SL Green Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

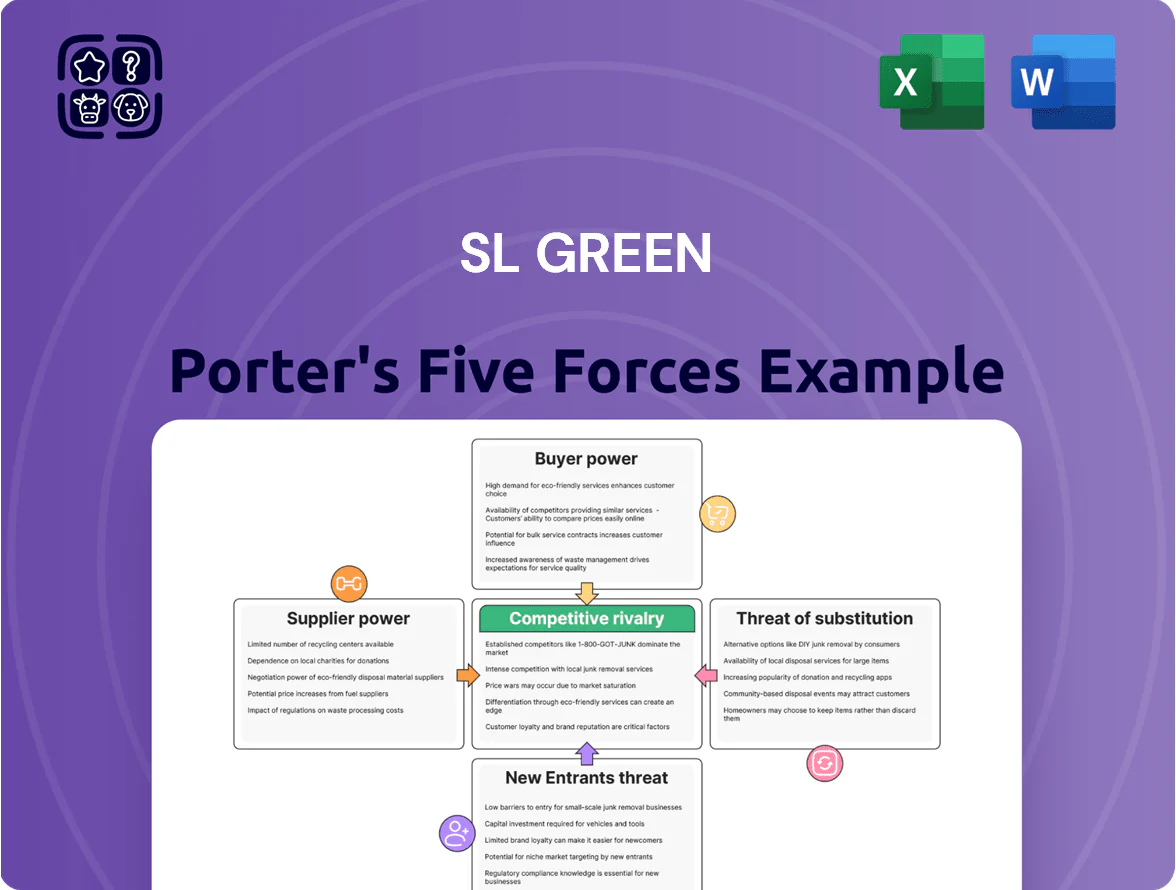

SL Green faces moderate buyer power and fragmented supplier influence, strong rivalry in NYC office markets, limited threat from substitutes but growing remote-work pressure, and high barriers deterring new entrants; strategic positioning hinges on asset mix and leasing agility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SL Green’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized construction labor

The pool of high-end contractors and unionized skilled labor for Manhattan skyscrapers is tight—NYC construction union membership rose to about 140,000 in 2024, concentrating bargaining power with a few firms and trades. This lets unions and specialists push wages: average construction wages in Manhattan hit roughly $62/hour in 2024, pressuring rehab margins. SL Green must control labor-driven cost inflation to protect returns on its $1.5B+ Midtown redevelopment pipeline.

Influence of debt and equity capital providers

As a REIT, SL Green Realty Corp. depends heavily on external financing from major investment banks and institutional investors to fund acquisitions and capex, with $1.8 billion of secured debt and $2.2 billion of unsecured debt on the balance sheet as of Q3 2025.

Strong lender relationships lower execution risk, but the company’s cost of capital—weighted average cost of capital near 7.4% in 2025—tracks macro interest rates and credit spreads.

By late 2025, rate stabilization reduced short-term refinancing pressure, making banks and institutional lenders key partners in SL Green’s deleveraging plan to cut net debt/EBITDA toward a 6x target and support selective growth.

Regulatory and municipal oversight

New York City agencies control development rights and zoning approvals, giving them outsized supplier power over SL Green; for example, DOB approvals and zoning variances can delay projects and add millions—permitting costs averaged $2.1M per large commercial project in 2023.

Local Law 97 (2019), tightened through 2024 targets, forces REITs to cut emissions or pay penalties up to $268 per metric ton CO2e, pushing SL Green to buy upgrades from a limited set of certified green vendors.

Compliance is non-negotiable and raises operating costs: SL Green estimated $500M–$1B portfolio retrofit needs by 2030, so municipal rules effectively set price and vendor choice, increasing supplier leverage.

Utility and energy service monopolies

Electricity and heating in Manhattan are dominated by Consolidated Edison (Con Edison) and a few large providers, leaving SL Green largely a price taker for grid energy; in 2024 Con Edison served ~3.4 million customers in NYC, limiting SL Green’s negotiating leverage.

To cut exposure SL Green reported investing $150 million through 2024 in on-site co-generation, combined heat and power (CHP), and efficiency projects, lowering portfolio energy use by ~12% year-over-year.

- Major provider: Con Edison ~3.4M NYC customers (2024)

- SL Green energy capex: $150M through 2024

- Portfolio energy reduction: ~12% YoY

- Role: price taker for grid rates

Technology and PropTech platform providers

Modern Class A office ops for SL Green rely on a few PropTech leaders for access control, HVAC automation, and tenant apps; Gartner-style estimates show top vendors serve >60% of large US CRE portfolios as of 2025.

As SL Green digitizes Midtown assets, proprietary integrations raise switching costs—implementations often cost $0.5–2.0M and 6–12 months—giving vendors moderate bargaining power.

Vendors can push price increases tied to SaaS fees (5–15% CAGR) and data services, but SL Green’s scale (>$20B NYC portfolio AUM in 2024) mitigates full vendor dominance.

- Top vendors cover >60% of large CRE portfolios (2025)

- Typical switch: $0.5–2.0M and 6–12 months

- SaaS pricing growth 5–15% CAGR

- SL Green AUM >$20B (2024) limits vendor leverage

Supplier leverage boosts SL Green costs: wages, $500M–$1B retrofits, $4B debt

Suppliers—unions, lenders, NYC agencies, Con Edison, and specialized PropTech/green vendors—hold moderate-to-high bargaining power, driving wage and retrofit costs (construction wages ~$62/hr, retrofit need $500M–$1B) and setting financing and utility terms (WACC ~7.4%, debt ~$4.0B). SL Green’s scale and $150M energy capex reduce but don’t eliminate supplier leverage.

| Item | Key number |

|---|---|

| Construction wage (Manhattan 2024) | $62/hr |

| Retrofit need by 2030 | $500M–$1B |

| Debt (Q3 2025) | $4.0B |

| WACC (2025) | 7.4% |

| Energy capex | $150M |

What is included in the product

Tailored Porter's Five Forces analysis for SL Green that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats to its Manhattan-focused office portfolio, with strategic commentary suitable for investor decks and internal strategy use.

Condensed Porter's Five Forces view for SL Green—instantly spot where pricing power, tenant bargaining, or new entrants threaten margins and make faster, smarter leasing or investment decisions.

Customers Bargaining Power

Consolidation of large financial and tech tenants

A significant share of SL Green Realty Corp.’s rent (about 40% of 2024 cash rent) comes from a handful of large financial and tech tenants, giving those high-credit customers leverage to extract lower rents and bigger tenant improvement allowances—average TI per lease renewal climbed to ~$120–150 per sq ft in 2024. Their ability to relocate entire workforces means SL Green faces concentrated renewal risk and bargaining pressure on lease length, rent escalations, and concessions.

Increased demand for flexible lease structures

By end-2025, 72% of corporate tenants report standardized hybrid models, pushing demand for shorter leases and scalable space; SL Green must offer modular offices or 3–24 month terms to compete for premium tenants.

Availability of high-quality Class A alternatives

The surge of projects like Hudson Yards and Midtown renovations raised NYC Class A vacancy to about 12.5% in 2024, giving tenants strong leverage to demand concessions from landlords including SL Green (NYSE: SLG). Tenants routinely extract 6–18 months free rent or higher TI (tenant improvement) allowances, pressuring SL Green to match offers. SL Green must invest—its 2024 capital expenditures were $480M—to keep amenities fresh and reduce churn risk.

Flight to quality and sustainability standards

Sophisticated tenants now prefer buildings with top wellness certifications and LEED ratings; 2024 data shows 62% of Fortune 500 firms factor ESG in real estate decisions, pushing SL Green to prioritize green assets.

Tenants can insist on measured environmental performance—energy use intensity, carbon reporting, EV charging—and make lease approval conditional on those features, raising SL Green’s compliance costs but reducing vacancy risk.

Selective tenant behavior gives customers leverage to set space standards and negotiate rents, forcing SL Green to match or exceed market sustainability benchmarks to retain premium tenants.

- 62% Fortune 500 cite ESG in real estate (2024)

- Tenants demand EUI and carbon data in leases

- Green features lower vacancy but raise capex

Economic sensitivity of small to mid-sized firms

Smaller professional firms in SL Green’s Manhattan portfolio are highly price-sensitive; surveys show 40–55% of small tenants consider relocating if rents rise more than 10% year-over-year, so SL Green cannot push uniform rent hikes without higher vacancy risk.

In 2025 SL Green’s core Manhattan effective rent growth target of mid-single digits clashes with submarket moves to outer boroughs offering 20–40% lower rents, capping upside on lower-tier floors.

- 40–55% small tenants consider move if rents +10%

- Outer-borough rents 20–40% lower than Manhattan (2024–25 data)

- Limits portfolio-wide rent increases to mid-single digits

Large tenants & rising vacancy force big concessions, capping SL Green rent gains

Large, creditworthy tenants (≈40% of 2024 cash rent) and rising NYC Class A vacancy (~12.5% in 2024) give customers strong bargaining power, forcing higher TI (~$120–150/sq ft in 2024), 6–18 months free rent, shorter leases, and ESG requirements (62% Fortune 500 cite ESG in 2024), capping SL Green’s rent hikes to mid-single digits.

| Metric | 2024–25 Value |

|---|---|

| Share from large tenants | ≈40% cash rent |

| Class A vacancy NYC | ≈12.5% |

| Avg TI per renewal | $120–150/sq ft |

| Tenant concessions | 6–18 months free rent |

| Fortune 500 ESG | 62% |

What You See Is What You Get

SL Green Porter's Five Forces Analysis

This preview shows the exact SL Green Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

SL Green faces moderate buyer power and fragmented supplier influence, strong rivalry in NYC office markets, limited threat from substitutes but growing remote-work pressure, and high barriers deterring new entrants; strategic positioning hinges on asset mix and leasing agility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SL Green’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized construction labor

The pool of high-end contractors and unionized skilled labor for Manhattan skyscrapers is tight—NYC construction union membership rose to about 140,000 in 2024, concentrating bargaining power with a few firms and trades. This lets unions and specialists push wages: average construction wages in Manhattan hit roughly $62/hour in 2024, pressuring rehab margins. SL Green must control labor-driven cost inflation to protect returns on its $1.5B+ Midtown redevelopment pipeline.

Influence of debt and equity capital providers

As a REIT, SL Green Realty Corp. depends heavily on external financing from major investment banks and institutional investors to fund acquisitions and capex, with $1.8 billion of secured debt and $2.2 billion of unsecured debt on the balance sheet as of Q3 2025.

Strong lender relationships lower execution risk, but the company’s cost of capital—weighted average cost of capital near 7.4% in 2025—tracks macro interest rates and credit spreads.

By late 2025, rate stabilization reduced short-term refinancing pressure, making banks and institutional lenders key partners in SL Green’s deleveraging plan to cut net debt/EBITDA toward a 6x target and support selective growth.

Regulatory and municipal oversight

New York City agencies control development rights and zoning approvals, giving them outsized supplier power over SL Green; for example, DOB approvals and zoning variances can delay projects and add millions—permitting costs averaged $2.1M per large commercial project in 2023.

Local Law 97 (2019), tightened through 2024 targets, forces REITs to cut emissions or pay penalties up to $268 per metric ton CO2e, pushing SL Green to buy upgrades from a limited set of certified green vendors.

Compliance is non-negotiable and raises operating costs: SL Green estimated $500M–$1B portfolio retrofit needs by 2030, so municipal rules effectively set price and vendor choice, increasing supplier leverage.

Utility and energy service monopolies

Electricity and heating in Manhattan are dominated by Consolidated Edison (Con Edison) and a few large providers, leaving SL Green largely a price taker for grid energy; in 2024 Con Edison served ~3.4 million customers in NYC, limiting SL Green’s negotiating leverage.

To cut exposure SL Green reported investing $150 million through 2024 in on-site co-generation, combined heat and power (CHP), and efficiency projects, lowering portfolio energy use by ~12% year-over-year.

- Major provider: Con Edison ~3.4M NYC customers (2024)

- SL Green energy capex: $150M through 2024

- Portfolio energy reduction: ~12% YoY

- Role: price taker for grid rates

Technology and PropTech platform providers

Modern Class A office ops for SL Green rely on a few PropTech leaders for access control, HVAC automation, and tenant apps; Gartner-style estimates show top vendors serve >60% of large US CRE portfolios as of 2025.

As SL Green digitizes Midtown assets, proprietary integrations raise switching costs—implementations often cost $0.5–2.0M and 6–12 months—giving vendors moderate bargaining power.

Vendors can push price increases tied to SaaS fees (5–15% CAGR) and data services, but SL Green’s scale (>$20B NYC portfolio AUM in 2024) mitigates full vendor dominance.

- Top vendors cover >60% of large CRE portfolios (2025)

- Typical switch: $0.5–2.0M and 6–12 months

- SaaS pricing growth 5–15% CAGR

- SL Green AUM >$20B (2024) limits vendor leverage

Supplier leverage boosts SL Green costs: wages, $500M–$1B retrofits, $4B debt

Suppliers—unions, lenders, NYC agencies, Con Edison, and specialized PropTech/green vendors—hold moderate-to-high bargaining power, driving wage and retrofit costs (construction wages ~$62/hr, retrofit need $500M–$1B) and setting financing and utility terms (WACC ~7.4%, debt ~$4.0B). SL Green’s scale and $150M energy capex reduce but don’t eliminate supplier leverage.

| Item | Key number |

|---|---|

| Construction wage (Manhattan 2024) | $62/hr |

| Retrofit need by 2030 | $500M–$1B |

| Debt (Q3 2025) | $4.0B |

| WACC (2025) | 7.4% |

| Energy capex | $150M |

What is included in the product

Tailored Porter's Five Forces analysis for SL Green that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats to its Manhattan-focused office portfolio, with strategic commentary suitable for investor decks and internal strategy use.

Condensed Porter's Five Forces view for SL Green—instantly spot where pricing power, tenant bargaining, or new entrants threaten margins and make faster, smarter leasing or investment decisions.

Customers Bargaining Power

Consolidation of large financial and tech tenants

A significant share of SL Green Realty Corp.’s rent (about 40% of 2024 cash rent) comes from a handful of large financial and tech tenants, giving those high-credit customers leverage to extract lower rents and bigger tenant improvement allowances—average TI per lease renewal climbed to ~$120–150 per sq ft in 2024. Their ability to relocate entire workforces means SL Green faces concentrated renewal risk and bargaining pressure on lease length, rent escalations, and concessions.

Increased demand for flexible lease structures

By end-2025, 72% of corporate tenants report standardized hybrid models, pushing demand for shorter leases and scalable space; SL Green must offer modular offices or 3–24 month terms to compete for premium tenants.

Availability of high-quality Class A alternatives

The surge of projects like Hudson Yards and Midtown renovations raised NYC Class A vacancy to about 12.5% in 2024, giving tenants strong leverage to demand concessions from landlords including SL Green (NYSE: SLG). Tenants routinely extract 6–18 months free rent or higher TI (tenant improvement) allowances, pressuring SL Green to match offers. SL Green must invest—its 2024 capital expenditures were $480M—to keep amenities fresh and reduce churn risk.

Flight to quality and sustainability standards

Sophisticated tenants now prefer buildings with top wellness certifications and LEED ratings; 2024 data shows 62% of Fortune 500 firms factor ESG in real estate decisions, pushing SL Green to prioritize green assets.

Tenants can insist on measured environmental performance—energy use intensity, carbon reporting, EV charging—and make lease approval conditional on those features, raising SL Green’s compliance costs but reducing vacancy risk.

Selective tenant behavior gives customers leverage to set space standards and negotiate rents, forcing SL Green to match or exceed market sustainability benchmarks to retain premium tenants.

- 62% Fortune 500 cite ESG in real estate (2024)

- Tenants demand EUI and carbon data in leases

- Green features lower vacancy but raise capex

Economic sensitivity of small to mid-sized firms

Smaller professional firms in SL Green’s Manhattan portfolio are highly price-sensitive; surveys show 40–55% of small tenants consider relocating if rents rise more than 10% year-over-year, so SL Green cannot push uniform rent hikes without higher vacancy risk.

In 2025 SL Green’s core Manhattan effective rent growth target of mid-single digits clashes with submarket moves to outer boroughs offering 20–40% lower rents, capping upside on lower-tier floors.

- 40–55% small tenants consider move if rents +10%

- Outer-borough rents 20–40% lower than Manhattan (2024–25 data)

- Limits portfolio-wide rent increases to mid-single digits

Large tenants & rising vacancy force big concessions, capping SL Green rent gains

Large, creditworthy tenants (≈40% of 2024 cash rent) and rising NYC Class A vacancy (~12.5% in 2024) give customers strong bargaining power, forcing higher TI (~$120–150/sq ft in 2024), 6–18 months free rent, shorter leases, and ESG requirements (62% Fortune 500 cite ESG in 2024), capping SL Green’s rent hikes to mid-single digits.

| Metric | 2024–25 Value |

|---|---|

| Share from large tenants | ≈40% cash rent |

| Class A vacancy NYC | ≈12.5% |

| Avg TI per renewal | $120–150/sq ft |

| Tenant concessions | 6–18 months free rent |

| Fortune 500 ESG | 62% |

What You See Is What You Get

SL Green Porter's Five Forces Analysis

This preview shows the exact SL Green Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.