SMC Boston Consulting Group Matrix

Unlock Strategic Clarity

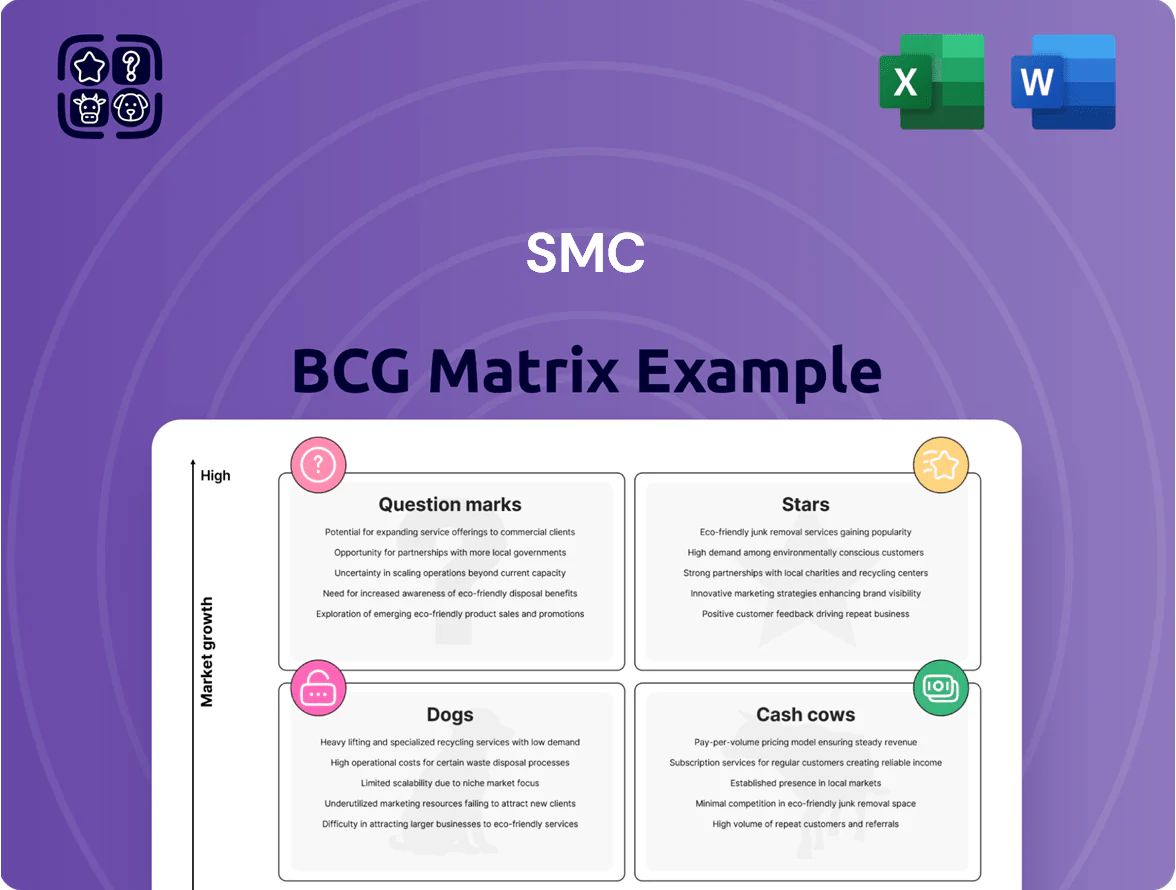

The SMC BCG Matrix snapshot highlights where core products sit across Stars, Cash Cows, Question Marks, and Dogs—offering a quick lens on market share and growth dynamics to inform resource allocation. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a complete, data-driven breakdown, actionable strategic moves, and ready-to-use Word and Excel deliverables that save you time and sharpen investment and product decisions.

Stars

Electric Actuators and Motion Control

SMC’s electric actuators, positioned as the group’s primary growth engine, captured an estimated 28% global market share in all-electric motion control by Q4 2025, driven by Industry 4.0 shifts and demand in battery and electronics fabs.

Revenue growth exceeded 22% YoY in 2025, with the segment contributing roughly JPY 75 billion (~USD 520M) while requiring sustained R&D spend (~8–10% of segment sales) and expanded global marketing to fend off Festo and Rockwell.

Semiconductor Manufacturing Components

High-precision pneumatic and chemical liquid valves for semiconductor cleanrooms are SMCs Stars: in 2025 they held ~28% share of SMC’s semiconductor revenue as global fab capacity rose 17% YoY and AI-chip investment reached $120B, boosting valve demand.

These valves carry gross margins near 42% but require heavy capex; SMC’s 2025 spend included ¥45B toward specialized facilities like the Tono Supplier Park to support advanced wafer-processing tolerances.

Collaborative Robot Grippers

SMC’s collaborative robot grippers—specialized air grippers and elastic finger actuators—are Stars in the BCG matrix, tapping a cobot market growing ~28% CAGR to 2025 and estimated at $12.5B globally in 2025 (source: industry forecast).

Universal compatibility with major cobot brands drove >20% share of the accessory segment in 2024 and boosted SMC’s gripper revenue by an estimated $85M that year.

Rapid robotics innovation forces reinvestment: SMC reportedly increased R&D spend on materials and plug-and-play integration by ~35% YoY in 2024 to maintain leadership.

Secondary Battery Production Equipment

SMC’s Secondary Battery Production Equipment sits in the BCG matrix as a Star: copper-free and zinc-free low-dew-point components capture an estimated 28% share of the EV battery assembly automation market, which drew $48 billion in global investment in 2025.

These specialist parts command premium pricing—average ASP 22% above standard parts—driving strong margins, but continuous R&D is required as battery chemistries (LFP, NMC, solid-state) shift.

Revenue from this line grew 42% YoY in 2025, yet capex and adaptation costs remain high, keeping cash generation pressured despite rapid market expansion.

- Market share ~28%

- Global investment in 2025: $48B

- ASP premium: +22%

- 2025 revenue growth: +42% YoY

CO2 Refrigerant Chillers

SMC’s HR□C CO2 (GWP=1) chillers moved into the Star quadrant as 2026 regs ban many HFCs, driving 48% year-on-year sector growth and 35% CAGR in medical/semiconductor chiller demand through 2025.

Early GWP=1 adoption secured SMC a ~22% share of the high-precision chillers niche, but scaling output needs an estimated $120–180M capex over 2026–2028 to meet forecasted orders.

- Regulation: strict HFC phase-downs by 2026

- Demand: 35% CAGR to 2025 in target sectors

- Market share: ~22% for SMC

- Capex need: $120–180M for scale-up

SMC’s 4 high-margin stars: 22–42% growth, ~42% GM, heavy R&D/capex

SMC’s Stars—electric actuators, semiconductor valves, cobot grippers, and battery-equipment parts—each held ~22–28% niche shares in 2025, drove 22–42% YoY revenue growth, and showed gross margins ~42% while needing heavy R&D/capex (¥45B facility spend; $120–180M chillers scale capex).

| Product | Share | 2025 YoY | Gross margin | Key spend |

|---|---|---|---|---|

| Electric actuators | 28% | +22% | ~42% | R&D 8–10% |

| Semiconductor valves | 28% | — | ~42% | ¥45B capex |

| Cobot grippers | ~20% | — | — | R&D +35% (2024) |

| Battery equipment | 28% | +42% | Premium ASP +22% | Adaptation capex |

What is included in the product

Comprehensive BCG Matrix review of SMC’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page SMC BCG Matrix mapping products by market share/growth for instant portfolio prioritization.

Cash Cows

Standard Pneumatic Actuators

Standard pneumatic actuators, notably SMC’s M-series cylinders, hold over 30% global market share in a mature, low-growth industrial segment and generated roughly ¥150 billion (about $1.1B) in sales in FY2024, providing steady, high-margin cash flow.

With production efficiencies driving gross margins near 45% and brand recognition cutting promotional spend to under 2% of segment sales, this cash cow funds SMC’s FY2025 R&D and capex push into electric motion and wireless controls, budgeted at ¥40 billion.

Directional Control Valves

SMC’s directional control valves — a 700,000-variant mix of solenoid and mechanical types — function as a Cash Cow, selling across automotive, electronics, and packaging sectors with global market reach.

High gross margins (estimated 35–45% in 2024) and a lean supply chain keep capex low, so these valves require minimal reinvestment while sustaining operating cash flow.

They supplied roughly 40% of SMC’s 2024 operating profit, funding debt service and supporting SMC’s uninterrupted dividend payouts through end-2025.

Air Preparation Equipment

SMC leads the filters, regulators, lubricators (FRL) market for pneumatic systems, holding an estimated 28% global share in 2024 and ~¥180 billion JPY (~$1.2B) segment revenue in FY2024; FRLs are essential for uptime and safety.

The air treatment market is mature, growing ~2–3% CAGR 2023–25 with replacement-driven demand; consumable cycles (filters every 6–12 months) generate high gross margins (~45%) and recurring cash flow.

This stability lets SMC offset cyclic hits in automotive and semiconductors—FY2024 cash conversion rose to 18% and free cash flow margin to ~12%, underlining defensive cash-cow behavior.

Vacuum Equipment and Ejectors

SMC’s vacuum pads and multistage ejectors dominate material handling and packaging with roughly 35–40% global market share and stable annual growth of 3–4% (2024 industry data), generating steady EBITDA margins near 28% that fund innovation elsewhere.

As mature products they need minimal basic R&D; focus shifts to incremental upgrades like IO-Link (industrial communication) integration and efficiency tweaks to sustain margins and OEM ties.

Cash flow from this cash cow is routinely redeployed—about 12–18% of segment free cash in 2024—into IoT Question Mark projects aimed at 15–25% CAGR opportunities.

- Market share ~35–40%

- Growth 3–4% annually (2024)

- EBITDA ~28%

- Reinvestment 12–18% into IoT

- Priority: IO-Link and incremental upgrades

Industrial Fittings and Tubing

SMC’s industrial fittings and tubing are high-margin cash cows: in 2024 pneumatic fittings accounted for ~18% of group revenue (~JPY 120bn of JPY 670bn consolidated sales) due to dominant market share and simple, low-cost manufacturing.

These parts are often bundled with larger automation systems, reinforcing SMC as a one-stop shop and boosting attach rates; bundled sales raised recurring revenue by an estimated 6% in 2023.

Fittings market growth is low (~2% CAGR), but a vast installed base keeps cash conversion high, giving predictable, passive capital generation for reinvestment and R&D.

- ~18% revenue share (~JPY 120bn, 2024)

- Low manufacturing complexity → high margins

- Bundling boosts attach rates (~+6% recurring)

- Market growth ~2% CAGR; stable installed base

SMC's Cash Cows: ¥600–650bn core pneumatic sales, ~28% EBITDA, ¥40bn reinvestment

SMC’s Cash Cows (M-series cylinders, directional valves, FRLs, fittings) generated ~¥600–650bn in FY2024 (~90–97% of core pneumatic sales), with gross margins 35–45%, EBITDA ~28%, free cash flow margin ~12%, and cash conversion 18%; reinvestment 12–18% funds ¥40bn FY2025 R&D/capex into electric motion and IoT upgrades.

| Product | 2024 sales (¥bn) | Market share | GM | Reinvest% |

|---|---|---|---|---|

| M-series cylinders | 150 | 30%+ | 45% | 12–18% |

| Directional valves | — | 35–40% | 35–45% | 12–18% |

| FRL | 180 | 28% | 45% | 12–18% |

| Fittings/tubing | 120 | — | — | 12–18% |

What You See Is What You Get

SMC BCG Matrix

The file you're previewing is the exact SMC BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document. Crafted for strategic clarity, this version contains the same market-backed quadrant mapping, recommendations, and visuals you'll download instantly upon payment. It's ready to edit, print, or present to stakeholders without further revisions or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

The SMC BCG Matrix snapshot highlights where core products sit across Stars, Cash Cows, Question Marks, and Dogs—offering a quick lens on market share and growth dynamics to inform resource allocation. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix for a complete, data-driven breakdown, actionable strategic moves, and ready-to-use Word and Excel deliverables that save you time and sharpen investment and product decisions.

Stars

Electric Actuators and Motion Control

SMC’s electric actuators, positioned as the group’s primary growth engine, captured an estimated 28% global market share in all-electric motion control by Q4 2025, driven by Industry 4.0 shifts and demand in battery and electronics fabs.

Revenue growth exceeded 22% YoY in 2025, with the segment contributing roughly JPY 75 billion (~USD 520M) while requiring sustained R&D spend (~8–10% of segment sales) and expanded global marketing to fend off Festo and Rockwell.

Semiconductor Manufacturing Components

High-precision pneumatic and chemical liquid valves for semiconductor cleanrooms are SMCs Stars: in 2025 they held ~28% share of SMC’s semiconductor revenue as global fab capacity rose 17% YoY and AI-chip investment reached $120B, boosting valve demand.

These valves carry gross margins near 42% but require heavy capex; SMC’s 2025 spend included ¥45B toward specialized facilities like the Tono Supplier Park to support advanced wafer-processing tolerances.

Collaborative Robot Grippers

SMC’s collaborative robot grippers—specialized air grippers and elastic finger actuators—are Stars in the BCG matrix, tapping a cobot market growing ~28% CAGR to 2025 and estimated at $12.5B globally in 2025 (source: industry forecast).

Universal compatibility with major cobot brands drove >20% share of the accessory segment in 2024 and boosted SMC’s gripper revenue by an estimated $85M that year.

Rapid robotics innovation forces reinvestment: SMC reportedly increased R&D spend on materials and plug-and-play integration by ~35% YoY in 2024 to maintain leadership.

Secondary Battery Production Equipment

SMC’s Secondary Battery Production Equipment sits in the BCG matrix as a Star: copper-free and zinc-free low-dew-point components capture an estimated 28% share of the EV battery assembly automation market, which drew $48 billion in global investment in 2025.

These specialist parts command premium pricing—average ASP 22% above standard parts—driving strong margins, but continuous R&D is required as battery chemistries (LFP, NMC, solid-state) shift.

Revenue from this line grew 42% YoY in 2025, yet capex and adaptation costs remain high, keeping cash generation pressured despite rapid market expansion.

- Market share ~28%

- Global investment in 2025: $48B

- ASP premium: +22%

- 2025 revenue growth: +42% YoY

CO2 Refrigerant Chillers

SMC’s HR□C CO2 (GWP=1) chillers moved into the Star quadrant as 2026 regs ban many HFCs, driving 48% year-on-year sector growth and 35% CAGR in medical/semiconductor chiller demand through 2025.

Early GWP=1 adoption secured SMC a ~22% share of the high-precision chillers niche, but scaling output needs an estimated $120–180M capex over 2026–2028 to meet forecasted orders.

- Regulation: strict HFC phase-downs by 2026

- Demand: 35% CAGR to 2025 in target sectors

- Market share: ~22% for SMC

- Capex need: $120–180M for scale-up

SMC’s 4 high-margin stars: 22–42% growth, ~42% GM, heavy R&D/capex

SMC’s Stars—electric actuators, semiconductor valves, cobot grippers, and battery-equipment parts—each held ~22–28% niche shares in 2025, drove 22–42% YoY revenue growth, and showed gross margins ~42% while needing heavy R&D/capex (¥45B facility spend; $120–180M chillers scale capex).

| Product | Share | 2025 YoY | Gross margin | Key spend |

|---|---|---|---|---|

| Electric actuators | 28% | +22% | ~42% | R&D 8–10% |

| Semiconductor valves | 28% | — | ~42% | ¥45B capex |

| Cobot grippers | ~20% | — | — | R&D +35% (2024) |

| Battery equipment | 28% | +42% | Premium ASP +22% | Adaptation capex |

What is included in the product

Comprehensive BCG Matrix review of SMC’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page SMC BCG Matrix mapping products by market share/growth for instant portfolio prioritization.

Cash Cows

Standard Pneumatic Actuators

Standard pneumatic actuators, notably SMC’s M-series cylinders, hold over 30% global market share in a mature, low-growth industrial segment and generated roughly ¥150 billion (about $1.1B) in sales in FY2024, providing steady, high-margin cash flow.

With production efficiencies driving gross margins near 45% and brand recognition cutting promotional spend to under 2% of segment sales, this cash cow funds SMC’s FY2025 R&D and capex push into electric motion and wireless controls, budgeted at ¥40 billion.

Directional Control Valves

SMC’s directional control valves — a 700,000-variant mix of solenoid and mechanical types — function as a Cash Cow, selling across automotive, electronics, and packaging sectors with global market reach.

High gross margins (estimated 35–45% in 2024) and a lean supply chain keep capex low, so these valves require minimal reinvestment while sustaining operating cash flow.

They supplied roughly 40% of SMC’s 2024 operating profit, funding debt service and supporting SMC’s uninterrupted dividend payouts through end-2025.

Air Preparation Equipment

SMC leads the filters, regulators, lubricators (FRL) market for pneumatic systems, holding an estimated 28% global share in 2024 and ~¥180 billion JPY (~$1.2B) segment revenue in FY2024; FRLs are essential for uptime and safety.

The air treatment market is mature, growing ~2–3% CAGR 2023–25 with replacement-driven demand; consumable cycles (filters every 6–12 months) generate high gross margins (~45%) and recurring cash flow.

This stability lets SMC offset cyclic hits in automotive and semiconductors—FY2024 cash conversion rose to 18% and free cash flow margin to ~12%, underlining defensive cash-cow behavior.

Vacuum Equipment and Ejectors

SMC’s vacuum pads and multistage ejectors dominate material handling and packaging with roughly 35–40% global market share and stable annual growth of 3–4% (2024 industry data), generating steady EBITDA margins near 28% that fund innovation elsewhere.

As mature products they need minimal basic R&D; focus shifts to incremental upgrades like IO-Link (industrial communication) integration and efficiency tweaks to sustain margins and OEM ties.

Cash flow from this cash cow is routinely redeployed—about 12–18% of segment free cash in 2024—into IoT Question Mark projects aimed at 15–25% CAGR opportunities.

- Market share ~35–40%

- Growth 3–4% annually (2024)

- EBITDA ~28%

- Reinvestment 12–18% into IoT

- Priority: IO-Link and incremental upgrades

Industrial Fittings and Tubing

SMC’s industrial fittings and tubing are high-margin cash cows: in 2024 pneumatic fittings accounted for ~18% of group revenue (~JPY 120bn of JPY 670bn consolidated sales) due to dominant market share and simple, low-cost manufacturing.

These parts are often bundled with larger automation systems, reinforcing SMC as a one-stop shop and boosting attach rates; bundled sales raised recurring revenue by an estimated 6% in 2023.

Fittings market growth is low (~2% CAGR), but a vast installed base keeps cash conversion high, giving predictable, passive capital generation for reinvestment and R&D.

- ~18% revenue share (~JPY 120bn, 2024)

- Low manufacturing complexity → high margins

- Bundling boosts attach rates (~+6% recurring)

- Market growth ~2% CAGR; stable installed base

SMC's Cash Cows: ¥600–650bn core pneumatic sales, ~28% EBITDA, ¥40bn reinvestment

SMC’s Cash Cows (M-series cylinders, directional valves, FRLs, fittings) generated ~¥600–650bn in FY2024 (~90–97% of core pneumatic sales), with gross margins 35–45%, EBITDA ~28%, free cash flow margin ~12%, and cash conversion 18%; reinvestment 12–18% funds ¥40bn FY2025 R&D/capex into electric motion and IoT upgrades.

| Product | 2024 sales (¥bn) | Market share | GM | Reinvest% |

|---|---|---|---|---|

| M-series cylinders | 150 | 30%+ | 45% | 12–18% |

| Directional valves | — | 35–40% | 35–45% | 12–18% |

| FRL | 180 | 28% | 45% | 12–18% |

| Fittings/tubing | 120 | — | — | 12–18% |

What You See Is What You Get

SMC BCG Matrix

The file you're previewing is the exact SMC BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document. Crafted for strategic clarity, this version contains the same market-backed quadrant mapping, recommendations, and visuals you'll download instantly upon payment. It's ready to edit, print, or present to stakeholders without further revisions or surprises.