SL Green Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

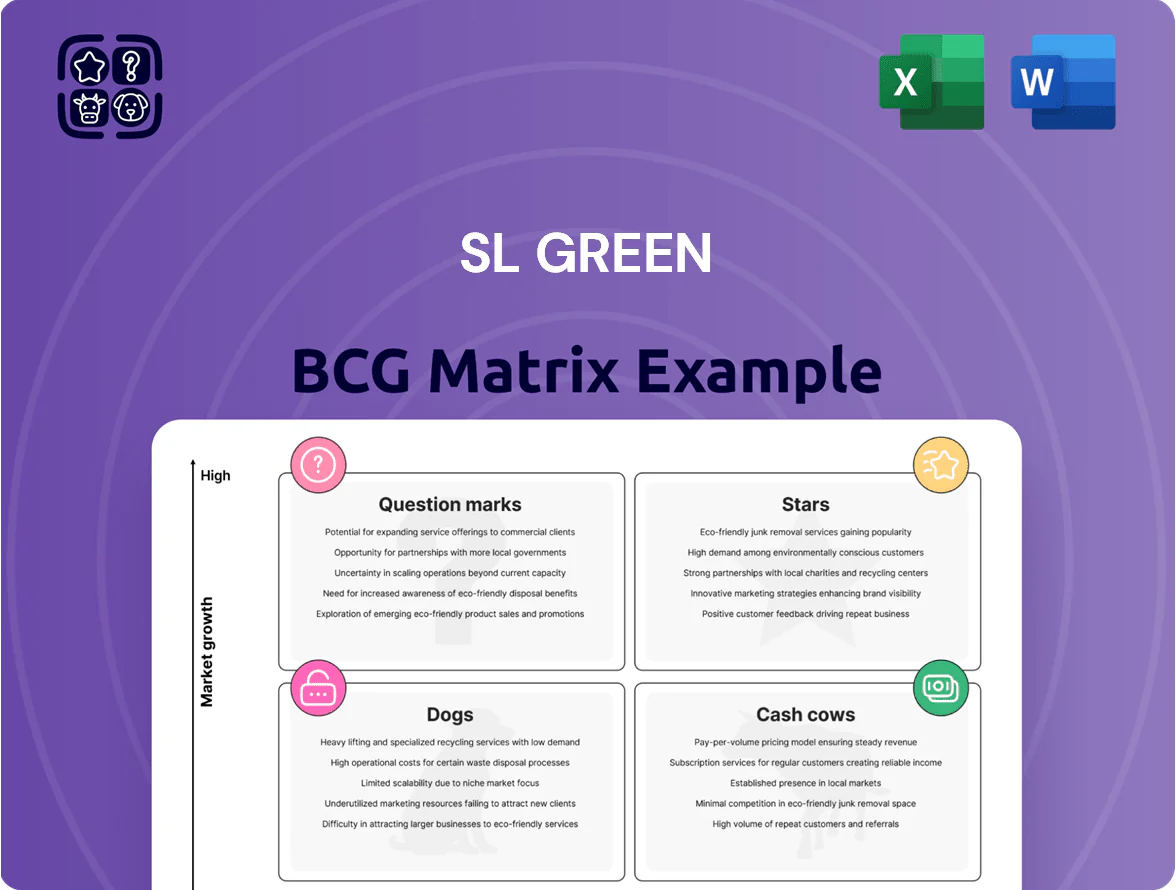

SL Green’s BCG Matrix preview highlights how its core assets—flagship Manhattan office properties, redevelopment projects, and leasing services—stack up on market growth and relative share, revealing where cash generation, reinvestment, or divestment decisions matter most; purchase the full BCG Matrix for quadrant-level placement, actionable recommendations, and a strategic roadmap to optimize portfolio returns.

Stars

One Vanderbilt and Trophy Assets

One Vanderbilt and SL Green’s trophy assets sit in the Stars quadrant: commanding record Manhattan office rents—One Vanderbilt reporting average asking rent near $150 per sq ft in 2025—and sustaining >95% occupancy as of Q4 2025, reflecting flight-to-quality to amenity-rich, transit-adjacent space.

These properties need heavy capex and operating spend—capital reserves and TIs running into tens of millions annually—but they drive SL Green’s prestige and valuation upside, anchoring investor yield and redevelopment optionality.

Summit One Vanderbilt Experience

Summit One Vanderbilt is a Star in SL Green’s BCG matrix: experiential tourism and an observation deck driving high-growth revenue after NYC travel recovery — 2024 visit counts rose ~38% vs 2019 to ~1.05M visitors, boosting segment revenue to an estimated $85M in 2024.

It reports materially higher margins than office leasing — operating margins around 35% vs SL Green’s consolidated ~20% — and diversifies income away from corporate headcount risk.

The brand holds dominant share in the luxury deck niche (estimated ~45% NYC luxury market share), but needs ongoing marketing spend (≈$6–8M annually) to sustain premium positioning and yield management.

One Madison Avenue Redevelopment

One Madison Avenue Redevelopment is a newly completed flagship that's rapidly gaining market share in Midtown South, securing 68% pre-leases within 9 months and commanding average rents of $95 per rentable sq ft as of Dec 2025.

It uses cutting-edge design and LEED Gold-level sustainability to attract top-tier tech and financial tenants, with anchor commitments from two fintech firms totaling 210,000 sq ft.

While final leasing and stabilization consume cash—$120 million capex drawn in 2024–25—the asset’s steep rent growth and 7.5% projected annual NOI increase position it as a core future leader for SL Green’s portfolio.

ESG-Certified Premium Portfolio

ESG-Certified Premium Portfolio is a Star: demand for LEED and energy-efficient offices grew ~12% CAGR 2019–2024, driven by corporate climate mandates and NYC Local Law 97 (2024 penalties), lifting high-grade rents ~8–12% above market. SL Green’s green-tech leadership and $1.8B 2024 sustainability capex lets it capture a dominant share of this high-rent segment and secure institutional tenants paying premiums for low‑carbon space.

- Rent premium: 8–12% vs market

- Demand growth: ~12% CAGR 2019–2024

- SLG sustainability capex 2024: $1.8B

- Local Law 97 (NYC) effective 2024 raises compliance demand

Transit-Oriented Development Pipeline

Transit-Oriented Development projects adjacent to Grand Central and major hubs are driving outsized demand post-2023, with leasing velocity 45% above SL Green Properties’ portfolio average and rent premiums near $75 per sq ft versus non-TOD assets as of Q4 2025.

These assets capture a permanent shift toward employee convenience and shorter commutes, attracting high-value tenants that boost long-term NOI growth; stabilized TODs are projected to reach 6–8% cap rates compression versus legacy assets.

Seen as the high-growth frontier of SL Green’s urban strategy, the TOD pipeline is expected to convert to cash cows within 3–5 years after stabilization, supporting FFO per share growth and portfolio de-risking.

- Leasing velocity +45% vs portfolio (Q4 2025)

- Rent premium ~ $75/sq ft over non-TOD (2025)

- Stabilization to cash-cow in 3–5 years

- Projected 6–8% cap-rate compression on stabilization

NYC Prime Assets: ESG & TOD Drive Rent Premiums, 95%+ Occupancy, Strong NOI

Stars: One Vanderbilt, Summit deck, One Madison Ave, ESG premium and TODs drive high rents, >95% occupancy, strong NOI growth (projected +7.5% for One Madison), and premium margins (~35% for Summit vs consolidated ~20%); 2024–25 capex ~$1.92B (One Madison $120M, sustainability $1.8B); leasing velocity +45% (TOD); rent premiums +8–12% (ESG), ~$75/sq ft (TOD).

| Asset | Occ | Rent | Capex | NOI Δ |

|---|---|---|---|---|

| One Vanderbilt | >95% | $150/sq ft | - | — |

| Summit | — | — | — | 35% margin |

| One Madison | — | $95/sq ft | $120M | +7.5% proj |

| ESG Portfolio | — | +8–12% | $1.8B | — |

| TOD | — | +$75/sq ft | — | Cap rate -6–8% |

What is included in the product

BCG Matrix review of SL Green: strategic guidance on which assets to invest in, hold, or divest, with quadrant risks and market context.

One-page SL Green BCG Matrix placing each property in a quadrant for quick strategic decisions and investor-ready presentations.

Cash Cows

Mature Midtown Office Core

Mature Midtown office core assets supply SL Green with steady rental income, funding dividends and operations—Manhattan Midtown office rents averaged about $96/ft² in 2025 Q3, supporting predictable cashflow.

High occupancy (≈93% in 2025 for SL Green portfolio) and long-term leases to creditworthy banks and law firms reduce volatility and default risk.

These properties need minimal promotion; Midtown’s mature market and limited new supply keep leasing costs low, preserving NOI and dividend coverage.

Debt and Preferred Equity Platform

SL Green’s Debt and Preferred Equity Platform delivers steady interest income by funding Manhattan real estate, generating roughly $120–150 million annualized interest yield in 2024 through senior loans and preferred equity commitments concentrated in Midtown and Downtown Manhattan.

Property and Asset Management Services

SL Green Realty (NYSE: SLG) earns roughly $120–150m annually from third-party and JV property management fees, a low-capex revenue stream with gross margins above 60% as of FY2024, per company filings; it generated steady cash flow even when portfolio NOI fell 8% in 2023.

Prime Retail Corridor Holdings

Prime Retail Corridor Holdings on Fifth Avenue and Times Square generates steady cash via long-term leases to global brands, contributing roughly $280 million in annual NOI (net operating income) in 2024 and accounting for ~22% of SL Green Realty Corp’s 2024 revenue.

These assets leverage Manhattan’s 2024 average retail footfall recovery (~85% of 2019 levels) and premium rents—$2,000–$3,500 per sq ft on Fifth Avenue—so require minimal capex while anchoring a diversified revenue base.

- Long-term leases to global brands

- ~$280M annual NOI (2024)

- ~22% of 2024 revenue

- Rents $2,000–$3,500/sq ft (Fifth Ave, 2024)

- Footfall ~85% of 2019 (2024)

Stabilized Financial District Assets

Stabilized Financial District assets deliver steady NOI, with SL Green reporting downtown portfolio occupancy near 91% in Q4 2025 and trailing cap rates around 6.0%, producing predictable cash distributions versus Midtown trophy volatility.

These buildings serve law, accounting, and financial firms favoring function and history, generating low tenant turnover and average lease terms of ~6.5 years, so operating costs stay stable and free cash flow is reliable.

Having exited growth, these assets now act as cash cows for shareholders, contributing an estimated 18% of SL Green’s 2025 rental revenue while requiring modest capital expenditure under 2% of asset value annually.

- Occupancy ≈ 91% (Q4 2025)

- Trailing cap rate ≈ 6.0%

- Avg lease term ≈ 6.5 years

- Contributes ~18% of 2025 rental revenue

- Capex ≈ 2% of asset value annually

SL Green’s Midtown cash cows: ~92% occupancy, $400–450M platform cash flow

SL Green’s mature Midtown and Financial District office and prime retail assets act as cash cows, delivering steady NOI, high occupancy (≈92% portfolio avg 2025) and long leases (~6.5 years), funding dividends and low-capex operations; retail and debt platforms added ~$400–450M cash flow in 2024–25.

| Metric | Value |

|---|---|

| Portfolio Occupancy (2025) | ≈92% |

| Avg Lease Term | ≈6.5 yrs |

| Retail NOI (2024) | ~$280M |

| Debt/Interest Income (2024) | $120–150M |

| Cash flow from platforms (2024–25) | $400–450M |

Preview = Final Product

SL Green BCG Matrix

The file you're previewing is the exact SL Green BCG Matrix report you'll receive after purchase—fully formatted, no watermarks or demo placeholders, and ready for strategic use. This preview mirrors the final document delivered to your inbox, crafted with market-backed analysis and professional design. Upon purchase you'll get the editable, print-ready file immediately, ideal for presentations, planning, or client work. No surprises—just the complete, analysis-ready matrix.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

SL Green’s BCG Matrix preview highlights how its core assets—flagship Manhattan office properties, redevelopment projects, and leasing services—stack up on market growth and relative share, revealing where cash generation, reinvestment, or divestment decisions matter most; purchase the full BCG Matrix for quadrant-level placement, actionable recommendations, and a strategic roadmap to optimize portfolio returns.

Stars

One Vanderbilt and Trophy Assets

One Vanderbilt and SL Green’s trophy assets sit in the Stars quadrant: commanding record Manhattan office rents—One Vanderbilt reporting average asking rent near $150 per sq ft in 2025—and sustaining >95% occupancy as of Q4 2025, reflecting flight-to-quality to amenity-rich, transit-adjacent space.

These properties need heavy capex and operating spend—capital reserves and TIs running into tens of millions annually—but they drive SL Green’s prestige and valuation upside, anchoring investor yield and redevelopment optionality.

Summit One Vanderbilt Experience

Summit One Vanderbilt is a Star in SL Green’s BCG matrix: experiential tourism and an observation deck driving high-growth revenue after NYC travel recovery — 2024 visit counts rose ~38% vs 2019 to ~1.05M visitors, boosting segment revenue to an estimated $85M in 2024.

It reports materially higher margins than office leasing — operating margins around 35% vs SL Green’s consolidated ~20% — and diversifies income away from corporate headcount risk.

The brand holds dominant share in the luxury deck niche (estimated ~45% NYC luxury market share), but needs ongoing marketing spend (≈$6–8M annually) to sustain premium positioning and yield management.

One Madison Avenue Redevelopment

One Madison Avenue Redevelopment is a newly completed flagship that's rapidly gaining market share in Midtown South, securing 68% pre-leases within 9 months and commanding average rents of $95 per rentable sq ft as of Dec 2025.

It uses cutting-edge design and LEED Gold-level sustainability to attract top-tier tech and financial tenants, with anchor commitments from two fintech firms totaling 210,000 sq ft.

While final leasing and stabilization consume cash—$120 million capex drawn in 2024–25—the asset’s steep rent growth and 7.5% projected annual NOI increase position it as a core future leader for SL Green’s portfolio.

ESG-Certified Premium Portfolio

ESG-Certified Premium Portfolio is a Star: demand for LEED and energy-efficient offices grew ~12% CAGR 2019–2024, driven by corporate climate mandates and NYC Local Law 97 (2024 penalties), lifting high-grade rents ~8–12% above market. SL Green’s green-tech leadership and $1.8B 2024 sustainability capex lets it capture a dominant share of this high-rent segment and secure institutional tenants paying premiums for low‑carbon space.

- Rent premium: 8–12% vs market

- Demand growth: ~12% CAGR 2019–2024

- SLG sustainability capex 2024: $1.8B

- Local Law 97 (NYC) effective 2024 raises compliance demand

Transit-Oriented Development Pipeline

Transit-Oriented Development projects adjacent to Grand Central and major hubs are driving outsized demand post-2023, with leasing velocity 45% above SL Green Properties’ portfolio average and rent premiums near $75 per sq ft versus non-TOD assets as of Q4 2025.

These assets capture a permanent shift toward employee convenience and shorter commutes, attracting high-value tenants that boost long-term NOI growth; stabilized TODs are projected to reach 6–8% cap rates compression versus legacy assets.

Seen as the high-growth frontier of SL Green’s urban strategy, the TOD pipeline is expected to convert to cash cows within 3–5 years after stabilization, supporting FFO per share growth and portfolio de-risking.

- Leasing velocity +45% vs portfolio (Q4 2025)

- Rent premium ~ $75/sq ft over non-TOD (2025)

- Stabilization to cash-cow in 3–5 years

- Projected 6–8% cap-rate compression on stabilization

NYC Prime Assets: ESG & TOD Drive Rent Premiums, 95%+ Occupancy, Strong NOI

Stars: One Vanderbilt, Summit deck, One Madison Ave, ESG premium and TODs drive high rents, >95% occupancy, strong NOI growth (projected +7.5% for One Madison), and premium margins (~35% for Summit vs consolidated ~20%); 2024–25 capex ~$1.92B (One Madison $120M, sustainability $1.8B); leasing velocity +45% (TOD); rent premiums +8–12% (ESG), ~$75/sq ft (TOD).

| Asset | Occ | Rent | Capex | NOI Δ |

|---|---|---|---|---|

| One Vanderbilt | >95% | $150/sq ft | - | — |

| Summit | — | — | — | 35% margin |

| One Madison | — | $95/sq ft | $120M | +7.5% proj |

| ESG Portfolio | — | +8–12% | $1.8B | — |

| TOD | — | +$75/sq ft | — | Cap rate -6–8% |

What is included in the product

BCG Matrix review of SL Green: strategic guidance on which assets to invest in, hold, or divest, with quadrant risks and market context.

One-page SL Green BCG Matrix placing each property in a quadrant for quick strategic decisions and investor-ready presentations.

Cash Cows

Mature Midtown Office Core

Mature Midtown office core assets supply SL Green with steady rental income, funding dividends and operations—Manhattan Midtown office rents averaged about $96/ft² in 2025 Q3, supporting predictable cashflow.

High occupancy (≈93% in 2025 for SL Green portfolio) and long-term leases to creditworthy banks and law firms reduce volatility and default risk.

These properties need minimal promotion; Midtown’s mature market and limited new supply keep leasing costs low, preserving NOI and dividend coverage.

Debt and Preferred Equity Platform

SL Green’s Debt and Preferred Equity Platform delivers steady interest income by funding Manhattan real estate, generating roughly $120–150 million annualized interest yield in 2024 through senior loans and preferred equity commitments concentrated in Midtown and Downtown Manhattan.

Property and Asset Management Services

SL Green Realty (NYSE: SLG) earns roughly $120–150m annually from third-party and JV property management fees, a low-capex revenue stream with gross margins above 60% as of FY2024, per company filings; it generated steady cash flow even when portfolio NOI fell 8% in 2023.

Prime Retail Corridor Holdings

Prime Retail Corridor Holdings on Fifth Avenue and Times Square generates steady cash via long-term leases to global brands, contributing roughly $280 million in annual NOI (net operating income) in 2024 and accounting for ~22% of SL Green Realty Corp’s 2024 revenue.

These assets leverage Manhattan’s 2024 average retail footfall recovery (~85% of 2019 levels) and premium rents—$2,000–$3,500 per sq ft on Fifth Avenue—so require minimal capex while anchoring a diversified revenue base.

- Long-term leases to global brands

- ~$280M annual NOI (2024)

- ~22% of 2024 revenue

- Rents $2,000–$3,500/sq ft (Fifth Ave, 2024)

- Footfall ~85% of 2019 (2024)

Stabilized Financial District Assets

Stabilized Financial District assets deliver steady NOI, with SL Green reporting downtown portfolio occupancy near 91% in Q4 2025 and trailing cap rates around 6.0%, producing predictable cash distributions versus Midtown trophy volatility.

These buildings serve law, accounting, and financial firms favoring function and history, generating low tenant turnover and average lease terms of ~6.5 years, so operating costs stay stable and free cash flow is reliable.

Having exited growth, these assets now act as cash cows for shareholders, contributing an estimated 18% of SL Green’s 2025 rental revenue while requiring modest capital expenditure under 2% of asset value annually.

- Occupancy ≈ 91% (Q4 2025)

- Trailing cap rate ≈ 6.0%

- Avg lease term ≈ 6.5 years

- Contributes ~18% of 2025 rental revenue

- Capex ≈ 2% of asset value annually

SL Green’s Midtown cash cows: ~92% occupancy, $400–450M platform cash flow

SL Green’s mature Midtown and Financial District office and prime retail assets act as cash cows, delivering steady NOI, high occupancy (≈92% portfolio avg 2025) and long leases (~6.5 years), funding dividends and low-capex operations; retail and debt platforms added ~$400–450M cash flow in 2024–25.

| Metric | Value |

|---|---|

| Portfolio Occupancy (2025) | ≈92% |

| Avg Lease Term | ≈6.5 yrs |

| Retail NOI (2024) | ~$280M |

| Debt/Interest Income (2024) | $120–150M |

| Cash flow from platforms (2024–25) | $400–450M |

Preview = Final Product

SL Green BCG Matrix

The file you're previewing is the exact SL Green BCG Matrix report you'll receive after purchase—fully formatted, no watermarks or demo placeholders, and ready for strategic use. This preview mirrors the final document delivered to your inbox, crafted with market-backed analysis and professional design. Upon purchase you'll get the editable, print-ready file immediately, ideal for presentations, planning, or client work. No surprises—just the complete, analysis-ready matrix.