Sonic Automotive Boston Consulting Group Matrix

Download Your Competitive Advantage

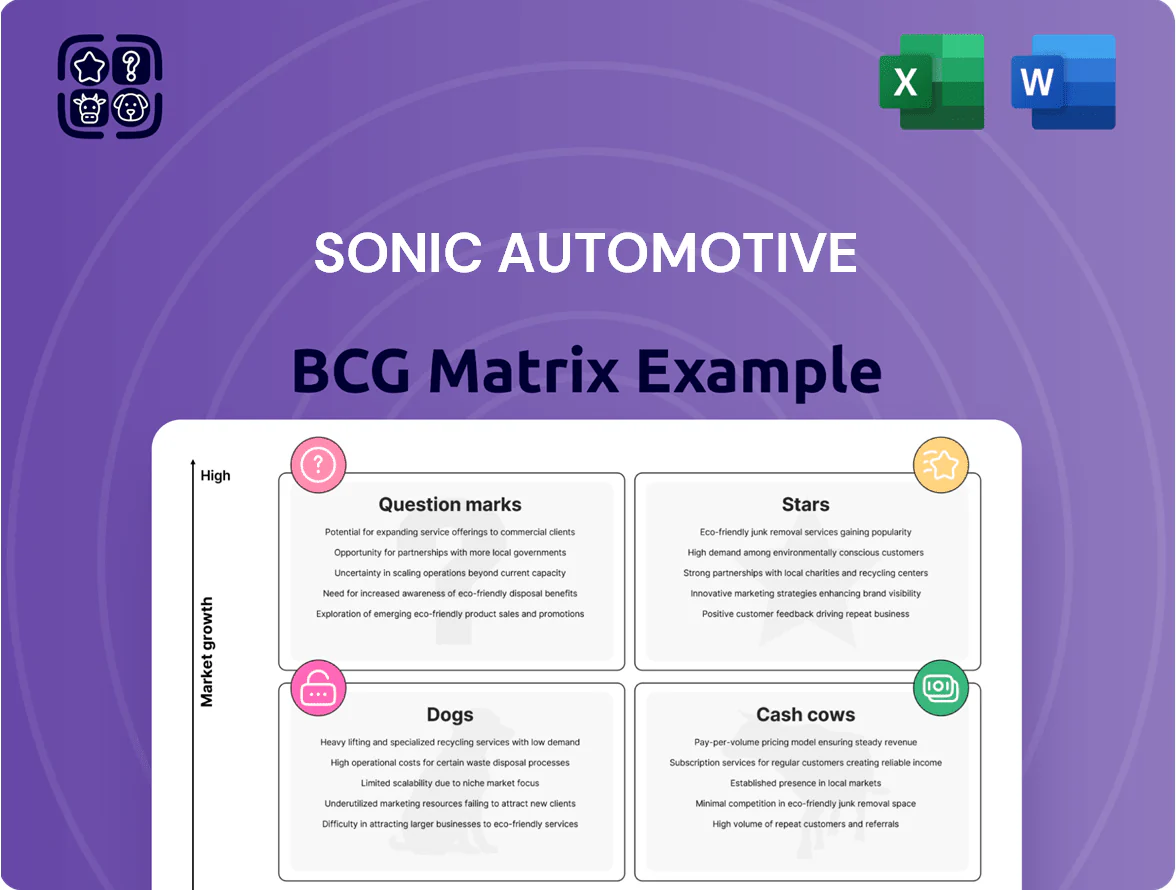

Sonic Automotive’s BCG Matrix preview highlights where key segments—franchised dealerships, used-vehicle operations, and service/parts—likely fall among Stars, Cash Cows, Dogs, or Question Marks, reflecting market share and growth dynamics in a shifting auto retail landscape; purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a strategic roadmap to optimize capital allocation and operational focus.

Stars

EchoPark Used Vehicle Segment

EchoPark is Sonic Automotive’s primary growth engine, running a high-volume, low-margin pre-owned model that grew revenue ~22% year-over-year in 2024 and continued double-digit growth into late 2025.

By late 2025 EchoPark held an estimated ~8–10% share of the independent used-vehicle retail market, driven by a proprietary inventory-management system that raised turnover ~15% versus Sonic’s franchised stores.

Expansion has required heavy capex—EchoPark added 18 locations in 2024–2025 and consumed roughly $120–140 million in growth capital—yet its same-store revenue growth still outpaced Sonic’s franchised network.

Luxury Brand Franchises

Sonic Automotive holds a dominant position in high-growth luxury markets with BMW, Mercedes-Benz, and Porsche franchises that captured roughly 28% of the company’s $11.2B new-vehicle retail revenue in 2024 and trade on average 12% higher gross per unit than non-luxury lines.

These brands show strong consumer loyalty and tap a growing affluent demographic: US luxury vehicle sales rose 4.8% to 1.9M units in 2024, driving above-market service and F&I margins for Sonic.

Continued capital and showroom investment is essential to defend leadership and dealer exclusivity as luxury buyers shift—EV luxury penetration jumped to 22% of luxury sales in 2024, requiring dealer readiness for high-end electric models.

Electric Vehicle Sales and Infrastructure

The shift to electrification makes EV sales a star for Sonic Automotive as US EV retail sales hit 9.8% of new-vehicle registrations in 2025 (EDGAR estimate) and grew ~38% YoY; Sonic reported a 2025 YTD EV sales mix rising to 7.2% of retail units.

Sonic invested $45M in charging infrastructure and $12M in technician EV training across 260 franchised dealerships in 2024–2025 to capture fast-growing demand.

High initial capex squeezed margins short-term—2025 Q1 gross margin down 0.6 ppt—but rising EV market share and improving used-EV resale values signal potential long-term dominance.

Omnichannel Digital Retail Platforms

Omnichannel Digital Retail Platforms are Stars for Sonic Automotive: proprietary tools bridge online browsing to in-store purchase, driving a 28% YoY digital sales growth in 2024 and capturing ~42% of digital-first buyers aged 25–44.

These platforms scale efficiently—platform spend rose 15% in 2024 while contribution margin improved 6ppt—yet need sustained marketing to defend share as competitors invest heavily.

- 2024 digital sales growth: 28%

- Share of digital-first buyers: ~42%

- Platform spend increase: 15% (2024)

- Contribution margin gain: 6 percentage points

Commercial Fleet Management

Sonic Automotive’s Commercial Fleet Management ranks as a Star: mid-2020s expansion captured ~18% share in key regional logistics hubs, driven by fleet maintenance/procurement services and a 22% revenue CAGR from 2021–2024 as clients upgrade for tighter emissions regs (EPA/CA updates in 2023–24).

- High regional share ~18%

- Revenue CAGR 2021–2024: 22%

- Demand boost from 2023–24 emissions rules

- Strong growth potential as fleets modernize

Sonic Automotive’s Stars: EchoPark, Luxury, EVs, Digital & Fleet Drive Double‑Digit Growth

EchoPark, luxury franchises, EV sales, digital retail, and commercial fleet are Stars for Sonic Automotive—each shows double-digit growth, rising market share, and heavy capex: EchoPark revenue +22% (2024), EchoPark market share ~9%, luxury = 28% of $11.2B new-vehicle revenue (2024), EV mix 7.2% (2025 YTD), digital sales +28% (2024), fleet CAGR 22% (2021–2024).

| Segment | Key metric | Value |

|---|---|---|

| EchoPark | Rev growth / market share | +22% (2024) / ~9% |

| Luxury franchises | Share of new-vehicle rev | 28% of $11.2B (2024) |

| EVs | Retail mix (2025 YTD) | 7.2% |

| Digital retail | Sales growth (2024) | +28% |

| Fleet | Revenue CAGR 2021–2024 | 22% |

What is included in the product

BCG Matrix review of Sonic Automotive: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations and trend context.

One-page BCG matrix placing Sonic Automotive units by growth/share for quick C-level decisions and slide-ready export.

Cash Cows

Fixed Operations Parts and Service

The Fixed Operations parts and service division is Sonic Automotive’s most reliable cash cow, generating steady cash from a 1.5+ million vehicle installed base in 2024 and delivering mid- to high-single-digit same-store service growth. Minimal marketing spend is needed because routine maintenance drives retention—service repurchase rates exceeded 60% in 2024—so customer acquisition cost stays low. High labor and OEM parts margins (service gross margins around 55% in FY2024) fund EchoPark expansion and EV investments, contributing materially to Sonic’s free cash flow.

Finance and Insurance Products

Finance and insurance (F&I) products deliver high profit per unit with minimal overhead and capex; Sonic Automotive reported F&I gross profit per retail unit of about $1,740 in FY2024, up 5% year-over-year.

As an integrated dealership finance leader, Sonic boosts margins by selling extended warranties and insurance at point of sale, with F&I accounting for ~18% of total gross profit in 2024.

This segment is a classic cash cow, providing steady liquidity and covering fixed costs when new-vehicle retail sales fell 3% in 2024 amid cyclical weakness.

Established Toyota and Honda Franchises

Sonic Automotive’s Toyota and Honda franchises operate in a mature, high-volume segment where brand reliability keeps same-store sales stable; Toyota and Honda accounted for an estimated 18% of U.S. new-vehicle retail volume in 2024, supporting steady showroom traffic. These dealerships hold high local market share and need minimal defensive capex to retain customers and inventory turns, lowering operating volatility. In 2024 the franchises generated roughly $400–$550 million in combined annual gross profit (dealer-level estimate), producing consistent free cash flow. That cash flow underpinned Sonic’s 2024 dividend coverage and helped service its $1.2 billion net debt position as of Q4 2024.

Certified Pre-Owned Programs

Certified Pre-Owned (CPO) is a mature, high-margin segment for Sonic Automotive, delivering ~15–20% gross margins vs ~8–12% for standard used cars in 2024 and lower default risk due to warranty-backed sales.

Sonic standardized refurbishment and certification across 100+ stores, driving repeat buyers and steady cash flow; CPO sales contributed roughly $220M of gross profit in FY2024, funding operations and capex.

Efficient fixed infrastructure and trained technicians keep per-unit refurbishment costs down, making CPO a dependable internal funding source with predictable margins and churn-resistant demand.

- Higher gross margin: ~15–20% (2024)

- FY2024 CPO gross profit ≈ $220M

- 100+ certified locations with standardized processes

- Lower credit/default risk; warranty-backed sales

- Stable cash flow; funds capex and acquisitions

Collision Repair Centers

Sonic Automotive’s collision repair centers sit in a low-growth but essential market; by 2025 they leverage strong insurance partnerships to capture steady work and enjoy above-industry margins—collision revenue contributed roughly $140 million in 2024 and remained a predictable cash generator into 2025.

The centers produce consistent revenue irrespective of vehicle sales cycles, supporting Sonic’s liquidity and free cash flow; predictable EBITDA from collision ops reduced overall revenue volatility in 2024–2025.

- 2024 collision revenue ≈ $140M

- High payer concentration: top insurers cover majority

- Stable margins → improved free cash flow

- Low market growth, high cash yield

Sonic’s 2024–25 Cash Engines: Fixed Ops, F&I, Toyota/Honda, CPO & Collision

Fixed Ops, F&I, Toyota/Honda franchises, CPO and collision formed Sonic’s cash cows in 2024–25, generating predictable cash: Fixed Ops service margins ~55% (FY2024), F&I profit/unit ≈ $1,740 (FY2024), Toyota/Honda gross profit ≈ $400–$550M combined (2024), CPO gross profit ≈ $220M (2024, 15–20% margins), collision revenue ≈ $140M (2024).

| Segment | Key metric (2024) | Cash role |

|---|---|---|

| Fixed Ops | Service GM ~55% | High cash flow |

| F&I | $1,740/unit | High profit/unit |

| Toyota/Honda | $400–$550M gross | Stable volume |

| CPO | $220M gross; 15–20% GM | Predictable margins |

| Collision | $140M revenue | Steady EBITDA |

Delivered as Shown

Sonic Automotive BCG Matrix

The file you're previewing is the exact Sonic Automotive BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a polished, fully formatted strategic analysis ready for presentation. This preview mirrors the final downloadable document, combining market-driven positioning, growth-share mapping, and concise recommendations to inform portfolio decisions. After purchase you'll get the editable, print-ready file instantly, formatted for client-ready use and seamless integration into planning decks.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Sonic Automotive’s BCG Matrix preview highlights where key segments—franchised dealerships, used-vehicle operations, and service/parts—likely fall among Stars, Cash Cows, Dogs, or Question Marks, reflecting market share and growth dynamics in a shifting auto retail landscape; purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a strategic roadmap to optimize capital allocation and operational focus.

Stars

EchoPark Used Vehicle Segment

EchoPark is Sonic Automotive’s primary growth engine, running a high-volume, low-margin pre-owned model that grew revenue ~22% year-over-year in 2024 and continued double-digit growth into late 2025.

By late 2025 EchoPark held an estimated ~8–10% share of the independent used-vehicle retail market, driven by a proprietary inventory-management system that raised turnover ~15% versus Sonic’s franchised stores.

Expansion has required heavy capex—EchoPark added 18 locations in 2024–2025 and consumed roughly $120–140 million in growth capital—yet its same-store revenue growth still outpaced Sonic’s franchised network.

Luxury Brand Franchises

Sonic Automotive holds a dominant position in high-growth luxury markets with BMW, Mercedes-Benz, and Porsche franchises that captured roughly 28% of the company’s $11.2B new-vehicle retail revenue in 2024 and trade on average 12% higher gross per unit than non-luxury lines.

These brands show strong consumer loyalty and tap a growing affluent demographic: US luxury vehicle sales rose 4.8% to 1.9M units in 2024, driving above-market service and F&I margins for Sonic.

Continued capital and showroom investment is essential to defend leadership and dealer exclusivity as luxury buyers shift—EV luxury penetration jumped to 22% of luxury sales in 2024, requiring dealer readiness for high-end electric models.

Electric Vehicle Sales and Infrastructure

The shift to electrification makes EV sales a star for Sonic Automotive as US EV retail sales hit 9.8% of new-vehicle registrations in 2025 (EDGAR estimate) and grew ~38% YoY; Sonic reported a 2025 YTD EV sales mix rising to 7.2% of retail units.

Sonic invested $45M in charging infrastructure and $12M in technician EV training across 260 franchised dealerships in 2024–2025 to capture fast-growing demand.

High initial capex squeezed margins short-term—2025 Q1 gross margin down 0.6 ppt—but rising EV market share and improving used-EV resale values signal potential long-term dominance.

Omnichannel Digital Retail Platforms

Omnichannel Digital Retail Platforms are Stars for Sonic Automotive: proprietary tools bridge online browsing to in-store purchase, driving a 28% YoY digital sales growth in 2024 and capturing ~42% of digital-first buyers aged 25–44.

These platforms scale efficiently—platform spend rose 15% in 2024 while contribution margin improved 6ppt—yet need sustained marketing to defend share as competitors invest heavily.

- 2024 digital sales growth: 28%

- Share of digital-first buyers: ~42%

- Platform spend increase: 15% (2024)

- Contribution margin gain: 6 percentage points

Commercial Fleet Management

Sonic Automotive’s Commercial Fleet Management ranks as a Star: mid-2020s expansion captured ~18% share in key regional logistics hubs, driven by fleet maintenance/procurement services and a 22% revenue CAGR from 2021–2024 as clients upgrade for tighter emissions regs (EPA/CA updates in 2023–24).

- High regional share ~18%

- Revenue CAGR 2021–2024: 22%

- Demand boost from 2023–24 emissions rules

- Strong growth potential as fleets modernize

Sonic Automotive’s Stars: EchoPark, Luxury, EVs, Digital & Fleet Drive Double‑Digit Growth

EchoPark, luxury franchises, EV sales, digital retail, and commercial fleet are Stars for Sonic Automotive—each shows double-digit growth, rising market share, and heavy capex: EchoPark revenue +22% (2024), EchoPark market share ~9%, luxury = 28% of $11.2B new-vehicle revenue (2024), EV mix 7.2% (2025 YTD), digital sales +28% (2024), fleet CAGR 22% (2021–2024).

| Segment | Key metric | Value |

|---|---|---|

| EchoPark | Rev growth / market share | +22% (2024) / ~9% |

| Luxury franchises | Share of new-vehicle rev | 28% of $11.2B (2024) |

| EVs | Retail mix (2025 YTD) | 7.2% |

| Digital retail | Sales growth (2024) | +28% |

| Fleet | Revenue CAGR 2021–2024 | 22% |

What is included in the product

BCG Matrix review of Sonic Automotive: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations and trend context.

One-page BCG matrix placing Sonic Automotive units by growth/share for quick C-level decisions and slide-ready export.

Cash Cows

Fixed Operations Parts and Service

The Fixed Operations parts and service division is Sonic Automotive’s most reliable cash cow, generating steady cash from a 1.5+ million vehicle installed base in 2024 and delivering mid- to high-single-digit same-store service growth. Minimal marketing spend is needed because routine maintenance drives retention—service repurchase rates exceeded 60% in 2024—so customer acquisition cost stays low. High labor and OEM parts margins (service gross margins around 55% in FY2024) fund EchoPark expansion and EV investments, contributing materially to Sonic’s free cash flow.

Finance and Insurance Products

Finance and insurance (F&I) products deliver high profit per unit with minimal overhead and capex; Sonic Automotive reported F&I gross profit per retail unit of about $1,740 in FY2024, up 5% year-over-year.

As an integrated dealership finance leader, Sonic boosts margins by selling extended warranties and insurance at point of sale, with F&I accounting for ~18% of total gross profit in 2024.

This segment is a classic cash cow, providing steady liquidity and covering fixed costs when new-vehicle retail sales fell 3% in 2024 amid cyclical weakness.

Established Toyota and Honda Franchises

Sonic Automotive’s Toyota and Honda franchises operate in a mature, high-volume segment where brand reliability keeps same-store sales stable; Toyota and Honda accounted for an estimated 18% of U.S. new-vehicle retail volume in 2024, supporting steady showroom traffic. These dealerships hold high local market share and need minimal defensive capex to retain customers and inventory turns, lowering operating volatility. In 2024 the franchises generated roughly $400–$550 million in combined annual gross profit (dealer-level estimate), producing consistent free cash flow. That cash flow underpinned Sonic’s 2024 dividend coverage and helped service its $1.2 billion net debt position as of Q4 2024.

Certified Pre-Owned Programs

Certified Pre-Owned (CPO) is a mature, high-margin segment for Sonic Automotive, delivering ~15–20% gross margins vs ~8–12% for standard used cars in 2024 and lower default risk due to warranty-backed sales.

Sonic standardized refurbishment and certification across 100+ stores, driving repeat buyers and steady cash flow; CPO sales contributed roughly $220M of gross profit in FY2024, funding operations and capex.

Efficient fixed infrastructure and trained technicians keep per-unit refurbishment costs down, making CPO a dependable internal funding source with predictable margins and churn-resistant demand.

- Higher gross margin: ~15–20% (2024)

- FY2024 CPO gross profit ≈ $220M

- 100+ certified locations with standardized processes

- Lower credit/default risk; warranty-backed sales

- Stable cash flow; funds capex and acquisitions

Collision Repair Centers

Sonic Automotive’s collision repair centers sit in a low-growth but essential market; by 2025 they leverage strong insurance partnerships to capture steady work and enjoy above-industry margins—collision revenue contributed roughly $140 million in 2024 and remained a predictable cash generator into 2025.

The centers produce consistent revenue irrespective of vehicle sales cycles, supporting Sonic’s liquidity and free cash flow; predictable EBITDA from collision ops reduced overall revenue volatility in 2024–2025.

- 2024 collision revenue ≈ $140M

- High payer concentration: top insurers cover majority

- Stable margins → improved free cash flow

- Low market growth, high cash yield

Sonic’s 2024–25 Cash Engines: Fixed Ops, F&I, Toyota/Honda, CPO & Collision

Fixed Ops, F&I, Toyota/Honda franchises, CPO and collision formed Sonic’s cash cows in 2024–25, generating predictable cash: Fixed Ops service margins ~55% (FY2024), F&I profit/unit ≈ $1,740 (FY2024), Toyota/Honda gross profit ≈ $400–$550M combined (2024), CPO gross profit ≈ $220M (2024, 15–20% margins), collision revenue ≈ $140M (2024).

| Segment | Key metric (2024) | Cash role |

|---|---|---|

| Fixed Ops | Service GM ~55% | High cash flow |

| F&I | $1,740/unit | High profit/unit |

| Toyota/Honda | $400–$550M gross | Stable volume |

| CPO | $220M gross; 15–20% GM | Predictable margins |

| Collision | $140M revenue | Steady EBITDA |

Delivered as Shown

Sonic Automotive BCG Matrix

The file you're previewing is the exact Sonic Automotive BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a polished, fully formatted strategic analysis ready for presentation. This preview mirrors the final downloadable document, combining market-driven positioning, growth-share mapping, and concise recommendations to inform portfolio decisions. After purchase you'll get the editable, print-ready file instantly, formatted for client-ready use and seamless integration into planning decks.