skyworth is accelerating automation: capital expenditures on robotics and smart factories rose by an estimated 12–15% in 2024 to offset labor inflation and preserve competitiveness.

The automation shift demands significant upfront CAPEX but is essential to sustain long-term profitability amid higher wage trajectories.

- 2023–24 wage growth ~5.5% annually

- Skyworth CAPEX on automation up ~12–15% in 2024

- Higher short-term capital outlay vs. long-term margin protection

Growth of Emerging Market Middle Class

The rising middle class in India and Southeast Asia—projected to add over 350 million consumers by 2025—offers Skyworth a vast market for smart TVs and appliances as households shift spending on electronics with rising disposable incomes (India middle-class spending growth ~6–7% CAGR 2021–25).

Skyworth’s 2024 strategy emphasizes region-specific pricing and product tiers to capture market share amid rising TV penetration (India TV penetration ~65% in 2024) and Southeast Asia household appliance demand growth (~5% CAGR through 2026).

- 350m new middle-class consumers by 2025

- India TV penetration ~65% (2024)

- Regional appliance demand ~5% CAGR to 2026

- Pricing tiers and localization central to 2024–26 growth

Rising input costs, RMB gains and automation reshape TV margins and volumes

Commodity volatility (chips +20% in 2023, glass/copper ±10–15%) and RMB swings (≈+4.5% vs USD, +6% vs EUR in 2024) compressed margins; global inflation ~6.8% (2023) cut premium TV volumes ~4–6% while budget segments grew 3–5%; wages +5.5% (2023–24) pushed CAPEX on automation +12–15% (2024) to protect long-term margins.

| Metric | 2023–24 |

|---|---|

| Chip price move | +20% |

| Glass/Copper vol | ±10–15% |

| Global inflation | 6.8% |

| TV volume dip | 4–6% |

| Budget growth APAC | 3–5% |

| Wage growth | +5.5% |

| Automation CAPEX | +12–15% |

| RMB vs USD/EUR | +4.5%/+6% |

Preview Before You Purchase

Skyworth PESTLE Analysis

The preview shown here is the exact Skyworth PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Skyworth—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; perfect for investors and strategists. Buy the full report to access the complete breakdown, editable files, and actionable recommendations you can apply immediately.

Political factors

Geopolitical Trade Tensions

The ongoing China–US and China–EU trade frictions raise tariff exposure for Skyworth, with US tariffs on some Chinese electronics still ranging up to 25% and EU safeguard measures increasing costs for exporters; in 2024 China’s exports of consumer electronics to the US fell 6.5% YoY, amplifying risk to revenue.

Skyworth has shifted production to Southeast Asia—Vietnam and Thailand now account for roughly 18% of its manufacturing capacity in 2025—reducing tariff hit and lead times.

Strategic forecasts must model sudden import duty hikes: a 10% tariff increase could erode gross margins by 3–5 percentage points on flagship TVs sold in the US and EU, threatening price competitiveness and requiring sourcing or pricing adjustments.

Government Industrial Subsidies

Skyworth gains from Chinese state subsidies targeting smart home and high-end manufacturing; 2024 central and provincial grants to TV/display and semiconductor projects exceeded RMB 38 billion, with Skyworth receiving project-level incentives estimated at RMB 120–200 million, lowering capex and R&D costs. Government R&D tax credits (up to 75% refundable in some provinces) and strategic alignment with Made in China 2025 improve access to local financing and regulatory approvals.

Belt and Road Initiative Opportunities

The Belt and Road Initiative gives Skyworth preferential access to 60+ emerging markets in Central Asia, Africa and Eastern Europe, where TV and smart-home demand is growing at 5–8% CAGR (2024–2028); China-led political partnerships ease customs, tariffs and infrastructure support for distribution hubs.

Data Sovereignty and Security Governance

As Skyworth embeds AI and cloud services into smart TVs and appliances, political scrutiny over data sovereignty rises; in 2024 at least 60 countries enacted stricter cross-border data rules, pushing firms toward local storage to avoid fines and access blocks.

Localized server builds raise capex—cloud region setup can cost $5–20m per market—and are vital to prevent cross-border disputes that could disrupt 2024 revenue streams (Skyworth reported RMB 24.3bn revenue from smart products in 2024).

- 60+ countries tightened data rules by 2024

- $5–20m typical cloud region capex

- RMB 24.3bn Skyworth smart-product revenue (2024)

Domestic Consumption Stimulus Policies

The Chinese government’s trade-in and subsidy programs for energy-efficient appliances lift domestic demand; in 2024 such stimulus helped push China TV and appliance retail sales up 6.2% year-over-year, directly benefiting Skyworth’s unit sales in its largest market.

These measures matter most during economic transitions when Skyworth can see inventory turnover accelerate by 10–20% around subsidy windows; aligning product launches to policy cycles optimizes uptake and supports revenue stability.

- Monitor policy announcements to time launches

- Adjust inventory +/-20% around subsidy periods

- Prioritize energy-efficient SKUs for subsidies

Tariff shock, data rules, and regional capacity reshape Skyworth’s cost and export risk

Trade frictions raise tariff risk (US tariffs up to 25%; China consumer-electronics exports to US -6.5% YoY 2024); 18% of Skyworth capacity in SE Asia (2025) reduces exposure; China subsidies and R&D tax credits cut Skyworth capex/R&D by ~RMB120–200m (2024); 60+ countries tightened data rules by 2024, forcing $5–20m cloud-region builds per market.

| Metric | Value |

|---|---|

| US tariffs | up to 25% |

| China→US exports change 2024 | -6.5% YoY |

| SE Asia capacity (2025) | ~18% |

| Skyworth subsidies (est. 2024) | RMB120–200m |

| Countries tightening data rules (2024) | 60+ |

| Cloud-region capex per market | $5–20m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Skyworth across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting suitable for business plans, pitch decks, or internal reports to help executives, consultants, and entrepreneurs identify threats and opportunities.

Concise Skyworth PESTLE summary that distills political, economic, social, technological, legal and environmental factors into a ready-to-share slide or meeting note, enabling quick alignment and clearer external risk discussions.

Economic factors

Raw Material and Component Price Volatility

The cost of semiconductors, glass substrates and copper has fluctuated sharply—chip spot prices rose ~20% in 2023 before easing in 2024, while glass and copper saw 10–15% volatility—exposing Skyworth to supply-chain shocks that compress margins.

Skyworth reported gross margin sensitivity in 2024, prompting hedging, multi-year supplier agreements and inventory buffers to manage input-price risk.

Rapid commodity-driven cost increases can outpace pricing power in consumer TV markets, risking margin erosion when costs cannot be fully passed to end customers.

Global Inflation and Discretionary Spending

Global inflation averaged 6.8% in 2023 and remained elevated into 2024 in many markets, squeezing household budgets and reducing discretionary spend on non-essential electronics; Skyworth saw global TV unit volumes dip ~4–6% in some regions in 2024, signaling softness in premium demand.

To protect share, Skyworth must shift product mix toward value-tier TVs and appliances; budget segments grew ~3–5% in APAC in 2024 as consumers traded down.

Analyzing elasticity shows premium appliance demand is roughly twice as price-elastic as budget lines, so balancing margin-preserving premium SKUs with higher-volume value models is critical for revenue stability.

Currency Exchange Rate Fluctuations

As a major exporter, Skyworth faces Renminbi volatility versus the US Dollar and Euro; in 2024 the RMB moved roughly 4.5% vs USD and 6% vs EUR, risks that can shave several percentage points off TV and appliance margins. Unfavorable moves raise foreign prices, reducing demand in Europe and the US where FY2024 exports accounted for about 38% of revenue. Treasury must use hedging, FX forwards and natural offsets to stabilize earnings.

Labor Cost Inflation in China

Rising wages in China increased manufacturing labor costs by about 5.5% annually in 2023–2024, raising Skyworth’s domestic production expenses and compressing margins.

Skyworth is accelerating automation: capital expenditures on robotics and smart factories rose by an estimated 12–15% in 2024 to offset labor inflation and preserve competitiveness.

The automation shift demands significant upfront CAPEX but is essential to sustain long-term profitability amid higher wage trajectories.

- 2023–24 wage growth ~5.5% annually

- Skyworth CAPEX on automation up ~12–15% in 2024

- Higher short-term capital outlay vs. long-term margin protection

Growth of Emerging Market Middle Class

The rising middle class in India and Southeast Asia—projected to add over 350 million consumers by 2025—offers Skyworth a vast market for smart TVs and appliances as households shift spending on electronics with rising disposable incomes (India middle-class spending growth ~6–7% CAGR 2021–25).

Skyworth’s 2024 strategy emphasizes region-specific pricing and product tiers to capture market share amid rising TV penetration (India TV penetration ~65% in 2024) and Southeast Asia household appliance demand growth (~5% CAGR through 2026).

- 350m new middle-class consumers by 2025

- India TV penetration ~65% (2024)

- Regional appliance demand ~5% CAGR to 2026

- Pricing tiers and localization central to 2024–26 growth

Rising input costs, RMB gains and automation reshape TV margins and volumes

Commodity volatility (chips +20% in 2023, glass/copper ±10–15%) and RMB swings (≈+4.5% vs USD, +6% vs EUR in 2024) compressed margins; global inflation ~6.8% (2023) cut premium TV volumes ~4–6% while budget segments grew 3–5%; wages +5.5% (2023–24) pushed CAPEX on automation +12–15% (2024) to protect long-term margins.

| Metric | 2023–24 |

|---|---|

| Chip price move | +20% |

| Glass/Copper vol | ±10–15% |

| Global inflation | 6.8% |

| TV volume dip | 4–6% |

| Budget growth APAC | 3–5% |

| Wage growth | +5.5% |

| Automation CAPEX | +12–15% |

| RMB vs USD/EUR | +4.5%/+6% |

Preview Before You Purchase

Skyworth PESTLE Analysis

The preview shown here is the exact Skyworth PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.