SNDL Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

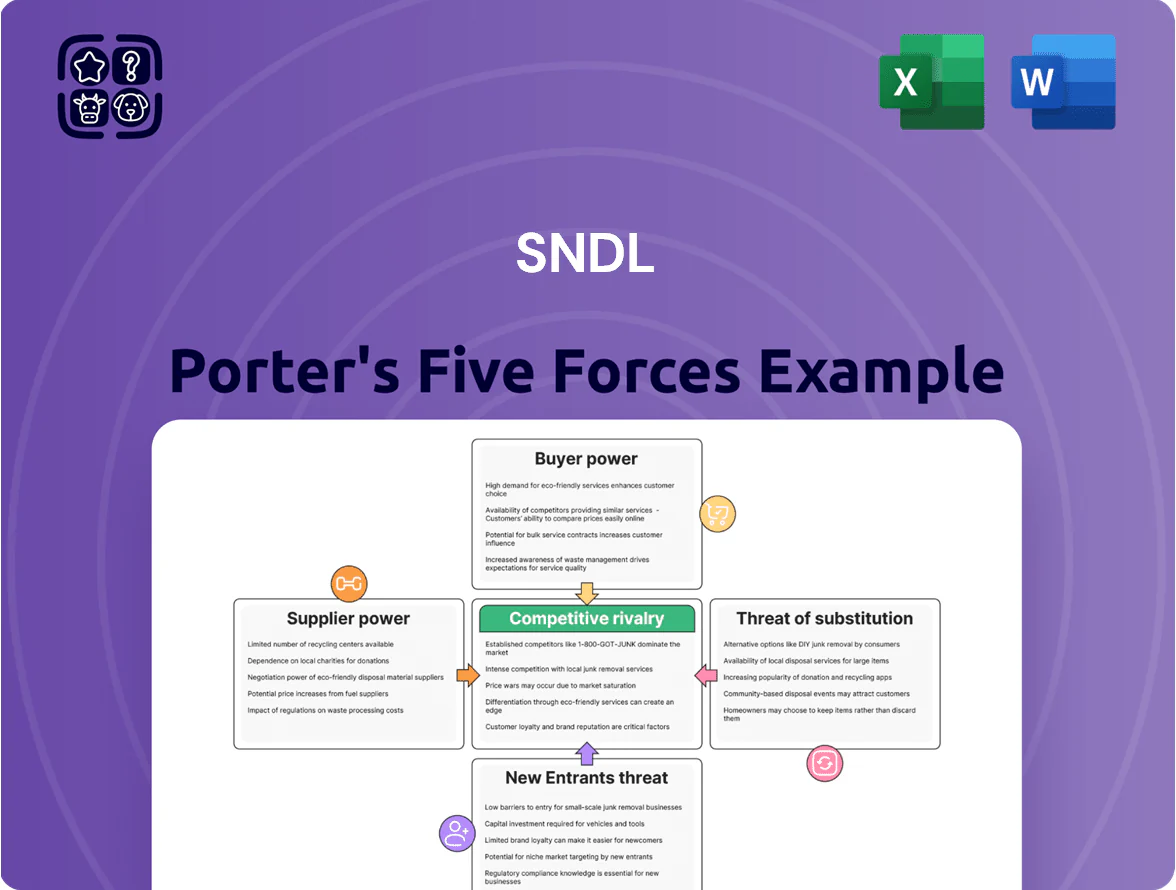

SNDL faces intense buyer pressure and margin constraints from large retail chains, moderate supplier leverage, and rising substitute threats from diversified cannabis and alternative wellness products, while regulatory complexity and capital demands raise barriers for new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SNDL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Cannabis Cultivation Landscape

The Canadian cannabis market remains saturated with over 700 licensed producers as of December 2025, creating chronic oversupply that weakens individual supplier leverage against large buyers like SNDL. This fragmentation means no single cultivator can dictate terms, letting SNDL diversify sourcing across dozens of vendors and negotiate volume discounts. In 2024 SNDL reported gross margin improvement tied to procurement and private-label scale, reflecting lower input costs from varied suppliers. As a result, supplier bargaining power is low, capping raw-material price pressure.

Vertical Integration and Self-Sourcing

SNDL has cut supplier power by owning cultivation and processing assets, producing about 60% of its biomass and over 50% of finished goods as of FY2024, so it depends less on third-party wholesalers. This vertical integration reduced COGS volatility, with input-cost swings damped compared to peers—gross margin variance fell 8 percentage points year-over-year in 2024. Internal supply also provided stock resilience during 2023–24 market shortages, lowering out-of-stock events by ~30%.

Consolidation of Liquor Wholesale

In SNDL’s liquor retail arm, large distributors and provincial liquor boards hold stronger bargaining power than cannabis growers, enforcing standardized pricing and rigid supply terms; for example, British Columbia Liquor Distribution Branch controls ~40% of provincial flow-through purchases as of 2025, tightening margins for retailers.

Access to Capital as a Supplier Constraint

- Industry mid-tiers debt/equity >1.2 (Q3 2025)

- SNDL cash ≈ CAD 250m (FY2024)

- Financing options → price concessions, exclusivity

Utility and Specialized Input Costs

Suppliers of specialized inputs—nutrients, lab gear, and high-intensity lighting—hold moderate bargaining power because their products are technical and few firms (e.g., Gavita, Fluence) set premium prices; SNDL spent ~C$48M on cultivation capex in 2024 to secure such gear.

Energy suppliers exert high power: indoor cannabis grows use ~30–50 kWh per kg, making electricity a fixed, non-negotiable cost; SNDL offsets this by boosting LED efficiency and negotiating multi-year utility contracts.

- Moderate power: specialized inputs, limited suppliers

- High power: energy—30–50 kWh/kg, fixed cost

- SNDL response: C$48M capex, efficiency upgrades, vendor diversification

SNDL: Low supplier power thanks to vertical integration, cash buffer and scale

Supplier power over SNDL is low overall due to >700 licensed producers (Dec 2025) and SNDL vertical integration (~60% biomass, FY2024), plus CAD250m cash (FY2024) enabling financing-driven leverage; moderate power exists for specialized inputs (C$48M capex 2024) and high power for energy (30–50 kWh/kg).

| Metric | Value |

|---|---|

| Licensed producers | >700 (Dec 2025) |

| Owned biomass | ~60% (FY2024) |

| Cash | CAD250m (FY2024) |

| Capex on gear | C$48M (2024) |

| Energy use | 30–50 kWh/kg |

What is included in the product

Tailored Porter's Five Forces analysis for SNDL uncovering competitive intensity, buyer/supplier leverage, threat of substitutes and new entrants, plus disruptive risks and strategic levers that influence its pricing power and profitability.

A concise Porter's Five Forces snapshot for SNDL that highlights competitive pressures and relief levers—ideal for quick strategy shifts and slide-ready summaries.

Customers Bargaining Power

High Price Sensitivity in Recreational Markets

Adult-use cannabis buyers show low brand loyalty and chase value—Surge Insights (2024) found 64% pick products by price per gram and 48% by THC, forcing SNDL to match value-tier pricing to defend share.

In Canada, average retail price fell to C$6.20/gram in 2024 (StatsCan), and digital menus let consumers compare dozens of SKUs in seconds, increasing price-based switching.

Influence of Provincial Wholesalers

Low Switching Costs for Retail Shoppers

Consumers face near-zero switching costs between cannabis brands and retail locations, so SNDL must compete on convenience, stock levels, and loyalty perks to keep shoppers returning; Canadian cannabis market churn remains high, with Ontario showing over 40% of buyers visiting multiple retailers in 2024. Retail footfall and repeat rates hinge on in-store availability—SNDL reported 12% same-store sales decline in Q3 2024 where product gaps appeared—so customer bargaining power stays strong.

Demand for Premium and Craft Segments

While value seekers still make up ~65% of Canada’s cannabis buyers, a rising 15–20% connoisseur segment pushes demand for craft-style cannabis and premium spirits, driving higher ASPs and margins.

These customers force transparency on cultivation, terpene profiles, and small-batch origin; SNDL responded in 2024 by adding premium brands and SKUs to capture this higher-margin cohort and reduce margin pressure.

Here’s the quick math: if premium ASPs are 25–40% above mainstream, a 5% shift toward connoisseurs raises blended revenue per unit by ~1.3–2%.

- SNDL portfolio diversification into premium brands (2024 additions)

- Connoisseur segment ~15–20% of market (2024 estimate)

- Premium ASPs +25–40% vs mainstream

Impact of Digital and Delivery Platforms

The rise of third-party delivery apps and online ordering gives customers instant price, potency, and review comparisons, commoditizing cannabis choices and raising churn risk for SNDL.

In 2024, Canadian cannabis online sales reached ~C$1.2B (StatCan estimate), so SNDL must invest in digital UX, POS integration, and loyalty tech to steer purchasing and protect margins.

Here’s the quick list:

- Customers compare price, potency, reviews in seconds

- Online/delivery sales ~C$1.2B Canada 2024

- SNDL needs stronger e‑commerce, POS, loyalty

Price-driven customers & provincial control squeeze margins; connoisseurs lift ASPs

Customers hold strong bargaining power: price-driven (64% by price, Surge Insights 2024) and low loyalty, aided by online menus and delivery (Canada online cannabis ≈C$1.2B 2024, StatCan). Provincial buyers control 70–90% distribution, cutting margins 3–7ppt via listing fees/returns. Connoisseurs (~15–20%) raise ASPs +25–40%; a 5% shift ups blended revenue ~1.3–2%.

| Metric | Value (2024) |

|---|---|

| Price-driven buyers | 64% |

| Online sales | C$1.2B |

| Provincial distro control | 70–90% |

| Listing fee margin hit | 3–7 ppt |

| Connoisseur share | 15–20% |

Preview Before You Purchase

SNDL Porter's Five Forces Analysis

This preview displays the exact SNDL Porter's Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download immediately with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

SNDL faces intense buyer pressure and margin constraints from large retail chains, moderate supplier leverage, and rising substitute threats from diversified cannabis and alternative wellness products, while regulatory complexity and capital demands raise barriers for new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore SNDL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Cannabis Cultivation Landscape

The Canadian cannabis market remains saturated with over 700 licensed producers as of December 2025, creating chronic oversupply that weakens individual supplier leverage against large buyers like SNDL. This fragmentation means no single cultivator can dictate terms, letting SNDL diversify sourcing across dozens of vendors and negotiate volume discounts. In 2024 SNDL reported gross margin improvement tied to procurement and private-label scale, reflecting lower input costs from varied suppliers. As a result, supplier bargaining power is low, capping raw-material price pressure.

Vertical Integration and Self-Sourcing

SNDL has cut supplier power by owning cultivation and processing assets, producing about 60% of its biomass and over 50% of finished goods as of FY2024, so it depends less on third-party wholesalers. This vertical integration reduced COGS volatility, with input-cost swings damped compared to peers—gross margin variance fell 8 percentage points year-over-year in 2024. Internal supply also provided stock resilience during 2023–24 market shortages, lowering out-of-stock events by ~30%.

Consolidation of Liquor Wholesale

In SNDL’s liquor retail arm, large distributors and provincial liquor boards hold stronger bargaining power than cannabis growers, enforcing standardized pricing and rigid supply terms; for example, British Columbia Liquor Distribution Branch controls ~40% of provincial flow-through purchases as of 2025, tightening margins for retailers.

Access to Capital as a Supplier Constraint

- Industry mid-tiers debt/equity >1.2 (Q3 2025)

- SNDL cash ≈ CAD 250m (FY2024)

- Financing options → price concessions, exclusivity

Utility and Specialized Input Costs

Suppliers of specialized inputs—nutrients, lab gear, and high-intensity lighting—hold moderate bargaining power because their products are technical and few firms (e.g., Gavita, Fluence) set premium prices; SNDL spent ~C$48M on cultivation capex in 2024 to secure such gear.

Energy suppliers exert high power: indoor cannabis grows use ~30–50 kWh per kg, making electricity a fixed, non-negotiable cost; SNDL offsets this by boosting LED efficiency and negotiating multi-year utility contracts.

- Moderate power: specialized inputs, limited suppliers

- High power: energy—30–50 kWh/kg, fixed cost

- SNDL response: C$48M capex, efficiency upgrades, vendor diversification

SNDL: Low supplier power thanks to vertical integration, cash buffer and scale

Supplier power over SNDL is low overall due to >700 licensed producers (Dec 2025) and SNDL vertical integration (~60% biomass, FY2024), plus CAD250m cash (FY2024) enabling financing-driven leverage; moderate power exists for specialized inputs (C$48M capex 2024) and high power for energy (30–50 kWh/kg).

| Metric | Value |

|---|---|

| Licensed producers | >700 (Dec 2025) |

| Owned biomass | ~60% (FY2024) |

| Cash | CAD250m (FY2024) |

| Capex on gear | C$48M (2024) |

| Energy use | 30–50 kWh/kg |

What is included in the product

Tailored Porter's Five Forces analysis for SNDL uncovering competitive intensity, buyer/supplier leverage, threat of substitutes and new entrants, plus disruptive risks and strategic levers that influence its pricing power and profitability.

A concise Porter's Five Forces snapshot for SNDL that highlights competitive pressures and relief levers—ideal for quick strategy shifts and slide-ready summaries.

Customers Bargaining Power

High Price Sensitivity in Recreational Markets

Adult-use cannabis buyers show low brand loyalty and chase value—Surge Insights (2024) found 64% pick products by price per gram and 48% by THC, forcing SNDL to match value-tier pricing to defend share.

In Canada, average retail price fell to C$6.20/gram in 2024 (StatsCan), and digital menus let consumers compare dozens of SKUs in seconds, increasing price-based switching.

Influence of Provincial Wholesalers

Low Switching Costs for Retail Shoppers

Consumers face near-zero switching costs between cannabis brands and retail locations, so SNDL must compete on convenience, stock levels, and loyalty perks to keep shoppers returning; Canadian cannabis market churn remains high, with Ontario showing over 40% of buyers visiting multiple retailers in 2024. Retail footfall and repeat rates hinge on in-store availability—SNDL reported 12% same-store sales decline in Q3 2024 where product gaps appeared—so customer bargaining power stays strong.

Demand for Premium and Craft Segments

While value seekers still make up ~65% of Canada’s cannabis buyers, a rising 15–20% connoisseur segment pushes demand for craft-style cannabis and premium spirits, driving higher ASPs and margins.

These customers force transparency on cultivation, terpene profiles, and small-batch origin; SNDL responded in 2024 by adding premium brands and SKUs to capture this higher-margin cohort and reduce margin pressure.

Here’s the quick math: if premium ASPs are 25–40% above mainstream, a 5% shift toward connoisseurs raises blended revenue per unit by ~1.3–2%.

- SNDL portfolio diversification into premium brands (2024 additions)

- Connoisseur segment ~15–20% of market (2024 estimate)

- Premium ASPs +25–40% vs mainstream

Impact of Digital and Delivery Platforms

The rise of third-party delivery apps and online ordering gives customers instant price, potency, and review comparisons, commoditizing cannabis choices and raising churn risk for SNDL.

In 2024, Canadian cannabis online sales reached ~C$1.2B (StatCan estimate), so SNDL must invest in digital UX, POS integration, and loyalty tech to steer purchasing and protect margins.

Here’s the quick list:

- Customers compare price, potency, reviews in seconds

- Online/delivery sales ~C$1.2B Canada 2024

- SNDL needs stronger e‑commerce, POS, loyalty

Price-driven customers & provincial control squeeze margins; connoisseurs lift ASPs

Customers hold strong bargaining power: price-driven (64% by price, Surge Insights 2024) and low loyalty, aided by online menus and delivery (Canada online cannabis ≈C$1.2B 2024, StatCan). Provincial buyers control 70–90% distribution, cutting margins 3–7ppt via listing fees/returns. Connoisseurs (~15–20%) raise ASPs +25–40%; a 5% shift ups blended revenue ~1.3–2%.

| Metric | Value (2024) |

|---|---|

| Price-driven buyers | 64% |

| Online sales | C$1.2B |

| Provincial distro control | 70–90% |

| Listing fee margin hit | 3–7 ppt |

| Connoisseur share | 15–20% |

Preview Before You Purchase

SNDL Porter's Five Forces Analysis

This preview displays the exact SNDL Porter's Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download immediately with no placeholders or mockups.