SMBC Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

SMBC's competitive landscape is shaped by powerful forces, from the bargaining power of its customers to the intense rivalry within the banking sector. Understanding these dynamics is crucial for navigating the financial industry.

The complete report reveals the real forces shaping SMBC’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Technology Providers

Technology providers, especially those specializing in AI, machine learning, and blockchain, wield considerable bargaining power. Financial institutions like SMFG must invest in these advanced technologies to stay competitive, often relying on external vendors for their specialized expertise and proprietary solutions. For instance, the global AI market was projected to reach over $500 billion in 2024, highlighting the significant investment and reliance on these tech giants.

Data and Analytics Providers

Data and analytics providers wield significant influence, especially as financial institutions like SMFG rely more heavily on data for everything from personalized customer experiences to robust risk management and fraud prevention. The demand for high-quality data and sophisticated analytics tools is escalating, making these suppliers critical partners.

In 2024, the global big data and business analytics market was projected to reach approximately $375 billion, highlighting the immense value placed on these services. SMFG's strategic focus on leveraging data for competitive advantage directly amplifies the bargaining power of its data and analytics suppliers, as access to granular customer insights and predictive market trends is paramount for innovation and operational efficiency.

Human Capital/Talent

The availability of skilled talent, especially in burgeoning fields like artificial intelligence, cybersecurity, and digital transformation, represents a crucial supplier input for SMFG. A scarcity of this specialized expertise can significantly amplify the bargaining power of both employees and external consultants. For instance, in 2024, the global demand for AI specialists outstripped supply, leading to reported salary increases of up to 30% for experienced professionals in this domain.

SMFG's ability to attract and retain top-tier talent is paramount for the successful execution of its digital transformation strategies and for sustaining its competitive advantage in the financial services industry. Reports from early 2025 indicate that financial institutions are increasingly competing with tech giants for the same pool of highly skilled individuals, further intensifying this talent-driven supplier pressure.

Regulatory Technology (RegTech) Vendors

The bargaining power of Regulatory Technology (RegTech) vendors is on the rise due to the escalating complexity and fragmentation of global regulations. These vendors offer automated solutions crucial for compliance and risk management, making them indispensable for financial institutions like SMFG. For instance, the global RegTech market was valued at approximately $11.1 billion in 2023 and is projected to reach $34.2 billion by 2028, indicating significant growth and vendor influence.

SMFG's need to invest in RegTech to effectively navigate evolving regulatory landscapes, particularly in areas such as data privacy, anti-money laundering (AML), and cybersecurity, directly amplifies the power of these suppliers. The increasing stringency of regulations, such as GDPR and various national data protection laws, necessitates sophisticated technological solutions that only specialized RegTech firms can provide. Failure to comply can result in substantial fines; for example, data privacy breaches alone resulted in over $1.3 billion in fines globally in 2023.

- Growing Regulatory Complexity: Financial institutions face an ever-expanding and intricate web of global regulations.

- Essential Nature of RegTech: RegTech solutions are vital for automating compliance processes and enhancing risk management capabilities.

- SMFG's Investment Needs: Significant investment in RegTech is required for SMFG to maintain compliance with evolving standards in data privacy, AML, and cybersecurity.

- Market Growth: The RegTech market is experiencing robust growth, with projections indicating a substantial increase in value, underscoring vendor importance.

Financial Market Infrastructure Providers

Financial market infrastructure providers, like payment networks and clearing houses, hold considerable bargaining power. Their services are fundamental to SMFG's operations, making them indispensable. For instance, SWIFT, a key player in global financial messaging, processed an average of 88 million messages daily in 2023, highlighting its critical role.

Any disruption or alteration in their services directly affects SMFG's operational efficiency and cost structure, particularly in transaction processing and settlement. The reliance on these specialized providers creates a significant dependency, allowing them to exert influence over terms and pricing.

- Criticality of Services: Payment networks and clearing houses offer essential services that are non-negotiable for financial institutions like SMFG.

- High Switching Costs: Migrating away from established infrastructure providers can be complex and expensive, reinforcing their power.

- Network Effects: The value of these infrastructure services increases with the number of participants, creating a barrier to entry for potential competitors and consolidating power among existing providers.

SMFG's Supplier Power: Navigating Critical Dependencies

Suppliers of critical financial technology, such as AI and blockchain specialists, wield significant bargaining power. SMFG's need for these advanced solutions to remain competitive, coupled with the high investment required, amplifies vendor influence. The global AI market's projected growth to over $500 billion in 2024 underscores this reliance.

Data and analytics providers also possess strong bargaining power as financial institutions increasingly depend on data for insights and risk management. The projected $375 billion market for big data and business analytics in 2024 highlights the essential nature of these services for SMFG's competitive edge.

The scarcity of specialized talent, particularly in AI and cybersecurity, grants significant bargaining power to skilled professionals and external consultants. In 2024, demand for AI specialists outstripped supply, leading to substantial salary increases, which SMFG must navigate.

RegTech vendors are gaining influence due to increasing regulatory complexity. SMFG's need for automated compliance solutions, given the projected growth of the RegTech market from $11.1 billion in 2023 to $34.2 billion by 2028, makes these suppliers crucial.

Financial market infrastructure providers, like payment networks, hold substantial bargaining power due to the essential nature of their services. SMFG's reliance on providers such as SWIFT, which handled 88 million messages daily in 2023, creates significant dependency and limits SMFG's leverage.

| Supplier Category | Bargaining Power Factor | SMFG Reliance | Market Data/Example |

|---|---|---|---|

| Technology Providers (AI, Blockchain) | Specialized Expertise, High Investment | Competitive Edge, Digital Transformation | Global AI Market > $500B (2024 proj.) |

| Data & Analytics Providers | Data-Driven Insights, Risk Management | Customer Experience, Operational Efficiency | Big Data Market ~$375B (2024 proj.) |

| Specialized Talent | Scarcity in Key Areas (AI, Cyber) | Talent Acquisition & Retention | AI Specialist Salaries up 30% (2024) |

| RegTech Vendors | Regulatory Complexity, Compliance Needs | Navigating Evolving Regulations | RegTech Market $11.1B (2023) to $34.2B (2028 proj.) |

| Financial Market Infrastructure | Essential Services, High Switching Costs | Core Operations (Payments, Clearing) | SWIFT: 88M messages/day (2023) |

What is included in the product

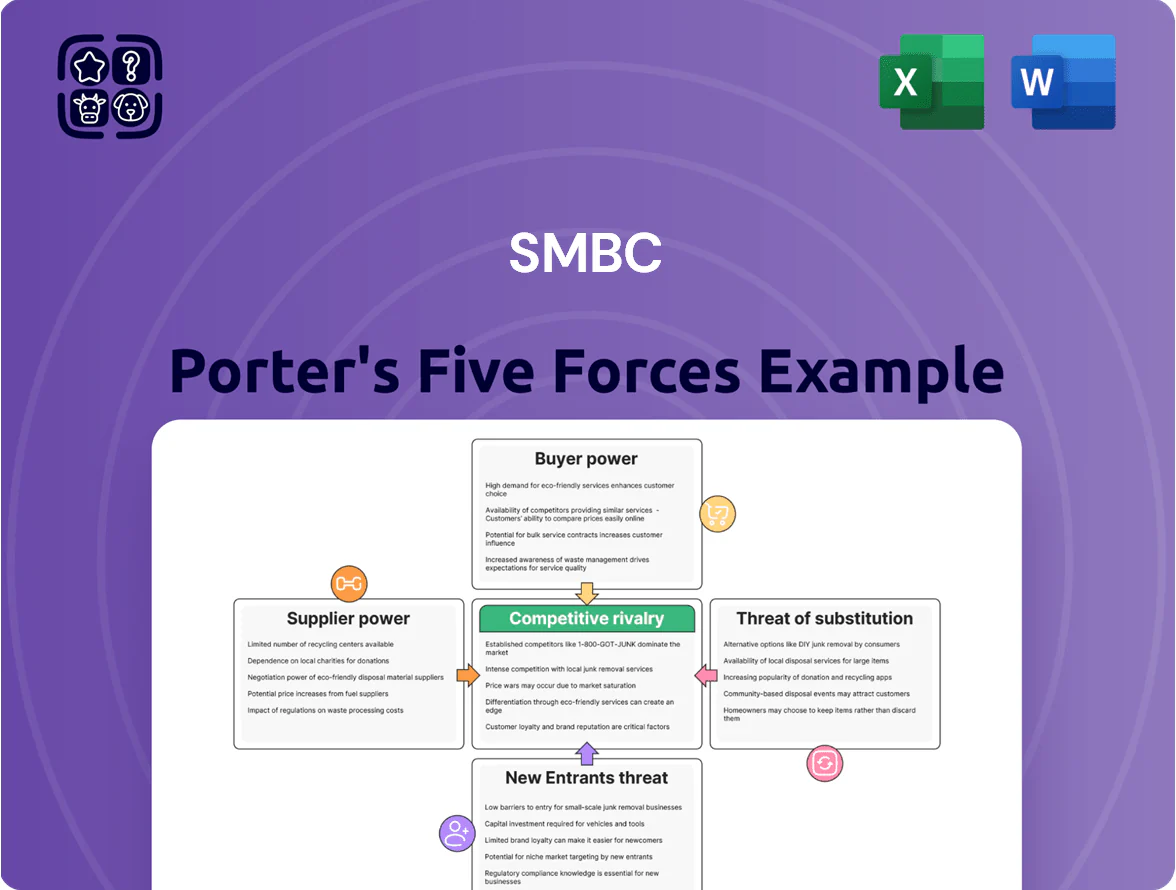

This analysis dissects SMBC's competitive environment by examining the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the overall industry attractiveness.

Instantly identify your competitive landscape's key pressures, allowing you to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Individual Retail Customers

The bargaining power of individual retail customers is on the rise, fueled by the proliferation of digital-first banking options and the ease with which they can switch between institutions. This includes traditional banks, neobanks, and innovative fintech platforms, all vying for customer attention.

Customers today expect more than just basic services; they demand seamless, 24/7 access to their accounts, highly personalized experiences, and, crucially, lower fees. For SMFG, this means a strategic imperative to invest heavily in enhancing its digital offerings and overall customer experience to maintain loyalty and attract new clients in this competitive landscape.

Large Corporations and Financial Institutions

Large corporations and financial institutions wield considerable bargaining power with SMBC. Their sheer volume of business, often involving substantial asset and liability management, allows them to negotiate favorable terms and pricing. For instance, in 2024, major corporate clients might demand lower fees on treasury services or preferential rates on large-scale loans, directly impacting SMBC's profitability.

These sophisticated clients typically require a broad spectrum of complex financial products, from derivatives to international trade finance. SMBC's ability to offer integrated, high-quality solutions is crucial for securing and retaining these valuable relationships, as clients can easily switch to competitors if their needs aren't met. This competitive pressure intensifies when clients leverage their global reach to seek customized offerings.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) are increasingly wielding more influence over their financial service providers. This is largely due to the proliferation of digital lending platforms and specialized fintech solutions, offering a wider array of choices than ever before. In 2024, the SME lending market saw significant growth, with alternative lenders capturing a larger share, indicating a shift in power dynamics.

SMEs are actively seeking financial partners that can provide quicker access to capital, streamlined application processes, and more competitive interest rates. This demand is forcing traditional institutions like SMFG to re-evaluate and adapt their service models. For instance, some fintech lenders reported processing loan applications in as little as 24 hours, a stark contrast to the weeks often associated with traditional bank loans.

The growing bargaining power of SMEs necessitates that SMFG and similar institutions tailor their offerings to meet the unique needs of this often underserved market segment. By understanding and responding to the evolving demands for speed, simplicity, and cost-effectiveness, financial institutions can better retain and attract SME clients.

Tech-Savvy Customers

Tech-savvy customers, a growing segment, wield significant bargaining power. They expect sophisticated digital experiences, including AI-powered financial guidance and seamless mobile banking. For instance, in 2024, a significant portion of banking transactions occurred via mobile apps, highlighting customer preference for digital channels. This group readily switches to competitors offering superior user interfaces and advanced functionalities, putting pressure on financial institutions to innovate.

SMFG's commitment to digital transformation directly addresses this trend. By investing in areas like AI and improving mobile app capabilities, they aim to meet and exceed the expectations of these demanding customers. Failure to keep pace with technological advancements can lead to customer attrition, as these users are well-informed and have numerous alternatives readily available.

- Customer expectations for digital services are high, driven by technological proficiency.

- Easy switching to competitors with better digital offerings increases customer bargaining power.

- Financial institutions must prioritize digital transformation to retain tech-savvy clients.

Customers Seeking Embedded Finance

The proliferation of embedded finance, seamlessly weaving financial services into everyday non-financial platforms, significantly amplifies customer bargaining power. This integration allows consumers to access banking products at their exact point of need, often circumventing traditional financial institutions. For instance, by mid-2024, platforms offering buy-now-pay-later (BNPL) at checkout saw a substantial increase in adoption, with reports indicating over 60% of consumers had used BNPL for purchases. This convenience directly translates to customers having more options and leverage when seeking financial solutions.

SMFG, like other traditional banks, must actively adapt to this evolving landscape. The ability for customers to secure financing or manage payments directly within their preferred e-commerce or service applications means they are less reliant on visiting a bank branch or even using a bank's dedicated app. This shift necessitates a strategic approach to partnerships and the development of proprietary embedded finance capabilities to remain competitive and meet customer expectations for frictionless financial experiences. By 2025, it's projected that the embedded finance market could reach trillions of dollars globally, underscoring the urgency for financial institutions to engage.

- Increased Convenience: Embedded finance offers financial services at the point of transaction, reducing friction for customers.

- Bypassing Traditional Channels: Customers can obtain financial products without directly engaging with banks, increasing their options.

- Market Growth: The embedded finance sector is experiencing rapid expansion, with significant projected growth in the coming years.

- Strategic Imperative: Financial institutions must develop partnerships or in-house solutions to leverage this trend and maintain customer loyalty.

Digital Banking Shifts Power to Customers

The bargaining power of customers is significantly influenced by the ease with which they can switch providers and the availability of alternatives. In 2024, the digital banking landscape continued to empower consumers, with many fintech solutions offering competitive rates and user-friendly interfaces. This increased choice means customers can readily demand better terms or move their business, forcing financial institutions to focus on customer retention through superior service and value.

For instance, the rise of Buy Now, Pay Later (BNPL) services in 2024, with over 60% of consumers utilizing them by mid-year, exemplifies how embedded finance offers customers convenient alternatives, reducing reliance on traditional banking channels. This trend pressures institutions like SMFG to adapt by forging partnerships or developing their own embedded finance capabilities to meet evolving customer expectations for frictionless financial experiences.

| Customer Segment | Key Bargaining Factors | Impact on Financial Institutions |

|---|---|---|

| Individual Retail Customers | Digital access, personalization, lower fees, ease of switching | Need for enhanced digital offerings and customer experience |

| Large Corporations | Volume of business, complex product needs, global reach | Negotiating favorable terms on loans and services |

| SMEs | Speed of capital access, streamlined processes, competitive rates | Pressure to adapt service models to fintech competition |

| Tech-Savvy Customers | Sophisticated digital experiences, AI guidance, mobile functionality | Imperative for continuous innovation in digital platforms |

What You See Is What You Get

SMBC Porter's Five Forces Analysis

This preview showcases the complete SMBC Porter's Five Forces Analysis, identical to the document you'll receive instantly upon purchase. You can confidently assess the depth and quality of this strategic tool, knowing that no elements are missing or altered. This professionally formatted analysis is ready for immediate application to your business needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

SMBC's competitive landscape is shaped by powerful forces, from the bargaining power of its customers to the intense rivalry within the banking sector. Understanding these dynamics is crucial for navigating the financial industry.

The complete report reveals the real forces shaping SMBC’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Technology Providers

Technology providers, especially those specializing in AI, machine learning, and blockchain, wield considerable bargaining power. Financial institutions like SMFG must invest in these advanced technologies to stay competitive, often relying on external vendors for their specialized expertise and proprietary solutions. For instance, the global AI market was projected to reach over $500 billion in 2024, highlighting the significant investment and reliance on these tech giants.

Data and Analytics Providers

Data and analytics providers wield significant influence, especially as financial institutions like SMFG rely more heavily on data for everything from personalized customer experiences to robust risk management and fraud prevention. The demand for high-quality data and sophisticated analytics tools is escalating, making these suppliers critical partners.

In 2024, the global big data and business analytics market was projected to reach approximately $375 billion, highlighting the immense value placed on these services. SMFG's strategic focus on leveraging data for competitive advantage directly amplifies the bargaining power of its data and analytics suppliers, as access to granular customer insights and predictive market trends is paramount for innovation and operational efficiency.

Human Capital/Talent

The availability of skilled talent, especially in burgeoning fields like artificial intelligence, cybersecurity, and digital transformation, represents a crucial supplier input for SMFG. A scarcity of this specialized expertise can significantly amplify the bargaining power of both employees and external consultants. For instance, in 2024, the global demand for AI specialists outstripped supply, leading to reported salary increases of up to 30% for experienced professionals in this domain.

SMFG's ability to attract and retain top-tier talent is paramount for the successful execution of its digital transformation strategies and for sustaining its competitive advantage in the financial services industry. Reports from early 2025 indicate that financial institutions are increasingly competing with tech giants for the same pool of highly skilled individuals, further intensifying this talent-driven supplier pressure.

Regulatory Technology (RegTech) Vendors

The bargaining power of Regulatory Technology (RegTech) vendors is on the rise due to the escalating complexity and fragmentation of global regulations. These vendors offer automated solutions crucial for compliance and risk management, making them indispensable for financial institutions like SMFG. For instance, the global RegTech market was valued at approximately $11.1 billion in 2023 and is projected to reach $34.2 billion by 2028, indicating significant growth and vendor influence.

SMFG's need to invest in RegTech to effectively navigate evolving regulatory landscapes, particularly in areas such as data privacy, anti-money laundering (AML), and cybersecurity, directly amplifies the power of these suppliers. The increasing stringency of regulations, such as GDPR and various national data protection laws, necessitates sophisticated technological solutions that only specialized RegTech firms can provide. Failure to comply can result in substantial fines; for example, data privacy breaches alone resulted in over $1.3 billion in fines globally in 2023.

- Growing Regulatory Complexity: Financial institutions face an ever-expanding and intricate web of global regulations.

- Essential Nature of RegTech: RegTech solutions are vital for automating compliance processes and enhancing risk management capabilities.

- SMFG's Investment Needs: Significant investment in RegTech is required for SMFG to maintain compliance with evolving standards in data privacy, AML, and cybersecurity.

- Market Growth: The RegTech market is experiencing robust growth, with projections indicating a substantial increase in value, underscoring vendor importance.

Financial Market Infrastructure Providers

Financial market infrastructure providers, like payment networks and clearing houses, hold considerable bargaining power. Their services are fundamental to SMFG's operations, making them indispensable. For instance, SWIFT, a key player in global financial messaging, processed an average of 88 million messages daily in 2023, highlighting its critical role.

Any disruption or alteration in their services directly affects SMFG's operational efficiency and cost structure, particularly in transaction processing and settlement. The reliance on these specialized providers creates a significant dependency, allowing them to exert influence over terms and pricing.

- Criticality of Services: Payment networks and clearing houses offer essential services that are non-negotiable for financial institutions like SMFG.

- High Switching Costs: Migrating away from established infrastructure providers can be complex and expensive, reinforcing their power.

- Network Effects: The value of these infrastructure services increases with the number of participants, creating a barrier to entry for potential competitors and consolidating power among existing providers.

SMFG's Supplier Power: Navigating Critical Dependencies

Suppliers of critical financial technology, such as AI and blockchain specialists, wield significant bargaining power. SMFG's need for these advanced solutions to remain competitive, coupled with the high investment required, amplifies vendor influence. The global AI market's projected growth to over $500 billion in 2024 underscores this reliance.

Data and analytics providers also possess strong bargaining power as financial institutions increasingly depend on data for insights and risk management. The projected $375 billion market for big data and business analytics in 2024 highlights the essential nature of these services for SMFG's competitive edge.

The scarcity of specialized talent, particularly in AI and cybersecurity, grants significant bargaining power to skilled professionals and external consultants. In 2024, demand for AI specialists outstripped supply, leading to substantial salary increases, which SMFG must navigate.

RegTech vendors are gaining influence due to increasing regulatory complexity. SMFG's need for automated compliance solutions, given the projected growth of the RegTech market from $11.1 billion in 2023 to $34.2 billion by 2028, makes these suppliers crucial.

Financial market infrastructure providers, like payment networks, hold substantial bargaining power due to the essential nature of their services. SMFG's reliance on providers such as SWIFT, which handled 88 million messages daily in 2023, creates significant dependency and limits SMFG's leverage.

| Supplier Category | Bargaining Power Factor | SMFG Reliance | Market Data/Example |

|---|---|---|---|

| Technology Providers (AI, Blockchain) | Specialized Expertise, High Investment | Competitive Edge, Digital Transformation | Global AI Market > $500B (2024 proj.) |

| Data & Analytics Providers | Data-Driven Insights, Risk Management | Customer Experience, Operational Efficiency | Big Data Market ~$375B (2024 proj.) |

| Specialized Talent | Scarcity in Key Areas (AI, Cyber) | Talent Acquisition & Retention | AI Specialist Salaries up 30% (2024) |

| RegTech Vendors | Regulatory Complexity, Compliance Needs | Navigating Evolving Regulations | RegTech Market $11.1B (2023) to $34.2B (2028 proj.) |

| Financial Market Infrastructure | Essential Services, High Switching Costs | Core Operations (Payments, Clearing) | SWIFT: 88M messages/day (2023) |

What is included in the product

This analysis dissects SMBC's competitive environment by examining the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the overall industry attractiveness.

Instantly identify your competitive landscape's key pressures, allowing you to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Individual Retail Customers

The bargaining power of individual retail customers is on the rise, fueled by the proliferation of digital-first banking options and the ease with which they can switch between institutions. This includes traditional banks, neobanks, and innovative fintech platforms, all vying for customer attention.

Customers today expect more than just basic services; they demand seamless, 24/7 access to their accounts, highly personalized experiences, and, crucially, lower fees. For SMFG, this means a strategic imperative to invest heavily in enhancing its digital offerings and overall customer experience to maintain loyalty and attract new clients in this competitive landscape.

Large Corporations and Financial Institutions

Large corporations and financial institutions wield considerable bargaining power with SMBC. Their sheer volume of business, often involving substantial asset and liability management, allows them to negotiate favorable terms and pricing. For instance, in 2024, major corporate clients might demand lower fees on treasury services or preferential rates on large-scale loans, directly impacting SMBC's profitability.

These sophisticated clients typically require a broad spectrum of complex financial products, from derivatives to international trade finance. SMBC's ability to offer integrated, high-quality solutions is crucial for securing and retaining these valuable relationships, as clients can easily switch to competitors if their needs aren't met. This competitive pressure intensifies when clients leverage their global reach to seek customized offerings.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) are increasingly wielding more influence over their financial service providers. This is largely due to the proliferation of digital lending platforms and specialized fintech solutions, offering a wider array of choices than ever before. In 2024, the SME lending market saw significant growth, with alternative lenders capturing a larger share, indicating a shift in power dynamics.

SMEs are actively seeking financial partners that can provide quicker access to capital, streamlined application processes, and more competitive interest rates. This demand is forcing traditional institutions like SMFG to re-evaluate and adapt their service models. For instance, some fintech lenders reported processing loan applications in as little as 24 hours, a stark contrast to the weeks often associated with traditional bank loans.

The growing bargaining power of SMEs necessitates that SMFG and similar institutions tailor their offerings to meet the unique needs of this often underserved market segment. By understanding and responding to the evolving demands for speed, simplicity, and cost-effectiveness, financial institutions can better retain and attract SME clients.

Tech-Savvy Customers

Tech-savvy customers, a growing segment, wield significant bargaining power. They expect sophisticated digital experiences, including AI-powered financial guidance and seamless mobile banking. For instance, in 2024, a significant portion of banking transactions occurred via mobile apps, highlighting customer preference for digital channels. This group readily switches to competitors offering superior user interfaces and advanced functionalities, putting pressure on financial institutions to innovate.

SMFG's commitment to digital transformation directly addresses this trend. By investing in areas like AI and improving mobile app capabilities, they aim to meet and exceed the expectations of these demanding customers. Failure to keep pace with technological advancements can lead to customer attrition, as these users are well-informed and have numerous alternatives readily available.

- Customer expectations for digital services are high, driven by technological proficiency.

- Easy switching to competitors with better digital offerings increases customer bargaining power.

- Financial institutions must prioritize digital transformation to retain tech-savvy clients.

Customers Seeking Embedded Finance

The proliferation of embedded finance, seamlessly weaving financial services into everyday non-financial platforms, significantly amplifies customer bargaining power. This integration allows consumers to access banking products at their exact point of need, often circumventing traditional financial institutions. For instance, by mid-2024, platforms offering buy-now-pay-later (BNPL) at checkout saw a substantial increase in adoption, with reports indicating over 60% of consumers had used BNPL for purchases. This convenience directly translates to customers having more options and leverage when seeking financial solutions.

SMFG, like other traditional banks, must actively adapt to this evolving landscape. The ability for customers to secure financing or manage payments directly within their preferred e-commerce or service applications means they are less reliant on visiting a bank branch or even using a bank's dedicated app. This shift necessitates a strategic approach to partnerships and the development of proprietary embedded finance capabilities to remain competitive and meet customer expectations for frictionless financial experiences. By 2025, it's projected that the embedded finance market could reach trillions of dollars globally, underscoring the urgency for financial institutions to engage.

- Increased Convenience: Embedded finance offers financial services at the point of transaction, reducing friction for customers.

- Bypassing Traditional Channels: Customers can obtain financial products without directly engaging with banks, increasing their options.

- Market Growth: The embedded finance sector is experiencing rapid expansion, with significant projected growth in the coming years.

- Strategic Imperative: Financial institutions must develop partnerships or in-house solutions to leverage this trend and maintain customer loyalty.

Digital Banking Shifts Power to Customers

The bargaining power of customers is significantly influenced by the ease with which they can switch providers and the availability of alternatives. In 2024, the digital banking landscape continued to empower consumers, with many fintech solutions offering competitive rates and user-friendly interfaces. This increased choice means customers can readily demand better terms or move their business, forcing financial institutions to focus on customer retention through superior service and value.

For instance, the rise of Buy Now, Pay Later (BNPL) services in 2024, with over 60% of consumers utilizing them by mid-year, exemplifies how embedded finance offers customers convenient alternatives, reducing reliance on traditional banking channels. This trend pressures institutions like SMFG to adapt by forging partnerships or developing their own embedded finance capabilities to meet evolving customer expectations for frictionless financial experiences.

| Customer Segment | Key Bargaining Factors | Impact on Financial Institutions |

|---|---|---|

| Individual Retail Customers | Digital access, personalization, lower fees, ease of switching | Need for enhanced digital offerings and customer experience |

| Large Corporations | Volume of business, complex product needs, global reach | Negotiating favorable terms on loans and services |

| SMEs | Speed of capital access, streamlined processes, competitive rates | Pressure to adapt service models to fintech competition |

| Tech-Savvy Customers | Sophisticated digital experiences, AI guidance, mobile functionality | Imperative for continuous innovation in digital platforms |

What You See Is What You Get

SMBC Porter's Five Forces Analysis

This preview showcases the complete SMBC Porter's Five Forces Analysis, identical to the document you'll receive instantly upon purchase. You can confidently assess the depth and quality of this strategic tool, knowing that no elements are missing or altered. This professionally formatted analysis is ready for immediate application to your business needs.