Southern Company PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of Southern Company—spot regulatory, economic, and technological forces shaping its trajectory and turn insights into competitive advantage; buy the full report for the complete, editable breakdown and immediate use in investment or strategic planning.

Political factors

Federal Clean Energy Incentives

The Inflation Reduction Act delivers tax credits that reduced Southern Company’s expected capital costs for renewables by an estimated 15–20%, supporting the utility’s target to add ~6 GW of solar and 3 GW of wind by 2030.

State Regulatory Relations

Southern Company benefits from traditionally supportive Public Service Commissions in Georgia, Alabama and Mississippi, facilitating consistent rate recovery for infrastructure spending; Georgia PSC approved a $7.3 billion multi-year rate plan through 2025 supporting grid investments.

Nuclear Energy Policy Support

The successful commercial operation of Vogtle Units 3 and 4, adding about 2,234 MW of carbon-free capacity, positions Southern Company as a leader in the U.S. nuclear renaissance and has driven a ~4% increase in the company’s generation capacity mix toward baseload nuclear in 2024.

Federal incentives such as the 2021 IRA production tax credits and $10+ billion in DOE loan guarantees continue to favor nuclear investment, aligning with Southern’s strategy to meet surging data center and manufacturing demand projected to grow annual electricity use by mid-single digits through 2028.

Ongoing government funding for nuclear R&D—over $2.6 billion in recent DOE budgets for advanced reactors and SMRs—gives Southern a long-term strategic edge in a decarbonizing economy and supports potential future cost reductions and capacity expansion.

Bipartisan Infrastructure Law Implementation

By late 2025 Southern Company secured roughly $1.2 billion in Bipartisan Infrastructure Law grants to bolster grid resilience and regional connectivity, enabling deployment of dynamic line rating and HVDC links to manage rising intermittent renewables.

These federal funds accelerate advanced transmission rollout—reducing projected capital recovery by an estimated $450 million over 10 years—and shift a portion of modernization costs away from ratepayers.

Energy Security and Geopolitical Stability

National security concerns over grid resilience have pushed federal action; the Bipartisan Infrastructure Law and 2024 DOE directives boosted funding for grid hardening, with $10.5 billion allocated nationally for transmission and resilience projects that pressure Southern Company to harden assets and diversify suppliers.

Federal mandates to limit foreign-critical components—especially transformers and semiconductors—affect procurement; Southern reported in 2025 that domestic sourcing increased by 18% YoY to reduce geopolitical risk and ensure compliance.

- Increased federal funding: $10.5B nationwide for grid resilience (BIL, 2024)

- Southern Company domestic sourcing +18% YoY (2025)

- Procurement shift toward U.S. suppliers for transformers/semiconductors

Federal incentives cut costs, fuel Vogtle 2,234 MW and $1.2B grid investments

Federal incentives (IRA, DOE guarantees) cut renewables/nuclear capital costs ~15–20% and supported Vogtle adding ~2,234 MW; Georgia PSC approved $7.3B multiyear rates to fund grid upgrades; Southern secured ~$1.2B BIL grants and increased domestic sourcing +18% YoY (2025) amid $10.5B national grid resilience funding.

| Item | Value |

|---|---|

| Vogtle capacity | 2,234 MW |

| IRA capital cost reduction | 15–20% |

| Georgia PSC plan | $7.3B |

| BIL grants | $1.2B |

| Domestic sourcing rise | +18% YoY (2025) |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect Southern Company, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists, delivered in concise, report-ready format for planning, pitching, and scenario design.

Concise PESTLE summary of Southern Company that’s easy to drop into presentations or planning sessions, visually segmented for quick interpretation and editable for region- or business-line–specific notes to support risk discussions and team alignment.

Economic factors

Interest Rate Environment

As a capital-intensive utility, Southern Company remains highly sensitive to interest rates, with the company's long-term debt totaling about $48.6 billion at year-end 2025, making borrowing costs materially influential on project viability.

Interest rates stabilized in late 2025 after Federal Reserve easing, but average interest expense of $2.9 billion in 2025 shows servicing legacy debt still pressures net income.

Management prioritizes optimizing capital structure—debt-to-capital ratio ~60% in 2025—to protect margins and keep WACC competitive for large-scale grid and generation investments.

Southeast Regional Economic Growth

The Southeastern US posted GDP growth of about 3.2% in 2024 as EV manufacturing and hyperscale data center investment surged, with Georgia, Alabama and Tennessee adding over $45 billion in announced projects through 2024; this drives meaningful residential and industrial electricity demand increases for Southern Company subsidiaries. The company forecasted system peak load growth of ~1.8–2.2% annually (2025–2030), prompting accelerated capital spending—Southern Company planned roughly $24–26 billion in T&D and generation investments in its 2024–2026 plan. The expanding customer base improves revenue visibility and regulatory support for rate-based investments versus slower-growth regions, underpinning stronger utility earnings resilience.

Fuel Price Volatility

Fluctuations in natural gas prices materially affect Southern Company’s gas distribution and thermal generation costs; in 2024 Henry Hub averaged about 3.83 USD/MMBtu, and a 30% price swing would notably raise fuel expense for the utility segments.

Southern uses hedging and long-term contracts—hedged volumes covered roughly 40–50% of 2024 expected consumption—to limit short-term volatility, but sustained spikes can force higher customer rates and invite regulatory scrutiny.

By 2025 the company accelerated fuel diversification, targeting added renewables and firmed capacity to reduce gas burn exposure, aiming to lower portfolio commodity sensitivity and stabilize margins amid global market swings.

Inflationary Pressures on Operations

Ongoing inflation pushed U.S. producer prices up 2.0% year-over-year in 2025 Q4, driving Southern Company’s reported O&M and capital project cost pressure—labor wages rose ~4–5% and materials like transformers increased 8–12% in 2024–25, complicating large-scale grid upgrades and routine maintenance.

Specialized equipment shortages and higher prices for transformers and high-voltage cables raise unit costs and project timelines; Southern’s 2024 capital expenditures of $6.8B face margin squeeze without tightened cost controls.

Efficient supply-chain strategies, bulk procurement, and lean project management are essential to protect operating margins and meet 2025–26 earnings targets amid persistent input-cost inflation.

- Labor up ~4–5% (2024–25)

- Transformers +8–12% price growth (2024–25)

- 2024 capex $6.8B at risk from inflation

- Supply-chain optimization required to safeguard margins

Capital Expenditure for Vogtle

With Vogtle units 3 and 4 online, Southern faces long-term recovery of about $30–35 billion in Vogtle capital costs (company disclosures through 2025), shifting focus from construction risk to rate-base realization and depreciation policies.

Ensuring depreciation and O&M for nuclear assets are fully reflected in regulated rate bases is critical to recouping costs and preserving cash flow, supporting an investment-grade credit profile (S&P BBB+ as of 2025) and sustaining the ~3.5% dividend yield.

- Vogtle capex recovery target: $30–35B (through 2025)

- Credit importance: S&P BBB+ (2025)

- Dividend yield: ~3.5% (2025)

High debt load ($48.6B) and heavy capex as Vogtle recovery drives credit watch

Interest-rate sensitivity: $48.6B debt (2025), interest expense $2.9B (2025); cap structure ~60% debt. Regional demand: SE GDP +3.2% (2024); system peak growth 1.8–2.2% (2025–30); 2024–26 capex $24–26B. Fuel/inflation: Henry Hub $3.83/MMBtu (2024); hedges 40–50% (2024); labor +4–5% (2024–25); 2024 capex $6.8B. Vogtle recovery $30–35B; S&P BBB+ (2025).

| Metric | Value |

|---|---|

| Total debt | $48.6B (2025) |

| Interest expense | $2.9B (2025) |

| Vogtle recovery | $30–35B (through 2025) |

| Capex plan | $24–26B (2024–26) |

Preview the Actual Deliverable

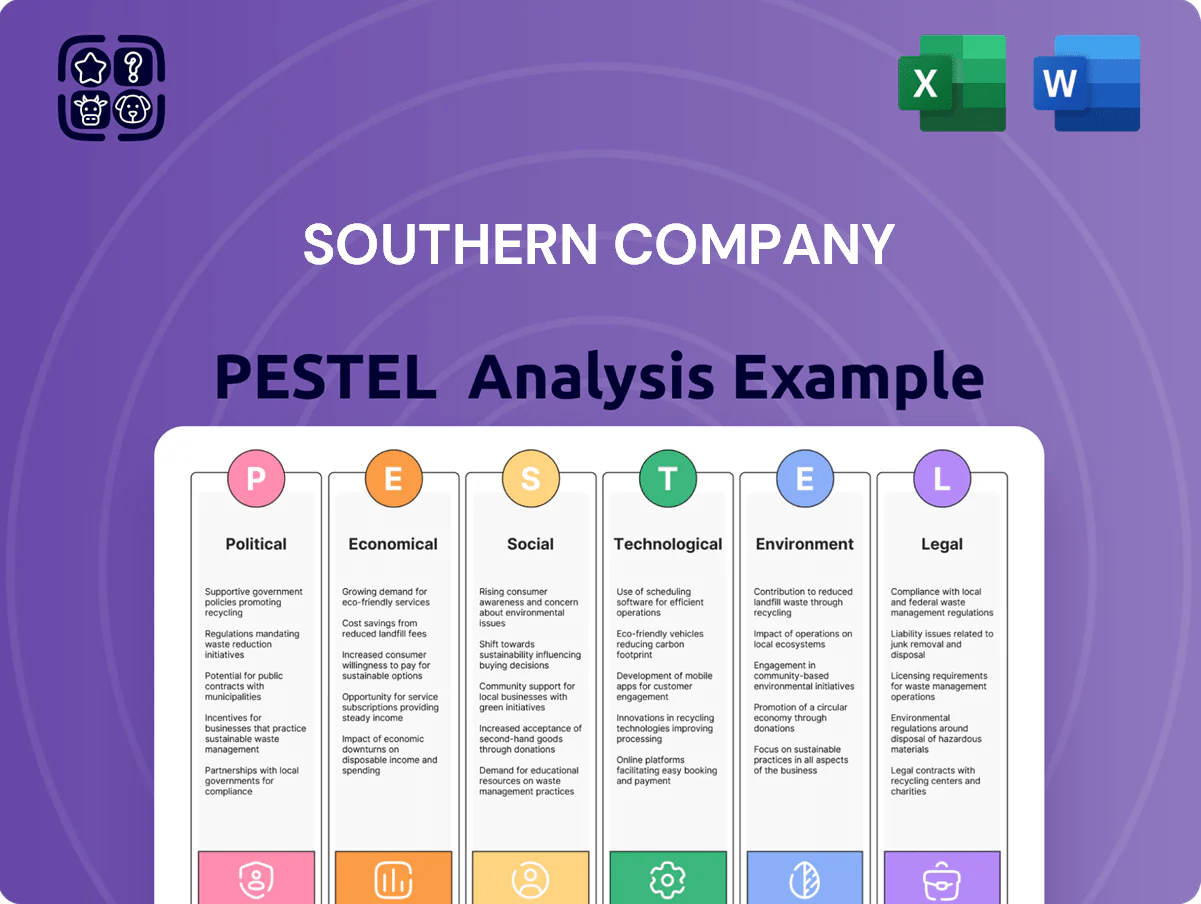

Southern Company PESTLE Analysis

The preview shown here is the exact Southern Company PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

This is a real screenshot of the product you’re buying—delivered exactly as shown with complete political, economic, social, technological, legal, and environmental insights.

No placeholders or teasers—what you see is the final file you’ll be able to download instantly after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of Southern Company—spot regulatory, economic, and technological forces shaping its trajectory and turn insights into competitive advantage; buy the full report for the complete, editable breakdown and immediate use in investment or strategic planning.

Political factors

Federal Clean Energy Incentives

The Inflation Reduction Act delivers tax credits that reduced Southern Company’s expected capital costs for renewables by an estimated 15–20%, supporting the utility’s target to add ~6 GW of solar and 3 GW of wind by 2030.

State Regulatory Relations

Southern Company benefits from traditionally supportive Public Service Commissions in Georgia, Alabama and Mississippi, facilitating consistent rate recovery for infrastructure spending; Georgia PSC approved a $7.3 billion multi-year rate plan through 2025 supporting grid investments.

Nuclear Energy Policy Support

The successful commercial operation of Vogtle Units 3 and 4, adding about 2,234 MW of carbon-free capacity, positions Southern Company as a leader in the U.S. nuclear renaissance and has driven a ~4% increase in the company’s generation capacity mix toward baseload nuclear in 2024.

Federal incentives such as the 2021 IRA production tax credits and $10+ billion in DOE loan guarantees continue to favor nuclear investment, aligning with Southern’s strategy to meet surging data center and manufacturing demand projected to grow annual electricity use by mid-single digits through 2028.

Ongoing government funding for nuclear R&D—over $2.6 billion in recent DOE budgets for advanced reactors and SMRs—gives Southern a long-term strategic edge in a decarbonizing economy and supports potential future cost reductions and capacity expansion.

Bipartisan Infrastructure Law Implementation

By late 2025 Southern Company secured roughly $1.2 billion in Bipartisan Infrastructure Law grants to bolster grid resilience and regional connectivity, enabling deployment of dynamic line rating and HVDC links to manage rising intermittent renewables.

These federal funds accelerate advanced transmission rollout—reducing projected capital recovery by an estimated $450 million over 10 years—and shift a portion of modernization costs away from ratepayers.

Energy Security and Geopolitical Stability

National security concerns over grid resilience have pushed federal action; the Bipartisan Infrastructure Law and 2024 DOE directives boosted funding for grid hardening, with $10.5 billion allocated nationally for transmission and resilience projects that pressure Southern Company to harden assets and diversify suppliers.

Federal mandates to limit foreign-critical components—especially transformers and semiconductors—affect procurement; Southern reported in 2025 that domestic sourcing increased by 18% YoY to reduce geopolitical risk and ensure compliance.

- Increased federal funding: $10.5B nationwide for grid resilience (BIL, 2024)

- Southern Company domestic sourcing +18% YoY (2025)

- Procurement shift toward U.S. suppliers for transformers/semiconductors

Federal incentives cut costs, fuel Vogtle 2,234 MW and $1.2B grid investments

Federal incentives (IRA, DOE guarantees) cut renewables/nuclear capital costs ~15–20% and supported Vogtle adding ~2,234 MW; Georgia PSC approved $7.3B multiyear rates to fund grid upgrades; Southern secured ~$1.2B BIL grants and increased domestic sourcing +18% YoY (2025) amid $10.5B national grid resilience funding.

| Item | Value |

|---|---|

| Vogtle capacity | 2,234 MW |

| IRA capital cost reduction | 15–20% |

| Georgia PSC plan | $7.3B |

| BIL grants | $1.2B |

| Domestic sourcing rise | +18% YoY (2025) |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect Southern Company, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists, delivered in concise, report-ready format for planning, pitching, and scenario design.

Concise PESTLE summary of Southern Company that’s easy to drop into presentations or planning sessions, visually segmented for quick interpretation and editable for region- or business-line–specific notes to support risk discussions and team alignment.

Economic factors

Interest Rate Environment

As a capital-intensive utility, Southern Company remains highly sensitive to interest rates, with the company's long-term debt totaling about $48.6 billion at year-end 2025, making borrowing costs materially influential on project viability.

Interest rates stabilized in late 2025 after Federal Reserve easing, but average interest expense of $2.9 billion in 2025 shows servicing legacy debt still pressures net income.

Management prioritizes optimizing capital structure—debt-to-capital ratio ~60% in 2025—to protect margins and keep WACC competitive for large-scale grid and generation investments.

Southeast Regional Economic Growth

The Southeastern US posted GDP growth of about 3.2% in 2024 as EV manufacturing and hyperscale data center investment surged, with Georgia, Alabama and Tennessee adding over $45 billion in announced projects through 2024; this drives meaningful residential and industrial electricity demand increases for Southern Company subsidiaries. The company forecasted system peak load growth of ~1.8–2.2% annually (2025–2030), prompting accelerated capital spending—Southern Company planned roughly $24–26 billion in T&D and generation investments in its 2024–2026 plan. The expanding customer base improves revenue visibility and regulatory support for rate-based investments versus slower-growth regions, underpinning stronger utility earnings resilience.

Fuel Price Volatility

Fluctuations in natural gas prices materially affect Southern Company’s gas distribution and thermal generation costs; in 2024 Henry Hub averaged about 3.83 USD/MMBtu, and a 30% price swing would notably raise fuel expense for the utility segments.

Southern uses hedging and long-term contracts—hedged volumes covered roughly 40–50% of 2024 expected consumption—to limit short-term volatility, but sustained spikes can force higher customer rates and invite regulatory scrutiny.

By 2025 the company accelerated fuel diversification, targeting added renewables and firmed capacity to reduce gas burn exposure, aiming to lower portfolio commodity sensitivity and stabilize margins amid global market swings.

Inflationary Pressures on Operations

Ongoing inflation pushed U.S. producer prices up 2.0% year-over-year in 2025 Q4, driving Southern Company’s reported O&M and capital project cost pressure—labor wages rose ~4–5% and materials like transformers increased 8–12% in 2024–25, complicating large-scale grid upgrades and routine maintenance.

Specialized equipment shortages and higher prices for transformers and high-voltage cables raise unit costs and project timelines; Southern’s 2024 capital expenditures of $6.8B face margin squeeze without tightened cost controls.

Efficient supply-chain strategies, bulk procurement, and lean project management are essential to protect operating margins and meet 2025–26 earnings targets amid persistent input-cost inflation.

- Labor up ~4–5% (2024–25)

- Transformers +8–12% price growth (2024–25)

- 2024 capex $6.8B at risk from inflation

- Supply-chain optimization required to safeguard margins

Capital Expenditure for Vogtle

With Vogtle units 3 and 4 online, Southern faces long-term recovery of about $30–35 billion in Vogtle capital costs (company disclosures through 2025), shifting focus from construction risk to rate-base realization and depreciation policies.

Ensuring depreciation and O&M for nuclear assets are fully reflected in regulated rate bases is critical to recouping costs and preserving cash flow, supporting an investment-grade credit profile (S&P BBB+ as of 2025) and sustaining the ~3.5% dividend yield.

- Vogtle capex recovery target: $30–35B (through 2025)

- Credit importance: S&P BBB+ (2025)

- Dividend yield: ~3.5% (2025)

High debt load ($48.6B) and heavy capex as Vogtle recovery drives credit watch

Interest-rate sensitivity: $48.6B debt (2025), interest expense $2.9B (2025); cap structure ~60% debt. Regional demand: SE GDP +3.2% (2024); system peak growth 1.8–2.2% (2025–30); 2024–26 capex $24–26B. Fuel/inflation: Henry Hub $3.83/MMBtu (2024); hedges 40–50% (2024); labor +4–5% (2024–25); 2024 capex $6.8B. Vogtle recovery $30–35B; S&P BBB+ (2025).

| Metric | Value |

|---|---|

| Total debt | $48.6B (2025) |

| Interest expense | $2.9B (2025) |

| Vogtle recovery | $30–35B (through 2025) |

| Capex plan | $24–26B (2024–26) |

Preview the Actual Deliverable

Southern Company PESTLE Analysis

The preview shown here is the exact Southern Company PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

This is a real screenshot of the product you’re buying—delivered exactly as shown with complete political, economic, social, technological, legal, and environmental insights.

No placeholders or teasers—what you see is the final file you’ll be able to download instantly after checkout.