SMC Porter's Five Forces Analysis

From Overview to Strategy Blueprint

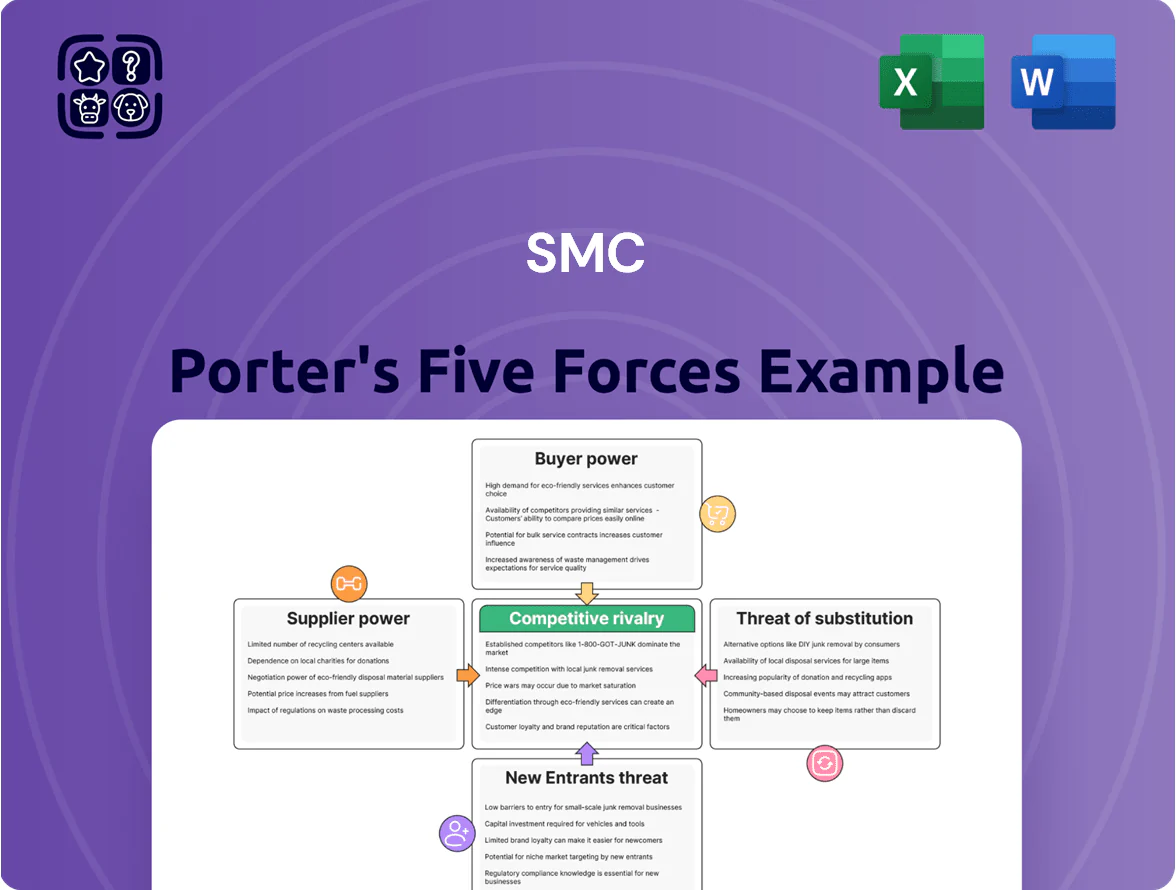

SMC’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive rivalry shaping its profit margins and strategic levers; barriers to entry and substitute threats round out the industry picture.

This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to SMC’s market position.

Suppliers Bargaining Power

Raw Material Price Volatility

SMC depends on aluminum, stainless steel and high-grade rubber for pneumatic parts; in 2025 aluminum futures rose ~18% YoY and nickel (stainless proxy) 12% YoY, so commodity swings can compress margins despite SMC’s ~¥500 billion annual purchasing scale.

Scale reduces supplier squeeze, but specialized rubber and alloy vendors retain moderate leverage; SMC needs ongoing strategic sourcing and multi-year contracts (typical 3–5 years) to lock prices and limit margin volatility.

Semiconductor and Electronic Component Constraints

SMC’s shift into electric actuators and digital sensors raises semiconductor dependence—about 35–40% of BOM value for new lines in 2025—boosting supplier leverage. Specialized chips have limited qualified vendors, so few alternatives meet industrial volume and reliability specs, making supply disruptions cause lead-time delays of 8–20 weeks reported in 2021–23. This reliance gives high-end electronic component makers greater bargaining power than SMC’s traditional metal suppliers.

Strategic Vertical Integration

SMC cuts supplier power through deep vertical integration: as of FY2024 SMC produced roughly 60% of key sub-components in-house, lowering purchased content and supplier spend by about 18% versus 2019.

Making specialized tools and parts gives SMC tighter quality and cost control, reduces lead-time risk, and limits third-party vendor leverage, keeping traditional supplier bargaining power relatively low.

Supplier Fragmentation for Standard Parts

For non-specialized components and standard hardware, SMC sources from a highly fragmented global supplier base, enabling it to switch vendors with little disruption and keep bargaining power high.

Competition among many small vendors keeps costs low; SMC’s FY2024 purchase volume—about $1.2 billion—secures preferential pricing and 10–15% better lead times versus market averages.

- Many suppliers → low supplier power

- Switchability → high negotiating leverage

- Volume ($1.2B in 2024) → better prices/delivery

- Steady supply for basics → low disruption risk

Logistics and Energy Costs

Suppliers of logistics and energy are critical for SMC’s global manufacturing; in 2024 shipping surcharges averaged 8–15% and industrial electricity prices rose 12% year-over-year in key markets like EU and Japan.

Rising energy costs trigger non-negotiable utility surcharges and freight add-ons; SMC can cut internal waste but cannot compel global shipping cartels or national grids to lower rates.

Because few viable global-distribution alternatives exist, these external providers retain steady bargaining power, raising cost volatility and margin risk for SMC.

- 2024 freight surcharges: 8–15%

- Industrial power rise (2024): ~12% in EU/Japan

- Limited negotiation vs shipping cartels/grids

- Internal efficiency helps, doesn’t eliminate risk

SMC supplier risk: scale & vertical integration vs rising metals, chips, freight and power

SMC’s supplier power is mixed: commodity metals/rubber have moderate pressure (aluminum +18% YoY, nickel +12% YoY in 2025) but SMC’s ¥500B scale and $1.2B 2024 purchases give negotiating leverage; vertical integration (60% in‑house FY2024) cuts bought content ~18% vs 2019; semiconductor dependence (35–40% BOM on new lines) and freight/energy surcharges (2024 freight 8–15%, power +12%) raise supplier risk.

| Metric | 2024–25 |

|---|---|

| Aluminum YoY | +18% |

| Nickel YoY | +12% |

| Purchasing scale | ¥500B |

| Purchase spend | $1.2B |

| In‑house | 60% |

| Semiconductor BOM | 35–40% |

| Freight surcharge | 8–15% |

| Power rise | ~12% |

What is included in the product

Uncovers SMC’s competitive pressures by detailing rivalry, supplier and buyer power, entry barriers, substitutes, and niche threats, with industry data and strategic commentary to inform positioning and risk mitigation.

Clear, one-sheet Porter's Five Forces summary for SMC—instantly shows competitive pressures and relieves decision fatigue in boardrooms and investor decks.

Customers Bargaining Power

High Switching Costs for Integrated Systems

Customers in semiconductor and automotive manufacturing deeply embed SMC pneumatic modules into designs, so switching brands often needs engineering re-validation and 2–4 weeks of downtime, lowering buyer leverage.

This technical lock-in helped SMC preserve pricing; despite cheaper rivals, SMC's 2024 sales mix showed 58% recurring OEM revenue, supporting stable margins.

The specialized nature of pneumatic circuits drives long-term loyalty—industry surveys report 65% of manufacturers keep suppliers >5 years.

Volume Leverage of Major OEMs

Large OEMs buying thousands of units yearly hold strong volume leverage, securing discounts of 10–25% on average in industrial pneumatics procurement; in 2024, top 5 OEMs accounted for ~42% of sector purchases, amplifying their bargaining power.

Tier 1 customers often require tailored components and dedicated support teams, raising SMC’s service costs by an estimated 3–6% of contract value while locking in multi-year agreements.

SMC must balance retaining high-volume accounts with margin targets—every 5% extra discount cuts gross margin by ~0.8–1.2 percentage points—so SMC competes on innovation and reliability to justify pricing.

Demand for Energy Efficient Solutions

By end-2025 industrial buyers increasingly prioritize cutting emissions and energy costs, with 68% of manufacturers citing energy efficiency as a top procurement criterion in a 2024 IDC survey; this raises customer bargaining power over suppliers like SMC. Buyers now demand pneumatic and electric systems meeting EU ETS and ISO 14001-linked targets, prompting SMC to pivot R&D to efficient actuators or risk losing share to greener rivals. Green specs are often the primary supplier filter in RFPs, driving price and feature pressure.

Industry Diversification and Risk Mitigation

SMC serves food processing, medical devices, and electronics, so no single buyer group dominates; diversified end-markets cut collective buyer leverage and stabilize revenue—SMC reported 2024 end-market mix: 32% electronics, 28% food, 22% medical, 18% other.

That mix means sector downturns tend to be offset by gains elsewhere, limiting buyer pressure on prices and allowing SMC to keep firm catalog pricing despite a few large accounts representing ~15% of 2024 sales.

- Diverse end-markets: 32% electronics, 28% food, 22% medical, 18% other

- Top clients ~15% of sales—no single-customer dominance

- Sector offsets reduce buyer bargaining

- Supports firmer pricing across catalog

Information Transparency and Digital Procurement

Digital procurement platforms increased price and spec transparency; 72% of industrial buyers used online sourcing in 2024, exposing SMC to direct comparison with Festo and Parker Hannifin on price, specs, and lead times.

This visibility forces SMC to emphasise superior technical support and faster delivery—37% of buyers in 2024 said lead time beat price when choosing suppliers—raising service SLAs as the key negotiation point.

Buyers now negotiate for tighter SLAs, integrated after-sales support, and faster fulfillment instead of just lower unit prices, reducing SMC’s pricing power but opening value-based differentiation.

- 72% industrial buyers used online sourcing (2024)

- 37% prioritize lead time over price (2024)

- Competitors: Festo, Parker Hannifin—easily compared

- SLA & technical support now key negotiation levers

Moderate Customer Power: OEM Discounts vs. 58% Recurring Revenue & 72% Online Sourcing

Customers have moderate bargaining power: engineering lock-in and 58% recurring OEM mix limit price pressure, but large OEMs (top 5 ≈42% sector purchases; top clients ≈15% SMC sales) extract 10–25% volume discounts and demand SLAs; 72% use online sourcing (2024) and 37% prioritize lead time, while diversified end-markets (32% electronics, 28% food, 22% medical) blunt collective leverage.

| Metric | 2024 |

|---|---|

| Recurring OEM revenue | 58% |

| Top 5 OEM share (sector) | ≈42% |

| Online sourcing | 72% |

Preview the Actual Deliverable

SMC Porter's Five Forces Analysis

This preview shows the exact SMC Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download upon purchase; no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

SMC’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive rivalry shaping its profit margins and strategic levers; barriers to entry and substitute threats round out the industry picture.

This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to SMC’s market position.

Suppliers Bargaining Power

Raw Material Price Volatility

SMC depends on aluminum, stainless steel and high-grade rubber for pneumatic parts; in 2025 aluminum futures rose ~18% YoY and nickel (stainless proxy) 12% YoY, so commodity swings can compress margins despite SMC’s ~¥500 billion annual purchasing scale.

Scale reduces supplier squeeze, but specialized rubber and alloy vendors retain moderate leverage; SMC needs ongoing strategic sourcing and multi-year contracts (typical 3–5 years) to lock prices and limit margin volatility.

Semiconductor and Electronic Component Constraints

SMC’s shift into electric actuators and digital sensors raises semiconductor dependence—about 35–40% of BOM value for new lines in 2025—boosting supplier leverage. Specialized chips have limited qualified vendors, so few alternatives meet industrial volume and reliability specs, making supply disruptions cause lead-time delays of 8–20 weeks reported in 2021–23. This reliance gives high-end electronic component makers greater bargaining power than SMC’s traditional metal suppliers.

Strategic Vertical Integration

SMC cuts supplier power through deep vertical integration: as of FY2024 SMC produced roughly 60% of key sub-components in-house, lowering purchased content and supplier spend by about 18% versus 2019.

Making specialized tools and parts gives SMC tighter quality and cost control, reduces lead-time risk, and limits third-party vendor leverage, keeping traditional supplier bargaining power relatively low.

Supplier Fragmentation for Standard Parts

For non-specialized components and standard hardware, SMC sources from a highly fragmented global supplier base, enabling it to switch vendors with little disruption and keep bargaining power high.

Competition among many small vendors keeps costs low; SMC’s FY2024 purchase volume—about $1.2 billion—secures preferential pricing and 10–15% better lead times versus market averages.

- Many suppliers → low supplier power

- Switchability → high negotiating leverage

- Volume ($1.2B in 2024) → better prices/delivery

- Steady supply for basics → low disruption risk

Logistics and Energy Costs

Suppliers of logistics and energy are critical for SMC’s global manufacturing; in 2024 shipping surcharges averaged 8–15% and industrial electricity prices rose 12% year-over-year in key markets like EU and Japan.

Rising energy costs trigger non-negotiable utility surcharges and freight add-ons; SMC can cut internal waste but cannot compel global shipping cartels or national grids to lower rates.

Because few viable global-distribution alternatives exist, these external providers retain steady bargaining power, raising cost volatility and margin risk for SMC.

- 2024 freight surcharges: 8–15%

- Industrial power rise (2024): ~12% in EU/Japan

- Limited negotiation vs shipping cartels/grids

- Internal efficiency helps, doesn’t eliminate risk

SMC supplier risk: scale & vertical integration vs rising metals, chips, freight and power

SMC’s supplier power is mixed: commodity metals/rubber have moderate pressure (aluminum +18% YoY, nickel +12% YoY in 2025) but SMC’s ¥500B scale and $1.2B 2024 purchases give negotiating leverage; vertical integration (60% in‑house FY2024) cuts bought content ~18% vs 2019; semiconductor dependence (35–40% BOM on new lines) and freight/energy surcharges (2024 freight 8–15%, power +12%) raise supplier risk.

| Metric | 2024–25 |

|---|---|

| Aluminum YoY | +18% |

| Nickel YoY | +12% |

| Purchasing scale | ¥500B |

| Purchase spend | $1.2B |

| In‑house | 60% |

| Semiconductor BOM | 35–40% |

| Freight surcharge | 8–15% |

| Power rise | ~12% |

What is included in the product

Uncovers SMC’s competitive pressures by detailing rivalry, supplier and buyer power, entry barriers, substitutes, and niche threats, with industry data and strategic commentary to inform positioning and risk mitigation.

Clear, one-sheet Porter's Five Forces summary for SMC—instantly shows competitive pressures and relieves decision fatigue in boardrooms and investor decks.

Customers Bargaining Power

High Switching Costs for Integrated Systems

Customers in semiconductor and automotive manufacturing deeply embed SMC pneumatic modules into designs, so switching brands often needs engineering re-validation and 2–4 weeks of downtime, lowering buyer leverage.

This technical lock-in helped SMC preserve pricing; despite cheaper rivals, SMC's 2024 sales mix showed 58% recurring OEM revenue, supporting stable margins.

The specialized nature of pneumatic circuits drives long-term loyalty—industry surveys report 65% of manufacturers keep suppliers >5 years.

Volume Leverage of Major OEMs

Large OEMs buying thousands of units yearly hold strong volume leverage, securing discounts of 10–25% on average in industrial pneumatics procurement; in 2024, top 5 OEMs accounted for ~42% of sector purchases, amplifying their bargaining power.

Tier 1 customers often require tailored components and dedicated support teams, raising SMC’s service costs by an estimated 3–6% of contract value while locking in multi-year agreements.

SMC must balance retaining high-volume accounts with margin targets—every 5% extra discount cuts gross margin by ~0.8–1.2 percentage points—so SMC competes on innovation and reliability to justify pricing.

Demand for Energy Efficient Solutions

By end-2025 industrial buyers increasingly prioritize cutting emissions and energy costs, with 68% of manufacturers citing energy efficiency as a top procurement criterion in a 2024 IDC survey; this raises customer bargaining power over suppliers like SMC. Buyers now demand pneumatic and electric systems meeting EU ETS and ISO 14001-linked targets, prompting SMC to pivot R&D to efficient actuators or risk losing share to greener rivals. Green specs are often the primary supplier filter in RFPs, driving price and feature pressure.

Industry Diversification and Risk Mitigation

SMC serves food processing, medical devices, and electronics, so no single buyer group dominates; diversified end-markets cut collective buyer leverage and stabilize revenue—SMC reported 2024 end-market mix: 32% electronics, 28% food, 22% medical, 18% other.

That mix means sector downturns tend to be offset by gains elsewhere, limiting buyer pressure on prices and allowing SMC to keep firm catalog pricing despite a few large accounts representing ~15% of 2024 sales.

- Diverse end-markets: 32% electronics, 28% food, 22% medical, 18% other

- Top clients ~15% of sales—no single-customer dominance

- Sector offsets reduce buyer bargaining

- Supports firmer pricing across catalog

Information Transparency and Digital Procurement

Digital procurement platforms increased price and spec transparency; 72% of industrial buyers used online sourcing in 2024, exposing SMC to direct comparison with Festo and Parker Hannifin on price, specs, and lead times.

This visibility forces SMC to emphasise superior technical support and faster delivery—37% of buyers in 2024 said lead time beat price when choosing suppliers—raising service SLAs as the key negotiation point.

Buyers now negotiate for tighter SLAs, integrated after-sales support, and faster fulfillment instead of just lower unit prices, reducing SMC’s pricing power but opening value-based differentiation.

- 72% industrial buyers used online sourcing (2024)

- 37% prioritize lead time over price (2024)

- Competitors: Festo, Parker Hannifin—easily compared

- SLA & technical support now key negotiation levers

Moderate Customer Power: OEM Discounts vs. 58% Recurring Revenue & 72% Online Sourcing

Customers have moderate bargaining power: engineering lock-in and 58% recurring OEM mix limit price pressure, but large OEMs (top 5 ≈42% sector purchases; top clients ≈15% SMC sales) extract 10–25% volume discounts and demand SLAs; 72% use online sourcing (2024) and 37% prioritize lead time, while diversified end-markets (32% electronics, 28% food, 22% medical) blunt collective leverage.

| Metric | 2024 |

|---|---|

| Recurring OEM revenue | 58% |

| Top 5 OEM share (sector) | ≈42% |

| Online sourcing | 72% |

Preview the Actual Deliverable

SMC Porter's Five Forces Analysis

This preview shows the exact SMC Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download upon purchase; no placeholders or mockups.