Sony SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Sony’s diversified portfolio—from PlayStation leadership to imaging sensors and entertainment content—drives resilience but faces fierce competition, supply-chain risks, and rapid tech shifts; our full SWOT unpacks these dynamics with financial context and strategic implications. Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel matrix to inform investment decisions, pitches, and strategic planning.

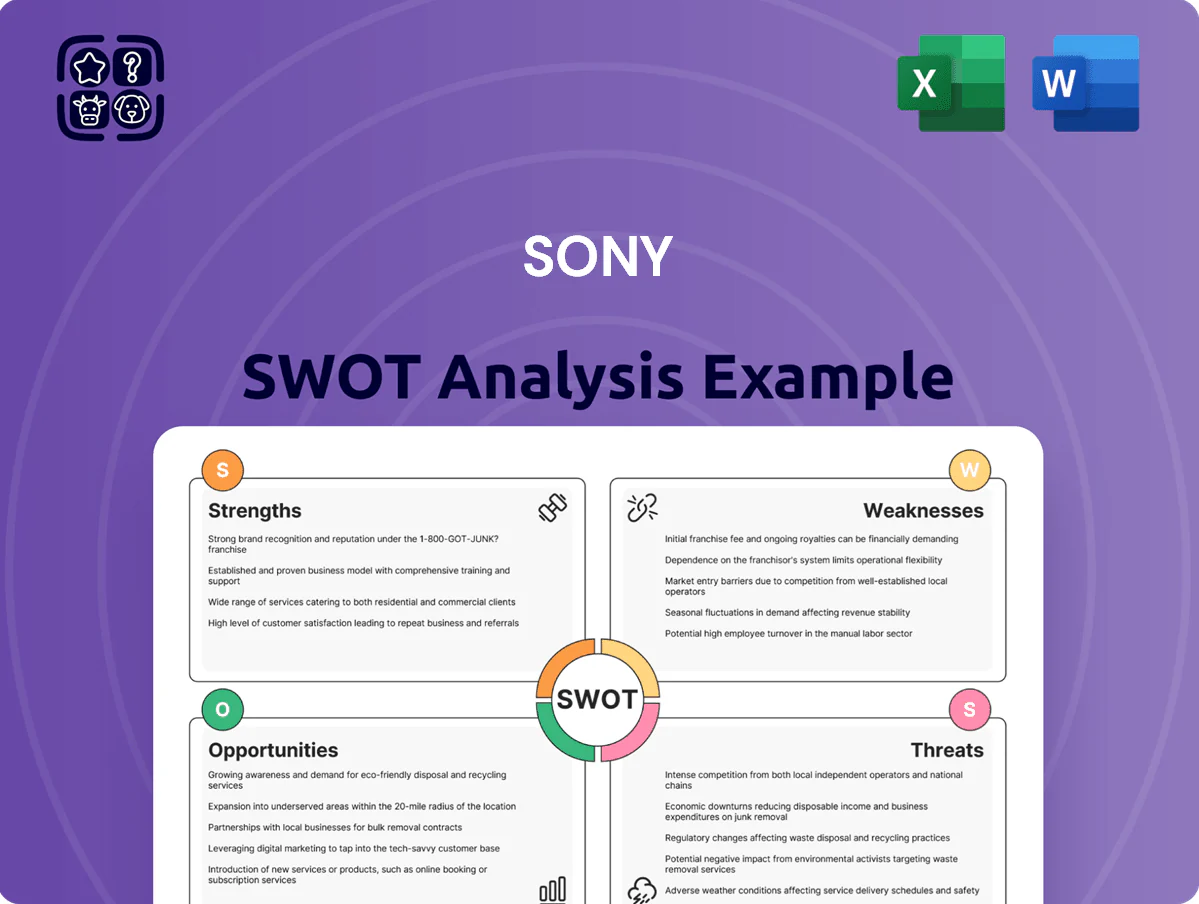

Strengths

Dominant Gaming Ecosystem and Hardware Base

By late 2025 Sony had >140 million PS5-ecosystem accounts and an installed console base exceeding 60 million, keeping engagement high through the generation’s mid-to-late cycle.

PlayStation Plus reached ~60 million subscribers in 2025, driving recurring, high-margin digital revenue—services and software gross margins above 50% in FY2024.

Strong first-party exclusives (Horizon, God of War) sustain playtime and lock‑in, creating material switching costs and steady service fees.

Global Leadership in CMOS Image Sensors

Sony remains the undisputed leader in global CMOS image sensors, holding about 45% market share by revenue in 2024 and roughly 50% of high-end smartphone sensors, supplying Apple, Samsung, and other tier-1 OEMs.

Its stacked CMOS sensor technology (IMX series) creates a strong moat—Sony reported ¥1.1 trillion (~$8.2B) in image sensor revenue FY2024, driven by premium stacked-sensor sales hard for rivals to match quickly.

As mobile photography and ADAS/autonomous driving grow, Sony benefits as a primary component supplier; image-sensor unit volumes rose ~12% YoY in 2024, supporting higher ASPs and margin resilience.

Extensive Intellectual Property and Content Library

Sony holds a world-class IP portfolio across Sony Music Entertainment and Sony Pictures, with recorded-music revenue at $11.2B and Pictures operating revenue $10.1B in FY2024, underpinning global licensing and physical sales.

By late 2025, cross-media hits—notably successful film adaptations of major PlayStation franchises—boosted group synergy, contributing an estimated $1.4B incremental revenue from box office and licensing in 2025.

This diversified library supports streaming, licensing, and merch channels worldwide, with content licensing revenue growing ~8% CAGR 2020–2025, reducing reliance on any single market.

Synergistic Conglomerate Business Model

Sony’s One Sony strategy tightly links hardware and content—gaming, music, film—driving higher ecosystem value; PlayStation content helped push FY2024 operating income to about JPY 1.3 trillion (Sony Group, FY2024).

Vertical integration lets Xperia and BRAVIA tune hardware for Sony’s streaming and gaming services, improving retention and ARPU; PlayStation Network had ~120 million monthly active users in 2024.

Cross-unit collaboration cuts R&D and marketing costs via shared tech (image sensors, AI), aiding margin resilience—Sony’s semiconductor (image sensor) sales grew ~15% in 2024, supporting device competitiveness.

- One Sony aligns hardware + content, boosting ecosystem ARPU

- Xperia/BRAVIA optimized for Sony content increases retention

- Shared R&D (image sensors, AI) reduced unit costs

- PlayStation Network ~120M MAU; FY2024 operating income ≈ JPY 1.3T

Strong Brand Equity and Premium Positioning

Sony’s brand is tied to quality, innovation, and premium design across consumer and professional markets, supporting stronger pricing power and margins versus many peers.

In FY2024 (ended Mar 31, 2024) Sony reported operating income of ¥1.21 trillion, reflecting premium segment strength, while PlayStation, Alpha cameras, and premium audio drove durable loyalty among gamers, audiophiles, and photographers.

- High pricing power — premium SKUs outprice rivals by 10–30%

- FY2024 operating income ¥1.21T

- Strong loyalty: PlayStation ecosystem, Alpha camera users, high-end audio fans

Sony: Gaming, Sensors & Content Powerhouse—¥1.21T Op Income, 60M+ PS5/PS Plus

Sony’s strengths: dominant PlayStation ecosystem (60M+ PS Plus, >60M PS5 base, ~120M PSN MAU) driving recurring high‑margin software/services; market‑leading CMOS image sensors (~45% revenue share, ¥1.1T/$8.2B FY2024); diversified content IP (Music $11.2B, Pictures $10.1B FY2024) enabling cross‑media synergies and premium pricing (FY2024 operating income ¥1.21T).

| Metric | Value |

|---|---|

| PS Plus subs (2025) | ~60M |

| PS5 installed base | >60M |

| Image sensor rev (FY2024) | ¥1.1T |

| Operating income (FY2024) | ¥1.21T |

What is included in the product

Provides a clear SWOT framework for analyzing Sony’s business strategy, highlighting its technological leadership and diversified entertainment ecosystem while identifying operational challenges, market opportunities in gaming, AI and streaming, and external threats from intense competition and rapid industry shifts.

Delivers a concise Sony SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Heavy Revenue Concentration in Gaming

Despite diversified consumer electronics and entertainment units, Sony still depends heavily on Game & Network Services, which generated ¥1.3 trillion operating income in FY2024 (ended March 31, 2024), roughly 45% of group operating profit; a hardware slump or delayed first-party titles can cut consolidated results sharply. Console cycles drive volatility—PlayStation shipments fell 12% YoY in H2 2024—making the stock sensitive to gaming’s cyclical demand.

Narrow Profit Margins in Consumer Electronics

The consumer electronics segment, notably TVs and mobile phones, faces fierce price pressure from lower-cost Chinese makers like Hisense and Xiaomi and South Korea’s Samsung; Sony’s Electronics operating margin was about 4.8% in FY2024 while PlayStation and Music posted mid-teens margins, highlighting the gap. Maintaining profitability needs constant R&D—Sony spent ¥685.6 billion on R&D in FY2024—but margins in hardware remain thin versus software/services. This forces ongoing cost cuts and supply-chain optimization while protecting Sony’s premium brand image, squeezing short-term profits.

Complex Conglomerate Organizational Structure

Operating across life insurance, semiconductors, music and film, Sony Group Corp. manages 8 reportable segments, which adds layers of coordination and raised SG&A: consolidated operating income was ¥2.13 trillion in FY2024, but segmental variance is wide (Sony Financial Group profit margins lag Electronics).

This sprawling structure can slow decisions versus focused rivals; Sony Semiconductor Solutions needed three board approvals in 2024 for a $4.5B fab expansion, delaying start by 9 months.

Aligning capital is costly: Sony allocated ¥1.2 trillion to content and imaging R&D in 2024, creating internal friction over returns versus higher-margin PlayStation and financial services bets.

Lagging Market Share in Mobile Communications

Sony makes high-quality Xperia phones, but its global mobile market share was about 0.6% in 2024 versus Apple 21% and Samsung 20% (IDC, 2024), keeping Sony marginal in volume.

The Xperia line targets prosumers and niche users, so it fails to win mass-market buyers and wider carrier distribution.

Low volumes prevent economies of scale, raising unit costs and limiting spending on price cuts or global marketing.

- 2024 share ~0.6% (IDC)

- Apple 21%, Samsung 20% (2024)

- Niche prosumer positioning

- Higher unit cost, limited marketing

High Research and Development Expenditures

Sony’s push to stay ahead in semiconductors and PlayStation forces rising R&D: Sony spent ¥579.7 billion (about $4.2bn) on R&D in FY2024, pressuring margins if launches flop.

The image sensor business is capital-heavy; continuous reinvestment is needed as competitors and shifting standards can make prior investments obsolete.

- FY2024 R&D: ¥579.7 billion (~$4.2bn)

- High fixed-cost risk if product adoption lags

- Sensor unit needs constant capex to match standards

Sony’s PlayStation Reliance and Slim Electronics Margins Heighten Profit Volatility

Sony’s heavy reliance on Game & Network Services (¥1.3T operating income, ~45% of group OP in FY2024) and cyclical PlayStation sales (shipments -12% H2 2024) raises volatility; thin Electronics margins (≈4.8% FY2024) face price pressure from Xiaomi/Hisense and Samsung; complex 8-segment structure raises SG&A and slows decisions; Xperia mobile share ~0.6% (2024, IDC), limiting scale and driving higher unit costs.

| Metric | Value (FY2024) |

|---|---|

| Game OP | ¥1.3T (~45% group) |

| Electronics margin | 4.8% |

| R&D | ¥685.6B |

| Xperia share | 0.6% (IDC) |

Full Version Awaits

Sony SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled straight from the final, editable file. You’re viewing a live preview of the real analysis; buy now to unlock the complete, detailed version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Sony’s diversified portfolio—from PlayStation leadership to imaging sensors and entertainment content—drives resilience but faces fierce competition, supply-chain risks, and rapid tech shifts; our full SWOT unpacks these dynamics with financial context and strategic implications. Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel matrix to inform investment decisions, pitches, and strategic planning.

Strengths

Dominant Gaming Ecosystem and Hardware Base

By late 2025 Sony had >140 million PS5-ecosystem accounts and an installed console base exceeding 60 million, keeping engagement high through the generation’s mid-to-late cycle.

PlayStation Plus reached ~60 million subscribers in 2025, driving recurring, high-margin digital revenue—services and software gross margins above 50% in FY2024.

Strong first-party exclusives (Horizon, God of War) sustain playtime and lock‑in, creating material switching costs and steady service fees.

Global Leadership in CMOS Image Sensors

Sony remains the undisputed leader in global CMOS image sensors, holding about 45% market share by revenue in 2024 and roughly 50% of high-end smartphone sensors, supplying Apple, Samsung, and other tier-1 OEMs.

Its stacked CMOS sensor technology (IMX series) creates a strong moat—Sony reported ¥1.1 trillion (~$8.2B) in image sensor revenue FY2024, driven by premium stacked-sensor sales hard for rivals to match quickly.

As mobile photography and ADAS/autonomous driving grow, Sony benefits as a primary component supplier; image-sensor unit volumes rose ~12% YoY in 2024, supporting higher ASPs and margin resilience.

Extensive Intellectual Property and Content Library

Sony holds a world-class IP portfolio across Sony Music Entertainment and Sony Pictures, with recorded-music revenue at $11.2B and Pictures operating revenue $10.1B in FY2024, underpinning global licensing and physical sales.

By late 2025, cross-media hits—notably successful film adaptations of major PlayStation franchises—boosted group synergy, contributing an estimated $1.4B incremental revenue from box office and licensing in 2025.

This diversified library supports streaming, licensing, and merch channels worldwide, with content licensing revenue growing ~8% CAGR 2020–2025, reducing reliance on any single market.

Synergistic Conglomerate Business Model

Sony’s One Sony strategy tightly links hardware and content—gaming, music, film—driving higher ecosystem value; PlayStation content helped push FY2024 operating income to about JPY 1.3 trillion (Sony Group, FY2024).

Vertical integration lets Xperia and BRAVIA tune hardware for Sony’s streaming and gaming services, improving retention and ARPU; PlayStation Network had ~120 million monthly active users in 2024.

Cross-unit collaboration cuts R&D and marketing costs via shared tech (image sensors, AI), aiding margin resilience—Sony’s semiconductor (image sensor) sales grew ~15% in 2024, supporting device competitiveness.

- One Sony aligns hardware + content, boosting ecosystem ARPU

- Xperia/BRAVIA optimized for Sony content increases retention

- Shared R&D (image sensors, AI) reduced unit costs

- PlayStation Network ~120M MAU; FY2024 operating income ≈ JPY 1.3T

Strong Brand Equity and Premium Positioning

Sony’s brand is tied to quality, innovation, and premium design across consumer and professional markets, supporting stronger pricing power and margins versus many peers.

In FY2024 (ended Mar 31, 2024) Sony reported operating income of ¥1.21 trillion, reflecting premium segment strength, while PlayStation, Alpha cameras, and premium audio drove durable loyalty among gamers, audiophiles, and photographers.

- High pricing power — premium SKUs outprice rivals by 10–30%

- FY2024 operating income ¥1.21T

- Strong loyalty: PlayStation ecosystem, Alpha camera users, high-end audio fans

Sony: Gaming, Sensors & Content Powerhouse—¥1.21T Op Income, 60M+ PS5/PS Plus

Sony’s strengths: dominant PlayStation ecosystem (60M+ PS Plus, >60M PS5 base, ~120M PSN MAU) driving recurring high‑margin software/services; market‑leading CMOS image sensors (~45% revenue share, ¥1.1T/$8.2B FY2024); diversified content IP (Music $11.2B, Pictures $10.1B FY2024) enabling cross‑media synergies and premium pricing (FY2024 operating income ¥1.21T).

| Metric | Value |

|---|---|

| PS Plus subs (2025) | ~60M |

| PS5 installed base | >60M |

| Image sensor rev (FY2024) | ¥1.1T |

| Operating income (FY2024) | ¥1.21T |

What is included in the product

Provides a clear SWOT framework for analyzing Sony’s business strategy, highlighting its technological leadership and diversified entertainment ecosystem while identifying operational challenges, market opportunities in gaming, AI and streaming, and external threats from intense competition and rapid industry shifts.

Delivers a concise Sony SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Heavy Revenue Concentration in Gaming

Despite diversified consumer electronics and entertainment units, Sony still depends heavily on Game & Network Services, which generated ¥1.3 trillion operating income in FY2024 (ended March 31, 2024), roughly 45% of group operating profit; a hardware slump or delayed first-party titles can cut consolidated results sharply. Console cycles drive volatility—PlayStation shipments fell 12% YoY in H2 2024—making the stock sensitive to gaming’s cyclical demand.

Narrow Profit Margins in Consumer Electronics

The consumer electronics segment, notably TVs and mobile phones, faces fierce price pressure from lower-cost Chinese makers like Hisense and Xiaomi and South Korea’s Samsung; Sony’s Electronics operating margin was about 4.8% in FY2024 while PlayStation and Music posted mid-teens margins, highlighting the gap. Maintaining profitability needs constant R&D—Sony spent ¥685.6 billion on R&D in FY2024—but margins in hardware remain thin versus software/services. This forces ongoing cost cuts and supply-chain optimization while protecting Sony’s premium brand image, squeezing short-term profits.

Complex Conglomerate Organizational Structure

Operating across life insurance, semiconductors, music and film, Sony Group Corp. manages 8 reportable segments, which adds layers of coordination and raised SG&A: consolidated operating income was ¥2.13 trillion in FY2024, but segmental variance is wide (Sony Financial Group profit margins lag Electronics).

This sprawling structure can slow decisions versus focused rivals; Sony Semiconductor Solutions needed three board approvals in 2024 for a $4.5B fab expansion, delaying start by 9 months.

Aligning capital is costly: Sony allocated ¥1.2 trillion to content and imaging R&D in 2024, creating internal friction over returns versus higher-margin PlayStation and financial services bets.

Lagging Market Share in Mobile Communications

Sony makes high-quality Xperia phones, but its global mobile market share was about 0.6% in 2024 versus Apple 21% and Samsung 20% (IDC, 2024), keeping Sony marginal in volume.

The Xperia line targets prosumers and niche users, so it fails to win mass-market buyers and wider carrier distribution.

Low volumes prevent economies of scale, raising unit costs and limiting spending on price cuts or global marketing.

- 2024 share ~0.6% (IDC)

- Apple 21%, Samsung 20% (2024)

- Niche prosumer positioning

- Higher unit cost, limited marketing

High Research and Development Expenditures

Sony’s push to stay ahead in semiconductors and PlayStation forces rising R&D: Sony spent ¥579.7 billion (about $4.2bn) on R&D in FY2024, pressuring margins if launches flop.

The image sensor business is capital-heavy; continuous reinvestment is needed as competitors and shifting standards can make prior investments obsolete.

- FY2024 R&D: ¥579.7 billion (~$4.2bn)

- High fixed-cost risk if product adoption lags

- Sensor unit needs constant capex to match standards

Sony’s PlayStation Reliance and Slim Electronics Margins Heighten Profit Volatility

Sony’s heavy reliance on Game & Network Services (¥1.3T operating income, ~45% of group OP in FY2024) and cyclical PlayStation sales (shipments -12% H2 2024) raises volatility; thin Electronics margins (≈4.8% FY2024) face price pressure from Xiaomi/Hisense and Samsung; complex 8-segment structure raises SG&A and slows decisions; Xperia mobile share ~0.6% (2024, IDC), limiting scale and driving higher unit costs.

| Metric | Value (FY2024) |

|---|---|

| Game OP | ¥1.3T (~45% group) |

| Electronics margin | 4.8% |

| R&D | ¥685.6B |

| Xperia share | 0.6% (IDC) |

Full Version Awaits

Sony SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled straight from the final, editable file. You’re viewing a live preview of the real analysis; buy now to unlock the complete, detailed version.