Snowflake Porter's Five Forces Analysis

Don't Miss the Bigger Picture

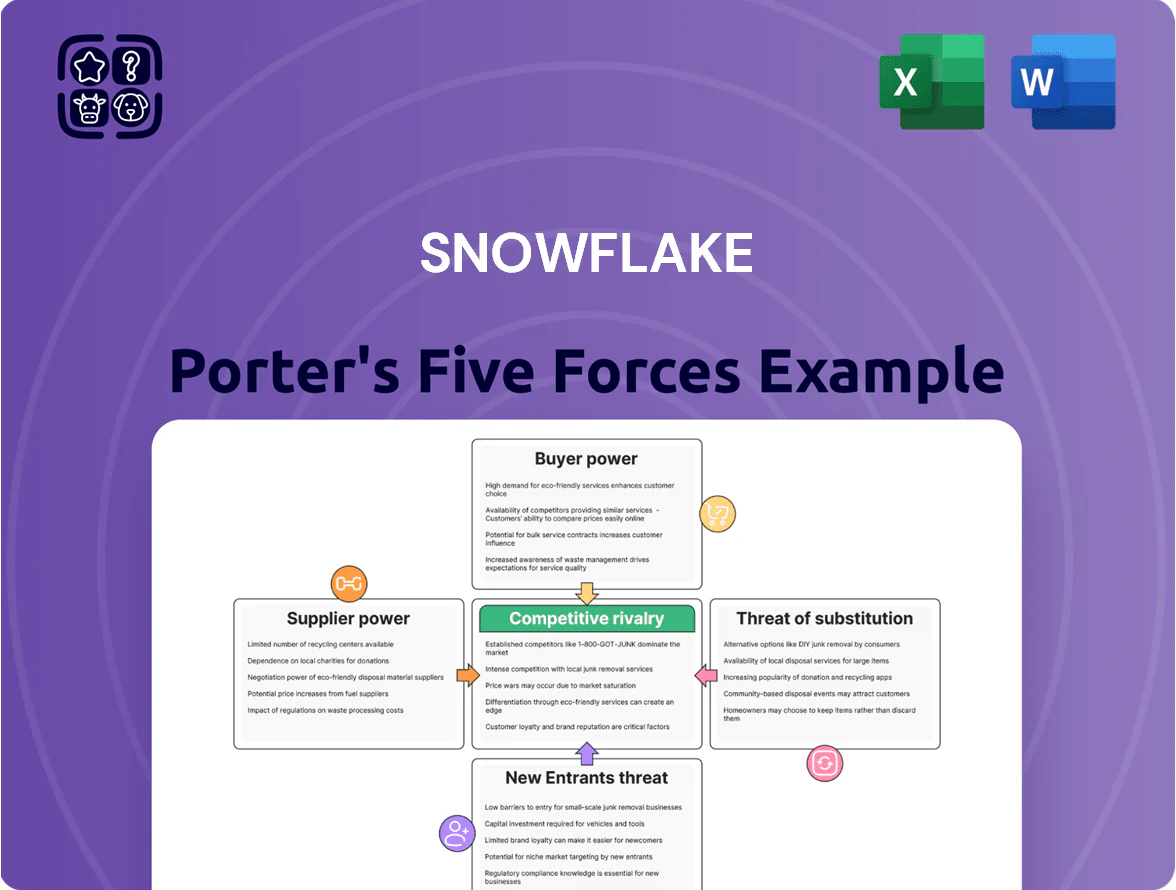

Snowflake faces intense rivalry from cloud giants and agile data-platform rivals, while strong buyer bargaining and emerging low-cost substitutes pressure pricing and margin expansion.

Supplier power is moderated by hyperscaler partnerships, but switching costs and network effects raise barriers for new entrants seeking scale quickly.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Snowflake’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Public Cloud Infrastructure Providers

Snowflake depends almost entirely on Amazon Web Services, Microsoft Azure, and Google Cloud Platform for storage and compute; in 2025 these three control roughly 64% (AWS 33%, Azure 22%, GCP 9%) of global cloud infrastructure, giving them strong pricing power over Snowflake’s margins.

Dependence on Specialized AI Hardware

As Snowflake scales generative AI via Cortex, its demand for high-performance GPUs rises; Nvidia held ~80% of discrete GPU market for AI training in 2024 and reported $110B revenue in FY2024, creating supplier leverage. Hardware shortages in 2020–22 showed GPU lead times hit 6–12 months, and a 10–30% price swing would materially raise Snowflake’s cloud costs and potentially slow Cortex adoption.

Competition for Specialized Engineering Talent

The market for cloud architects and AI researchers remained highly competitive in late 2025, with US median AI engineer wages around $190,000 and top cloud architect offers exceeding $250,000 annually, boosting supplier bargaining power. Skilled professionals act as a critical input, so Snowflake faces wage inflation and must match market packages to retain staff. Snowflake spent $1.2B on R&D and personnel-related costs in FY2025, signaling ongoing investment to curb talent drain to Big Tech and deep‑tech startups.

Third-Party Software and Data Integration Partners

Snowflake integrates with 200+ third-party vendors for ingestion, BI, and security, but relies on them to keep its platform seamless; in 2024 partner-driven connectors accounted for an estimated 18% of customer onboarding time reduction in case studies.

If major partners shift focus to rivals like Databricks, Snowflake’s ecosystem value and potential ARR growth rates (Snowflake reported $3.8bn FY2024 revenue) could face headwinds.

- 200+ partners integrated

- 18% onboarding time reduction (case studies)

- $3.8bn Snowflake FY2024 revenue at risk

- Partner defection could reduce platform stickiness

Energy and Real Estate Constraints

Energy and real estate constraints raise supplier power for Snowflake because hyperscale data centers need vast electricity and land, tying costs to local utility rates and zoning rules.

Tighter environmental rules through 2025 pushed data-center renewable sourcing and carbon offsets up; public reports show hyperscalers saw energy-related capex/O&M rise ~5–10% in 2024–25, pressures passed to cloud tenants like Snowflake.

Indirect supplier costs compress gross margins for cloud-native platforms, especially during high-usage periods and in regions with steep green-energy premiums.

- Data centers consume ~1–2% of global electricity (IEA 2023)

- Hyperscaler energy costs rose ~5–10% in 2024–25

- Carbon pricing and offsets increased unit infra cost in EU/CA

Supplier dominance (Cloud 64%, Nvidia 80%, AI pay $190k) squeezes Snowflake margins

Suppliers wield high power: AWS/Azure/GCP held ~64% cloud infra share in 2025 (AWS 33%, Azure 22%, GCP 9%), Nvidia ~80% of AI GPUs in 2024, and AI talent median pay ~ $190k (US, 2025), all pressuring Snowflake margins and growth.

| Supplier | Metric | 2024–25 |

|---|---|---|

| Cloud providers | Market share | 64% (AWS 33%, Azure 22%, GCP 9%) |

| GPU vendor | Market share | Nvidia ~80% |

| Talent | Median AI pay (US) | $190,000 |

What is included in the product

Analyzes Snowflake's competitive intensity by evaluating rivalry, buyer and supplier power, threat of entrants and substitutes, and highlights disruptive technologies and strategic barriers shaping its pricing power and growth prospects.

A concise Porter's Five Forces snapshot for Snowflake—quickly assess supplier/buyer power, threat of entrants, substitutes, and rivalry to inform strategic moves and investment decisions.

Customers Bargaining Power

High Switching Costs and Data Gravity

Moving petabytes from Snowflake often triggers multi-million-dollar egress fees and months of engineering work; a 2024 IDC estimate found median migration cost for large enterprises at $2.1M and 6–9 months of effort.

After integrating BI and ETL tools, workflow rewiring and retraining add friction, so technical lock-in raises effective switching costs and lowers existing customers’ bargaining power versus prospects.

Consumption-Based Pricing Flexibility

Snowflake’s consumption-based pricing lets customers pay only for storage and compute used, giving clear control over spend; in 2025 Snowflake reported 75% of revenue from usage-based contracts, highlighting this trend.

Buyers can optimize queries or cut usage in slow periods to lower bills without contract renegotiation; customers reducing compute by 20–40% often see proportional cost cuts.

That billing transparency creates tactical leverage: procurement can time heavy workloads or push for usage-efficiency to constrain total expenditure.

Adoption of Open Data Standards

Adoption of open formats like Apache Iceberg lets customers store data in S3/ADLS while still running Snowflake, and 2024 estimates show 28% of enterprise lakehouses using Iceberg or Delta, raising buyer leverage. By keeping data portable, firms can mix engines (Spark, Trino, Snowflake), lowering switching costs and reducing Snowflake’s proprietary lock-in. This trend boosts customer bargaining power and pressures Snowflake on pricing and feature parity.

Availability of Multi-Cloud Alternatives

Large enterprises use multi-cloud to avoid vendor lock-in, and with Databricks, Google BigQuery, and AWS Redshift offering comparable analytics, Snowflake faces strong negotiation pressure.

In 2025, top-100 customer concentration remained about 28% of Snowflake revenue, so losing a few accounts or conceding discounts materially impacts ARR; Snowflake often offers credits, lower prices, or feature bundles to retain renewals.

- Multi-cloud common: enterprise strategy

- Key rivals: Databricks, BigQuery, Redshift

- Top-100 = ~28% of revenue (2025)

- Result: discounts, credits, feature bundles

Sophistication of Enterprise Procurement

By 2025, enterprise IT teams audit cloud spend tightly; 72% of Fortune 500 firms report formal cloud-cost governance, enabling aggressive negotiations that lower list prices for large Snowflake deals.

Large buyers now demand custom pricing tiers and premium SLAs; Snowflake disclosed in 2024 that top-10 customers represented ~18% of revenue, concentrating bargaining leverage and pressuring gross margins.

Professional procurement drives longer contracts but compresses margin per dollar, forcing Snowflake to trade price for scale and retention.

- 72% Fortune 500 cloud governance (2025)

- Top-10 customers ≈18% revenue (Snowflake FY2024)

- Custom tiers + SLAs → lower realized margins

Customers wield strong leverage: high lock‑in but demand discounts, SLAs & credits

Customers hold moderate-to-strong bargaining power: high technical and egress switching costs limit churn, but usage pricing, open formats (Iceberg ~28% lakehouses, 2024), multi-cloud rivals (Databricks, BigQuery, Redshift), and concentrated top-customer revenue (Top-100 ~28% 2025; Top-10 ~18% FY2024) force discounts, custom SLAs, and credits.

| Metric | Value |

|---|---|

| Migration cost (median) | $2.1M, 6–9 mo (IDC 2024) |

| Usage revenue | 75% (2025) |

| Iceberg/Delta adoption | 28% (2024) |

Full Version Awaits

Snowflake Porter's Five Forces Analysis

This preview shows the exact Snowflake Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples: what you see is the final, professionally written file available for instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Snowflake faces intense rivalry from cloud giants and agile data-platform rivals, while strong buyer bargaining and emerging low-cost substitutes pressure pricing and margin expansion.

Supplier power is moderated by hyperscaler partnerships, but switching costs and network effects raise barriers for new entrants seeking scale quickly.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Snowflake’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Public Cloud Infrastructure Providers

Snowflake depends almost entirely on Amazon Web Services, Microsoft Azure, and Google Cloud Platform for storage and compute; in 2025 these three control roughly 64% (AWS 33%, Azure 22%, GCP 9%) of global cloud infrastructure, giving them strong pricing power over Snowflake’s margins.

Dependence on Specialized AI Hardware

As Snowflake scales generative AI via Cortex, its demand for high-performance GPUs rises; Nvidia held ~80% of discrete GPU market for AI training in 2024 and reported $110B revenue in FY2024, creating supplier leverage. Hardware shortages in 2020–22 showed GPU lead times hit 6–12 months, and a 10–30% price swing would materially raise Snowflake’s cloud costs and potentially slow Cortex adoption.

Competition for Specialized Engineering Talent

The market for cloud architects and AI researchers remained highly competitive in late 2025, with US median AI engineer wages around $190,000 and top cloud architect offers exceeding $250,000 annually, boosting supplier bargaining power. Skilled professionals act as a critical input, so Snowflake faces wage inflation and must match market packages to retain staff. Snowflake spent $1.2B on R&D and personnel-related costs in FY2025, signaling ongoing investment to curb talent drain to Big Tech and deep‑tech startups.

Third-Party Software and Data Integration Partners

Snowflake integrates with 200+ third-party vendors for ingestion, BI, and security, but relies on them to keep its platform seamless; in 2024 partner-driven connectors accounted for an estimated 18% of customer onboarding time reduction in case studies.

If major partners shift focus to rivals like Databricks, Snowflake’s ecosystem value and potential ARR growth rates (Snowflake reported $3.8bn FY2024 revenue) could face headwinds.

- 200+ partners integrated

- 18% onboarding time reduction (case studies)

- $3.8bn Snowflake FY2024 revenue at risk

- Partner defection could reduce platform stickiness

Energy and Real Estate Constraints

Energy and real estate constraints raise supplier power for Snowflake because hyperscale data centers need vast electricity and land, tying costs to local utility rates and zoning rules.

Tighter environmental rules through 2025 pushed data-center renewable sourcing and carbon offsets up; public reports show hyperscalers saw energy-related capex/O&M rise ~5–10% in 2024–25, pressures passed to cloud tenants like Snowflake.

Indirect supplier costs compress gross margins for cloud-native platforms, especially during high-usage periods and in regions with steep green-energy premiums.

- Data centers consume ~1–2% of global electricity (IEA 2023)

- Hyperscaler energy costs rose ~5–10% in 2024–25

- Carbon pricing and offsets increased unit infra cost in EU/CA

Supplier dominance (Cloud 64%, Nvidia 80%, AI pay $190k) squeezes Snowflake margins

Suppliers wield high power: AWS/Azure/GCP held ~64% cloud infra share in 2025 (AWS 33%, Azure 22%, GCP 9%), Nvidia ~80% of AI GPUs in 2024, and AI talent median pay ~ $190k (US, 2025), all pressuring Snowflake margins and growth.

| Supplier | Metric | 2024–25 |

|---|---|---|

| Cloud providers | Market share | 64% (AWS 33%, Azure 22%, GCP 9%) |

| GPU vendor | Market share | Nvidia ~80% |

| Talent | Median AI pay (US) | $190,000 |

What is included in the product

Analyzes Snowflake's competitive intensity by evaluating rivalry, buyer and supplier power, threat of entrants and substitutes, and highlights disruptive technologies and strategic barriers shaping its pricing power and growth prospects.

A concise Porter's Five Forces snapshot for Snowflake—quickly assess supplier/buyer power, threat of entrants, substitutes, and rivalry to inform strategic moves and investment decisions.

Customers Bargaining Power

High Switching Costs and Data Gravity

Moving petabytes from Snowflake often triggers multi-million-dollar egress fees and months of engineering work; a 2024 IDC estimate found median migration cost for large enterprises at $2.1M and 6–9 months of effort.

After integrating BI and ETL tools, workflow rewiring and retraining add friction, so technical lock-in raises effective switching costs and lowers existing customers’ bargaining power versus prospects.

Consumption-Based Pricing Flexibility

Snowflake’s consumption-based pricing lets customers pay only for storage and compute used, giving clear control over spend; in 2025 Snowflake reported 75% of revenue from usage-based contracts, highlighting this trend.

Buyers can optimize queries or cut usage in slow periods to lower bills without contract renegotiation; customers reducing compute by 20–40% often see proportional cost cuts.

That billing transparency creates tactical leverage: procurement can time heavy workloads or push for usage-efficiency to constrain total expenditure.

Adoption of Open Data Standards

Adoption of open formats like Apache Iceberg lets customers store data in S3/ADLS while still running Snowflake, and 2024 estimates show 28% of enterprise lakehouses using Iceberg or Delta, raising buyer leverage. By keeping data portable, firms can mix engines (Spark, Trino, Snowflake), lowering switching costs and reducing Snowflake’s proprietary lock-in. This trend boosts customer bargaining power and pressures Snowflake on pricing and feature parity.

Availability of Multi-Cloud Alternatives

Large enterprises use multi-cloud to avoid vendor lock-in, and with Databricks, Google BigQuery, and AWS Redshift offering comparable analytics, Snowflake faces strong negotiation pressure.

In 2025, top-100 customer concentration remained about 28% of Snowflake revenue, so losing a few accounts or conceding discounts materially impacts ARR; Snowflake often offers credits, lower prices, or feature bundles to retain renewals.

- Multi-cloud common: enterprise strategy

- Key rivals: Databricks, BigQuery, Redshift

- Top-100 = ~28% of revenue (2025)

- Result: discounts, credits, feature bundles

Sophistication of Enterprise Procurement

By 2025, enterprise IT teams audit cloud spend tightly; 72% of Fortune 500 firms report formal cloud-cost governance, enabling aggressive negotiations that lower list prices for large Snowflake deals.

Large buyers now demand custom pricing tiers and premium SLAs; Snowflake disclosed in 2024 that top-10 customers represented ~18% of revenue, concentrating bargaining leverage and pressuring gross margins.

Professional procurement drives longer contracts but compresses margin per dollar, forcing Snowflake to trade price for scale and retention.

- 72% Fortune 500 cloud governance (2025)

- Top-10 customers ≈18% revenue (Snowflake FY2024)

- Custom tiers + SLAs → lower realized margins

Customers wield strong leverage: high lock‑in but demand discounts, SLAs & credits

Customers hold moderate-to-strong bargaining power: high technical and egress switching costs limit churn, but usage pricing, open formats (Iceberg ~28% lakehouses, 2024), multi-cloud rivals (Databricks, BigQuery, Redshift), and concentrated top-customer revenue (Top-100 ~28% 2025; Top-10 ~18% FY2024) force discounts, custom SLAs, and credits.

| Metric | Value |

|---|---|

| Migration cost (median) | $2.1M, 6–9 mo (IDC 2024) |

| Usage revenue | 75% (2025) |

| Iceberg/Delta adoption | 28% (2024) |

Full Version Awaits

Snowflake Porter's Five Forces Analysis

This preview shows the exact Snowflake Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples: what you see is the final, professionally written file available for instant access upon payment.