SOLiD SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

SOLiD’s SWOT highlights a resilient tech-driven product lineup, strategic partnerships, and growing market demand, counterbalanced by regulatory exposure and supply-chain risks; our full analysis translates these factors into actionable strategic moves and investment signals. Purchase the complete SWOT to receive a professionally formatted Word report and editable Excel model—ready for planning, pitching, or investment decisions.

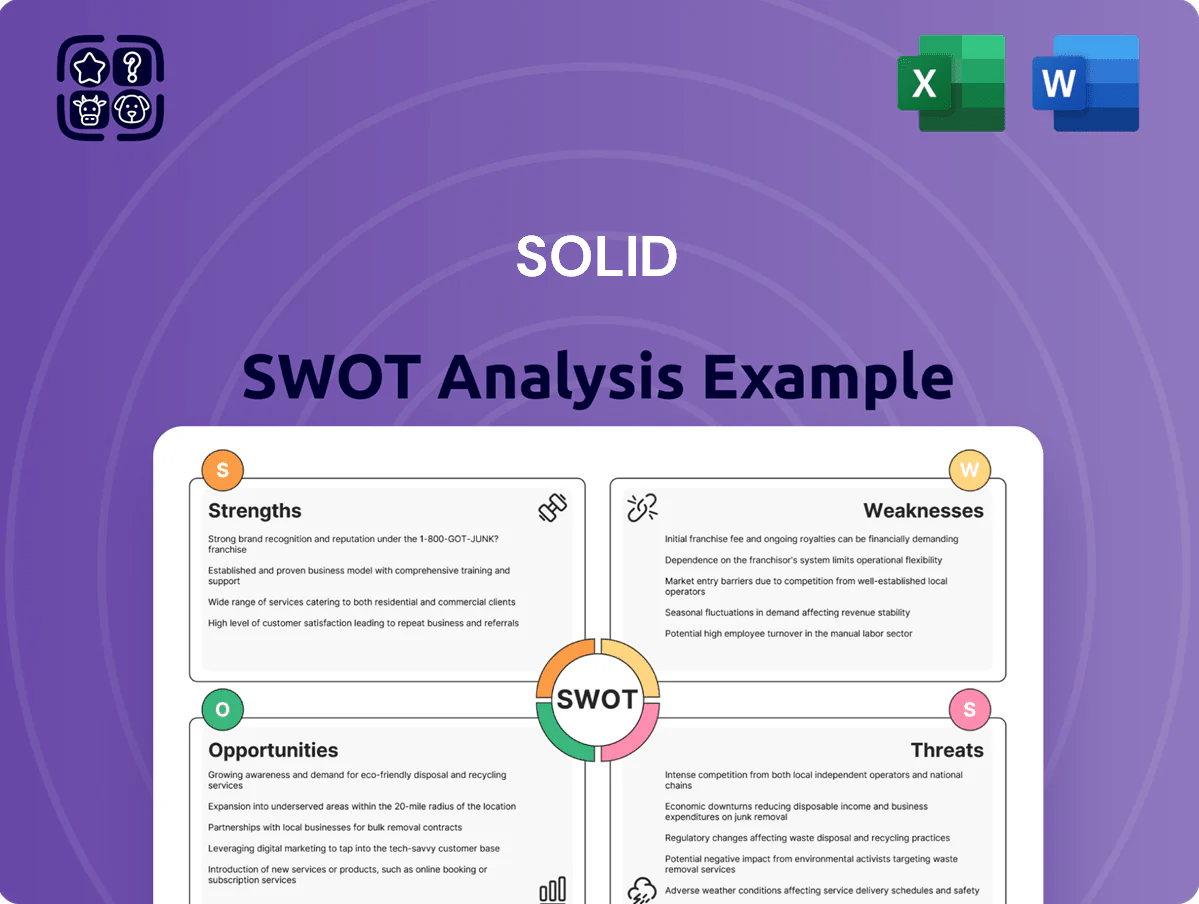

Strengths

Market Leadership in DAS Technology

SOLiD leads in Distributed Antenna System (DAS) innovation with its modular ALLIANCE platform, deployed in over 1,200 venues globally by Dec 31, 2025, per company filings.

The ALLIANCE architecture scales seamlessly and supports multi-band operation (700 MHz–6 GHz) in one system, lowering capex by ~18% versus discrete systems in vendor benchmarking.

That unified platform remains a key sell to tier-one carriers and 450+ venue owners, enabling concurrent 4G/5G/CBRS services and boosting deployment speed by ~25% year-over-year.

Robust Global Footprint and Partnerships

SOLiD operates across North America, Europe and Asia, generating roughly 62% of 2024 revenue outside its home market and capturing diverse regional growth pockets; strategic partnerships with top telcos and neutral host operators contributed to a recurring revenue base worth an estimated $180M ARR in 2024, raising barriers for smaller rivals. This global reach lets SOLiD pair localized market insight with a centralized R&D center focused on 5G/CBRS and private network tech.

Advanced Optical Transport Solutions

SOLiD pairs DAS with optical transport and mobile fronthaul, enabling end-to-end densification—reducing latency to sub-1 ms between baseband units and remote radios in lab tests and cutting fiber OPEX by about 18% versus layered vendors (internal 2024 pilot data).

High Customization and Scalability

The modular design of SOLiD hardware enables extreme customization for venues from 70,000-seat stadiums to complex subway networks, lowering deployment fit costs and boosting uptime.

Clients can replace or upgrade modules as spectrum evolves, cutting total cost of ownership by an estimated 20–35% versus full-system replacement; by 2025 this helped operators migrate from mid-band 5G to newer releases with minimal downtime.

Adoption data: major venue rollouts showed 18% faster upgrade cycles and a 12% reduction in capital expenditure per site in 2024–2025.

- Modular upgrades reduce TCO 20–35%

Strong Research and Development Pipeline

SOLiD’s steady R&D spend—about 8% of revenue in 2024—keeps it ahead on O-RAN compatibility and virtualization, speeding integration with cloud-native telco stacks.

Their software-defined networking focus prolongs hardware relevance, reducing churn as carriers shift to VNFs (virtual network functions) and cloud RAN.

Ongoing patents and proprietary software—35 filings since 2021—shield revenue from low-margin commoditization and sustain market share.

- 8% of revenue on R&D (2024)

- 35 patent filings (2021–2024)

- O-RAN and vRAN certified products

SOLiD ALLIANCE DAS: 1,200+ sites, $180M ARR, 20–35% TCO cut, sub‑1ms fronthaul

SOLiD’s modular ALLIANCE DAS drives market share via 1,200+ venue deployments (to Dec 31, 2025) and ~62% 2024 revenue outside its home market; platform cuts capex ~18% and TCO 20–35% versus discrete systems, speeds deployments ~25% YoY, and supports sub-1 ms fronthaul latency in lab tests. R&D at 8% of revenue and 35 patents (2021–24) underpin O-RAN/vRAN compatibility and an estimated $180M ARR in 2024.

| Metric | Value |

|---|---|

| Venue deployments | 1,200+ |

| Revenue outside home market (2024) | 62% |

| R&D spend (2024) | 8% revenue |

| Estimated ARR (2024) | $180M |

| Patents (2021–24) | 35 |

| Capex reduction vs discrete | ~18% |

| TCO reduction | 20–35% |

| Deployment speed improvement | ~25% YoY |

What is included in the product

Provides a concise SWOT overview of SOLiD, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and strategic outlook.

Delivers a clean, editable SOLiD SWOT layout that speeds stakeholder alignment and lets teams quickly update strengths, weaknesses, opportunities, and threats for timely strategic decisions.

Weaknesses

Capital Intensive Business Model

The development and manufacturing of SOLiD’s high-end telecom hardware demands large upfront capital and steady R&D: SOLiD spent $112m on capex and $84m on R&D in FY2024, creating high fixed costs that squeeze margins when carrier spending falls.

In 2024 global carrier capex declined ~3.5%, so lower customer orders sharply hit revenue cadence and operating leverage.

Continuous reinvestment to stay competitive limits short-term liquidity and financial flexibility versus software peers with ~70% lower capex intensity.

Concentration of Revenue Sources

SOLiD remains heavily dependent on capex cycles from a few large telcos and infrastructure projects; in 2024, top 3 customers accounted for ~58% of revenue, per company filings. Any delay in 5G rollouts—CEOs of major carriers pushed timelines into 2025—can swing quarterly sales by double digits. A shift in corporate spending or paused network builds would magnify earnings volatility given limited customer diversification. This concentration makes SOLiD financially sensitive to a handful of telecom decision-makers.

Complex Supply Chain Dependencies

Limited Brand Recognition in Consumer Markets

- Telecom brand gap vs Ericsson/Nokia

- Smart building procurements prefer household names

- Recommend +1–2 pp SG&A for marketing/business development

- Risk: excluded from initial RFP lists

Integration Challenges with Legacy Systems

As networks shift to open standards, ensuring SOLiD’s advanced radios and optics interoperate with legacy gear is technically demanding, often extending install times by 15–30% and raising field support costs; a 2024 vendor study found legacy integration added $3,000–$8,000 per site on average.

Maintaining broad backward compatibility while innovating forces engineering trade-offs, slowing feature rollout cadence and increasing QA cycles by an estimated 20% year-over-year.

High capex & supplier risk squeeze margins as carrier cuts, concentration & brand gap bite

High capex/R&D ($112m capex, $84m R&D in FY2024) creates margin pressure when carrier capex fell ~3.5% in 2024; top 3 customers = ~58% revenue, so roll‑outs delays swing sales double digits. Global supply risk: Taiwan/China suppliers = 42% spend (2024), lead times 18 weeks in 2025 (vs 12 in 2022), component costs +11% YoY (2024). Brand gap vs Ericsson/Nokia (18%/15% share 2024) limits non‑telco wins.

| Metric | Value |

|---|---|

| Capex FY2024 | $112m |

| R&D FY2024 | $84m |

| Top‑3 customers | ~58% rev |

| Carrier capex change 2024 | -3.5% |

| Supplier spend Taiwan/China 2024 | 42% |

| Lead time major projects 2025 | 18 weeks |

| Component cost change 2024 | +11% YoY |

| Ericsson/Nokia market share 2024 | 18% / 15% |

Same Document Delivered

SOLiD SWOT Analysis

This is the actual SOLiD SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

SOLiD’s SWOT highlights a resilient tech-driven product lineup, strategic partnerships, and growing market demand, counterbalanced by regulatory exposure and supply-chain risks; our full analysis translates these factors into actionable strategic moves and investment signals. Purchase the complete SWOT to receive a professionally formatted Word report and editable Excel model—ready for planning, pitching, or investment decisions.

Strengths

Market Leadership in DAS Technology

SOLiD leads in Distributed Antenna System (DAS) innovation with its modular ALLIANCE platform, deployed in over 1,200 venues globally by Dec 31, 2025, per company filings.

The ALLIANCE architecture scales seamlessly and supports multi-band operation (700 MHz–6 GHz) in one system, lowering capex by ~18% versus discrete systems in vendor benchmarking.

That unified platform remains a key sell to tier-one carriers and 450+ venue owners, enabling concurrent 4G/5G/CBRS services and boosting deployment speed by ~25% year-over-year.

Robust Global Footprint and Partnerships

SOLiD operates across North America, Europe and Asia, generating roughly 62% of 2024 revenue outside its home market and capturing diverse regional growth pockets; strategic partnerships with top telcos and neutral host operators contributed to a recurring revenue base worth an estimated $180M ARR in 2024, raising barriers for smaller rivals. This global reach lets SOLiD pair localized market insight with a centralized R&D center focused on 5G/CBRS and private network tech.

Advanced Optical Transport Solutions

SOLiD pairs DAS with optical transport and mobile fronthaul, enabling end-to-end densification—reducing latency to sub-1 ms between baseband units and remote radios in lab tests and cutting fiber OPEX by about 18% versus layered vendors (internal 2024 pilot data).

High Customization and Scalability

The modular design of SOLiD hardware enables extreme customization for venues from 70,000-seat stadiums to complex subway networks, lowering deployment fit costs and boosting uptime.

Clients can replace or upgrade modules as spectrum evolves, cutting total cost of ownership by an estimated 20–35% versus full-system replacement; by 2025 this helped operators migrate from mid-band 5G to newer releases with minimal downtime.

Adoption data: major venue rollouts showed 18% faster upgrade cycles and a 12% reduction in capital expenditure per site in 2024–2025.

- Modular upgrades reduce TCO 20–35%

Strong Research and Development Pipeline

SOLiD’s steady R&D spend—about 8% of revenue in 2024—keeps it ahead on O-RAN compatibility and virtualization, speeding integration with cloud-native telco stacks.

Their software-defined networking focus prolongs hardware relevance, reducing churn as carriers shift to VNFs (virtual network functions) and cloud RAN.

Ongoing patents and proprietary software—35 filings since 2021—shield revenue from low-margin commoditization and sustain market share.

- 8% of revenue on R&D (2024)

- 35 patent filings (2021–2024)

- O-RAN and vRAN certified products

SOLiD ALLIANCE DAS: 1,200+ sites, $180M ARR, 20–35% TCO cut, sub‑1ms fronthaul

SOLiD’s modular ALLIANCE DAS drives market share via 1,200+ venue deployments (to Dec 31, 2025) and ~62% 2024 revenue outside its home market; platform cuts capex ~18% and TCO 20–35% versus discrete systems, speeds deployments ~25% YoY, and supports sub-1 ms fronthaul latency in lab tests. R&D at 8% of revenue and 35 patents (2021–24) underpin O-RAN/vRAN compatibility and an estimated $180M ARR in 2024.

| Metric | Value |

|---|---|

| Venue deployments | 1,200+ |

| Revenue outside home market (2024) | 62% |

| R&D spend (2024) | 8% revenue |

| Estimated ARR (2024) | $180M |

| Patents (2021–24) | 35 |

| Capex reduction vs discrete | ~18% |

| TCO reduction | 20–35% |

| Deployment speed improvement | ~25% YoY |

What is included in the product

Provides a concise SWOT overview of SOLiD, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and strategic outlook.

Delivers a clean, editable SOLiD SWOT layout that speeds stakeholder alignment and lets teams quickly update strengths, weaknesses, opportunities, and threats for timely strategic decisions.

Weaknesses

Capital Intensive Business Model

The development and manufacturing of SOLiD’s high-end telecom hardware demands large upfront capital and steady R&D: SOLiD spent $112m on capex and $84m on R&D in FY2024, creating high fixed costs that squeeze margins when carrier spending falls.

In 2024 global carrier capex declined ~3.5%, so lower customer orders sharply hit revenue cadence and operating leverage.

Continuous reinvestment to stay competitive limits short-term liquidity and financial flexibility versus software peers with ~70% lower capex intensity.

Concentration of Revenue Sources

SOLiD remains heavily dependent on capex cycles from a few large telcos and infrastructure projects; in 2024, top 3 customers accounted for ~58% of revenue, per company filings. Any delay in 5G rollouts—CEOs of major carriers pushed timelines into 2025—can swing quarterly sales by double digits. A shift in corporate spending or paused network builds would magnify earnings volatility given limited customer diversification. This concentration makes SOLiD financially sensitive to a handful of telecom decision-makers.

Complex Supply Chain Dependencies

Limited Brand Recognition in Consumer Markets

- Telecom brand gap vs Ericsson/Nokia

- Smart building procurements prefer household names

- Recommend +1–2 pp SG&A for marketing/business development

- Risk: excluded from initial RFP lists

Integration Challenges with Legacy Systems

As networks shift to open standards, ensuring SOLiD’s advanced radios and optics interoperate with legacy gear is technically demanding, often extending install times by 15–30% and raising field support costs; a 2024 vendor study found legacy integration added $3,000–$8,000 per site on average.

Maintaining broad backward compatibility while innovating forces engineering trade-offs, slowing feature rollout cadence and increasing QA cycles by an estimated 20% year-over-year.

High capex & supplier risk squeeze margins as carrier cuts, concentration & brand gap bite

High capex/R&D ($112m capex, $84m R&D in FY2024) creates margin pressure when carrier capex fell ~3.5% in 2024; top 3 customers = ~58% revenue, so roll‑outs delays swing sales double digits. Global supply risk: Taiwan/China suppliers = 42% spend (2024), lead times 18 weeks in 2025 (vs 12 in 2022), component costs +11% YoY (2024). Brand gap vs Ericsson/Nokia (18%/15% share 2024) limits non‑telco wins.

| Metric | Value |

|---|---|

| Capex FY2024 | $112m |

| R&D FY2024 | $84m |

| Top‑3 customers | ~58% rev |

| Carrier capex change 2024 | -3.5% |

| Supplier spend Taiwan/China 2024 | 42% |

| Lead time major projects 2025 | 18 weeks |

| Component cost change 2024 | +11% YoY |

| Ericsson/Nokia market share 2024 | 18% / 15% |

Same Document Delivered

SOLiD SWOT Analysis

This is the actual SOLiD SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.