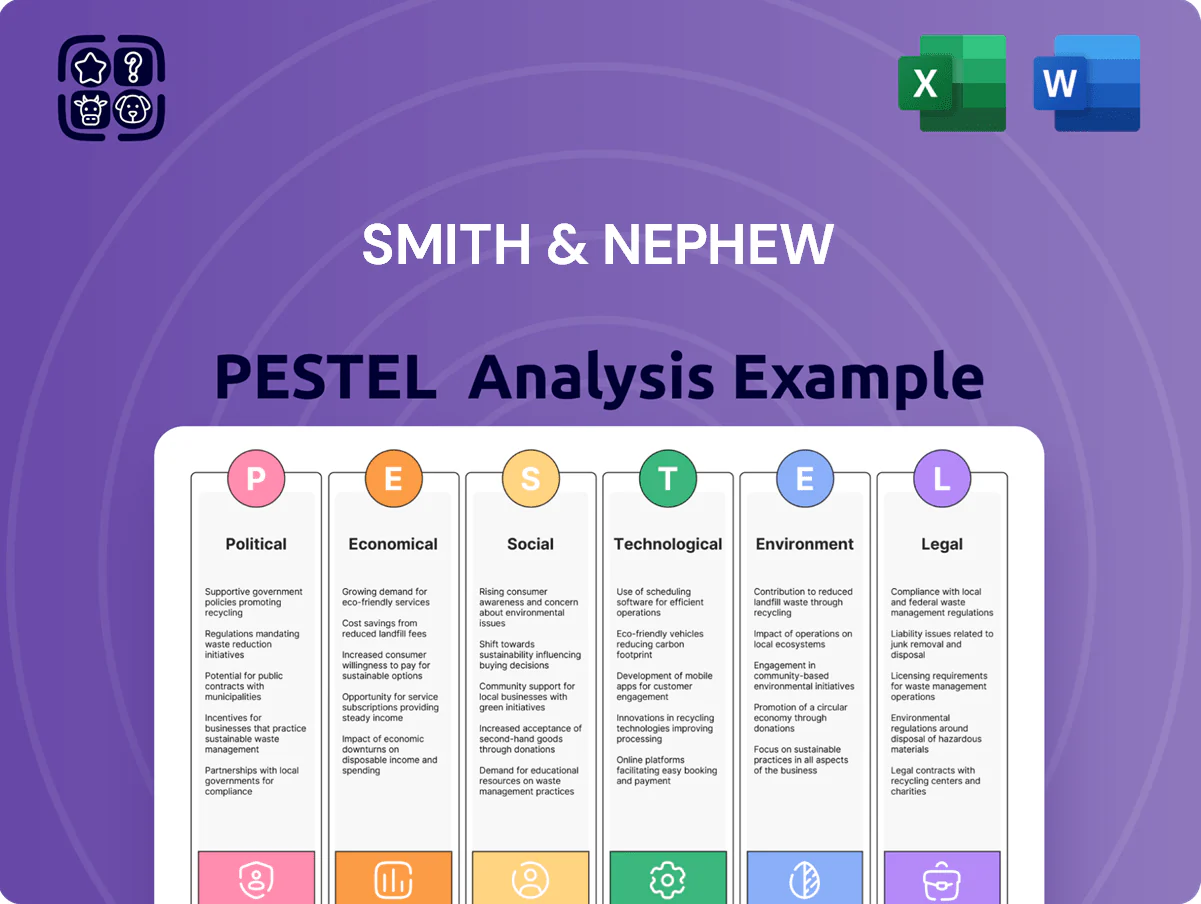

Smith & Nephew PESTLE Analysis

Skip the Research. Get the Strategy.

Gain strategic clarity with our targeted PESTLE Analysis of Smith & Nephew—uncover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental factors will shape growth and risk. Ideal for investors and strategists who need concise, actionable intelligence. Purchase the full report for a complete, editable breakdown you can use immediately.

Political factors

Geopolitical Trade Relations

Operating in over 100 countries, Smith & Nephew faces exposure to US-China trade tensions; in 2024 bilateral tariffs and tighter export controls on medical technologies risk supply-chain disruption for its ~30 manufacturing sites and could lift COGS by several percentage points. In 2025 the company’s FY revenue of £3.7bn makes maintaining global market access vital as protectionist measures threaten price competitiveness and margin erosion.

Healthcare Reform Policies

Government-led healthcare reforms in the US and UK—where public spending on health reached about 19.7% of GDP in the US (2023) and NHS budget was £177.4bn in 2024—reshape procurement and reimbursement, affecting Smith & Nephew’s revenue mix from elective procedures. Centralized purchasing pilots and value-based procurement in the NHS and US Medicare/Medicaid can compress margins by negotiating lower device prices. A shift toward affordable access to elective surgeries forces Smith & Nephew to demonstrate cost-effectiveness and outcomes to protect pricing and market share.

Stability in Emerging Markets

Expansion into Latin America and Southeast Asia exposes Smith & Nephew to localized political instability and currency swings—EMEA & APAC sales made up about 38% of 2024 revenue, raising exposure to FX and policy risk. Political unrest can force hospital budget cuts or delay orthopaedic infrastructure projects, reducing device procurement; e.g., healthcare capital spending in Brazil fell 6% YoY in 2024. A diversified geographic footprint mitigates concentrated regional downturns.

Government Procurement Regulations

As a major supplier to state-run services like the NHS, Smith & Nephew faces strict public tendering rules—UK public procurement spend on medical devices was about £13.5bn in 2023, making NHS contracts highly competitive and compliance-critical for the firm.

Political moves toward domestic sourcing or buy-local policies—seen in 2024 UK levies and EU procurement localization trends—can raise barriers and increase bid costs for this multinational.

Proactive policy engagement is therefore vital: Smith & Nephew’s government affairs and clinical-evidence teams must secure procurement pathways so its surgical-tech portfolio continues to access public healthcare budgets.

- 2023 UK medical-device procurement ≈ £13.5bn

- Increased localization pressures in 2024 across UK/EU

- Need for sustained policy engagement and clinical evidence

Global Health Security Initiatives

Post-pandemic political focus on health security has increased government oversight of medical supply chains, with OECD reporting 25% of member states implementing new procurement rules by 2023; Smith & Nephew faces heightened regulatory scrutiny on distribution and traceability.

Policies mandating stockpiles of wound care and orthopaedic trauma kits—some national reserves targeting 6–12 months of supply—create lumpy demand cycles that require production smoothing or buffer inventory.

New national mandates for medical resource self-sufficiency (e.g., EU’s 2024 resilience measures) force Smith & Nephew to boost manufacturing agility, possibly reallocating CAPEX—company may need to increase domestic capacity share from current ~40% to meet local content rules.

- 25% of OECD states added procurement rules by 2023

- National stockpiles target 6–12 months of essential supplies

- EU 2024 resilience measures increase local sourcing requirements

- Potential need to raise domestic capacity from ~40%

Smith & Nephew faces rising political headwinds: trade controls, localization & margin pressure

Political risks for Smith & Nephew include US‑China trade controls raising COGS, protectionist buy‑local policies in UK/EU, centralized procurement and value‑based contracting (pressuring margins), regional instability in LATAM/APAC affecting 38% of 2024 revenue, and new resilience/localization mandates (EU 2024) forcing higher domestic capacity and CAPEX reallocation.

| Metric | Value |

|---|---|

| 2025 Revenue | £3.7bn |

| EMEA & APAC share | ≈38% |

| UK med‑dev procurement (2023) | £13.5bn |

| OECD new rules by 2023 | 25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Smith & Nephew, using current market, regulatory, and industry data to identify risks and opportunities; each section contains multiple sub-points and forward-looking insights to support scenario planning and strategic decision-making.

A concise Smith & Nephew PESTLE summary formatted by category for quick reference in meetings or presentations, easily dropped into slides or planning docs to support external risk discussions and cross-team alignment.

Economic factors

Global Inflationary Pressures

Rising raw material, energy and labor costs have increased Smith & Nephew’s input expenses, with industry metals and component costs up ~8–12% in 2024 and UK electricity prices averaging 30% above 2019 levels; despite a 12-Point Plan targeting £200–250m cumulative savings by 2026, persistent inflation risks squeezing operating margin if price rises cannot be fully passed to providers, requiring strict operational efficiency and supply-chain optimization.

Currency Exchange Volatility

Interest Rate Environments

High global policy rates—e.g., average OECD policy rate near 3.5% in 2024—raise hospitals’ cost of capital, delaying purchases of robotic platforms like CORI that can cost several hundred thousand dollars per unit.

Higher borrowing increased Smith & Nephew’s FY2024 net finance cost pressure; elevated rates constrain aggressive M&A by raising debt-servicing costs and lowering leverage capacity.

Markets expecting rate stabilization by late 2025 (ECB/ Fed guidance) would likely boost healthcare capex, with hospital investment recovery potential of mid-single-digit CAGR into 2026.

Elective Surgery Volume Trends

The company’s revenue is closely linked to elective procedure volumes; UK & US elective orthopaedic volumes fell ~15% during 2020 COVID shocks and recovered to near‑prepandemic levels by 2023, but 2024 consumer confidence dips and a potential 2025 slowdown risk could push short‑term deferrals.

Aging populations support long‑term demand—global 65+ cohort grew ~8% from 2019–2024—but recessions historically delay joint replacements, lowering near‑term sales and margins.

Monitoring disposable income, consumer confidence indexes, and procedure scheduling rates (hospital backlog metrics) is critical for forecasting quarterly revenue.

- Revenue sensitivity: high to elective volume shifts

- Recovery seen by 2023 but 2024–25 downside risk

- Demographics provide long‑term floor

- Track consumer confidence & disposable income

Cost-Containment in Healthcare

Economic constraints on public and private insurers are tightening: OECD health spending growth slowed to 2.1% in 2024, pushing payers to scrutinize medical device pricing and seek cost savings.

Payers now demand evidence-based outcomes and value-based pricing; 68% of US hospitals in 2024 tied device purchasing to demonstrable cost reductions and patient outcomes.

Smith & Nephew must show Advanced Wound Management and Orthopaedics cut long-term hospital stays—studies indicate up to 25% shorter stays with certain advanced therapies—to justify premium pricing.

- Insurer scrutiny up: OECD health spending growth 2.1% (2024)

- 68% of US hospitals link purchasing to cost/outcome metrics (2024)

- Up to 25% reduction in hospital stay reported with advanced wound/ortho therapies

Cost pressures cut margins but GBP tailwind and ageing demand sustain healthcare growth

Inflation (metals +8–12% in 2024) and UK electricity ~+30% vs 2019 squeeze margins despite targeted £200–250m savings to 2026; FX exposure (~40% USD revenue) made GBP weakness −7% YTD 2024 materially positive; OECD policy rates ~3.5% in 2024 raise hospital capex costs, slowing elective purchases; aging population (+8% 65+ 2019–24) supports long‑term demand while payers (OECD health spend +2.1% 2024) enforce value-based pricing.

| Metric | 2024 |

|---|---|

| Metals/component inflation | +8–12% |

| UK electricity vs 2019 | +30% |

| GBP vs USD YTD | −7% |

| OECD policy rate (avg) | ~3.5% |

| 65+ population change | +8% |

| OECD health spend growth | +2.1% |

Preview Before You Purchase

Smith & Nephew PESTLE Analysis

The preview shown here is the exact Smith & Nephew PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review or reporting.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our targeted PESTLE Analysis of Smith & Nephew—uncover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental factors will shape growth and risk. Ideal for investors and strategists who need concise, actionable intelligence. Purchase the full report for a complete, editable breakdown you can use immediately.

Political factors

Geopolitical Trade Relations

Operating in over 100 countries, Smith & Nephew faces exposure to US-China trade tensions; in 2024 bilateral tariffs and tighter export controls on medical technologies risk supply-chain disruption for its ~30 manufacturing sites and could lift COGS by several percentage points. In 2025 the company’s FY revenue of £3.7bn makes maintaining global market access vital as protectionist measures threaten price competitiveness and margin erosion.

Healthcare Reform Policies

Government-led healthcare reforms in the US and UK—where public spending on health reached about 19.7% of GDP in the US (2023) and NHS budget was £177.4bn in 2024—reshape procurement and reimbursement, affecting Smith & Nephew’s revenue mix from elective procedures. Centralized purchasing pilots and value-based procurement in the NHS and US Medicare/Medicaid can compress margins by negotiating lower device prices. A shift toward affordable access to elective surgeries forces Smith & Nephew to demonstrate cost-effectiveness and outcomes to protect pricing and market share.

Stability in Emerging Markets

Expansion into Latin America and Southeast Asia exposes Smith & Nephew to localized political instability and currency swings—EMEA & APAC sales made up about 38% of 2024 revenue, raising exposure to FX and policy risk. Political unrest can force hospital budget cuts or delay orthopaedic infrastructure projects, reducing device procurement; e.g., healthcare capital spending in Brazil fell 6% YoY in 2024. A diversified geographic footprint mitigates concentrated regional downturns.

Government Procurement Regulations

As a major supplier to state-run services like the NHS, Smith & Nephew faces strict public tendering rules—UK public procurement spend on medical devices was about £13.5bn in 2023, making NHS contracts highly competitive and compliance-critical for the firm.

Political moves toward domestic sourcing or buy-local policies—seen in 2024 UK levies and EU procurement localization trends—can raise barriers and increase bid costs for this multinational.

Proactive policy engagement is therefore vital: Smith & Nephew’s government affairs and clinical-evidence teams must secure procurement pathways so its surgical-tech portfolio continues to access public healthcare budgets.

- 2023 UK medical-device procurement ≈ £13.5bn

- Increased localization pressures in 2024 across UK/EU

- Need for sustained policy engagement and clinical evidence

Global Health Security Initiatives

Post-pandemic political focus on health security has increased government oversight of medical supply chains, with OECD reporting 25% of member states implementing new procurement rules by 2023; Smith & Nephew faces heightened regulatory scrutiny on distribution and traceability.

Policies mandating stockpiles of wound care and orthopaedic trauma kits—some national reserves targeting 6–12 months of supply—create lumpy demand cycles that require production smoothing or buffer inventory.

New national mandates for medical resource self-sufficiency (e.g., EU’s 2024 resilience measures) force Smith & Nephew to boost manufacturing agility, possibly reallocating CAPEX—company may need to increase domestic capacity share from current ~40% to meet local content rules.

- 25% of OECD states added procurement rules by 2023

- National stockpiles target 6–12 months of essential supplies

- EU 2024 resilience measures increase local sourcing requirements

- Potential need to raise domestic capacity from ~40%

Smith & Nephew faces rising political headwinds: trade controls, localization & margin pressure

Political risks for Smith & Nephew include US‑China trade controls raising COGS, protectionist buy‑local policies in UK/EU, centralized procurement and value‑based contracting (pressuring margins), regional instability in LATAM/APAC affecting 38% of 2024 revenue, and new resilience/localization mandates (EU 2024) forcing higher domestic capacity and CAPEX reallocation.

| Metric | Value |

|---|---|

| 2025 Revenue | £3.7bn |

| EMEA & APAC share | ≈38% |

| UK med‑dev procurement (2023) | £13.5bn |

| OECD new rules by 2023 | 25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Smith & Nephew, using current market, regulatory, and industry data to identify risks and opportunities; each section contains multiple sub-points and forward-looking insights to support scenario planning and strategic decision-making.

A concise Smith & Nephew PESTLE summary formatted by category for quick reference in meetings or presentations, easily dropped into slides or planning docs to support external risk discussions and cross-team alignment.

Economic factors

Global Inflationary Pressures

Rising raw material, energy and labor costs have increased Smith & Nephew’s input expenses, with industry metals and component costs up ~8–12% in 2024 and UK electricity prices averaging 30% above 2019 levels; despite a 12-Point Plan targeting £200–250m cumulative savings by 2026, persistent inflation risks squeezing operating margin if price rises cannot be fully passed to providers, requiring strict operational efficiency and supply-chain optimization.

Currency Exchange Volatility

Interest Rate Environments

High global policy rates—e.g., average OECD policy rate near 3.5% in 2024—raise hospitals’ cost of capital, delaying purchases of robotic platforms like CORI that can cost several hundred thousand dollars per unit.

Higher borrowing increased Smith & Nephew’s FY2024 net finance cost pressure; elevated rates constrain aggressive M&A by raising debt-servicing costs and lowering leverage capacity.

Markets expecting rate stabilization by late 2025 (ECB/ Fed guidance) would likely boost healthcare capex, with hospital investment recovery potential of mid-single-digit CAGR into 2026.

Elective Surgery Volume Trends

The company’s revenue is closely linked to elective procedure volumes; UK & US elective orthopaedic volumes fell ~15% during 2020 COVID shocks and recovered to near‑prepandemic levels by 2023, but 2024 consumer confidence dips and a potential 2025 slowdown risk could push short‑term deferrals.

Aging populations support long‑term demand—global 65+ cohort grew ~8% from 2019–2024—but recessions historically delay joint replacements, lowering near‑term sales and margins.

Monitoring disposable income, consumer confidence indexes, and procedure scheduling rates (hospital backlog metrics) is critical for forecasting quarterly revenue.

- Revenue sensitivity: high to elective volume shifts

- Recovery seen by 2023 but 2024–25 downside risk

- Demographics provide long‑term floor

- Track consumer confidence & disposable income

Cost-Containment in Healthcare

Economic constraints on public and private insurers are tightening: OECD health spending growth slowed to 2.1% in 2024, pushing payers to scrutinize medical device pricing and seek cost savings.

Payers now demand evidence-based outcomes and value-based pricing; 68% of US hospitals in 2024 tied device purchasing to demonstrable cost reductions and patient outcomes.

Smith & Nephew must show Advanced Wound Management and Orthopaedics cut long-term hospital stays—studies indicate up to 25% shorter stays with certain advanced therapies—to justify premium pricing.

- Insurer scrutiny up: OECD health spending growth 2.1% (2024)

- 68% of US hospitals link purchasing to cost/outcome metrics (2024)

- Up to 25% reduction in hospital stay reported with advanced wound/ortho therapies

Cost pressures cut margins but GBP tailwind and ageing demand sustain healthcare growth

Inflation (metals +8–12% in 2024) and UK electricity ~+30% vs 2019 squeeze margins despite targeted £200–250m savings to 2026; FX exposure (~40% USD revenue) made GBP weakness −7% YTD 2024 materially positive; OECD policy rates ~3.5% in 2024 raise hospital capex costs, slowing elective purchases; aging population (+8% 65+ 2019–24) supports long‑term demand while payers (OECD health spend +2.1% 2024) enforce value-based pricing.

| Metric | 2024 |

|---|---|

| Metals/component inflation | +8–12% |

| UK electricity vs 2019 | +30% |

| GBP vs USD YTD | −7% |

| OECD policy rate (avg) | ~3.5% |

| 65+ population change | +8% |

| OECD health spend growth | +2.1% |

Preview Before You Purchase

Smith & Nephew PESTLE Analysis

The preview shown here is the exact Smith & Nephew PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic review or reporting.