Smartbox Group Limited Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

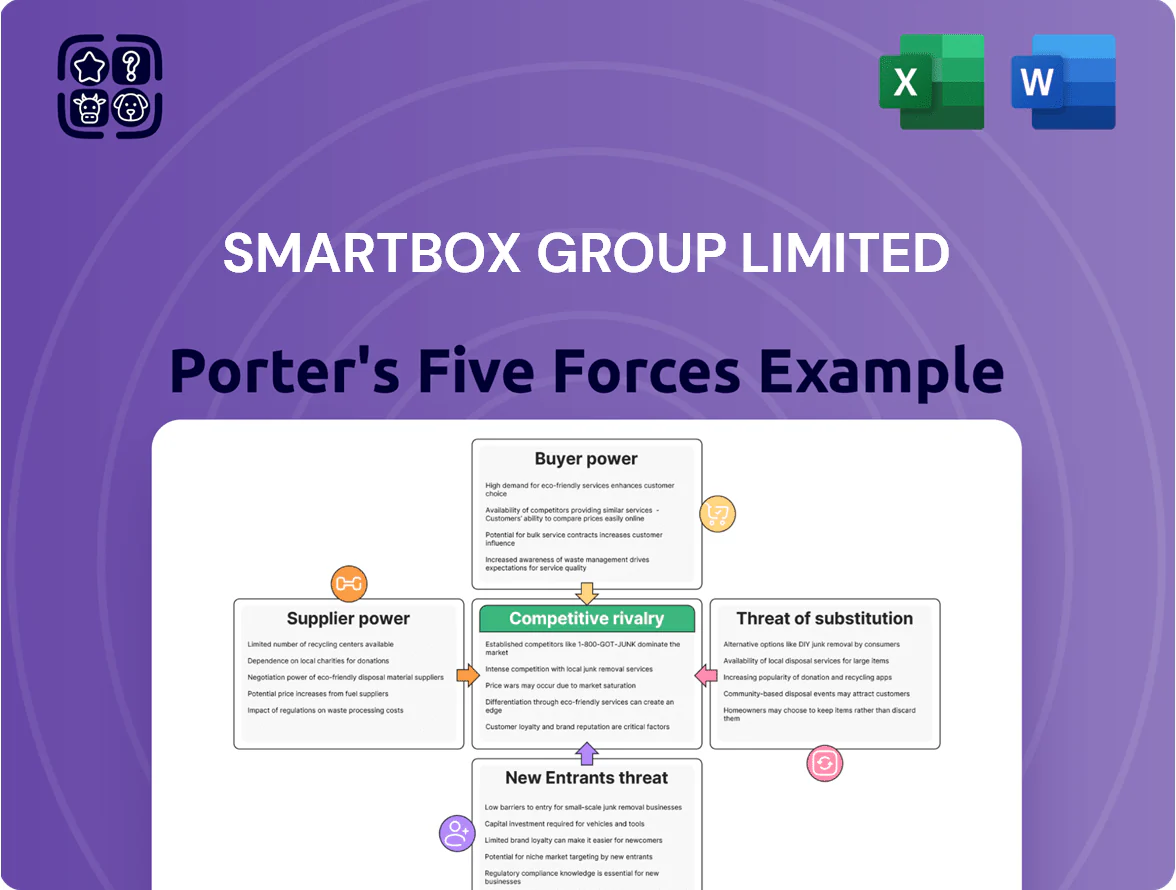

Smartbox Group Limited faces moderate buyer power and substitution risk amid a niche gifting market, while supplier leverage and new entrants remain contained by brand recognition and distribution partnerships; competitive rivalry, however, is intensifying as digital platforms expand. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smartbox Group Limited’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of Service Providers

The vast network of small and medium providers—local spas, independent restaurants, boutique hotels—reduces supplier leverage over Smartbox: individual partners lack scale and global marketing budgets and depend on Smartbox for customer acquisition.

With over 12,000 listed partners in 2024 across Europe, thousands of replacements exist, letting Smartbox swap non-compliant providers with little disruption to its core product.

That fragmentation gives Smartbox the upper hand in most contractual negotiations, pressuring margins and terms in its favor.

Value of Incremental Revenue

Suppliers treat Smartbox Group Limited as a channel to fill excess capacity in off-peak periods, so even with commission rates around 15–25% reported in 2024, the incremental revenue is highly valuable to them.

Marginal cost per additional guest for short-stay and experience providers is often under 10% of revenue, so suppliers accept thinner margins for guaranteed volume.

As a result, Smartbox faces limited downward pressure on its take-rate across its broad supplier base, supported by occupancy uplifts of 5–20% in published partner case studies.

Brand Exposure and Marketing Reach

Featuring in a Smartbox gift set gives many local suppliers high-visibility advertising they couldn’t otherwise afford: Smartbox provided professional photos, translations, and placement in major retailers like Fnac-Darty and John Lewis in 2024, reaching ~12 million shoppers across channels. This boosts supplier brand prestige and long-term equity beyond the sale, so suppliers accept weaker pricing or terms because the non-monetary marketing value is substantial.

Standardization of Service Agreements

Smartbox enforces standardized, take-it-or-leave-it service agreements that block supplier negotiation on terms or pricing, leveraging control of its digital distribution and in-store shelf placement.

Because Smartbox reached ~£120m revenue in 2024 and services millions of gift buyers, suppliers must meet its operational specs to access that market, keeping supplier bargaining weak and admin low.

- Standard contracts limit negotiation

- Platform + retail shelf control = leverage

- £120m 2024 revenue backs market access power

- Operational rules reduce supplier influence

Switching Costs for Partners

Smartbox’s integrated booking API and staff training create real switching costs: suppliers listed elsewhere face a week+ integration and retraining cost, and Smartbox reports ~65% of redemptions via its digital tools in 2024, boosting stickiness.

Moving exclusively to a competitor risks losing pre-paid revenue — Smartbox held ~£120m in outstanding voucher liability at FY2024 — and years of customer redemption data, so supplier bargaining power remains limited.

- Integration/time cost: week+ per partner

- Digital redemptions: ~65% (2024)

- Outstanding vouchers: ~£120m (FY2024)

- Data loss risk reduces switching

Smartbox’s scale and reach mute suppliers—12k partners, £120m revenue, ~12m shoppers

Suppliers have weak bargaining power: 12,000+ partners (2024), fragmented small-scale base, and Smartbox’s £120m 2024 revenue and voucher liability give distribution leverage; standard contracts, API integration (week+), ~65% digital redemptions and marketing reach (~12m shoppers via Fnac-Darty/John Lewis) keep take-rates at ~15–25% and limit supplier negotiation.

| Metric | 2024 |

|---|---|

| Partners | 12,000+ |

| Revenue | £120m |

| Digital redemptions | ~65% |

| Take-rate | 15–25% |

| Retail reach | ~12m shoppers |

What is included in the product

Tailored Porter's Five Forces analysis for Smartbox Group Limited, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive forces and strategic levers that impact its pricing, profitability, and market positioning.

A concise one-sheet Porter's Five Forces summary for Smartbox Group Ltd—ideal for rapid strategic decisions and slide-ready boardroom use.

Customers Bargaining Power

Low Switching Costs for Individual Buyers

Retail buyers face almost zero switching costs between Smartbox and rivals like Wonderbox or local providers; with a few clicks or a different kiosk choice they chase the best promo, driving price sensitivity—UK price promos lifted gift-box sales 18% in 2024, per industry data—so loyalty often yields to perceived value. Smartbox must refresh packaging and add 10–15% new experiences yearly to hold share against this fluid demand.

Information Transparency and Price Comparison

The digital gift market lets customers compare Smartbox Group Limited boxes and prices instantly; in 2024, 62% of UK shoppers used price comparison before buying gift experiences, raising switching risk.

Review sites and social media (Trustpilot, Instagram) transmit quality signals in real time; Smartbox’s Net Promoter Score drop of 8 points in 2023 after a product issue shows rapid reputational impact.

Poor ratings drive quick migration—industry data show 45% of consumers abandon brands after two negative reviews—forcing Smartbox to respond fast to feedback and adjust offerings monthly.

B2B Client Leverage

Corporate clients buying experience gifts in bulk wield high leverage over Smartbox Group Limited; in 2024 B2B sales accounted for about 38% of UK and France revenue, letting buyers demand volume discounts, custom branding, and exclusive terms unavailable to retail customers.

Smartbox often concedes pricing and service SLAs to retain large accounts—loss of a single global corporate contract (worth ~£4–6m annually) can cut regional EBITDA by 3–7% and materially pressure cash flow.

Availability of Direct Booking Options

Recipients increasingly spot better deals or flexible dates by booking directly, which caps Smartbox Group Limited’s ability to charge premiums for curation and packaging.

If the price gap exceeds roughly 20–30%—industry studies in 2024 show many consumers abandon intermediaries at that range—perceived value drops and churn rises.

Customers then bypass Smartbox, exercising bargaining power by choosing the direct, cheaper option; Smartbox must tighten margins or add non-price value.

- Direct-booking awareness up; >30% of gift recipients compare prices (2024 survey)

- Price gap elasticity: ~20–30% trigger bypass

- Response: focus on exclusive partners, experience add-ons

Demand for Digital Flexibility

Modern consumers demand instant gratification and frictionless voucher exchanges, pushing power to buyers who favor platforms with top mobile UX and flexible policies; 72% of UK consumers (2024 Deloitte) prefer brands that offer real-time digital exchanges.

Smartbox has invested ~£15m since 2022 in digital infrastructure and mobile apps to reduce churn; without seamless UX it risks immediate defections to tech-native rivals growing 18% CAGR (2021–24).

- 72% UK prefer real-time exchange (Deloitte 2024)

- Smartbox digital spend ≈ £15m (2022–25)

- Rivals’ revenue CAGR 18% (2021–24)

High customer power: 62% compare, B2B discounts cut EBITDA 3–7%; £15m UX spend

Customers hold strong bargaining power: low switching costs and 62% comparison shopping (UK, 2024) drive price sensitivity; B2B buyers (≈38% revenue, 2024) extract discounts that can cut regional EBITDA 3–7% per lost contract; UX and direct-booking awareness (>30% compare, 2024) force Smartbox to invest (~£15m since 2022) to avoid churn.

| Metric | 2024 value |

|---|---|

| Retail comparison rate | 62% |

| B2B revenue share | ≈38% |

| Digital spend (2022–25) | ≈£15m |

| EBITDA hit per lost contract | 3–7% |

Full Version Awaits

Smartbox Group Limited Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Smartbox Group Limited you will receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Smartbox Group Limited faces moderate buyer power and substitution risk amid a niche gifting market, while supplier leverage and new entrants remain contained by brand recognition and distribution partnerships; competitive rivalry, however, is intensifying as digital platforms expand. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smartbox Group Limited’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of Service Providers

The vast network of small and medium providers—local spas, independent restaurants, boutique hotels—reduces supplier leverage over Smartbox: individual partners lack scale and global marketing budgets and depend on Smartbox for customer acquisition.

With over 12,000 listed partners in 2024 across Europe, thousands of replacements exist, letting Smartbox swap non-compliant providers with little disruption to its core product.

That fragmentation gives Smartbox the upper hand in most contractual negotiations, pressuring margins and terms in its favor.

Value of Incremental Revenue

Suppliers treat Smartbox Group Limited as a channel to fill excess capacity in off-peak periods, so even with commission rates around 15–25% reported in 2024, the incremental revenue is highly valuable to them.

Marginal cost per additional guest for short-stay and experience providers is often under 10% of revenue, so suppliers accept thinner margins for guaranteed volume.

As a result, Smartbox faces limited downward pressure on its take-rate across its broad supplier base, supported by occupancy uplifts of 5–20% in published partner case studies.

Brand Exposure and Marketing Reach

Featuring in a Smartbox gift set gives many local suppliers high-visibility advertising they couldn’t otherwise afford: Smartbox provided professional photos, translations, and placement in major retailers like Fnac-Darty and John Lewis in 2024, reaching ~12 million shoppers across channels. This boosts supplier brand prestige and long-term equity beyond the sale, so suppliers accept weaker pricing or terms because the non-monetary marketing value is substantial.

Standardization of Service Agreements

Smartbox enforces standardized, take-it-or-leave-it service agreements that block supplier negotiation on terms or pricing, leveraging control of its digital distribution and in-store shelf placement.

Because Smartbox reached ~£120m revenue in 2024 and services millions of gift buyers, suppliers must meet its operational specs to access that market, keeping supplier bargaining weak and admin low.

- Standard contracts limit negotiation

- Platform + retail shelf control = leverage

- £120m 2024 revenue backs market access power

- Operational rules reduce supplier influence

Switching Costs for Partners

Smartbox’s integrated booking API and staff training create real switching costs: suppliers listed elsewhere face a week+ integration and retraining cost, and Smartbox reports ~65% of redemptions via its digital tools in 2024, boosting stickiness.

Moving exclusively to a competitor risks losing pre-paid revenue — Smartbox held ~£120m in outstanding voucher liability at FY2024 — and years of customer redemption data, so supplier bargaining power remains limited.

- Integration/time cost: week+ per partner

- Digital redemptions: ~65% (2024)

- Outstanding vouchers: ~£120m (FY2024)

- Data loss risk reduces switching

Smartbox’s scale and reach mute suppliers—12k partners, £120m revenue, ~12m shoppers

Suppliers have weak bargaining power: 12,000+ partners (2024), fragmented small-scale base, and Smartbox’s £120m 2024 revenue and voucher liability give distribution leverage; standard contracts, API integration (week+), ~65% digital redemptions and marketing reach (~12m shoppers via Fnac-Darty/John Lewis) keep take-rates at ~15–25% and limit supplier negotiation.

| Metric | 2024 |

|---|---|

| Partners | 12,000+ |

| Revenue | £120m |

| Digital redemptions | ~65% |

| Take-rate | 15–25% |

| Retail reach | ~12m shoppers |

What is included in the product

Tailored Porter's Five Forces analysis for Smartbox Group Limited, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive forces and strategic levers that impact its pricing, profitability, and market positioning.

A concise one-sheet Porter's Five Forces summary for Smartbox Group Ltd—ideal for rapid strategic decisions and slide-ready boardroom use.

Customers Bargaining Power

Low Switching Costs for Individual Buyers

Retail buyers face almost zero switching costs between Smartbox and rivals like Wonderbox or local providers; with a few clicks or a different kiosk choice they chase the best promo, driving price sensitivity—UK price promos lifted gift-box sales 18% in 2024, per industry data—so loyalty often yields to perceived value. Smartbox must refresh packaging and add 10–15% new experiences yearly to hold share against this fluid demand.

Information Transparency and Price Comparison

The digital gift market lets customers compare Smartbox Group Limited boxes and prices instantly; in 2024, 62% of UK shoppers used price comparison before buying gift experiences, raising switching risk.

Review sites and social media (Trustpilot, Instagram) transmit quality signals in real time; Smartbox’s Net Promoter Score drop of 8 points in 2023 after a product issue shows rapid reputational impact.

Poor ratings drive quick migration—industry data show 45% of consumers abandon brands after two negative reviews—forcing Smartbox to respond fast to feedback and adjust offerings monthly.

B2B Client Leverage

Corporate clients buying experience gifts in bulk wield high leverage over Smartbox Group Limited; in 2024 B2B sales accounted for about 38% of UK and France revenue, letting buyers demand volume discounts, custom branding, and exclusive terms unavailable to retail customers.

Smartbox often concedes pricing and service SLAs to retain large accounts—loss of a single global corporate contract (worth ~£4–6m annually) can cut regional EBITDA by 3–7% and materially pressure cash flow.

Availability of Direct Booking Options

Recipients increasingly spot better deals or flexible dates by booking directly, which caps Smartbox Group Limited’s ability to charge premiums for curation and packaging.

If the price gap exceeds roughly 20–30%—industry studies in 2024 show many consumers abandon intermediaries at that range—perceived value drops and churn rises.

Customers then bypass Smartbox, exercising bargaining power by choosing the direct, cheaper option; Smartbox must tighten margins or add non-price value.

- Direct-booking awareness up; >30% of gift recipients compare prices (2024 survey)

- Price gap elasticity: ~20–30% trigger bypass

- Response: focus on exclusive partners, experience add-ons

Demand for Digital Flexibility

Modern consumers demand instant gratification and frictionless voucher exchanges, pushing power to buyers who favor platforms with top mobile UX and flexible policies; 72% of UK consumers (2024 Deloitte) prefer brands that offer real-time digital exchanges.

Smartbox has invested ~£15m since 2022 in digital infrastructure and mobile apps to reduce churn; without seamless UX it risks immediate defections to tech-native rivals growing 18% CAGR (2021–24).

- 72% UK prefer real-time exchange (Deloitte 2024)

- Smartbox digital spend ≈ £15m (2022–25)

- Rivals’ revenue CAGR 18% (2021–24)

High customer power: 62% compare, B2B discounts cut EBITDA 3–7%; £15m UX spend

Customers hold strong bargaining power: low switching costs and 62% comparison shopping (UK, 2024) drive price sensitivity; B2B buyers (≈38% revenue, 2024) extract discounts that can cut regional EBITDA 3–7% per lost contract; UX and direct-booking awareness (>30% compare, 2024) force Smartbox to invest (~£15m since 2022) to avoid churn.

| Metric | 2024 value |

|---|---|

| Retail comparison rate | 62% |

| B2B revenue share | ≈38% |

| Digital spend (2022–25) | ≈£15m |

| EBITDA hit per lost contract | 3–7% |

Full Version Awaits

Smartbox Group Limited Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Smartbox Group Limited you will receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready for download and use.