Sonae SGPS, S.A PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Sonae SGPS, S.A. faces regulatory shifts, economic cyclicality, and accelerating digital disruption that reshape its retail and diversified holdings; environmental obligations and evolving consumer behavior further pressure margins and strategy. Gain a competitive edge with our in-depth PESTLE Analysis—crafted specifically for Sonae SGPS, S.A. Download the full version now and get actionable intelligence at your fingertips.

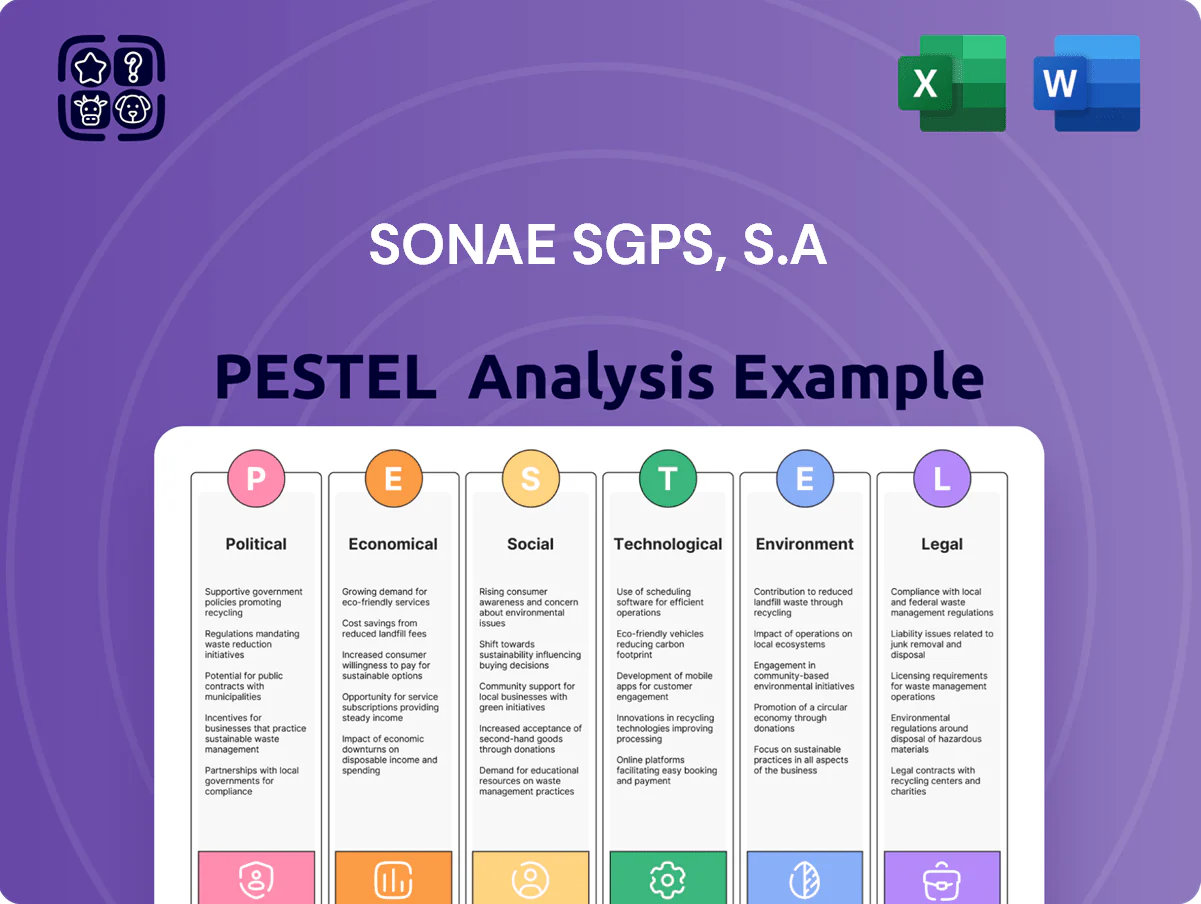

Political factors

Geopolitical Stability in Iberia

Geopolitical stability in Iberia is central to Sonae SGPS as Portugal and Spain account for over 80% of its 2024 revenue, making government shifts and fiscal policy changes material to investment security.

Changes in regional coalitions or VAT and property tax reforms can directly affect Sonae's retail margins and real estate valuations, where Portugal retail sales rose 3.8% y/y in 2024.

By end-2025, alignment with EU trade directives—notably logistics and customs rules tied to the EU Single Market—will be critical for cross-border supply chains that handled roughly 70% of Sonae's Iberian goods flows in 2024.

European Union Regulatory Influence

Sonae SGPS is subject to EU digital markets and competition rules, with its telecom/tech units monitored under the DMA and EU antitrust framework; in 2024 the European Commission levied fines totaling over €7.5bn for DMA/antitrust breaches across sectors, underscoring enforcement risk. Compliance avoids penalties and leverages single-market access—EU rules facilitate cross-border operations that supported Sonae’s €6.1bn 2024 group revenue. Strategic plans must incorporate rising Eurozone economic oversight, including tighter merger controls and state aid scrutiny.

International Trade Relations

Sonae’s operations across Portugal, Spain, and Brazil make it sensitive to EU–Mercosur trade dynamics; changes to tariffs could affect its retail import bill, which for 2024 saw non-EU sourced goods represent an estimated 18% of group procurement spend. Fluctuating duties or regulatory barriers would raise COGS for specialized imports and logistic costs across its global sourcing network. The group’s diversified footprint—over 1,000 stores in Iberia and Latin America and international sourcing from 12 countries—reduces exposure to localized protectionism.

Taxation Policies and Fiscal Reforms

Rising national corporate tax rates and possible windfall taxes on retail or energy—Portugal’s corporate rate 21% (2025) and recent EU discussions on windfall levies—could compress Sonae’s EBITDA margins and EPS, reducing distributable profits.

Shifts toward austerity or reduced public spending in Portugal, Spain or Brazil can lower consumer spending; Portugal’s real household consumption fell 1.2% YoY in 2024 in some quarters, signaling demand risk for Sonae’s retail units.

Operating across Portugal, Spain and Brazil forces Sonae to manage transfer pricing, withholding taxes and repatriation rules, affecting capital allocation and dividends while aiming to preserve ROIC targets.

- Portugal corporate tax: 21% (2025)

- Potential windfall levies under EU/ national debate

- Portugal real household consumption down ~1.2% YoY in parts of 2024

- Cross-jurisdiction tax complexity impacts dividend repatriation and ROIC

Public Infrastructure Investment

Government commitments to digital infrastructure and transport boost Sonae’s e-commerce and logistics, with Portugal allocating €2.7bn from 2021–2027 for digital transition and mobility projects that improve delivery efficiency.

Political backing for 5G rollout and high-speed rail expansion enhances connectivity for Sonae’s telecommunications arm and retail supply chains; Portugal targets nationwide 5G by 2025 and €4.3bn in rail investments through 2030.

Strategic public–private partnerships give Sonae first-mover advantages in smart city initiatives, leveraging municipal pilot projects and EU recovery funds—Portugal received €13.9bn from NextGenerationEU aiding such collaborations.

- €2.7bn national digital/mobility funding (2021–2027)

- Nationwide 5G target by 2025; €4.3bn rail investment to 2030

- €13.9bn NextGenerationEU for Portugal enabling smart city PPPs

Sonae political risks: Iberian taxes, EU enforcement, and supply‑chain exposure

Political risk for Sonae centers on Iberian fiscal shifts, EU competition/DMA enforcement, and cross-border tax/tariff changes affecting margins and supply chains; Portugal corporate tax 21% (2025), Portugal real household consumption down ~1.2% YoY in parts of 2024, non-EU goods ~18% of 2024 procurement; EU fines €7.5bn in 2024 underscore compliance risk.

| Metric | Value |

|---|---|

| Portugal corp tax | 21% (2025) |

| Household consumption | -1.2% YoY (2024, parts) |

| Non-EU procurement | ~18% (2024) |

| EU antitrust fines (2024) | €7.5bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sonae SGPS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Sonae SGPS, S.A. that distills political, economic, social, technological, legal, and environmental factors for quick reference in meetings and strategy sessions.

Economic factors

Inflationary Pressures and Purchasing Power

Persistent Eurozone inflation averaged 5.8% in 2025 YTD, forcing Sonae to trade off price competitiveness and margin preservation in food retail; same-store price increases boosted grocery ASPs but compressed EBIT margins in 1H25. Rising cost-of-living drove consumers to private-labels—Sonae MC’s private-label penetration reached ~34% of sales in 2025—supporting volume resilience. Analysts should track real wage growth (Eurozone real wages up 0.6% YoY in 2025 Q1) versus Sonae’s sales volumes across formats.

Interest Rate Environment

The European Central Bank's policy directly affects Sonae SGPS financing costs for capital-intensive projects like shopping center developments; the ECB's main refinancing rate rose to 4.50% in 2023–2024, pushing borrowing costs and compressing real estate valuations. Higher rates increased interest expense on the group's leverage, reducing NAV and weighted-average cost of capital for new investments. By late 2025, ECB rates began stabilizing near 3.75–4.00%, offering more predictability for long-term projects and refinancing decisions.

Currency Exchange Rate Volatility

Operating in South America exposes Sonae to currency volatility that affects Euro consolidation; in 2024, BRL fell ~6% vs EUR, lowering reported revenues from Brazilian operations.

Significant devaluations in emerging markets can erode dollar-denominated asset and dividend values—Latin American currency declines wiped an estimated 8–12% off local asset values for comparable multinationals in 2023–24.

Hedging strategies are essential: Sonae reported using FX forwards and cross-currency swaps to cover ~60–75% of short-term exposure in 2024, protecting the balance sheet from non-Euro swings.

Labor Market Dynamics

- Minimum wage 2024: 910 EUR (+6.1%)

- Sonae personnel costs +5–7% YoY (2024)

- Automation can cut labor hours 10–30%

- Platform work growth ~3–5% annually

Consumer Confidence Levels

Economic uncertainty reduces discretionary spend, hitting Sonae’s fashion and specialized retail harder than grocery; Portuguese retail sales fell 1.8% YoY in 2024 Q3, weighing on apparel demand.

Higher consumer confidence boosts footfall in Sonae’s shopping centers and sales of high-margin electronics/apparel; Portugal consumer confidence rose to -6 in Dec 2025 from -12 in Dec 2024, correlating with a 4% increase in Sonae MC’s non-food sales in 2025 H1.

Monitoring regional sentiment indices enables Sonae to tweak inventory and marketing; Sonae reported a 7% reduction in markdowns in 2025 after adopting quarterly sentiment-led assortment changes.

- Discretionary spend vulnerability: 1.8% YoY retail decline (2024 Q3)

- Confidence rebound: index -12 to -6 (Dec 2024–Dec 2025)

- Sales impact: +4% non-food sales (2025 H1)

- Operational benefit: 7% fewer markdowns post-sentiment adjustments

Inflation bites margins; private label lifts volumes as FX and rates pressure NAV

Eurozone inflation (5.8% YTD 2025) pressured margins despite higher ASPs; private-label penetration rose to ~34% (2025) supporting volumes. ECB rate normalization to ~3.75–4.00% by late 2025 eased refinancing risk after peaks at 4.50% (2023–24); interest costs compressed NAV. BRL weakness (~-6% vs EUR in 2024) cut consolidated revenues; Sonae hedged ~60–75% short-term FX exposure (2024).

| Metric | Value |

|---|---|

| Eurozone inflation 2025 YTD | 5.8% |

| Sonae private-label (2025) | ~34% sales |

| ECB rate (late 2025) | 3.75–4.00% |

| BRL vs EUR (2024) | -6% |

| FX hedged (2024) | 60–75% |

Same Document Delivered

Sonae SGPS, S.A PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Sonae SGPS, S.A. you’ll receive after purchase—fully formatted, comprehensive, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Sonae SGPS, S.A. faces regulatory shifts, economic cyclicality, and accelerating digital disruption that reshape its retail and diversified holdings; environmental obligations and evolving consumer behavior further pressure margins and strategy. Gain a competitive edge with our in-depth PESTLE Analysis—crafted specifically for Sonae SGPS, S.A. Download the full version now and get actionable intelligence at your fingertips.

Political factors

Geopolitical Stability in Iberia

Geopolitical stability in Iberia is central to Sonae SGPS as Portugal and Spain account for over 80% of its 2024 revenue, making government shifts and fiscal policy changes material to investment security.

Changes in regional coalitions or VAT and property tax reforms can directly affect Sonae's retail margins and real estate valuations, where Portugal retail sales rose 3.8% y/y in 2024.

By end-2025, alignment with EU trade directives—notably logistics and customs rules tied to the EU Single Market—will be critical for cross-border supply chains that handled roughly 70% of Sonae's Iberian goods flows in 2024.

European Union Regulatory Influence

Sonae SGPS is subject to EU digital markets and competition rules, with its telecom/tech units monitored under the DMA and EU antitrust framework; in 2024 the European Commission levied fines totaling over €7.5bn for DMA/antitrust breaches across sectors, underscoring enforcement risk. Compliance avoids penalties and leverages single-market access—EU rules facilitate cross-border operations that supported Sonae’s €6.1bn 2024 group revenue. Strategic plans must incorporate rising Eurozone economic oversight, including tighter merger controls and state aid scrutiny.

International Trade Relations

Sonae’s operations across Portugal, Spain, and Brazil make it sensitive to EU–Mercosur trade dynamics; changes to tariffs could affect its retail import bill, which for 2024 saw non-EU sourced goods represent an estimated 18% of group procurement spend. Fluctuating duties or regulatory barriers would raise COGS for specialized imports and logistic costs across its global sourcing network. The group’s diversified footprint—over 1,000 stores in Iberia and Latin America and international sourcing from 12 countries—reduces exposure to localized protectionism.

Taxation Policies and Fiscal Reforms

Rising national corporate tax rates and possible windfall taxes on retail or energy—Portugal’s corporate rate 21% (2025) and recent EU discussions on windfall levies—could compress Sonae’s EBITDA margins and EPS, reducing distributable profits.

Shifts toward austerity or reduced public spending in Portugal, Spain or Brazil can lower consumer spending; Portugal’s real household consumption fell 1.2% YoY in 2024 in some quarters, signaling demand risk for Sonae’s retail units.

Operating across Portugal, Spain and Brazil forces Sonae to manage transfer pricing, withholding taxes and repatriation rules, affecting capital allocation and dividends while aiming to preserve ROIC targets.

- Portugal corporate tax: 21% (2025)

- Potential windfall levies under EU/ national debate

- Portugal real household consumption down ~1.2% YoY in parts of 2024

- Cross-jurisdiction tax complexity impacts dividend repatriation and ROIC

Public Infrastructure Investment

Government commitments to digital infrastructure and transport boost Sonae’s e-commerce and logistics, with Portugal allocating €2.7bn from 2021–2027 for digital transition and mobility projects that improve delivery efficiency.

Political backing for 5G rollout and high-speed rail expansion enhances connectivity for Sonae’s telecommunications arm and retail supply chains; Portugal targets nationwide 5G by 2025 and €4.3bn in rail investments through 2030.

Strategic public–private partnerships give Sonae first-mover advantages in smart city initiatives, leveraging municipal pilot projects and EU recovery funds—Portugal received €13.9bn from NextGenerationEU aiding such collaborations.

- €2.7bn national digital/mobility funding (2021–2027)

- Nationwide 5G target by 2025; €4.3bn rail investment to 2030

- €13.9bn NextGenerationEU for Portugal enabling smart city PPPs

Sonae political risks: Iberian taxes, EU enforcement, and supply‑chain exposure

Political risk for Sonae centers on Iberian fiscal shifts, EU competition/DMA enforcement, and cross-border tax/tariff changes affecting margins and supply chains; Portugal corporate tax 21% (2025), Portugal real household consumption down ~1.2% YoY in parts of 2024, non-EU goods ~18% of 2024 procurement; EU fines €7.5bn in 2024 underscore compliance risk.

| Metric | Value |

|---|---|

| Portugal corp tax | 21% (2025) |

| Household consumption | -1.2% YoY (2024, parts) |

| Non-EU procurement | ~18% (2024) |

| EU antitrust fines (2024) | €7.5bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sonae SGPS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Sonae SGPS, S.A. that distills political, economic, social, technological, legal, and environmental factors for quick reference in meetings and strategy sessions.

Economic factors

Inflationary Pressures and Purchasing Power

Persistent Eurozone inflation averaged 5.8% in 2025 YTD, forcing Sonae to trade off price competitiveness and margin preservation in food retail; same-store price increases boosted grocery ASPs but compressed EBIT margins in 1H25. Rising cost-of-living drove consumers to private-labels—Sonae MC’s private-label penetration reached ~34% of sales in 2025—supporting volume resilience. Analysts should track real wage growth (Eurozone real wages up 0.6% YoY in 2025 Q1) versus Sonae’s sales volumes across formats.

Interest Rate Environment

The European Central Bank's policy directly affects Sonae SGPS financing costs for capital-intensive projects like shopping center developments; the ECB's main refinancing rate rose to 4.50% in 2023–2024, pushing borrowing costs and compressing real estate valuations. Higher rates increased interest expense on the group's leverage, reducing NAV and weighted-average cost of capital for new investments. By late 2025, ECB rates began stabilizing near 3.75–4.00%, offering more predictability for long-term projects and refinancing decisions.

Currency Exchange Rate Volatility

Operating in South America exposes Sonae to currency volatility that affects Euro consolidation; in 2024, BRL fell ~6% vs EUR, lowering reported revenues from Brazilian operations.

Significant devaluations in emerging markets can erode dollar-denominated asset and dividend values—Latin American currency declines wiped an estimated 8–12% off local asset values for comparable multinationals in 2023–24.

Hedging strategies are essential: Sonae reported using FX forwards and cross-currency swaps to cover ~60–75% of short-term exposure in 2024, protecting the balance sheet from non-Euro swings.

Labor Market Dynamics

- Minimum wage 2024: 910 EUR (+6.1%)

- Sonae personnel costs +5–7% YoY (2024)

- Automation can cut labor hours 10–30%

- Platform work growth ~3–5% annually

Consumer Confidence Levels

Economic uncertainty reduces discretionary spend, hitting Sonae’s fashion and specialized retail harder than grocery; Portuguese retail sales fell 1.8% YoY in 2024 Q3, weighing on apparel demand.

Higher consumer confidence boosts footfall in Sonae’s shopping centers and sales of high-margin electronics/apparel; Portugal consumer confidence rose to -6 in Dec 2025 from -12 in Dec 2024, correlating with a 4% increase in Sonae MC’s non-food sales in 2025 H1.

Monitoring regional sentiment indices enables Sonae to tweak inventory and marketing; Sonae reported a 7% reduction in markdowns in 2025 after adopting quarterly sentiment-led assortment changes.

- Discretionary spend vulnerability: 1.8% YoY retail decline (2024 Q3)

- Confidence rebound: index -12 to -6 (Dec 2024–Dec 2025)

- Sales impact: +4% non-food sales (2025 H1)

- Operational benefit: 7% fewer markdowns post-sentiment adjustments

Inflation bites margins; private label lifts volumes as FX and rates pressure NAV

Eurozone inflation (5.8% YTD 2025) pressured margins despite higher ASPs; private-label penetration rose to ~34% (2025) supporting volumes. ECB rate normalization to ~3.75–4.00% by late 2025 eased refinancing risk after peaks at 4.50% (2023–24); interest costs compressed NAV. BRL weakness (~-6% vs EUR in 2024) cut consolidated revenues; Sonae hedged ~60–75% short-term FX exposure (2024).

| Metric | Value |

|---|---|

| Eurozone inflation 2025 YTD | 5.8% |

| Sonae private-label (2025) | ~34% sales |

| ECB rate (late 2025) | 3.75–4.00% |

| BRL vs EUR (2024) | -6% |

| FX hedged (2024) | 60–75% |

Same Document Delivered

Sonae SGPS, S.A PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Sonae SGPS, S.A. you’ll receive after purchase—fully formatted, comprehensive, and ready to use for strategic decision-making.