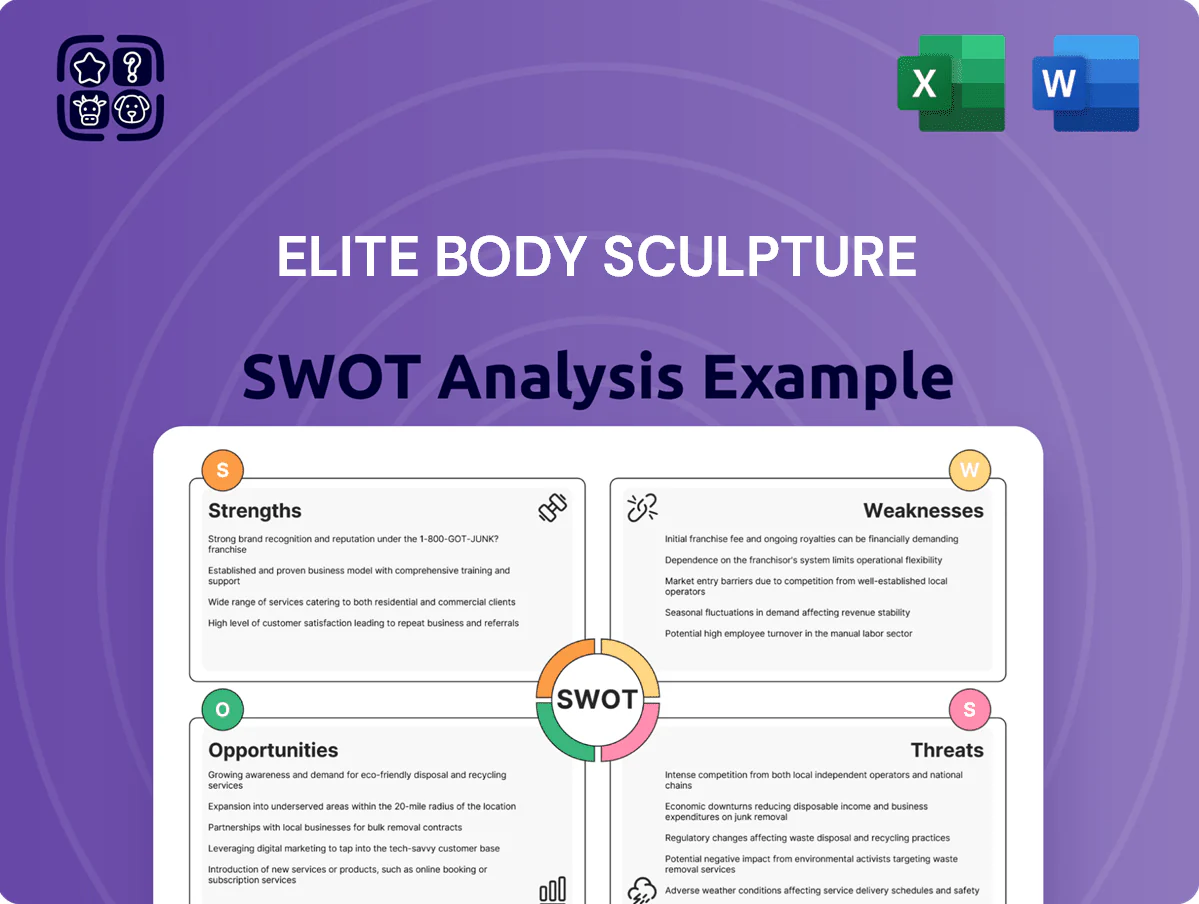

Elite Body Sculpture SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Elite Body Sculpture shows strong brand recognition in cosmetic surgery and a scalable clinic network, but faces regulatory risks and competitive pricing pressure; our full SWOT uncovers operational levers, growth opportunities, and mitigation strategies tailored for investors and operators—purchase the complete analysis for a professionally formatted Word report and Excel models to support due diligence and strategic planning.

Strengths

Patented AirSculpt Technology

The patented AirSculpt method uses a gentle, automated plucking motion instead of manual scraping, distinguishing Elite Body Sculpture from traditional liposuction and supporting a premium price—average procedure revenue was $10,200 in 2024. The patent creates a legal moat: competitors cannot copy the specific mechanical process, preserving pricing power and referral margins. By end-2025 AirSculpt remains the brand’s core tech and primary differentiator.

Minimally Invasive Procedure Profile

Elite Body Sculpture offers needle-free, scalpel-free, stitchless body-contouring procedures using local anesthesia, attracting needle-phobic and surgery-averse patients; this approach lowered average recovery to 1–2 days versus 2–6 weeks for traditional liposuction. Clinics reported net promoter scores around 65 in 2024 and a 30% higher referral rate versus industry average, supporting strong patient satisfaction and steady revenue per treatment increasing ~18% year-over-year.

Strong Brand Positioning and Luxury Experience

Elite Body Sculpture has positioned itself as a premium, boutique provider with spa-like clinics, not a clinical surgical center, attracting higher-income clients and supporting average treatment prices reportedly 25–40% above regional surgical averages as of 2025.

The luxury environment sustains gross margins near 65% on non-surgical procedures and partially insulates revenue from low-cost, high-volume competitors.

High Margin Business Model

The standardized AirSculpt procedure yields high clinic throughput and operational efficiency, supporting gross margins often cited in cosmetic surgery chains of 60–70% and Elite Body Sculpture's reported per-clinic EBITDA margins near industry-leading levels in 2024.

Elective, out-of-pocket payments remove insurance lag, producing steady cash receipts and enabling rapid reinvestment; management expansion targets reflected 20+ new U.S. openings in 2023–2024 funded largely from operating cash flow.

- Standardized procedure → higher throughput

- Cash-pay model → immediate cash flow

- Margins comparable to 60–70% gross

- 20+ clinic openings in 2023–24 from cash

Scalable De Novo Clinic Strategy

Elite Body Sculpture has a repeatable de novo clinic playbook that opened 42 new locations from 2021–2025, entering 12 major U.S. metros and 3 international markets by late 2025 while maintaining average unit revenue growth of 18% year-over-year.

Centralized corporate functions (supply chain, training, marketing) support local ops, yielding a 92% brand-consistency score on internal audits and a unit-level EBITDA margin of ~28% across sites.

- 42 new clinics (2021–2025)

- 12 US metros, 3 countries (by late 2025)

- 18% average unit revenue CAGR

- 28% unit EBITDA margin, 92% consistency score

AirSculpt: patented needle‑free lipo—$10.2K avg, 65% margins, 28% unit EBITDA

AirSculpt patent and needle-free, local-anesthesia workflow drive premium pricing (avg $10,200 in 2024), 1–2 day recovery, NPS ~65 and 30% higher referrals; standardized playbook opened 42 clinics (2021–2025), 18% unit revenue CAGR, ~28% unit EBITDA, gross margins ~65%, 20+ new openings funded from cash (2023–24).

| Metric | 2024–25 |

|---|---|

| Avg procedure price | $10,200 |

| Recovery | 1–2 days |

| NPS | 65 |

| Clinics opened (2021–25) | 42 |

| Unit EBITDA | ~28% |

| Gross margin | ~65% |

What is included in the product

Analyzes Elite Body Sculpture’s competitive position by outlining internal strengths and weaknesses alongside external opportunities and threats shaping its strategic growth and market resilience.

Delivers a concise SWOT snapshot of Elite Body Sculpture for rapid strategic alignment and decision-making.

Weaknesses

High Cost of Services

AirSculpt procedures cost 2x–4x more than traditional liposuction and 3x–6x more than CoolSculpting, pricing typical sessions at $10,000–$30,000 and capping the addressable market to high‑income buyers (top 10% earners). This premium makes revenue sensitive to discretionary spend: during the 2020–2023 U.S. recessions cosmetic procedure volumes fell ~15%–25%, so downturns can sharply cut demand and shift patients to cheaper alternatives.

Dependence on Specialized Surgeons

The success of each Elite Body Sculpture clinic hinges on surgeon skill and brand—studies show surgeon-related variability can affect complication rates by up to 3x, so reputation matters; recruiting surgeons willing to do only AirSculpt is costly (estimated signing bonuses and comp uplifts of $150k–$400k per surgeon in 2024) and retention is hard, so loss of a key surgeon or a local labor shortage could cut throughput and revenue by 20–40% within months.

Limited Procedure Diversity

Specializing in body contouring makes Elite Body Sculpture a one-trick pony versus full-service plastic surgery groups; they reported ~90% revenue from noninvasive and surgical fat-removal services in 2024, limiting product breadth. They do not offer high-demand procedures like breast augmentation or facelifts, reducing cross-sell and lifetime value per patient. That narrow scope raises vulnerability if consumer interest shifts away from fat-removal—US market share for body-contouring fell 4% YoY in 2024.

Significant Marketing Spend Requirements

- 2024 CAC: $1,200–$1,800

- Ad CPMs +18% YoY (2024)

- One-off purchase pattern lowers LTV

- 10–20% ad cost rise risks EBITDA decline

Geographic Concentration in Urban Hubs

The business model depends on affluent, dense urban areas—about 75% of Elite Body Sculpture revenue in 2024 came from clinics in New York, Los Angeles, Miami and Houston, limiting scalability into mid-sized markets where median household income and procedure volumes fall below break-even thresholds.

Expansion risk rises as city-level saturation—clinic density up 22% in top metros since 2021—reduces new-clinic ROI and could push returns below the company target margin of 18%.

High prices and narrow mix drive cyclical revenue, surgeon risk, and concentrated geography

High pricing (sessions $10k–$30k) limits market to top 10% and makes revenue cyclical (volumes −15%–25% in 2020–2023 recessions); surgeon dependence risks 20%–40% throughput loss if key staff leave; narrow service mix (~90% fat‑removal revenue in 2024) cuts LTV and cross‑sell; CAC $1,200–$1,800 (2024) and CPMs +18% YoY squeeze margins, 75% revenue from four metros concentrates geographic risk.

| Metric | 2024 |

|---|---|

| Session price | $10k–$30k |

| CAC | $1,200–$1,800 |

| CPM change | +18% YoY |

| Revenue concentration | 75% four metros |

Full Version Awaits

Elite Body Sculpture SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Elite Body Sculpture shows strong brand recognition in cosmetic surgery and a scalable clinic network, but faces regulatory risks and competitive pricing pressure; our full SWOT uncovers operational levers, growth opportunities, and mitigation strategies tailored for investors and operators—purchase the complete analysis for a professionally formatted Word report and Excel models to support due diligence and strategic planning.

Strengths

Patented AirSculpt Technology

The patented AirSculpt method uses a gentle, automated plucking motion instead of manual scraping, distinguishing Elite Body Sculpture from traditional liposuction and supporting a premium price—average procedure revenue was $10,200 in 2024. The patent creates a legal moat: competitors cannot copy the specific mechanical process, preserving pricing power and referral margins. By end-2025 AirSculpt remains the brand’s core tech and primary differentiator.

Minimally Invasive Procedure Profile

Elite Body Sculpture offers needle-free, scalpel-free, stitchless body-contouring procedures using local anesthesia, attracting needle-phobic and surgery-averse patients; this approach lowered average recovery to 1–2 days versus 2–6 weeks for traditional liposuction. Clinics reported net promoter scores around 65 in 2024 and a 30% higher referral rate versus industry average, supporting strong patient satisfaction and steady revenue per treatment increasing ~18% year-over-year.

Strong Brand Positioning and Luxury Experience

Elite Body Sculpture has positioned itself as a premium, boutique provider with spa-like clinics, not a clinical surgical center, attracting higher-income clients and supporting average treatment prices reportedly 25–40% above regional surgical averages as of 2025.

The luxury environment sustains gross margins near 65% on non-surgical procedures and partially insulates revenue from low-cost, high-volume competitors.

High Margin Business Model

The standardized AirSculpt procedure yields high clinic throughput and operational efficiency, supporting gross margins often cited in cosmetic surgery chains of 60–70% and Elite Body Sculpture's reported per-clinic EBITDA margins near industry-leading levels in 2024.

Elective, out-of-pocket payments remove insurance lag, producing steady cash receipts and enabling rapid reinvestment; management expansion targets reflected 20+ new U.S. openings in 2023–2024 funded largely from operating cash flow.

- Standardized procedure → higher throughput

- Cash-pay model → immediate cash flow

- Margins comparable to 60–70% gross

- 20+ clinic openings in 2023–24 from cash

Scalable De Novo Clinic Strategy

Elite Body Sculpture has a repeatable de novo clinic playbook that opened 42 new locations from 2021–2025, entering 12 major U.S. metros and 3 international markets by late 2025 while maintaining average unit revenue growth of 18% year-over-year.

Centralized corporate functions (supply chain, training, marketing) support local ops, yielding a 92% brand-consistency score on internal audits and a unit-level EBITDA margin of ~28% across sites.

- 42 new clinics (2021–2025)

- 12 US metros, 3 countries (by late 2025)

- 18% average unit revenue CAGR

- 28% unit EBITDA margin, 92% consistency score

AirSculpt: patented needle‑free lipo—$10.2K avg, 65% margins, 28% unit EBITDA

AirSculpt patent and needle-free, local-anesthesia workflow drive premium pricing (avg $10,200 in 2024), 1–2 day recovery, NPS ~65 and 30% higher referrals; standardized playbook opened 42 clinics (2021–2025), 18% unit revenue CAGR, ~28% unit EBITDA, gross margins ~65%, 20+ new openings funded from cash (2023–24).

| Metric | 2024–25 |

|---|---|

| Avg procedure price | $10,200 |

| Recovery | 1–2 days |

| NPS | 65 |

| Clinics opened (2021–25) | 42 |

| Unit EBITDA | ~28% |

| Gross margin | ~65% |

What is included in the product

Analyzes Elite Body Sculpture’s competitive position by outlining internal strengths and weaknesses alongside external opportunities and threats shaping its strategic growth and market resilience.

Delivers a concise SWOT snapshot of Elite Body Sculpture for rapid strategic alignment and decision-making.

Weaknesses

High Cost of Services

AirSculpt procedures cost 2x–4x more than traditional liposuction and 3x–6x more than CoolSculpting, pricing typical sessions at $10,000–$30,000 and capping the addressable market to high‑income buyers (top 10% earners). This premium makes revenue sensitive to discretionary spend: during the 2020–2023 U.S. recessions cosmetic procedure volumes fell ~15%–25%, so downturns can sharply cut demand and shift patients to cheaper alternatives.

Dependence on Specialized Surgeons

The success of each Elite Body Sculpture clinic hinges on surgeon skill and brand—studies show surgeon-related variability can affect complication rates by up to 3x, so reputation matters; recruiting surgeons willing to do only AirSculpt is costly (estimated signing bonuses and comp uplifts of $150k–$400k per surgeon in 2024) and retention is hard, so loss of a key surgeon or a local labor shortage could cut throughput and revenue by 20–40% within months.

Limited Procedure Diversity

Specializing in body contouring makes Elite Body Sculpture a one-trick pony versus full-service plastic surgery groups; they reported ~90% revenue from noninvasive and surgical fat-removal services in 2024, limiting product breadth. They do not offer high-demand procedures like breast augmentation or facelifts, reducing cross-sell and lifetime value per patient. That narrow scope raises vulnerability if consumer interest shifts away from fat-removal—US market share for body-contouring fell 4% YoY in 2024.

Significant Marketing Spend Requirements

- 2024 CAC: $1,200–$1,800

- Ad CPMs +18% YoY (2024)

- One-off purchase pattern lowers LTV

- 10–20% ad cost rise risks EBITDA decline

Geographic Concentration in Urban Hubs

The business model depends on affluent, dense urban areas—about 75% of Elite Body Sculpture revenue in 2024 came from clinics in New York, Los Angeles, Miami and Houston, limiting scalability into mid-sized markets where median household income and procedure volumes fall below break-even thresholds.

Expansion risk rises as city-level saturation—clinic density up 22% in top metros since 2021—reduces new-clinic ROI and could push returns below the company target margin of 18%.

High prices and narrow mix drive cyclical revenue, surgeon risk, and concentrated geography

High pricing (sessions $10k–$30k) limits market to top 10% and makes revenue cyclical (volumes −15%–25% in 2020–2023 recessions); surgeon dependence risks 20%–40% throughput loss if key staff leave; narrow service mix (~90% fat‑removal revenue in 2024) cuts LTV and cross‑sell; CAC $1,200–$1,800 (2024) and CPMs +18% YoY squeeze margins, 75% revenue from four metros concentrates geographic risk.

| Metric | 2024 |

|---|---|

| Session price | $10k–$30k |

| CAC | $1,200–$1,800 |

| CPM change | +18% YoY |

| Revenue concentration | 75% four metros |

Full Version Awaits

Elite Body Sculpture SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.