Schlumberger Porter's Five Forces Analysis

From Overview to Strategy Blueprint

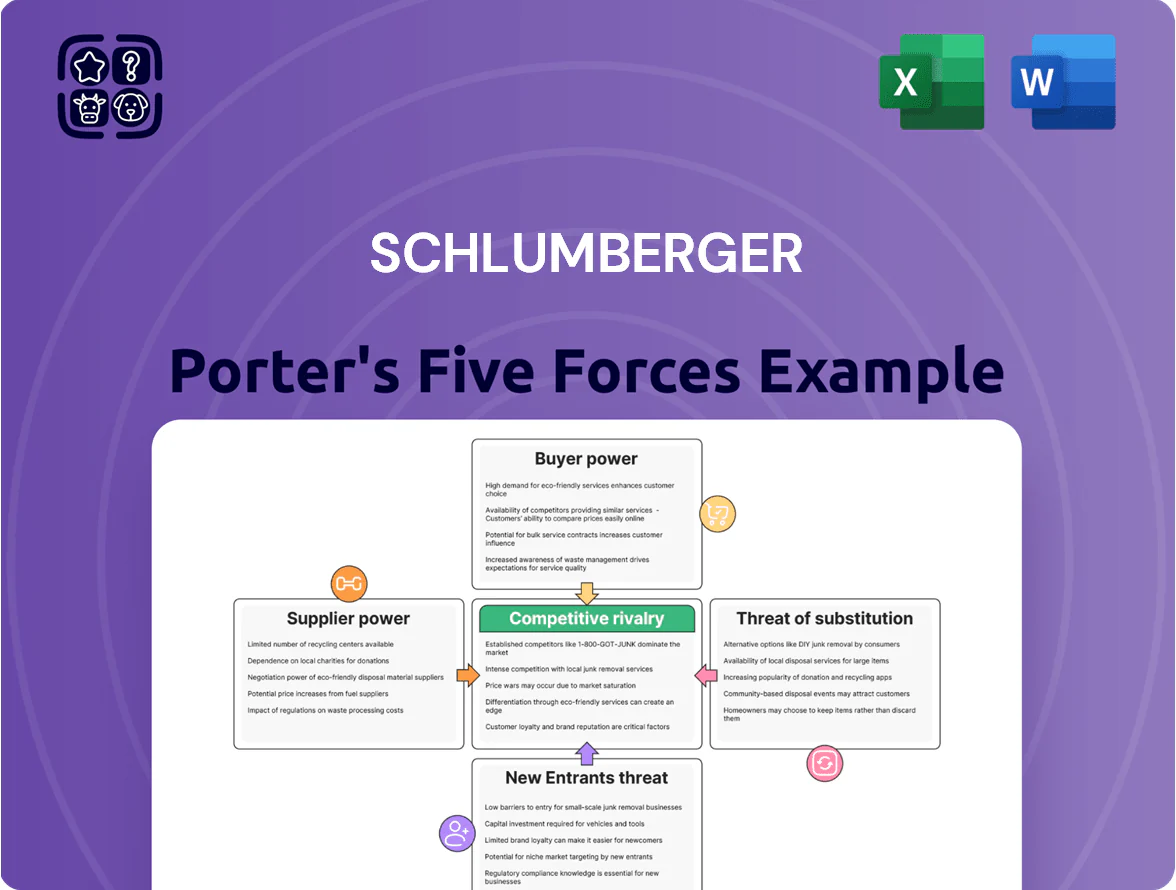

Schlumberger faces high supplier and buyer bargaining power, significant rivalry among established oilfield services players, moderate threat from substitutes as energy transition advances, and substantial barriers deterring new entrants—this snapshot highlights core competitive pressures shaping its margins and strategic moves.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Schlumberger’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Manufacturers

The supply of high-precision subsea and drilling components is concentrated among a few specialized vendors, with the top 5 suppliers estimated to cover ~60% of SLB’s critical parts market in 2024, reflecting high quality barriers. These suppliers hold moderate leverage because their engineering underpins SLB’s proprietary tool reliability and performance. SLB reduces risk via a diverse global supply chain and >$450m capex in internal manufacturing from 2022–2024 to onshore core tech production.

Raw Material Price Volatility

Skilled Technical Labor

The limited pool of specialized petroleum engineers and data scientists creates a real supply constraint for energy services, with US demand for oilfield data scientists rising ~18% YoY in 2024 and tech-sector salaries 20–40% higher than legacy oilfield pay. This talent premium raises suppliers’ bargaining power as firms compete with tech giants for skills. SLB (Schlumberger) counters with $200m+ annual training and reskilling investments and partnerships with 15 universities to retain staff. Positioning as an energy-transition leader helps SLB attract top-tier talent and reduce turnover.

Digital Infrastructure Providers

As SLB scales its Delfi digital platform, it depends on cloud and security providers such as Microsoft Azure and Google Cloud, whose global market shares were 24% and 11% respectively in 2024—giving them leverage tied to uptime and data integrity for SLB’s remote well operations.

To limit supplier power, SLB pursues multi-cloud deployments and negotiated SLAs; multi-cloud reduces single-vendor outage risk (Azure/Google outages cost enterprises millions per hour) and boosts SLB’s bargaining on pricing and data- residency terms.

- 2024: Azure 24% market share, Google 11%

- Multi-cloud reduces vendor-lock and outage exposure

- SLA leverage improves pricing, redundancy, data-residency controls

Logistics and Distribution Networks

The global scale of Schlumberger (SLB) forces complex logistics to move 200+ tonne rigs and hazardous materials to remote offshore/onshore sites, raising supplier importance.

Specialist heavy-lift and hazardous-capable carriers in volatile regions wield higher bargaining power despite many providers.

SLB’s $25B 2024 revenue and volume gives leverage to secure favorable rates, but late-2025 geopolitical tensions lift niche providers’ edge.

- Heavy-lift/hazard capability increases supplier power

- Many providers, few specialists

- SLB scale (2024 revenue $25B) lowers costs

- Late-2025 geopolitics boost niche leverage

Mixed supplier power: specialized vendors boost leverage; hedges protect margins

Supplier power is mixed: few specialized vendors supply ~60% of critical parts (2024), giving moderate leverage, while bulk-input suppliers are weaker but commodity swings raised costs (alloy premiums +12% in 2023). SLB hedges/multi‑year contracts cover ~40–60% inputs, protecting ~150–200 bps margin; cloud providers (Azure 24%, Google 11% in 2024) and niche heavy‑lift carriers retain pockets of leverage.

What is included in the product

Tailored Porter's Five Forces assessment for Schlumberger, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal strategic pressures, pricing leverage, and potential disruptive threats to its market leadership.

Schlumberger Porter's Five Forces condensed into a one-sheet—quickly spot supplier/customer power, rivalry, substitutes, and entry threats to guide strategic moves in oilfield services.

Customers Bargaining Power

Concentration of Major Oil Companies

A significant share of Schlumberger’s 2024 revenue—about 28% of its $28.8 billion total—comes from a handful of IOCs and NOCs, concentrating customer power. Large buyers like Saudi Aramco and ExxonMobil use multi-year contracts worth hundreds of millions to demand aggressive pricing and bundled services. That scale forces SLB to prove efficiency and technical superiority continually, pressuring margins and driving investment in integrated solutions. In 2024 SLB reported margin compression in regions with top-5 customers, underscoring this leverage.

Shift Toward Performance Based Contracts

Customers are shifting from day-rate contracts to performance-based deals, moving operational risk to SLB and demanding higher productivity; in 2024 about 28% of upstream service contracts were reported as performance-linked, up from ~18% in 2021 (IEA, industry surveys).

This trend boosts buyer leverage because payment ties to outcomes, raising pressure on SLB to deliver consistent well/field KPIs and accept downside risk on cost overruns.

SLB offsets risk with proprietary data analytics and digital platforms—Reservoir-to-Revenue tools—claiming >90% success rates on optimized completions and using results to capture performance bonuses and protect margins.

Customer Focus on Decarbonization

By end-2025 major buyers (BP, Shell, ExxonMobil) set net-zero/2030 scope 1–2 targets, forcing SLB to supply low-carbon tech and carbon capture; ~40% of service contracts now include emissions KPIs, boosting buyer leverage.

Buyers can switch vendors if suppliers fail to cut extraction emissions; procurement tends to favor partners with verifiable carbon intensity cuts and CCS readiness.

SLB defends position via Fit-for-Basin offerings—electrified rigs and optimized drilling—claiming up to 30% methane/CO2 reduction on pilot projects, keeping SLB preferred despite price pressure.

Adoption of In-House Digital Capabilities

Large oil majors like Saudi Aramco and ExxonMobil invested over $1.2B in in‑house digital projects in 2024, building digital twins and analytics that can cut reliance on SLB’s software.

This raises customer bargaining power: SLB must show its ecosystem delivers better integration and ROI than internal tools, else risk lost software revenue (SLB software & digital revenue was $2.1B in 2024).

SLB counters with open‑architecture platforms and APIs so customers can plug in their data, improving stickiness and making comparisons on ROI clearer.

- Major customers spent $1.2B+ on in‑house digital (2024)

- SLB digital/software revenue: $2.1B (2024)

- Open architecture + APIs = easier customer integration

- Key metric: prove superior total cost of ownership and faster time-to-value

Price Sensitivity in Mature Basins

In mature basins with tighter margins, customers push Schlumberger (SLB) to bid via competitive tendering, making price sensitivity high and deal awards volume-driven rather than feature-driven.

SLB shifts focus from premium tech to cost-efficiency, cutting service delivery costs via automation, digital workflows, and lean operating models to protect margins.

In 2025 SLB reported digital and automation uptake reduced operational costs by ~8–12% on pilot rigs, lowering client break-even thresholds and helping retain share in price-competitive tenders.

- High price sensitivity → frequent tenders

- Competition on cost, not just tech

- Automation + lean ops cut costs ~8–12% (2025 pilots)

- Helps lower client break-even, retain share

SLB faces buyer leverage as top clients drive 28% revenue; digital pilots cut ops 8–12%

Buyers hold high leverage: top clients drove ~28% of SLB’s $28.8B revenue in 2024, pressuring margins via large multi‑year and outcome‑linked contracts; ~28% of upstream contracts were performance‑based in 2024 (IEA). SLB’s $2.1B digital revenue and open APIs offset some risk versus customers’ $1.2B+ in‑house digital spend, while 2025 pilots cut ops costs ~8–12%, easing tender pressure.

| Metric | Value |

|---|---|

| SLB revenue (2024) | $28.8B |

| Share from top clients | ~28% |

| Performance‑based contracts (2024) | ~28% |

| SLB digital revenue (2024) | $2.1B |

| Customer in‑house digital spend (2024) | $1.2B+ |

| Pilot ops cost reduction (2025) | ~8–12% |

Preview Before You Purchase

Schlumberger Porter's Five Forces Analysis

This preview shows the exact Schlumberger Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. You're looking at the actual, fully formatted document ready for download and use the moment you buy. The file contains the complete competitive assessment tailored to Schlumberger, including force-by-force insights and strategic implications. Purchase grants instant access to this same professional deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Schlumberger faces high supplier and buyer bargaining power, significant rivalry among established oilfield services players, moderate threat from substitutes as energy transition advances, and substantial barriers deterring new entrants—this snapshot highlights core competitive pressures shaping its margins and strategic moves.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Schlumberger’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Manufacturers

The supply of high-precision subsea and drilling components is concentrated among a few specialized vendors, with the top 5 suppliers estimated to cover ~60% of SLB’s critical parts market in 2024, reflecting high quality barriers. These suppliers hold moderate leverage because their engineering underpins SLB’s proprietary tool reliability and performance. SLB reduces risk via a diverse global supply chain and >$450m capex in internal manufacturing from 2022–2024 to onshore core tech production.

Raw Material Price Volatility

Skilled Technical Labor

The limited pool of specialized petroleum engineers and data scientists creates a real supply constraint for energy services, with US demand for oilfield data scientists rising ~18% YoY in 2024 and tech-sector salaries 20–40% higher than legacy oilfield pay. This talent premium raises suppliers’ bargaining power as firms compete with tech giants for skills. SLB (Schlumberger) counters with $200m+ annual training and reskilling investments and partnerships with 15 universities to retain staff. Positioning as an energy-transition leader helps SLB attract top-tier talent and reduce turnover.

Digital Infrastructure Providers

As SLB scales its Delfi digital platform, it depends on cloud and security providers such as Microsoft Azure and Google Cloud, whose global market shares were 24% and 11% respectively in 2024—giving them leverage tied to uptime and data integrity for SLB’s remote well operations.

To limit supplier power, SLB pursues multi-cloud deployments and negotiated SLAs; multi-cloud reduces single-vendor outage risk (Azure/Google outages cost enterprises millions per hour) and boosts SLB’s bargaining on pricing and data- residency terms.

- 2024: Azure 24% market share, Google 11%

- Multi-cloud reduces vendor-lock and outage exposure

- SLA leverage improves pricing, redundancy, data-residency controls

Logistics and Distribution Networks

The global scale of Schlumberger (SLB) forces complex logistics to move 200+ tonne rigs and hazardous materials to remote offshore/onshore sites, raising supplier importance.

Specialist heavy-lift and hazardous-capable carriers in volatile regions wield higher bargaining power despite many providers.

SLB’s $25B 2024 revenue and volume gives leverage to secure favorable rates, but late-2025 geopolitical tensions lift niche providers’ edge.

- Heavy-lift/hazard capability increases supplier power

- Many providers, few specialists

- SLB scale (2024 revenue $25B) lowers costs

- Late-2025 geopolitics boost niche leverage

Mixed supplier power: specialized vendors boost leverage; hedges protect margins

Supplier power is mixed: few specialized vendors supply ~60% of critical parts (2024), giving moderate leverage, while bulk-input suppliers are weaker but commodity swings raised costs (alloy premiums +12% in 2023). SLB hedges/multi‑year contracts cover ~40–60% inputs, protecting ~150–200 bps margin; cloud providers (Azure 24%, Google 11% in 2024) and niche heavy‑lift carriers retain pockets of leverage.

What is included in the product

Tailored Porter's Five Forces assessment for Schlumberger, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal strategic pressures, pricing leverage, and potential disruptive threats to its market leadership.

Schlumberger Porter's Five Forces condensed into a one-sheet—quickly spot supplier/customer power, rivalry, substitutes, and entry threats to guide strategic moves in oilfield services.

Customers Bargaining Power

Concentration of Major Oil Companies

A significant share of Schlumberger’s 2024 revenue—about 28% of its $28.8 billion total—comes from a handful of IOCs and NOCs, concentrating customer power. Large buyers like Saudi Aramco and ExxonMobil use multi-year contracts worth hundreds of millions to demand aggressive pricing and bundled services. That scale forces SLB to prove efficiency and technical superiority continually, pressuring margins and driving investment in integrated solutions. In 2024 SLB reported margin compression in regions with top-5 customers, underscoring this leverage.

Shift Toward Performance Based Contracts

Customers are shifting from day-rate contracts to performance-based deals, moving operational risk to SLB and demanding higher productivity; in 2024 about 28% of upstream service contracts were reported as performance-linked, up from ~18% in 2021 (IEA, industry surveys).

This trend boosts buyer leverage because payment ties to outcomes, raising pressure on SLB to deliver consistent well/field KPIs and accept downside risk on cost overruns.

SLB offsets risk with proprietary data analytics and digital platforms—Reservoir-to-Revenue tools—claiming >90% success rates on optimized completions and using results to capture performance bonuses and protect margins.

Customer Focus on Decarbonization

By end-2025 major buyers (BP, Shell, ExxonMobil) set net-zero/2030 scope 1–2 targets, forcing SLB to supply low-carbon tech and carbon capture; ~40% of service contracts now include emissions KPIs, boosting buyer leverage.

Buyers can switch vendors if suppliers fail to cut extraction emissions; procurement tends to favor partners with verifiable carbon intensity cuts and CCS readiness.

SLB defends position via Fit-for-Basin offerings—electrified rigs and optimized drilling—claiming up to 30% methane/CO2 reduction on pilot projects, keeping SLB preferred despite price pressure.

Adoption of In-House Digital Capabilities

Large oil majors like Saudi Aramco and ExxonMobil invested over $1.2B in in‑house digital projects in 2024, building digital twins and analytics that can cut reliance on SLB’s software.

This raises customer bargaining power: SLB must show its ecosystem delivers better integration and ROI than internal tools, else risk lost software revenue (SLB software & digital revenue was $2.1B in 2024).

SLB counters with open‑architecture platforms and APIs so customers can plug in their data, improving stickiness and making comparisons on ROI clearer.

- Major customers spent $1.2B+ on in‑house digital (2024)

- SLB digital/software revenue: $2.1B (2024)

- Open architecture + APIs = easier customer integration

- Key metric: prove superior total cost of ownership and faster time-to-value

Price Sensitivity in Mature Basins

In mature basins with tighter margins, customers push Schlumberger (SLB) to bid via competitive tendering, making price sensitivity high and deal awards volume-driven rather than feature-driven.

SLB shifts focus from premium tech to cost-efficiency, cutting service delivery costs via automation, digital workflows, and lean operating models to protect margins.

In 2025 SLB reported digital and automation uptake reduced operational costs by ~8–12% on pilot rigs, lowering client break-even thresholds and helping retain share in price-competitive tenders.

- High price sensitivity → frequent tenders

- Competition on cost, not just tech

- Automation + lean ops cut costs ~8–12% (2025 pilots)

- Helps lower client break-even, retain share

SLB faces buyer leverage as top clients drive 28% revenue; digital pilots cut ops 8–12%

Buyers hold high leverage: top clients drove ~28% of SLB’s $28.8B revenue in 2024, pressuring margins via large multi‑year and outcome‑linked contracts; ~28% of upstream contracts were performance‑based in 2024 (IEA). SLB’s $2.1B digital revenue and open APIs offset some risk versus customers’ $1.2B+ in‑house digital spend, while 2025 pilots cut ops costs ~8–12%, easing tender pressure.

| Metric | Value |

|---|---|

| SLB revenue (2024) | $28.8B |

| Share from top clients | ~28% |

| Performance‑based contracts (2024) | ~28% |

| SLB digital revenue (2024) | $2.1B |

| Customer in‑house digital spend (2024) | $1.2B+ |

| Pilot ops cost reduction (2025) | ~8–12% |

Preview Before You Purchase

Schlumberger Porter's Five Forces Analysis

This preview shows the exact Schlumberger Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. You're looking at the actual, fully formatted document ready for download and use the moment you buy. The file contains the complete competitive assessment tailored to Schlumberger, including force-by-force insights and strategic implications. Purchase grants instant access to this same professional deliverable.