Southern Company Boston Consulting Group Matrix

See the Bigger Picture

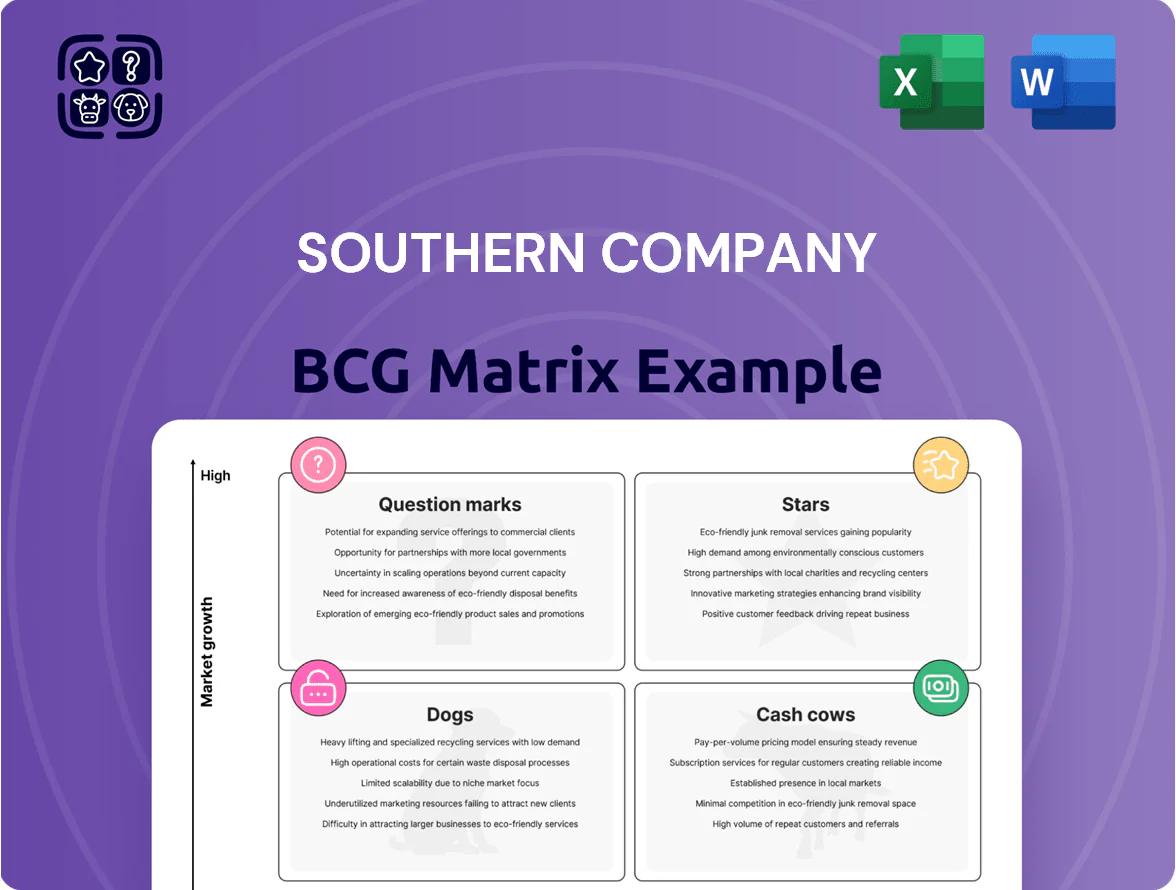

Southern Company sits at an inflection point as shifting energy demand and regulatory pressure reshape its portfolio—our preview highlights which business units lean toward Cash Cows and which may be Question Marks amid decarbonization trends. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Data Center Electricity Sales

As of late 2025, Southern Company reports data center electricity sales up 17% year-over-year, driven by AI demand and large-load customers.

The company has 10 GW of signed contracts for hyperscale and AI facilities, giving it a dominant regional share in a high-growth market.

This segment is capital-intensive; Southern expanded its five-year plan to $81 billion to fund generation and transmission capacity for this watershed demand.

Plant Vogtle Units 3 and 4

With Unit 4 reaching full commercial operation in July 2024, Plant Vogtle Units 3 and 4 became the largest clean-energy generator in the US by 2025, adding ~2,400 MW combined of carbon-free capacity that served ~1.9 million homes.

These reactors supply always-on baseload power ideal for hyperscalers and heavy industry; in 2025 Vogtle’s output cut ~11 million metric tons CO2 annually versus gas generation.

Despite earlier cost overruns (final cost ~25–30 billion USD), Vogtle now drives material revenue for Southern Company, supporting RPS compliance and corporate clean-energy contracts.

Renewable Energy Expansion

Southern Company is scaling renewables: solar capacity is projected at 2,500 MW and wind at 1,800 MW by end-2025, making this a Stars quadrant asset with high market growth and strong share.

Growth is driven by the 10-year Inflation Reduction Act tax incentives and state decarbonization mandates; US utility-scale renewables grew ~15% in 2024, fueling demand.

By integrating these assets with its transmission and distribution network, Southern captures more green-market revenue while keeping reliability metrics (SAIDI/SAIFI) stable.

Fiber Optics and Connectivity

Southern Company leverages 250,000+ utility right-of-way miles to expand dark fiber and telco services, making this unit a high-growth Star in digital infrastructure; revenue from fiber and telecom rose ~22% year-over-year to an estimated $420M in 2025.

That fiber directly serves data center developers—responsible for ~30% of regional electricity load growth—creating tight demand coupling as AI and cloud compute drive bandwidth needs.

With average fiber IRR targets near 12–15% and low incremental capex per mile versus greenfield builds, Southern is capturing specialized, strategic market share in high-density corridors.

- 250k ROW miles; fiber revenue ~$420M (2025)

- YoY growth ~22%

- Data centers ≈30% of local load growth

- Target IRR 12–15%

Battery Energy Storage Systems (BESS)

Southern Company has deployed 3,000 MW of battery energy storage systems (BESS) through 2025 to integrate intermittent renewables and stabilize the grid, positioning it as a regional leader in the Southeast for peak management and ancillary services.

These BESS investments sit in the BCG Matrix Stars quadrant: high-growth, high-share assets critical to the modern grid and forming a material part of Southern Company’s $81 billion capex plan through 2030, with storage accounting for a multi-hundred-million-dollar annual spend.

- 3,000 MW storage deployed by 2025

- Targets peak shaving, frequency response, reserve services

- Key to integrating solar/wind and reducing curtailment

- Significant line item within $81B capex program

Southern Surge: 10GW Data Centers, 2.4GW Nuclear, 4.3GW Renewables, $81B Capex

Southern’s Stars: 10 GW data-center contracts, 2.4 GW Vogtle nuclear, 4.3 GW renewables+storage (2.5 GW solar, 1.8 GW wind, 3.0 GW BESS overlap), $81B capex 2025–30, fiber revenue ~$420M (2025), fiber YoY +22%.

| Metric | Value (2025) |

|---|---|

| Data-center contracts | 10 GW |

| Vogtle capacity | 2.4 GW |

| Solar | 2.5 GW |

| Wind | 1.8 GW |

| BESS | 3.0 GW |

| Capex plan | $81B |

| Fiber revenue | $420M (+22% YoY) |

What is included in the product

In-depth BCG analysis of Southern Company’s units with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix placing Southern Company units in clear quadrants for swift portfolio decisions and executive briefings

Cash Cows

Regulated Electric Operations in Alabama

Alabama Power, Southern Company’s regulated electric utility in Alabama, is a cash cow with ~5,000 MW capacity and roughly 1.4 million retail customers, holding dominant market share in a mature market.

In 2025 Alabama Power pledged to keep base rates steady through 2027, supporting stable EBITDA (2024 adj. EBITDA ~ $1.8B) via high operating margins and tight cost control.

Its predictable cash flow funds Southern’s dividends (2025 dividend yield ~3.9%) and finances high-growth capital projects across the group.

Georgia Power Residential and Industrial Sales

Georgia Power’s residential and industrial sales are classic cash cows for Southern Company, delivering stable, high-margin revenues from a dominant market share across Georgia while data centers drive incremental growth.

In 2025 Georgia Power added 39,000 new residential customers, reinforcing steady demand in a mature, regulated market that generated roughly $11.2 billion in retail electric revenues in 2024.

These entrenched cash flows fund the company’s clean-energy investments and underpin Southern Company’s 78-year dividend streak, supporting a 2025 dividend yield near 3.8% while keeping leverage manageable.

Southern Company Gas Distribution

Southern Company Gas Distribution, the market leader in states like Illinois and Georgia, serves over 4 million customers via its local distribution companies and generated roughly $2.8 billion in 2024 operating revenues, per Southern Company filings.

Its authorized rate base has tripled since 2015 to about $9.5 billion in 2024, funding safety-driven pipeline modernization that produces steady, regulated cash flows.

Given low market growth for mature natural gas utilities, this unit is a classic Cash Cow that underpins Southern Company’s dividend capacity and financial stability.

Mississippi Power Regulated Services

Mississippi Power’s regulated utility generates steady cash from ~190,000 customers in southern Mississippi and southeast Alabama, producing roughly $300–350 million in annual EBITDA for Southern Company in 2024, acting as a high-market-share, low-growth cash cow despite Kemper cost overruns.

Cash is directed to service corporate debt and fund Southern Company’s 2024 capital allocation, including $2.8 billion in parent dividends and share repurchases, supporting credit metrics.

- ~190,000 customers

- $300–350M estimated 2024 EBITDA

- High market share, low growth

- Kemper caused past losses, core business intact

- Funds debt service and $2.8B 2024 capital allocation

Southern Power Long-term Contracts

Southern Power holds >13 GW of capacity, with substantially all assets under long-term contracts with investment-grade counterparties, producing highly predictable cash flows and minimal commodity exposure—qualifying as a Cash Cow in the unregulated portfolio.

Revenue from these mature assets generated roughly $2.1 billion in adjusted EBITDA for Southern Company’s unregulated segment in 2024 and is routinely reinvested into energy transition projects and grid modernization through 2025.

- 13+ GW capacity

- Nearly all capacity long-term contracted

- Minimal commodity risk; predictable cash flows

- ~$2.1B adjusted EBITDA (2024, unregulated)

- Reinvested into energy transition & grid upgrades

Southern Co.'s regulated units and Southern Power: $5.4B EBITDA cash cow funding transition

Alabama Power, Georgia Power, Southern Company Gas, Mississippi Power and Southern Power are cash cows: combined 2024 adj. EBITDA ~ $5.4B, regulated customer base ~7.7M, Southern Power 13+ GW contracted; cash funds dividends (2025 yield ~3.8–3.9%), capex for clean-energy transition, and debt service while growth remains low.

| Unit | 2024 adj. EBITDA | Customers / Capacity | Role |

|---|---|---|---|

| Alabama Power | $1.8B | ~1.4M customers | Regulated cash cow |

| Georgia Power | — (part of $11.2B revenues) | 39,000 new customers 2025 | Primary cash engine |

| Gas Distribution | — | ~4M customers | Stable rate base $9.5B |

| Mississippi Power | $300–350M | ~190k customers | Low-growth cash flow |

| Southern Power | $2.1B (unregulated) | 13+ GW contracted | Predictable merchant cash |

Full Transparency, Always

Southern Company BCG Matrix

The file you're previewing is the exact Southern Company BCG Matrix report you'll receive after purchase — fully formatted, analysis-ready, and free of watermarks or demo content. This document mirrors the preview precisely, crafted with market-backed insights and strategic clarity for immediate use in presentations, planning, or client briefs. Upon purchase you'll get the same editable, printable file delivered directly to your inbox—no surprises, no further edits required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Southern Company sits at an inflection point as shifting energy demand and regulatory pressure reshape its portfolio—our preview highlights which business units lean toward Cash Cows and which may be Question Marks amid decarbonization trends. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Data Center Electricity Sales

As of late 2025, Southern Company reports data center electricity sales up 17% year-over-year, driven by AI demand and large-load customers.

The company has 10 GW of signed contracts for hyperscale and AI facilities, giving it a dominant regional share in a high-growth market.

This segment is capital-intensive; Southern expanded its five-year plan to $81 billion to fund generation and transmission capacity for this watershed demand.

Plant Vogtle Units 3 and 4

With Unit 4 reaching full commercial operation in July 2024, Plant Vogtle Units 3 and 4 became the largest clean-energy generator in the US by 2025, adding ~2,400 MW combined of carbon-free capacity that served ~1.9 million homes.

These reactors supply always-on baseload power ideal for hyperscalers and heavy industry; in 2025 Vogtle’s output cut ~11 million metric tons CO2 annually versus gas generation.

Despite earlier cost overruns (final cost ~25–30 billion USD), Vogtle now drives material revenue for Southern Company, supporting RPS compliance and corporate clean-energy contracts.

Renewable Energy Expansion

Southern Company is scaling renewables: solar capacity is projected at 2,500 MW and wind at 1,800 MW by end-2025, making this a Stars quadrant asset with high market growth and strong share.

Growth is driven by the 10-year Inflation Reduction Act tax incentives and state decarbonization mandates; US utility-scale renewables grew ~15% in 2024, fueling demand.

By integrating these assets with its transmission and distribution network, Southern captures more green-market revenue while keeping reliability metrics (SAIDI/SAIFI) stable.

Fiber Optics and Connectivity

Southern Company leverages 250,000+ utility right-of-way miles to expand dark fiber and telco services, making this unit a high-growth Star in digital infrastructure; revenue from fiber and telecom rose ~22% year-over-year to an estimated $420M in 2025.

That fiber directly serves data center developers—responsible for ~30% of regional electricity load growth—creating tight demand coupling as AI and cloud compute drive bandwidth needs.

With average fiber IRR targets near 12–15% and low incremental capex per mile versus greenfield builds, Southern is capturing specialized, strategic market share in high-density corridors.

- 250k ROW miles; fiber revenue ~$420M (2025)

- YoY growth ~22%

- Data centers ≈30% of local load growth

- Target IRR 12–15%

Battery Energy Storage Systems (BESS)

Southern Company has deployed 3,000 MW of battery energy storage systems (BESS) through 2025 to integrate intermittent renewables and stabilize the grid, positioning it as a regional leader in the Southeast for peak management and ancillary services.

These BESS investments sit in the BCG Matrix Stars quadrant: high-growth, high-share assets critical to the modern grid and forming a material part of Southern Company’s $81 billion capex plan through 2030, with storage accounting for a multi-hundred-million-dollar annual spend.

- 3,000 MW storage deployed by 2025

- Targets peak shaving, frequency response, reserve services

- Key to integrating solar/wind and reducing curtailment

- Significant line item within $81B capex program

Southern Surge: 10GW Data Centers, 2.4GW Nuclear, 4.3GW Renewables, $81B Capex

Southern’s Stars: 10 GW data-center contracts, 2.4 GW Vogtle nuclear, 4.3 GW renewables+storage (2.5 GW solar, 1.8 GW wind, 3.0 GW BESS overlap), $81B capex 2025–30, fiber revenue ~$420M (2025), fiber YoY +22%.

| Metric | Value (2025) |

|---|---|

| Data-center contracts | 10 GW |

| Vogtle capacity | 2.4 GW |

| Solar | 2.5 GW |

| Wind | 1.8 GW |

| BESS | 3.0 GW |

| Capex plan | $81B |

| Fiber revenue | $420M (+22% YoY) |

What is included in the product

In-depth BCG analysis of Southern Company’s units with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG Matrix placing Southern Company units in clear quadrants for swift portfolio decisions and executive briefings

Cash Cows

Regulated Electric Operations in Alabama

Alabama Power, Southern Company’s regulated electric utility in Alabama, is a cash cow with ~5,000 MW capacity and roughly 1.4 million retail customers, holding dominant market share in a mature market.

In 2025 Alabama Power pledged to keep base rates steady through 2027, supporting stable EBITDA (2024 adj. EBITDA ~ $1.8B) via high operating margins and tight cost control.

Its predictable cash flow funds Southern’s dividends (2025 dividend yield ~3.9%) and finances high-growth capital projects across the group.

Georgia Power Residential and Industrial Sales

Georgia Power’s residential and industrial sales are classic cash cows for Southern Company, delivering stable, high-margin revenues from a dominant market share across Georgia while data centers drive incremental growth.

In 2025 Georgia Power added 39,000 new residential customers, reinforcing steady demand in a mature, regulated market that generated roughly $11.2 billion in retail electric revenues in 2024.

These entrenched cash flows fund the company’s clean-energy investments and underpin Southern Company’s 78-year dividend streak, supporting a 2025 dividend yield near 3.8% while keeping leverage manageable.

Southern Company Gas Distribution

Southern Company Gas Distribution, the market leader in states like Illinois and Georgia, serves over 4 million customers via its local distribution companies and generated roughly $2.8 billion in 2024 operating revenues, per Southern Company filings.

Its authorized rate base has tripled since 2015 to about $9.5 billion in 2024, funding safety-driven pipeline modernization that produces steady, regulated cash flows.

Given low market growth for mature natural gas utilities, this unit is a classic Cash Cow that underpins Southern Company’s dividend capacity and financial stability.

Mississippi Power Regulated Services

Mississippi Power’s regulated utility generates steady cash from ~190,000 customers in southern Mississippi and southeast Alabama, producing roughly $300–350 million in annual EBITDA for Southern Company in 2024, acting as a high-market-share, low-growth cash cow despite Kemper cost overruns.

Cash is directed to service corporate debt and fund Southern Company’s 2024 capital allocation, including $2.8 billion in parent dividends and share repurchases, supporting credit metrics.

- ~190,000 customers

- $300–350M estimated 2024 EBITDA

- High market share, low growth

- Kemper caused past losses, core business intact

- Funds debt service and $2.8B 2024 capital allocation

Southern Power Long-term Contracts

Southern Power holds >13 GW of capacity, with substantially all assets under long-term contracts with investment-grade counterparties, producing highly predictable cash flows and minimal commodity exposure—qualifying as a Cash Cow in the unregulated portfolio.

Revenue from these mature assets generated roughly $2.1 billion in adjusted EBITDA for Southern Company’s unregulated segment in 2024 and is routinely reinvested into energy transition projects and grid modernization through 2025.

- 13+ GW capacity

- Nearly all capacity long-term contracted

- Minimal commodity risk; predictable cash flows

- ~$2.1B adjusted EBITDA (2024, unregulated)

- Reinvested into energy transition & grid upgrades

Southern Co.'s regulated units and Southern Power: $5.4B EBITDA cash cow funding transition

Alabama Power, Georgia Power, Southern Company Gas, Mississippi Power and Southern Power are cash cows: combined 2024 adj. EBITDA ~ $5.4B, regulated customer base ~7.7M, Southern Power 13+ GW contracted; cash funds dividends (2025 yield ~3.8–3.9%), capex for clean-energy transition, and debt service while growth remains low.

| Unit | 2024 adj. EBITDA | Customers / Capacity | Role |

|---|---|---|---|

| Alabama Power | $1.8B | ~1.4M customers | Regulated cash cow |

| Georgia Power | — (part of $11.2B revenues) | 39,000 new customers 2025 | Primary cash engine |

| Gas Distribution | — | ~4M customers | Stable rate base $9.5B |

| Mississippi Power | $300–350M | ~190k customers | Low-growth cash flow |

| Southern Power | $2.1B (unregulated) | 13+ GW contracted | Predictable merchant cash |

Full Transparency, Always

Southern Company BCG Matrix

The file you're previewing is the exact Southern Company BCG Matrix report you'll receive after purchase — fully formatted, analysis-ready, and free of watermarks or demo content. This document mirrors the preview precisely, crafted with market-backed insights and strategic clarity for immediate use in presentations, planning, or client briefs. Upon purchase you'll get the same editable, printable file delivered directly to your inbox—no surprises, no further edits required.