Smurfit Kappa - Solid board & Graphic Board Operations Porter's Five Forces Analysis

Don't Miss the Bigger Picture

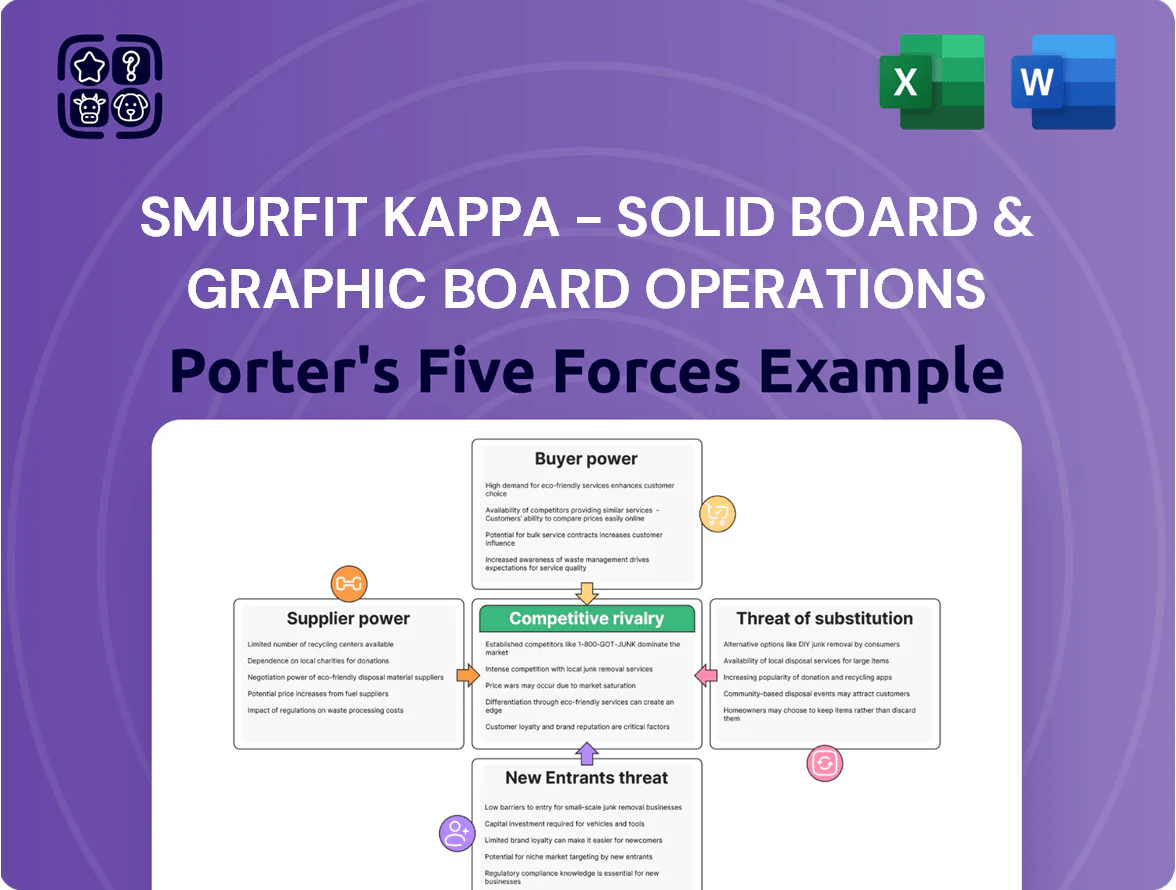

Smurfit Kappa’s Solid Board & Graphic Board operations face moderate supplier power due to pulp market concentration, intense buyer pressure from large retailers and brand owners, and significant rivalry from global packaging peers driving margin compression and innovation in sustainability.

Barriers to entry are high—capital intensity and recycling networks protect incumbents—while substitutes (flexible packaging, digital media) pose a steady, evolving threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smurfit Kappa - Solid board & Graphic Board Operations’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Raw Material Inputs

Production of solid and graphic board relies heavily on recycled fiber and wood pulp; global waste paper prices rose ~18% in 2024 and remained volatile into late 2025, driven by uneven regional collection rates (EU ~55% recovery, US ~68%).

Supply chains are sensitive: shortages in Southeast Asia and Eastern Europe pushed spot pulp costs up 12% in H1 2025, increasing input-cost risk for Smurfit Kappa’s specialized board lines.

Suppliers of high-quality virgin fiber hold leverage as tightening EU and NZ forestry rules cut available harvest volumes by ~6% in 2024–25, pressuring prices and availability.

Smurfit Kappa must actively hedge and optimize mix of recycled vs virgin fiber to protect margins; a 100-ton swing in pulp cost can change segment EBITDA by several percentage points.

Energy and Chemical Costs

Manufacturing solid board needs large electricity and thermal energy for drying; energy typically accounts for ~8–12% of variable costs in containerboard plants, so spikes hurt margins quickly.

Suppliers of industrial gases and specialty coating chemicals keep high bargaining power due to few producers and technical specs, pressuring input costs and lead times.

Smurfit Kappa faces vulnerability from energy-price volatility tied to geopolitics and net-zero policies; in 2024 it reported ~€150m annual energy procurement and uses long-term hedges plus on-site renewables like solar and biomass investments to cut exposure.

Vertical Integration Advantages

Smurfit Kappa, after integrating WestRock in 2023, owns about 40% of its fiber mills and recycling capacity, cutting third-party pulp purchases by roughly 35% and lowering input cost volatility.

This vertical integration shields operations from pulp price spikes (pulp up 18% in 2024) and limits supplier bargaining, supporting a 2025 gross margin near 22% in solid and graphic boards.

Logistics and Transportation Constraints

Logistics and freight firms hold elevated bargaining power for Smurfit Kappa’s Solid & Graphic Board ops as bulky board shipments need heavy-duty trucks and specialized trailers; global road freight rates rose ~18% in 2024 and driver shortages remain acute in EU/UK with vacancy rates ~10% (2024 Eurostat/FTA data), pushing spot rates and lead times up.

Limited specialized capacity increases transit times and per-tonne rates, so Smurfit Kappa must lock long-term contracts, use multi-modal routing, and share forecasts to protect margins and delivery reliability.

- Global road freight +18% in 2024

- EU/UK driver vacancy ~10% (2024)

- Specialized heavy haul scarcity raises lead times

- Long-term logistics contracts reduce cost volatility

Sustainability and Certification Requirements

Suppliers of FSC (Forest Stewardship Council) or PEFC (Programme for the Endorsement of Forest Certification) fibers exercise higher bargaining power because Smurfit Kappa’s customers demand fully traceable sustainable packaging, pushing the firm to source certified input to retain contracts.

Stricter rules like the EU Deforestation Regulation, tightening in late 2025, shrink the pool of compliant suppliers; certified timber and pulp producers now command price premiums—industry reports show 10–20% higher mill-gate prices for certified pulp in 2024–25.

Smurfit Kappa must prioritize certified suppliers to protect market access and ESG ratings, accepting higher input costs and potential supply concentration risk that can compress margins during peak demand.

- Certified suppliers = more leverage

- EU rule (late 2025) narrows supply

- Certified pulp premium ~10–20% (2024–25)

- Smurfit Kappa forced to accept higher costs

Supply pressures lift costs but integration preserves ~22% gross margin

Suppliers hold moderate-to-high power: recycled fiber volatility (waste paper +18% in 2024) and certified pulp premiums (10–20% in 2024–25) tighten supply; energy (~€150m annual procurement, 8–12% variable cost) and specialty chemicals/gases add leverage. Vertical integration (≈40% owned mills, -35% third-party pulp) and long-term logistics/contracts partially offset supplier power, supporting ~22% gross margin in 2025.

| Metric | Value |

|---|---|

| Waste paper price change (2024) | +18% |

| Certified pulp premium (2024–25) | 10–20% |

| Owned mills/recycling | ≈40% |

| Third-party pulp reduction | -35% |

| Energy procurement (2024) | ≈€150m |

| Solid & graphic gross margin (2025) | ≈22% |

What is included in the product

Tailored Porter’s Five Forces analysis of Smurfit Kappa – Solid Board & Graphic Board Operations, uncovering competitive drivers, buyer/supplier power, threat of substitutes and entrants, and key disruptive trends affecting pricing and profitability.

A concise Porter's Five Forces one-sheet for Smurfit Kappa's Solid Board & Graphic Board operations—quickly highlights competitive intensity and supplier/buyer leverage to speed strategic decisions.

Customers Bargaining Power

Consolidation of Global Retailers and FMCGs

Low Switching Costs for Standardized Products

In basic solid board and industrial partitions, switching costs are low, so buyers treat the product as a commodity and prioritize price; in 2024 Smurfit Kappa reported that commodity board prices fell ~6% YoY in parts of Europe, intensifying price competition.

Large customers leverage volume—up to millions of sheets per year—to pit suppliers for the lowest bids, pressuring margins; Smurfit Kappa counters by offering technical support, bespoke design services and supply-chain integration, which in 2024 drove a reported 3.5% premium on contract renewals.

Demand for Specialized Graphic Board Solutions

Customers in luxury goods, stationery and high-end displays demand specific aesthetic and structural qualities, giving them moderate bargaining power since they value consistency over lowest price; global packaging buyers paid 7–12% premiums for premium graphic boards in 2024, per industry pricing surveys. They still expect ongoing innovation in printability and tactile finishes, so Smurfit Kappa’s 22 design centres and €400m packaging R&D budget (2024) lower churn by matching specs and reducing switches to cheaper suppliers.

E-commerce Service Level Expectations

By end-2025 e-commerce sales hit about 22% of global retail, shifting bargaining power to customers demanding rapid turnaround and custom box sizes; large online retailers now require just-in-time delivery and flexibility, pressuring Smurfit Kappa to boost agility and localised capacity.

Smurfit Kappa faces risk of losing major accounts if it misses SLAs—regional converters with faster lead times (often 24–72 hours) and lower freight costs can capture share; 2024 investor reports show logistics and service performance tied to top-line retention.

- 22% global retail e-commerce (2025)

- Buyers demand JIT delivery, 24–72h lead times

- Need for localized hubs increases capex/opex

- Missed SLAs → risk of account loss to regional players

Transparency and Sustainability Mandates

Modern buyers push circular economy rules, demanding carbon-footprint data and high recycled content; a 2024 Euromonitor survey found 62% of European packaging buyers reject suppliers without clear ESG metrics.

That raises buyer power—clients can drop vendors lacking plastic-replacement options or recycled board grades, pressuring margins and innovation spend.

Smurfit Kappa has marketed sustainable design and claims 88% recycled fibre use in its corrugated and solid board portfolio in 2024 to meet these demands.

- 62% of buyers reject suppliers without ESG metrics (Euromonitor 2024)

- Smurfit Kappa reported 88% recycled fibre use in 2024

- Demand shifts raise switching risk and require R&D for plastic alternatives

Buyers Hold Sway: Discounts, Long Terms & ESG Risks Threaten Smurfit Kappa EBITDA

| Metric | 2024/25 |

|---|---|

| Buyer share of demand | 40–55% |

| Avg discounts | 8–15% |

| Payment terms | 60–120 days |

| Commodity price change | −6% YoY |

| Top-10 account revenue | €50–150m |

| R&D spend | €400m |

| E‑commerce share | 22% (2025) |

| Buyers rejecting no‑ESG | 62% |

What You See Is What You Get

Smurfit Kappa - Solid board & Graphic Board Operations Porter's Five Forces Analysis

This preview shows the exact Smurfit Kappa - Solid board & Graphic Board Operations Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, fully formatted and ready to use. The document is the complete, professionally written analysis of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Once bought, you’ll get instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Smurfit Kappa’s Solid Board & Graphic Board operations face moderate supplier power due to pulp market concentration, intense buyer pressure from large retailers and brand owners, and significant rivalry from global packaging peers driving margin compression and innovation in sustainability.

Barriers to entry are high—capital intensity and recycling networks protect incumbents—while substitutes (flexible packaging, digital media) pose a steady, evolving threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smurfit Kappa - Solid board & Graphic Board Operations’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Raw Material Inputs

Production of solid and graphic board relies heavily on recycled fiber and wood pulp; global waste paper prices rose ~18% in 2024 and remained volatile into late 2025, driven by uneven regional collection rates (EU ~55% recovery, US ~68%).

Supply chains are sensitive: shortages in Southeast Asia and Eastern Europe pushed spot pulp costs up 12% in H1 2025, increasing input-cost risk for Smurfit Kappa’s specialized board lines.

Suppliers of high-quality virgin fiber hold leverage as tightening EU and NZ forestry rules cut available harvest volumes by ~6% in 2024–25, pressuring prices and availability.

Smurfit Kappa must actively hedge and optimize mix of recycled vs virgin fiber to protect margins; a 100-ton swing in pulp cost can change segment EBITDA by several percentage points.

Energy and Chemical Costs

Manufacturing solid board needs large electricity and thermal energy for drying; energy typically accounts for ~8–12% of variable costs in containerboard plants, so spikes hurt margins quickly.

Suppliers of industrial gases and specialty coating chemicals keep high bargaining power due to few producers and technical specs, pressuring input costs and lead times.

Smurfit Kappa faces vulnerability from energy-price volatility tied to geopolitics and net-zero policies; in 2024 it reported ~€150m annual energy procurement and uses long-term hedges plus on-site renewables like solar and biomass investments to cut exposure.

Vertical Integration Advantages

Smurfit Kappa, after integrating WestRock in 2023, owns about 40% of its fiber mills and recycling capacity, cutting third-party pulp purchases by roughly 35% and lowering input cost volatility.

This vertical integration shields operations from pulp price spikes (pulp up 18% in 2024) and limits supplier bargaining, supporting a 2025 gross margin near 22% in solid and graphic boards.

Logistics and Transportation Constraints

Logistics and freight firms hold elevated bargaining power for Smurfit Kappa’s Solid & Graphic Board ops as bulky board shipments need heavy-duty trucks and specialized trailers; global road freight rates rose ~18% in 2024 and driver shortages remain acute in EU/UK with vacancy rates ~10% (2024 Eurostat/FTA data), pushing spot rates and lead times up.

Limited specialized capacity increases transit times and per-tonne rates, so Smurfit Kappa must lock long-term contracts, use multi-modal routing, and share forecasts to protect margins and delivery reliability.

- Global road freight +18% in 2024

- EU/UK driver vacancy ~10% (2024)

- Specialized heavy haul scarcity raises lead times

- Long-term logistics contracts reduce cost volatility

Sustainability and Certification Requirements

Suppliers of FSC (Forest Stewardship Council) or PEFC (Programme for the Endorsement of Forest Certification) fibers exercise higher bargaining power because Smurfit Kappa’s customers demand fully traceable sustainable packaging, pushing the firm to source certified input to retain contracts.

Stricter rules like the EU Deforestation Regulation, tightening in late 2025, shrink the pool of compliant suppliers; certified timber and pulp producers now command price premiums—industry reports show 10–20% higher mill-gate prices for certified pulp in 2024–25.

Smurfit Kappa must prioritize certified suppliers to protect market access and ESG ratings, accepting higher input costs and potential supply concentration risk that can compress margins during peak demand.

- Certified suppliers = more leverage

- EU rule (late 2025) narrows supply

- Certified pulp premium ~10–20% (2024–25)

- Smurfit Kappa forced to accept higher costs

Supply pressures lift costs but integration preserves ~22% gross margin

Suppliers hold moderate-to-high power: recycled fiber volatility (waste paper +18% in 2024) and certified pulp premiums (10–20% in 2024–25) tighten supply; energy (~€150m annual procurement, 8–12% variable cost) and specialty chemicals/gases add leverage. Vertical integration (≈40% owned mills, -35% third-party pulp) and long-term logistics/contracts partially offset supplier power, supporting ~22% gross margin in 2025.

| Metric | Value |

|---|---|

| Waste paper price change (2024) | +18% |

| Certified pulp premium (2024–25) | 10–20% |

| Owned mills/recycling | ≈40% |

| Third-party pulp reduction | -35% |

| Energy procurement (2024) | ≈€150m |

| Solid & graphic gross margin (2025) | ≈22% |

What is included in the product

Tailored Porter’s Five Forces analysis of Smurfit Kappa – Solid Board & Graphic Board Operations, uncovering competitive drivers, buyer/supplier power, threat of substitutes and entrants, and key disruptive trends affecting pricing and profitability.

A concise Porter's Five Forces one-sheet for Smurfit Kappa's Solid Board & Graphic Board operations—quickly highlights competitive intensity and supplier/buyer leverage to speed strategic decisions.

Customers Bargaining Power

Consolidation of Global Retailers and FMCGs

Low Switching Costs for Standardized Products

In basic solid board and industrial partitions, switching costs are low, so buyers treat the product as a commodity and prioritize price; in 2024 Smurfit Kappa reported that commodity board prices fell ~6% YoY in parts of Europe, intensifying price competition.

Large customers leverage volume—up to millions of sheets per year—to pit suppliers for the lowest bids, pressuring margins; Smurfit Kappa counters by offering technical support, bespoke design services and supply-chain integration, which in 2024 drove a reported 3.5% premium on contract renewals.

Demand for Specialized Graphic Board Solutions

Customers in luxury goods, stationery and high-end displays demand specific aesthetic and structural qualities, giving them moderate bargaining power since they value consistency over lowest price; global packaging buyers paid 7–12% premiums for premium graphic boards in 2024, per industry pricing surveys. They still expect ongoing innovation in printability and tactile finishes, so Smurfit Kappa’s 22 design centres and €400m packaging R&D budget (2024) lower churn by matching specs and reducing switches to cheaper suppliers.

E-commerce Service Level Expectations

By end-2025 e-commerce sales hit about 22% of global retail, shifting bargaining power to customers demanding rapid turnaround and custom box sizes; large online retailers now require just-in-time delivery and flexibility, pressuring Smurfit Kappa to boost agility and localised capacity.

Smurfit Kappa faces risk of losing major accounts if it misses SLAs—regional converters with faster lead times (often 24–72 hours) and lower freight costs can capture share; 2024 investor reports show logistics and service performance tied to top-line retention.

- 22% global retail e-commerce (2025)

- Buyers demand JIT delivery, 24–72h lead times

- Need for localized hubs increases capex/opex

- Missed SLAs → risk of account loss to regional players

Transparency and Sustainability Mandates

Modern buyers push circular economy rules, demanding carbon-footprint data and high recycled content; a 2024 Euromonitor survey found 62% of European packaging buyers reject suppliers without clear ESG metrics.

That raises buyer power—clients can drop vendors lacking plastic-replacement options or recycled board grades, pressuring margins and innovation spend.

Smurfit Kappa has marketed sustainable design and claims 88% recycled fibre use in its corrugated and solid board portfolio in 2024 to meet these demands.

- 62% of buyers reject suppliers without ESG metrics (Euromonitor 2024)

- Smurfit Kappa reported 88% recycled fibre use in 2024

- Demand shifts raise switching risk and require R&D for plastic alternatives

Buyers Hold Sway: Discounts, Long Terms & ESG Risks Threaten Smurfit Kappa EBITDA

| Metric | 2024/25 |

|---|---|

| Buyer share of demand | 40–55% |

| Avg discounts | 8–15% |

| Payment terms | 60–120 days |

| Commodity price change | −6% YoY |

| Top-10 account revenue | €50–150m |

| R&D spend | €400m |

| E‑commerce share | 22% (2025) |

| Buyers rejecting no‑ESG | 62% |

What You See Is What You Get

Smurfit Kappa - Solid board & Graphic Board Operations Porter's Five Forces Analysis

This preview shows the exact Smurfit Kappa - Solid board & Graphic Board Operations Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, fully formatted and ready to use. The document is the complete, professionally written analysis of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Once bought, you’ll get instant access to this identical file.