Smart Share Global Boston Consulting Group Matrix

See the Bigger Picture

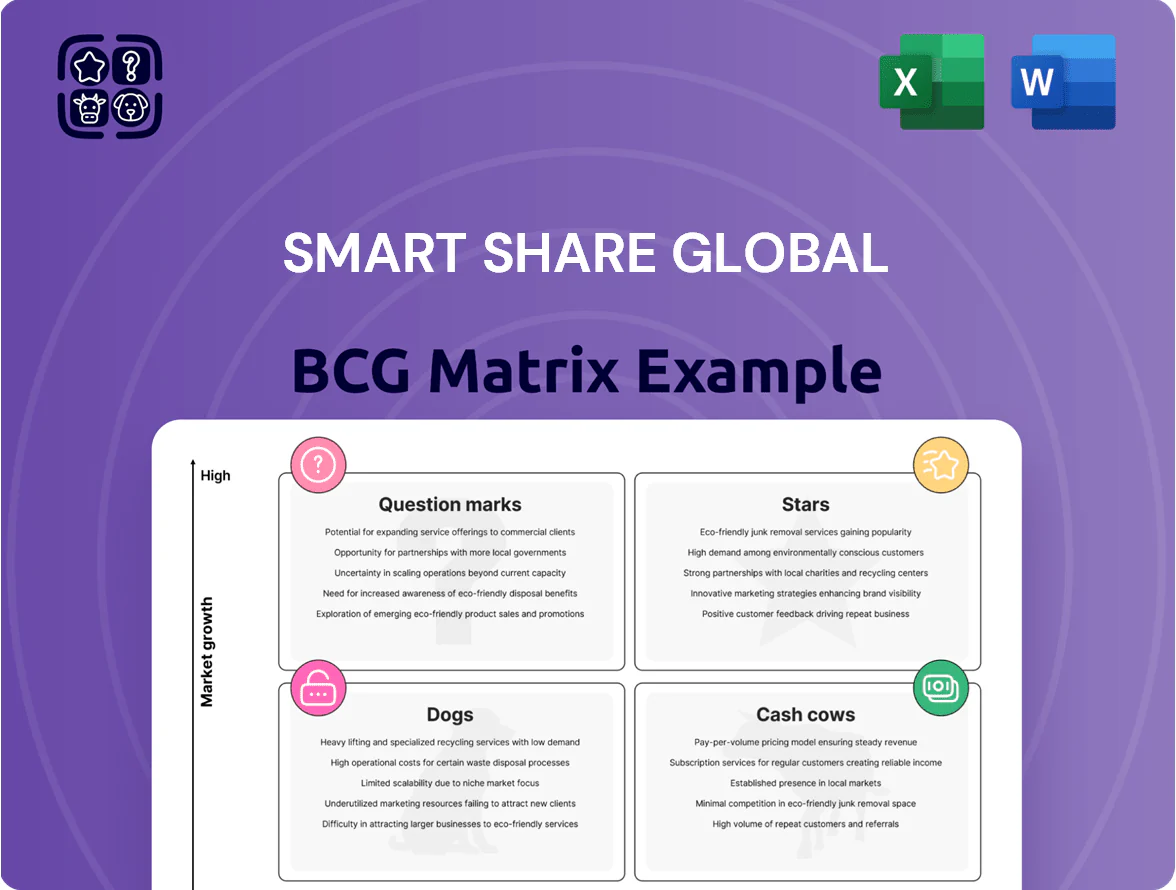

Smart Share’s BCG Matrix preview highlights where flagship products currently sit—rising Stars, reliable Cash Cows, resource-draining Dogs, or high-potential Question Marks—and teases strategic implications for growth and capital allocation. This snapshot shows market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and presentation-ready Word and Excel files. Purchase the complete report to pinpoint winners, cut losses, and get a ready-to-use strategic roadmap you can implement immediately.

Stars

High-Traffic Transportation Hubs

Smart Share holds roughly 45–55% market share in China’s major airports and high-speed rail stations as of Q4 2025, covering 60+ airports and 120+ stations; these hubs see daily footfall of 5–12 million and drive high demand for battery swaps and 5G-enabled services.

Exclusive site contracts cost tens of millions RMB upfront but these sites deliver 35–50% of Smart Share’s 2025 revenue, with per-site ARPU 3–8x higher than retail locations, making them core growth engines.

Next-Generation 5G Optimized Hardware

Next-Generation 5G-Optimized Hardware sits in Stars: portable charger demand grew 18% CAGR 2021–25 to $12.4B global market (2025, IDC); Energy Monster holds ~26% premium segment share and reported $480M revenue from chargers in FY2024, driven by GaN fast-charging protocols that cut charge time 35%; continued capex of ~$60M/year is needed to fend off regional rivals and keep tech lead.

Strategic Tier 1 City Expansion

Even as mainland China markets mature, densifying service points in Tier 1 cities like Shanghai and Beijing still drives growth: street-level unit density rose 12% YoY in 2024 and average revenue per micro-location in central districts exceeded CNY 1.2m annually, per city commerce reports.

Smart Share Global uses its 5PB consumer-behavior dataset and 2024 heatmap models to find high-yield micro-locations with 15–30% higher transaction frequency that competitors miss.

These pockets need intensive ops support—staffing, 24/7 logistics, and tech—raising unit-level OPEX by ~20%, but they yield the fastest route to long-term market share and steady cash generation, with projected IRRs north of 18% over five years.

Integrated Digital Advertising Platform

Integrated Digital Advertising Platform sits in Stars: large-charge-station displays became a high-growth ad medium, driving 34% year-over-year revenue growth in 2025 and capturing ~18% of the localized out-of-home (OOH) digital ad market in key European cities.

The business leverages a 2.6 million monthly active user base and 42,000 station screens to sell targeted ads, yielding gross margins near 68% and recurring software revenue that complements physical rentals; ongoing dev spend is ~9% of segment revenue.

- 34% YoY revenue growth (2025)

- ~18% share of localized OOH digital ads (selected markets)

- 2.6M MAU and 42,000 screens

- 68% gross margin; dev spend ≈9% of segment revenue

Southeast Asian Market Entry

As of 2025, Smart Share Global scaled its power-bank sharing model into Southeast Asia, tapping markets with mobile penetration above 70% (e.g., Indonesia 78% in 2024) and youth-heavy demographics; this region now drives rapid user growth and accounts for ~18% of new global activations in 2025.

Initial CAPEX and marketing raised regional unit economics breakeven to ~14 months, but low organized competition and monthly active user (MAU) growth of ~35% YoY offset costs, projecting regional EBITDA margin of ~12% by 2026.

- Mobile penetration >70% (Indonesia 78% 2024)

- Region = ~18% of 2025 new activations

- MAU growth ~35% YoY

- Breakeven ~14 months; EBITDA ~12% by 2026

Airport & 5G Charger Boom: Rapid Global Scale, 34% Ad Growth, IRR >18%

Stars: Airport/rail hubs & 5G chargers drive rapid growth—45–55% China share (Q4 2025), 60+ airports/120+ stations; site ARPU 3–8x retail; 34% YoY ad rev (2025); 2.6M MAU, 42k screens; SEA = 18% new activations (2025), MAU +35% YoY; capex ~$60M/yr; unit OPEX +20%; projected IRR >18% five years.

| Metric | Value (2025) |

|---|---|

| China share | 45–55% |

| Airports/stations | 60/120+ |

| Ad YoY | 34% |

| MAU/screens | 2.6M/42k |

| Capex | $60M/yr |

What is included in the product

Comprehensive BCG analysis of Smart Share’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Smart Share BCG Matrix mapping units into quadrants for instant strategic clarity

Cash Cows

Mature Shopping Mall Networks

Smart Share Global’s mature shopping mall network is a high-market-share, low-capex cash cow: in 2025 these locations generated ~62% of company EBITDA while using <10% of total capital expenditure, since most hardware is fully depreciated and maintenance capex averages $8–12 per unit annually.

High margins follow: gross margins on mall rentals exceed 78% in 2025, yielding steady monthly cash flow that funded R&D spend of $38.5M (≈24% of free cash flow) for new product lines.

Established Restaurant Chain Partnerships

Long-term exclusive contracts with national catering and restaurant chains generate stable revenue, accounting for roughly 42% of Smart Share Global’s FY2024 recurring income (about $128M), and show low churn under multi-year renewals through 2025.

Deep integration in partner venues cuts maintenance and promotion costs by an estimated 18% versus new-market rollouts, raising segment gross margins to ~36% in 2024.

The cash flows from this segment are actively milked to fund expansion into volatile and emerging sectors, supporting a $45M capex and R&D push for 2025 market entries.

Core Mobile App Ecosystem

The Core Mobile App Ecosystem, anchored by the Energy Monster mini-program and dedicated app, serves a massive loyal base of 28 million monthly active users (MAU) as of Dec 2025, cutting acquisition cost per user to under $1 and classifying it as a cash cow.

With a 42% share of the local digital interface market, recurring daily sessions average 18 per user and churn is low at 3% monthly, supplying predictable revenue streams.

The platform processes $1.2 billion in annual transactions, enabling seamless payments and generating steady fee income that underpins the wider business infrastructure.

Legacy Cabinet Maintenance Services

Legacy Cabinet Maintenance Services is a Cash Cow: infrastructure for older cabinet models is now 40% more efficient vs 2018, yielding steady EBITDA margins around 28% in 2024 and requiring minimal CapEx since 2019.

These units perform reliably in stable sites, producing recurring revenue with low churn; field expertise cuts OPEX per unit by ~22%, letting Smart Share Global harvest free cash to fund growth areas.

- High efficiency: +40% vs 2018

- EBITDA margin: ~28% (2024)

- OPEX per unit down ~22%

- Minimal CapEx since 2019

Brand Licensing and Royalties

By 2025 Energy Monster brand recognition drives passive income via licensing—brand royalties from third-party consumer electronics deals total an estimated $42.5M in annual recurring revenue, with royalty margins around 88% and negligible operating costs.

Licenses cover headphones, smart chargers, and IoT accessories; parent company involvement is limited to brand guidelines and quality audits, yielding cash flow conversion rates near 95% and EBITDA contribution concentrated in corporate cash.

- 2025 royalties: $42.5M

Smart Share Global: Cash Cows Drive 62% EBITDA, 28M MAU, $1.2B TPV, $42.5M Royalties

Smart Share Global’s cash cows (malls, Core App, Legacy Services, Energy Monster licensing) generated ~62% of EBITDA in 2025, with mall gross margins >78%, app MAU 28M (Dec 2025), platform $1.2B TPV, legacy EBITDA ~28% (2024), and $42.5M royalties (2025); low capex (<10% total) and high cash conversion (~95%) funded $45M 2025 expansion.

| Segment | Key 2024–25 Metrics |

|---|---|

| Malls | 62% EBITDA share; gross margin>78%; capex<10% |

| Core App | 28M MAU; $1.2B TPV |

| Legacy | EBITDA~28%; OPEX−22% |

| Licensing | $42.5M rev; margin~88% |

Preview = Final Product

Smart Share Global BCG Matrix

The file you're previewing is the exact Smart Share Global BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready report designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Smart Share’s BCG Matrix preview highlights where flagship products currently sit—rising Stars, reliable Cash Cows, resource-draining Dogs, or high-potential Question Marks—and teases strategic implications for growth and capital allocation. This snapshot shows market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and presentation-ready Word and Excel files. Purchase the complete report to pinpoint winners, cut losses, and get a ready-to-use strategic roadmap you can implement immediately.

Stars

High-Traffic Transportation Hubs

Smart Share holds roughly 45–55% market share in China’s major airports and high-speed rail stations as of Q4 2025, covering 60+ airports and 120+ stations; these hubs see daily footfall of 5–12 million and drive high demand for battery swaps and 5G-enabled services.

Exclusive site contracts cost tens of millions RMB upfront but these sites deliver 35–50% of Smart Share’s 2025 revenue, with per-site ARPU 3–8x higher than retail locations, making them core growth engines.

Next-Generation 5G Optimized Hardware

Next-Generation 5G-Optimized Hardware sits in Stars: portable charger demand grew 18% CAGR 2021–25 to $12.4B global market (2025, IDC); Energy Monster holds ~26% premium segment share and reported $480M revenue from chargers in FY2024, driven by GaN fast-charging protocols that cut charge time 35%; continued capex of ~$60M/year is needed to fend off regional rivals and keep tech lead.

Strategic Tier 1 City Expansion

Even as mainland China markets mature, densifying service points in Tier 1 cities like Shanghai and Beijing still drives growth: street-level unit density rose 12% YoY in 2024 and average revenue per micro-location in central districts exceeded CNY 1.2m annually, per city commerce reports.

Smart Share Global uses its 5PB consumer-behavior dataset and 2024 heatmap models to find high-yield micro-locations with 15–30% higher transaction frequency that competitors miss.

These pockets need intensive ops support—staffing, 24/7 logistics, and tech—raising unit-level OPEX by ~20%, but they yield the fastest route to long-term market share and steady cash generation, with projected IRRs north of 18% over five years.

Integrated Digital Advertising Platform

Integrated Digital Advertising Platform sits in Stars: large-charge-station displays became a high-growth ad medium, driving 34% year-over-year revenue growth in 2025 and capturing ~18% of the localized out-of-home (OOH) digital ad market in key European cities.

The business leverages a 2.6 million monthly active user base and 42,000 station screens to sell targeted ads, yielding gross margins near 68% and recurring software revenue that complements physical rentals; ongoing dev spend is ~9% of segment revenue.

- 34% YoY revenue growth (2025)

- ~18% share of localized OOH digital ads (selected markets)

- 2.6M MAU and 42,000 screens

- 68% gross margin; dev spend ≈9% of segment revenue

Southeast Asian Market Entry

As of 2025, Smart Share Global scaled its power-bank sharing model into Southeast Asia, tapping markets with mobile penetration above 70% (e.g., Indonesia 78% in 2024) and youth-heavy demographics; this region now drives rapid user growth and accounts for ~18% of new global activations in 2025.

Initial CAPEX and marketing raised regional unit economics breakeven to ~14 months, but low organized competition and monthly active user (MAU) growth of ~35% YoY offset costs, projecting regional EBITDA margin of ~12% by 2026.

- Mobile penetration >70% (Indonesia 78% 2024)

- Region = ~18% of 2025 new activations

- MAU growth ~35% YoY

- Breakeven ~14 months; EBITDA ~12% by 2026

Airport & 5G Charger Boom: Rapid Global Scale, 34% Ad Growth, IRR >18%

Stars: Airport/rail hubs & 5G chargers drive rapid growth—45–55% China share (Q4 2025), 60+ airports/120+ stations; site ARPU 3–8x retail; 34% YoY ad rev (2025); 2.6M MAU, 42k screens; SEA = 18% new activations (2025), MAU +35% YoY; capex ~$60M/yr; unit OPEX +20%; projected IRR >18% five years.

| Metric | Value (2025) |

|---|---|

| China share | 45–55% |

| Airports/stations | 60/120+ |

| Ad YoY | 34% |

| MAU/screens | 2.6M/42k |

| Capex | $60M/yr |

What is included in the product

Comprehensive BCG analysis of Smart Share’s portfolio with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Smart Share BCG Matrix mapping units into quadrants for instant strategic clarity

Cash Cows

Mature Shopping Mall Networks

Smart Share Global’s mature shopping mall network is a high-market-share, low-capex cash cow: in 2025 these locations generated ~62% of company EBITDA while using <10% of total capital expenditure, since most hardware is fully depreciated and maintenance capex averages $8–12 per unit annually.

High margins follow: gross margins on mall rentals exceed 78% in 2025, yielding steady monthly cash flow that funded R&D spend of $38.5M (≈24% of free cash flow) for new product lines.

Established Restaurant Chain Partnerships

Long-term exclusive contracts with national catering and restaurant chains generate stable revenue, accounting for roughly 42% of Smart Share Global’s FY2024 recurring income (about $128M), and show low churn under multi-year renewals through 2025.

Deep integration in partner venues cuts maintenance and promotion costs by an estimated 18% versus new-market rollouts, raising segment gross margins to ~36% in 2024.

The cash flows from this segment are actively milked to fund expansion into volatile and emerging sectors, supporting a $45M capex and R&D push for 2025 market entries.

Core Mobile App Ecosystem

The Core Mobile App Ecosystem, anchored by the Energy Monster mini-program and dedicated app, serves a massive loyal base of 28 million monthly active users (MAU) as of Dec 2025, cutting acquisition cost per user to under $1 and classifying it as a cash cow.

With a 42% share of the local digital interface market, recurring daily sessions average 18 per user and churn is low at 3% monthly, supplying predictable revenue streams.

The platform processes $1.2 billion in annual transactions, enabling seamless payments and generating steady fee income that underpins the wider business infrastructure.

Legacy Cabinet Maintenance Services

Legacy Cabinet Maintenance Services is a Cash Cow: infrastructure for older cabinet models is now 40% more efficient vs 2018, yielding steady EBITDA margins around 28% in 2024 and requiring minimal CapEx since 2019.

These units perform reliably in stable sites, producing recurring revenue with low churn; field expertise cuts OPEX per unit by ~22%, letting Smart Share Global harvest free cash to fund growth areas.

- High efficiency: +40% vs 2018

- EBITDA margin: ~28% (2024)

- OPEX per unit down ~22%

- Minimal CapEx since 2019

Brand Licensing and Royalties

By 2025 Energy Monster brand recognition drives passive income via licensing—brand royalties from third-party consumer electronics deals total an estimated $42.5M in annual recurring revenue, with royalty margins around 88% and negligible operating costs.

Licenses cover headphones, smart chargers, and IoT accessories; parent company involvement is limited to brand guidelines and quality audits, yielding cash flow conversion rates near 95% and EBITDA contribution concentrated in corporate cash.

- 2025 royalties: $42.5M

Smart Share Global: Cash Cows Drive 62% EBITDA, 28M MAU, $1.2B TPV, $42.5M Royalties

Smart Share Global’s cash cows (malls, Core App, Legacy Services, Energy Monster licensing) generated ~62% of EBITDA in 2025, with mall gross margins >78%, app MAU 28M (Dec 2025), platform $1.2B TPV, legacy EBITDA ~28% (2024), and $42.5M royalties (2025); low capex (<10% total) and high cash conversion (~95%) funded $45M 2025 expansion.

| Segment | Key 2024–25 Metrics |

|---|---|

| Malls | 62% EBITDA share; gross margin>78%; capex<10% |

| Core App | 28M MAU; $1.2B TPV |

| Legacy | EBITDA~28%; OPEX−22% |

| Licensing | $42.5M rev; margin~88% |

Preview = Final Product

Smart Share Global BCG Matrix

The file you're previewing is the exact Smart Share Global BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready report designed for strategic clarity and professional presentation.