Sony Pictures Entertainment Inc. PESTLE Analysis

Your Competitive Advantage Starts with This Report

Sony Pictures Entertainment faces regulatory scrutiny, shifting consumer habits, and rapid tech-driven disruption—from streaming competition to AI in content creation—impacting revenue models and global distribution strategies; our PESTLE pinpoints these forces and strategic responses. Buy the full PESTLE analysis to access actionable insights, scenarios, and editable tools that inform investment decisions and competitive planning.

Political factors

Geopolitical tensions and international distribution

Sony Pictures operates across 40+ markets where shifting alliances and trade curbs can delay releases and distribution revenue; in 2024 China accounted for roughly 8–10% of global box office receipts, making censorship risk material to earnings.

Regulatory hurdles in emerging markets—Africa and Southeast Asia growing at ~5–7% annual box office—force tailored release strategies and local partnerships to protect margins.

The studio must weigh creative integrity against political sensitivities to preserve a $9–11B global content pipeline and maintain profitability.

Governmental tax incentives and subsidies

Government tax credits and subsidies drive Sony Pictures Entertainment location choices; U.S. state incentives averaged $3.5 billion annually in 2023, with California offering rebates up to 25% and Georgia providing a 30% credit that attracted major productions.

SPE strategically selects sites to trim budgets—a 10% incentive differential can shift shooting decisions—making the studio sensitive to election-driven policy changes and fiscal tightening.

Reductions or expirations of these programs can raise production costs materially; for example, losing a 20% credit on a $100m film increases spend by $20m, squeezing margins on theatrical and streaming releases.

Trade policies and intellectual property protection

Sony Pictures, exporting films and streaming content to 170+ countries, depends on trade agreements that enforce IP; global box office was $28.6bn in 2023, so IP breaches materially risk revenue. Political instability or protectionism raises piracy—IFPI estimates digital piracy costs rightsholders $2.7bn–$4.2bn annually in lost sales in key markets. Sony actively monitors trade talks (USMCA, CPTPP, EU trade deals) to safeguard digital and physical assets under international law.

Media ownership and antitrust regulations

Political scrutiny of media consolidation constrains Sony Pictures Entertainment’s M&A activity; regulators flagged that global media deals declined 22% in 2024 vs 2023, increasing hurdles for large-scale acquisitions.

Antitrust reviews assess SPE’s market share amid the shift to integrated streaming/production—Sony Pictures’ 2024 global box office share was about 7%, while Sony’s streaming licensing revenue rose 18% YoY, attracting regulator attention.

Shifts in US and EU administrations change enforcement intensity; from 2021–2025 major antitrust actions doubled, altering Sony’s long-term growth planning and deal timing.

- Regulatory scrutiny up with 22% drop in media deals (2024 v 2023)

- SPE ~7% global box office share; streaming licensing revenue +18% YoY (2024)

- Major antitrust actions doubled 2021–2025, affecting deal timing

Labor relations and union negotiations

The political climate around labor rights affects Sony Pictures Entertainment through collective bargaining with SAG-AFTRA, WGA and IATSE; 2023–24 strikes cost the US film/TV industry an estimated $6.5–$8.5 billion in lost revenue, directly pressuring SPE’s schedules and cash flows.

Legislative support for labor movements increases likelihood of concessions—higher wages/benefits—which raise production budgets; major studios reported average per-project cost increases of 5–12% during recent negotiations.

Sony must balance political pressures to avoid prolonged shutdowns that disrupt release calendars and box office receipts, protect the 2024–25 content pipeline, and manage contingency reserves and insurance exposure.

- 2023–24 strike impact: $6.5–$8.5B industry loss

- Estimated per-project cost rise: 5–12%

- Key unions: SAG-AFTRA, WGA, IATSE

- Risks: schedule delays, higher budgets, insurance/contingency needs

Sony Pictures faces China censorship, antitrust heat and costly labor strikes

Political risks for Sony Pictures include censorship in China (~8–10% of global box office 2024), trade/IP exposure from $28.6B global box office (2023), rising antitrust scrutiny (media deals -22% 2024 v 2023; antitrust actions doubled 2021–2025), and labor disruptions (2023–24 strikes cost $6.5–$8.5B; per-project costs +5–12%).

| Metric | Value |

|---|---|

| China box office share | 8–10% (2024) |

| Global box office | $28.6B (2023) |

| Media deals change | -22% (2024 v 2023) |

| Strike impact | $6.5–$8.5B (2023–24) |

What is included in the product

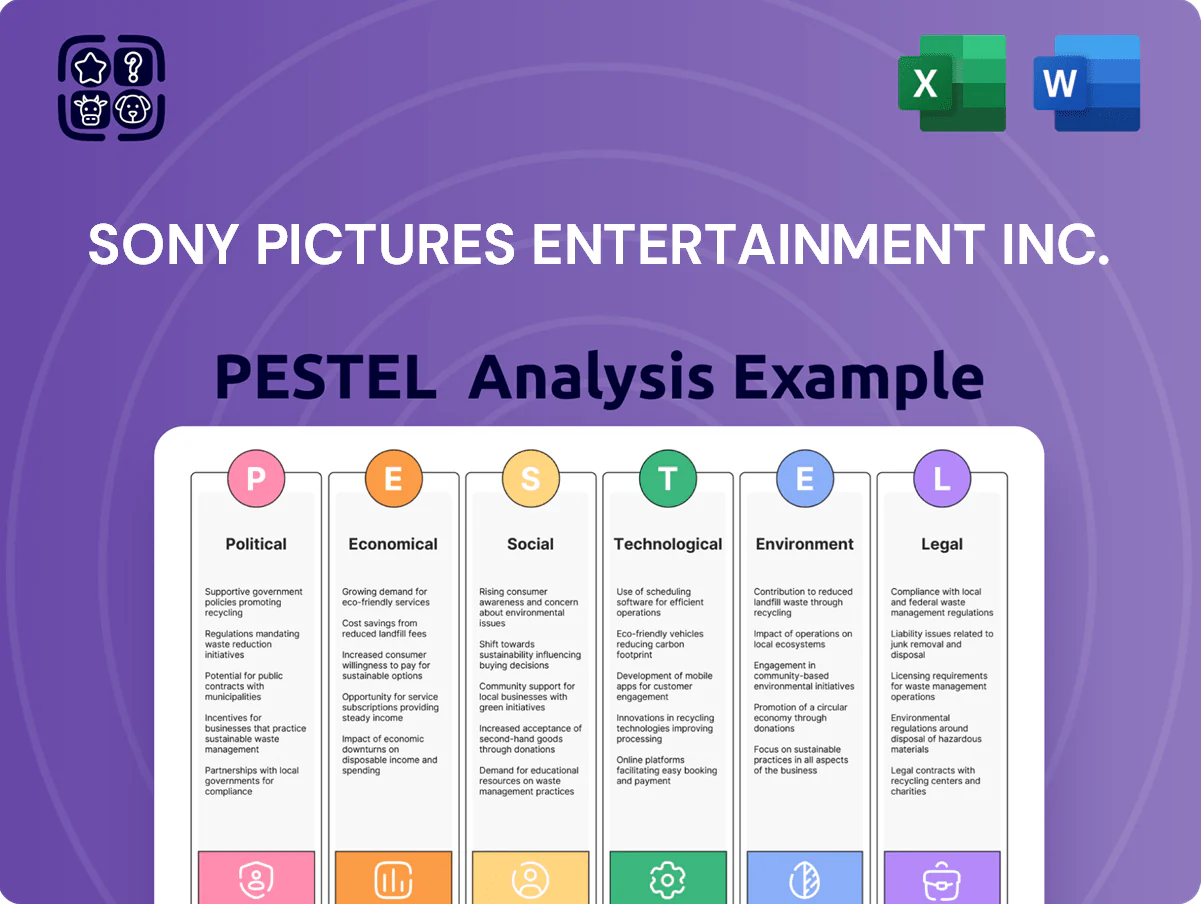

Explores how external macro-environmental factors uniquely affect Sony Pictures Entertainment Inc. across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current industry data and trends to identify threats, opportunities, and actionable insights for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sony Pictures Entertainment that distills regulatory, economic, social, technological, environmental, and legal drivers into an easy-to-share slide or meeting handout, enabling quick alignment, risk discussion, and tailored note-taking for regional or business-line strategies.

Economic factors

Global exchange rate volatility

As a subsidiary of a Japanese conglomerate with massive global sales, Sony Pictures is highly sensitive to fluctuations in the yen; a 10% yen appreciation vs. the dollar in 2024 would cut repatriated dollar revenues by about 9–11%, pressuring consolidated results. Revenue earned abroad can lose value when converted, contributing to Sony Group’s FY2024 foreign exchange loss of ¥94.3bn reported in Q4. Active hedging—forwards, options and natural hedges—remains essential to stabilize cash flows and protect operating margins.

Consumer discretionary spending trends

The demand for theatrical releases and premium streaming is sensitive to global GDP and disposable income; in 2023 US real consumer spending on recreation fell 1.2% year-over-year and global box office revenue dropped to $25.6B in 2023 from $31.4B in 2019, signaling constrained entertainment spend. High inflation (CPI 2023 US avg 3.4%) and recession risks can depress box office and subs, so Sony must adapt pricing, hybrid release windows and lower-price tiers to retain budget-conscious viewers.

Rising production and marketing costs

Rising talent fees, costly VFX and global marketing squeezed SPE margins as average US studio marketing spend reached about $100–150M per tentpole by 2024; top-tier directors/actors commanded multimillion-dollar paydays, pushing break-even thresholds higher. Competition for specialized technicians elevated VFX vendor rates—global VFX market grew to $8.5B in 2023—forcing SPE to use co-financing, slate deals and tax incentives to spread risk and preserve ROIs.

Growth of emerging market middle classes

The expanding middle class in Southeast Asia and India—projected to add ~1.5 billion people to global middle-income cohorts by 2030—boosts demand for theatrical and TV content, enabling Sony Pictures to raise average ticket spend and subscription ARPU in these markets.

Sony is scaling regional production hubs (notably India and Indonesia), diversifying revenue from Western markets that delivered ~60% of global box office in 2023, and targeting higher local content share to capture rising disposable incomes.

- Emerging middle-class growth: +1.5bn by 2030

- Western box office share ~60% in 2023

- Focus: India, Southeast Asia regional hubs

Impact of interest rates on capital investment

High interest rates raise Sony Pictures Entertainment’s borrowing costs for studio expansions or buying IP, increasing weighted average cost of capital and potentially delaying projects; US federal funds rate rose to 5.25–5.50% in 2024, tightening financing conditions.

Sony must manage debt—net debt on Sony Group consolidated was about ¥2.4 trillion (~$16.5B) in FY2024—timing investments around central bank cues to avoid refinancing stress.

Low-rate periods (e.g., 2020–2021) enabled faster content spend and tech upgrades; with current higher rates, capex and M&A may be more conservative.

- Higher rates → higher borrowing cost, project delays

- FY2024 net debt ~¥2.4T (~$16.5B)

- Monetary policy dictates investment timing

- Low rates historically boosted content/tech spending

Currency hits squeeze profits; box office dips as costs surge—Asia middle class offers growth

Currency swings cut repatriated revenues (FY2024 FX loss ¥94.3bn); hedging needed. Global box office fell to $25.6B in 2023; US recreation spending down 1.2% YoY. Talent/VFX costs rose (VFX market $8.5B in 2023; tentpole marketing $100–150M). Rising SE Asia/India middle class (+~1.5bn by 2030) expands regional revenue; FY2024 net debt ~¥2.4T (~$16.5B).

| Metric | Value |

|---|---|

| FY2024 FX loss | ¥94.3bn |

| Global box office 2023 | $25.6B |

| VFX market 2023 | $8.5B |

| Tentpole marketing | $100–150M |

| Middle-class add by 2030 | ~1.5bn |

| Sony Group net debt FY2024 | ¥2.4T (~$16.5B) |

What You See Is What You Get

Sony Pictures Entertainment Inc. PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Sony Pictures Entertainment Inc. PESTLE analysis covers political, economic, social, technological, legal, and environmental factors affecting the company, with concise insights and actionable implications. What you see is the final, professionally structured file available for immediate download after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Sony Pictures Entertainment faces regulatory scrutiny, shifting consumer habits, and rapid tech-driven disruption—from streaming competition to AI in content creation—impacting revenue models and global distribution strategies; our PESTLE pinpoints these forces and strategic responses. Buy the full PESTLE analysis to access actionable insights, scenarios, and editable tools that inform investment decisions and competitive planning.

Political factors

Geopolitical tensions and international distribution

Sony Pictures operates across 40+ markets where shifting alliances and trade curbs can delay releases and distribution revenue; in 2024 China accounted for roughly 8–10% of global box office receipts, making censorship risk material to earnings.

Regulatory hurdles in emerging markets—Africa and Southeast Asia growing at ~5–7% annual box office—force tailored release strategies and local partnerships to protect margins.

The studio must weigh creative integrity against political sensitivities to preserve a $9–11B global content pipeline and maintain profitability.

Governmental tax incentives and subsidies

Government tax credits and subsidies drive Sony Pictures Entertainment location choices; U.S. state incentives averaged $3.5 billion annually in 2023, with California offering rebates up to 25% and Georgia providing a 30% credit that attracted major productions.

SPE strategically selects sites to trim budgets—a 10% incentive differential can shift shooting decisions—making the studio sensitive to election-driven policy changes and fiscal tightening.

Reductions or expirations of these programs can raise production costs materially; for example, losing a 20% credit on a $100m film increases spend by $20m, squeezing margins on theatrical and streaming releases.

Trade policies and intellectual property protection

Sony Pictures, exporting films and streaming content to 170+ countries, depends on trade agreements that enforce IP; global box office was $28.6bn in 2023, so IP breaches materially risk revenue. Political instability or protectionism raises piracy—IFPI estimates digital piracy costs rightsholders $2.7bn–$4.2bn annually in lost sales in key markets. Sony actively monitors trade talks (USMCA, CPTPP, EU trade deals) to safeguard digital and physical assets under international law.

Media ownership and antitrust regulations

Political scrutiny of media consolidation constrains Sony Pictures Entertainment’s M&A activity; regulators flagged that global media deals declined 22% in 2024 vs 2023, increasing hurdles for large-scale acquisitions.

Antitrust reviews assess SPE’s market share amid the shift to integrated streaming/production—Sony Pictures’ 2024 global box office share was about 7%, while Sony’s streaming licensing revenue rose 18% YoY, attracting regulator attention.

Shifts in US and EU administrations change enforcement intensity; from 2021–2025 major antitrust actions doubled, altering Sony’s long-term growth planning and deal timing.

- Regulatory scrutiny up with 22% drop in media deals (2024 v 2023)

- SPE ~7% global box office share; streaming licensing revenue +18% YoY (2024)

- Major antitrust actions doubled 2021–2025, affecting deal timing

Labor relations and union negotiations

The political climate around labor rights affects Sony Pictures Entertainment through collective bargaining with SAG-AFTRA, WGA and IATSE; 2023–24 strikes cost the US film/TV industry an estimated $6.5–$8.5 billion in lost revenue, directly pressuring SPE’s schedules and cash flows.

Legislative support for labor movements increases likelihood of concessions—higher wages/benefits—which raise production budgets; major studios reported average per-project cost increases of 5–12% during recent negotiations.

Sony must balance political pressures to avoid prolonged shutdowns that disrupt release calendars and box office receipts, protect the 2024–25 content pipeline, and manage contingency reserves and insurance exposure.

- 2023–24 strike impact: $6.5–$8.5B industry loss

- Estimated per-project cost rise: 5–12%

- Key unions: SAG-AFTRA, WGA, IATSE

- Risks: schedule delays, higher budgets, insurance/contingency needs

Sony Pictures faces China censorship, antitrust heat and costly labor strikes

Political risks for Sony Pictures include censorship in China (~8–10% of global box office 2024), trade/IP exposure from $28.6B global box office (2023), rising antitrust scrutiny (media deals -22% 2024 v 2023; antitrust actions doubled 2021–2025), and labor disruptions (2023–24 strikes cost $6.5–$8.5B; per-project costs +5–12%).

| Metric | Value |

|---|---|

| China box office share | 8–10% (2024) |

| Global box office | $28.6B (2023) |

| Media deals change | -22% (2024 v 2023) |

| Strike impact | $6.5–$8.5B (2023–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sony Pictures Entertainment Inc. across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current industry data and trends to identify threats, opportunities, and actionable insights for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sony Pictures Entertainment that distills regulatory, economic, social, technological, environmental, and legal drivers into an easy-to-share slide or meeting handout, enabling quick alignment, risk discussion, and tailored note-taking for regional or business-line strategies.

Economic factors

Global exchange rate volatility

As a subsidiary of a Japanese conglomerate with massive global sales, Sony Pictures is highly sensitive to fluctuations in the yen; a 10% yen appreciation vs. the dollar in 2024 would cut repatriated dollar revenues by about 9–11%, pressuring consolidated results. Revenue earned abroad can lose value when converted, contributing to Sony Group’s FY2024 foreign exchange loss of ¥94.3bn reported in Q4. Active hedging—forwards, options and natural hedges—remains essential to stabilize cash flows and protect operating margins.

Consumer discretionary spending trends

The demand for theatrical releases and premium streaming is sensitive to global GDP and disposable income; in 2023 US real consumer spending on recreation fell 1.2% year-over-year and global box office revenue dropped to $25.6B in 2023 from $31.4B in 2019, signaling constrained entertainment spend. High inflation (CPI 2023 US avg 3.4%) and recession risks can depress box office and subs, so Sony must adapt pricing, hybrid release windows and lower-price tiers to retain budget-conscious viewers.

Rising production and marketing costs

Rising talent fees, costly VFX and global marketing squeezed SPE margins as average US studio marketing spend reached about $100–150M per tentpole by 2024; top-tier directors/actors commanded multimillion-dollar paydays, pushing break-even thresholds higher. Competition for specialized technicians elevated VFX vendor rates—global VFX market grew to $8.5B in 2023—forcing SPE to use co-financing, slate deals and tax incentives to spread risk and preserve ROIs.

Growth of emerging market middle classes

The expanding middle class in Southeast Asia and India—projected to add ~1.5 billion people to global middle-income cohorts by 2030—boosts demand for theatrical and TV content, enabling Sony Pictures to raise average ticket spend and subscription ARPU in these markets.

Sony is scaling regional production hubs (notably India and Indonesia), diversifying revenue from Western markets that delivered ~60% of global box office in 2023, and targeting higher local content share to capture rising disposable incomes.

- Emerging middle-class growth: +1.5bn by 2030

- Western box office share ~60% in 2023

- Focus: India, Southeast Asia regional hubs

Impact of interest rates on capital investment

High interest rates raise Sony Pictures Entertainment’s borrowing costs for studio expansions or buying IP, increasing weighted average cost of capital and potentially delaying projects; US federal funds rate rose to 5.25–5.50% in 2024, tightening financing conditions.

Sony must manage debt—net debt on Sony Group consolidated was about ¥2.4 trillion (~$16.5B) in FY2024—timing investments around central bank cues to avoid refinancing stress.

Low-rate periods (e.g., 2020–2021) enabled faster content spend and tech upgrades; with current higher rates, capex and M&A may be more conservative.

- Higher rates → higher borrowing cost, project delays

- FY2024 net debt ~¥2.4T (~$16.5B)

- Monetary policy dictates investment timing

- Low rates historically boosted content/tech spending

Currency hits squeeze profits; box office dips as costs surge—Asia middle class offers growth

Currency swings cut repatriated revenues (FY2024 FX loss ¥94.3bn); hedging needed. Global box office fell to $25.6B in 2023; US recreation spending down 1.2% YoY. Talent/VFX costs rose (VFX market $8.5B in 2023; tentpole marketing $100–150M). Rising SE Asia/India middle class (+~1.5bn by 2030) expands regional revenue; FY2024 net debt ~¥2.4T (~$16.5B).

| Metric | Value |

|---|---|

| FY2024 FX loss | ¥94.3bn |

| Global box office 2023 | $25.6B |

| VFX market 2023 | $8.5B |

| Tentpole marketing | $100–150M |

| Middle-class add by 2030 | ~1.5bn |

| Sony Group net debt FY2024 | ¥2.4T (~$16.5B) |

What You See Is What You Get

Sony Pictures Entertainment Inc. PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Sony Pictures Entertainment Inc. PESTLE analysis covers political, economic, social, technological, legal, and environmental factors affecting the company, with concise insights and actionable implications. What you see is the final, professionally structured file available for immediate download after checkout.