South Indian Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

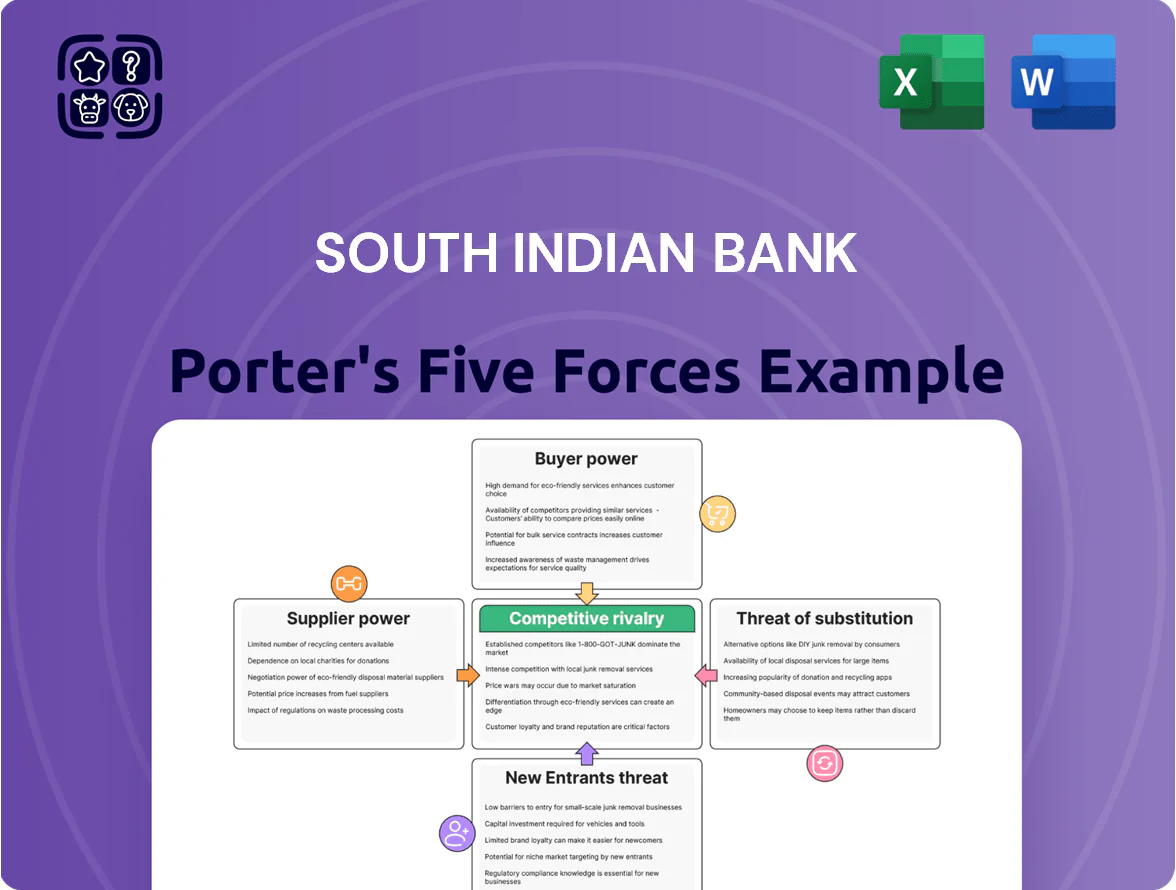

South Indian Bank navigates a dynamic banking landscape where intense rivalry, the growing threat of new entrants, and evolving customer expectations significantly shape its competitive environment. Understanding the power of suppliers and the availability of substitutes is crucial for strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore South Indian Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology and Infrastructure Providers

South Indian Bank's reliance on technology providers for core banking, digital payments, and cybersecurity is substantial. The bargaining power of these specialized suppliers is often moderate to high, particularly when dealing with proprietary software or critical infrastructure where switching costs are significant, or the required expertise is scarce. For instance, banks globally are channeling considerable resources into digital transformation and AI integration, thereby amplifying their dependence on these tech vendors.

Depositors (Fund Suppliers)

Depositors are crucial 'fund suppliers' for South Indian Bank, providing the capital it needs to operate and lend. Their bargaining power is directly tied to the interest rates offered by competing financial institutions and how easy it is for them to move their money elsewhere.

In 2024, with inflation concerns persisting and the proliferation of user-friendly digital banking platforms, depositors are increasingly scrutinizing the rates they receive on their savings. This heightened awareness of alternative investment options and the ease of switching banks means depositors are likely to exert greater influence on the bank's cost of funds.

Skilled Human Capital

The banking sector's digital evolution fuels a significant demand for specialized talent in IT, data analytics, cybersecurity, and fintech. This scarcity of skilled professionals grants them considerable bargaining power, as institutions like South Indian Bank vie for these crucial resources to bolster digital initiatives and operational efficiency.

Regulatory Bodies (RBI)

Regulatory bodies, particularly the Reserve Bank of India (RBI), exert considerable influence over South Indian Bank, akin to suppliers dictating terms. The RBI's directives on capital adequacy ratios, for instance, directly impact a bank's ability to lend and its profitability. For example, in 2023-24, the RBI continued to emphasize robust capital buffers, with banks generally maintaining their Capital Adequacy Ratio (CAR) well above the regulatory minimums, providing a degree of stability but also constraining aggressive growth strategies.

These mandates, such as evolving digital lending guidelines or revised provisioning norms for bad loans, can significantly alter a bank's operational costs and strategic flexibility. For instance, stricter provisioning requirements can reduce a bank's net profit, impacting its overall financial health and the resources available for expansion or innovation. South Indian Bank, like its peers, must adapt to these evolving regulatory landscapes, which can be seen as a cost of doing business imposed by a powerful external entity.

- RBI's Capital Requirements: Mandates like Basel III norms dictate minimum capital levels, influencing lending capacity and profitability.

- Digital Lending Norms: New regulations can increase compliance costs and affect revenue streams from digital channels.

- Provisioning Standards: Stricter rules on setting aside funds for potential loan defaults directly impact a bank's bottom line.

- Investment Caps: Limits on certain types of investments can restrict diversification and return opportunities.

Interbank Market and Financial Institutions

The interbank market and other financial institutions are crucial for South Indian Bank's operations, supplying essential liquidity and specialized financial products. These relationships, while generally stable, can shift. For instance, in early 2024, increased demand for short-term funding across the banking sector may have slightly elevated the bargaining power of institutions holding significant liquidity, potentially impacting the cost of funds for banks like South Indian Bank.

While the interbank market is typically liquid, specific funding needs or the requirement for niche financial services can empower certain institutions. This can translate into them having some leverage over South Indian Bank, influencing the cost of borrowing or the terms of access to particular financial instruments. For example, if a bank requires a very specific type of derivative for hedging, the provider of that niche product might command a higher price or more favorable terms.

- Liquidity Provision: Interbank markets and financial institutions are primary sources of short-term and long-term funding for banks.

- Specialized Services: These entities offer services like foreign exchange, derivatives, and syndicated loans, which banks may not provide internally.

- Cost of Funds Influence: The rates at which banks borrow from each other or from other financial institutions directly impact their profitability.

- 2024 Market Dynamics: Global interest rate hikes and evolving regulatory landscapes in 2024 created a more dynamic environment for interbank lending, potentially increasing supplier power in certain segments.

Bank's Supplier Power Dynamics: Tech, Deposits, and Regulation

South Indian Bank's suppliers, ranging from technology vendors to depositors and even regulatory bodies, wield varying degrees of bargaining power. Technology providers offering specialized, proprietary software or critical infrastructure can command higher prices due to significant switching costs and scarce expertise. Depositors, particularly in 2024, are more informed about rates and the ease of switching, increasing their influence on the bank's cost of funds. Furthermore, the demand for skilled IT and data analytics professionals grants these individuals considerable leverage.

The Reserve Bank of India (RBI) acts as a powerful supplier of regulatory frameworks, directly impacting South Indian Bank's operational costs and strategic flexibility. Mandates like capital adequacy ratios and evolving digital lending guidelines necessitate compliance, which can constrain growth and affect profitability. In 2023-24, banks generally maintained robust Capital Adequacy Ratios above minimums, a testament to regulatory influence.

The interbank market also serves as a supplier of liquidity and specialized financial products. In early 2024, increased sector-wide funding demand potentially amplified the bargaining power of institutions with ample liquidity, influencing borrowing costs for banks like South Indian Bank.

| Supplier Type | Bargaining Power Influence | Key Factors | 2024 Context |

| Technology Providers | Moderate to High | Proprietary software, switching costs, scarce expertise | Increased reliance on digital transformation and AI |

| Depositors | Moderate to High | Interest rate competition, ease of switching, digital platform access | Heightened awareness of alternative investments |

| Skilled Professionals (IT, Data) | High | Scarcity of talent, demand for digital initiatives | Intensified competition for specialized skills |

| RBI (Regulatory Body) | Very High | Capital adequacy, lending norms, provisioning standards | Continued emphasis on robust capital buffers |

| Interbank Market/Financial Institutions | Moderate | Liquidity provision, specialized services, cost of funds | Dynamic environment due to interest rate shifts |

What is included in the product

Tailored exclusively for South Indian Bank, this analysis dissects the intensity of rivalry, buyer and supplier power, the threat of new entrants and substitutes, providing strategic insights into its competitive environment.

A visual representation of competitive intensity—helping to pinpoint where South Indian Bank can build sustainable advantage.

Customers Bargaining Power

High Customer Choice and Low Switching Costs

Customers in India's banking landscape enjoy a wealth of choices, ranging from established public and private sector banks to foreign institutions, specialized small finance banks, and emerging payment banks. This diverse ecosystem is further enriched by a growing number of fintech companies offering innovative financial solutions.

The digital transformation sweeping through the banking sector significantly reduces the effort and expense associated with switching providers. As more services become accessible online and through mobile apps, customers can easily compare offerings and move their business to institutions that provide more favorable terms, better interest rates, or a superior user experience, thereby amplifying their bargaining power.

Price Sensitivity to Interest Rates and Fees

Customers' sensitivity to interest rates on loans and deposits, along with various banking fees, significantly impacts their choices. For instance, during 2024, many banks adjusted their deposit rates in response to evolving monetary policy, directly influencing customer decisions on where to park their savings. This price sensitivity means banks like South Indian Bank must remain competitive to retain their customer base.

In a market with numerous banking options, South Indian Bank faces pressure to offer attractive interest rates and clear, reasonable fee structures. Failing to do so can lead customers to switch to competitors. This dynamic limits the bank's power to unilaterally hike charges or reduce customer benefits, as it could result in a loss of business, especially for retail and small business segments that are more rate-sensitive.

Increasing Digital Literacy and Access to Information

As digital literacy surges across India, with smartphone penetration reaching approximately 70% by early 2024 and internet access expanding rapidly, bank customers are better equipped than ever to research and compare financial products. This heightened awareness allows them to easily identify and switch to competitors offering more favorable terms or lower fees, significantly amplifying their bargaining power.

Availability of Alternative Financial Service Providers

The increasing presence of Non-Banking Financial Companies (NBFCs) and burgeoning fintech startups significantly amplifies customer bargaining power. These entities offer specialized, agile alternatives for services like instant credit, digital transactions, and investment management, directly challenging traditional banks. For instance, by mid-2024, India's fintech sector saw a surge, with digital payment volumes alone crossing 10 billion transactions monthly, providing consumers with a wider array of choices and greater leverage.

This proliferation of financial service providers means customers are no longer solely reliant on established banks. They can readily switch to providers offering better rates, more convenient digital interfaces, or tailored products. This competitive landscape forces traditional institutions like South Indian Bank to innovate and improve their offerings to retain customers, thereby increasing the bargaining power of the customer base.

- Increased Competition: NBFCs and fintech firms offer specialized services, fragmenting the market and giving customers more options.

- Digital Transformation: Fintech advancements provide easier access to alternative financial solutions, empowering customers.

- Customer Choice: A broader range of providers means customers can seek out the best terms and services for their specific needs.

- Rate Sensitivity: Customers are more likely to switch providers for better interest rates or lower fees, driven by the availability of alternatives.

Customer Demand for Personalized and Seamless Experiences

Customers today demand hyper-personalized services and seamless digital interactions. This means banks must offer tailored products and easy-to-use online platforms. Failure to adapt can lead to customer attrition, as seen in the growing market share of fintechs that excel in these areas.

South Indian Bank, like its peers, faces pressure to invest in customer-centric innovations to retain its client base. In 2023, digital transactions through South Indian Bank's mobile banking platform saw a significant increase, reflecting this shift in customer preference. This ongoing trend necessitates continuous upgrades to digital infrastructure and service offerings.

- Customer Expectations: Modern consumers expect financial institutions to understand their individual needs and provide integrated, easy-to-access services across all channels.

- Digital Dominance: The increasing reliance on mobile and online platforms means that a poor digital experience can quickly drive customers to competitors.

- Fintech Competition: Agile fintech companies often lead the way in offering personalized and seamless experiences, posing a direct challenge to traditional banks.

- Investment Imperative: Banks must allocate resources towards technology and data analytics to meet these evolving customer demands and maintain competitiveness.

Customer Power Reshapes India's Banking Landscape

The bargaining power of customers in India's banking sector is substantial, driven by intense competition and rapid digital transformation. Customers have access to a wide array of choices, from traditional banks to agile fintechs and NBFCs, making it easier than ever to switch providers for better rates or services. This environment compels banks like South Indian Bank to remain competitive and customer-centric.

| Factor | Impact on South Indian Bank | Supporting Data (2023-2024) |

|---|---|---|

| Increased Competition | Limits pricing power, necessitates competitive offerings. | India's fintech sector saw over 10 billion digital payment transactions monthly by mid-2024. |

| Digital Transformation | Reduces switching costs, amplifies customer ability to compare. | Smartphone penetration reached ~70% by early 2024, facilitating easy access to online banking. |

| Customer Expectations | Demand for personalization and seamless digital experiences. | South Indian Bank's digital transactions increased significantly in 2023, reflecting customer preference. |

| Rate Sensitivity | Customers readily switch for better interest rates or lower fees. | Banks adjusted deposit rates in 2024 due to monetary policy changes, directly influencing customer decisions. |

Preview the Actual Deliverable

South Indian Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. This comprehensive Porter's Five Forces analysis delves into the competitive landscape of South Indian Bank, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector. Understand the strategic implications for South Indian Bank's market position and future growth.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

South Indian Bank navigates a dynamic banking landscape where intense rivalry, the growing threat of new entrants, and evolving customer expectations significantly shape its competitive environment. Understanding the power of suppliers and the availability of substitutes is crucial for strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore South Indian Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology and Infrastructure Providers

South Indian Bank's reliance on technology providers for core banking, digital payments, and cybersecurity is substantial. The bargaining power of these specialized suppliers is often moderate to high, particularly when dealing with proprietary software or critical infrastructure where switching costs are significant, or the required expertise is scarce. For instance, banks globally are channeling considerable resources into digital transformation and AI integration, thereby amplifying their dependence on these tech vendors.

Depositors (Fund Suppliers)

Depositors are crucial 'fund suppliers' for South Indian Bank, providing the capital it needs to operate and lend. Their bargaining power is directly tied to the interest rates offered by competing financial institutions and how easy it is for them to move their money elsewhere.

In 2024, with inflation concerns persisting and the proliferation of user-friendly digital banking platforms, depositors are increasingly scrutinizing the rates they receive on their savings. This heightened awareness of alternative investment options and the ease of switching banks means depositors are likely to exert greater influence on the bank's cost of funds.

Skilled Human Capital

The banking sector's digital evolution fuels a significant demand for specialized talent in IT, data analytics, cybersecurity, and fintech. This scarcity of skilled professionals grants them considerable bargaining power, as institutions like South Indian Bank vie for these crucial resources to bolster digital initiatives and operational efficiency.

Regulatory Bodies (RBI)

Regulatory bodies, particularly the Reserve Bank of India (RBI), exert considerable influence over South Indian Bank, akin to suppliers dictating terms. The RBI's directives on capital adequacy ratios, for instance, directly impact a bank's ability to lend and its profitability. For example, in 2023-24, the RBI continued to emphasize robust capital buffers, with banks generally maintaining their Capital Adequacy Ratio (CAR) well above the regulatory minimums, providing a degree of stability but also constraining aggressive growth strategies.

These mandates, such as evolving digital lending guidelines or revised provisioning norms for bad loans, can significantly alter a bank's operational costs and strategic flexibility. For instance, stricter provisioning requirements can reduce a bank's net profit, impacting its overall financial health and the resources available for expansion or innovation. South Indian Bank, like its peers, must adapt to these evolving regulatory landscapes, which can be seen as a cost of doing business imposed by a powerful external entity.

- RBI's Capital Requirements: Mandates like Basel III norms dictate minimum capital levels, influencing lending capacity and profitability.

- Digital Lending Norms: New regulations can increase compliance costs and affect revenue streams from digital channels.

- Provisioning Standards: Stricter rules on setting aside funds for potential loan defaults directly impact a bank's bottom line.

- Investment Caps: Limits on certain types of investments can restrict diversification and return opportunities.

Interbank Market and Financial Institutions

The interbank market and other financial institutions are crucial for South Indian Bank's operations, supplying essential liquidity and specialized financial products. These relationships, while generally stable, can shift. For instance, in early 2024, increased demand for short-term funding across the banking sector may have slightly elevated the bargaining power of institutions holding significant liquidity, potentially impacting the cost of funds for banks like South Indian Bank.

While the interbank market is typically liquid, specific funding needs or the requirement for niche financial services can empower certain institutions. This can translate into them having some leverage over South Indian Bank, influencing the cost of borrowing or the terms of access to particular financial instruments. For example, if a bank requires a very specific type of derivative for hedging, the provider of that niche product might command a higher price or more favorable terms.

- Liquidity Provision: Interbank markets and financial institutions are primary sources of short-term and long-term funding for banks.

- Specialized Services: These entities offer services like foreign exchange, derivatives, and syndicated loans, which banks may not provide internally.

- Cost of Funds Influence: The rates at which banks borrow from each other or from other financial institutions directly impact their profitability.

- 2024 Market Dynamics: Global interest rate hikes and evolving regulatory landscapes in 2024 created a more dynamic environment for interbank lending, potentially increasing supplier power in certain segments.

Bank's Supplier Power Dynamics: Tech, Deposits, and Regulation

South Indian Bank's suppliers, ranging from technology vendors to depositors and even regulatory bodies, wield varying degrees of bargaining power. Technology providers offering specialized, proprietary software or critical infrastructure can command higher prices due to significant switching costs and scarce expertise. Depositors, particularly in 2024, are more informed about rates and the ease of switching, increasing their influence on the bank's cost of funds. Furthermore, the demand for skilled IT and data analytics professionals grants these individuals considerable leverage.

The Reserve Bank of India (RBI) acts as a powerful supplier of regulatory frameworks, directly impacting South Indian Bank's operational costs and strategic flexibility. Mandates like capital adequacy ratios and evolving digital lending guidelines necessitate compliance, which can constrain growth and affect profitability. In 2023-24, banks generally maintained robust Capital Adequacy Ratios above minimums, a testament to regulatory influence.

The interbank market also serves as a supplier of liquidity and specialized financial products. In early 2024, increased sector-wide funding demand potentially amplified the bargaining power of institutions with ample liquidity, influencing borrowing costs for banks like South Indian Bank.

| Supplier Type | Bargaining Power Influence | Key Factors | 2024 Context |

| Technology Providers | Moderate to High | Proprietary software, switching costs, scarce expertise | Increased reliance on digital transformation and AI |

| Depositors | Moderate to High | Interest rate competition, ease of switching, digital platform access | Heightened awareness of alternative investments |

| Skilled Professionals (IT, Data) | High | Scarcity of talent, demand for digital initiatives | Intensified competition for specialized skills |

| RBI (Regulatory Body) | Very High | Capital adequacy, lending norms, provisioning standards | Continued emphasis on robust capital buffers |

| Interbank Market/Financial Institutions | Moderate | Liquidity provision, specialized services, cost of funds | Dynamic environment due to interest rate shifts |

What is included in the product

Tailored exclusively for South Indian Bank, this analysis dissects the intensity of rivalry, buyer and supplier power, the threat of new entrants and substitutes, providing strategic insights into its competitive environment.

A visual representation of competitive intensity—helping to pinpoint where South Indian Bank can build sustainable advantage.

Customers Bargaining Power

High Customer Choice and Low Switching Costs

Customers in India's banking landscape enjoy a wealth of choices, ranging from established public and private sector banks to foreign institutions, specialized small finance banks, and emerging payment banks. This diverse ecosystem is further enriched by a growing number of fintech companies offering innovative financial solutions.

The digital transformation sweeping through the banking sector significantly reduces the effort and expense associated with switching providers. As more services become accessible online and through mobile apps, customers can easily compare offerings and move their business to institutions that provide more favorable terms, better interest rates, or a superior user experience, thereby amplifying their bargaining power.

Price Sensitivity to Interest Rates and Fees

Customers' sensitivity to interest rates on loans and deposits, along with various banking fees, significantly impacts their choices. For instance, during 2024, many banks adjusted their deposit rates in response to evolving monetary policy, directly influencing customer decisions on where to park their savings. This price sensitivity means banks like South Indian Bank must remain competitive to retain their customer base.

In a market with numerous banking options, South Indian Bank faces pressure to offer attractive interest rates and clear, reasonable fee structures. Failing to do so can lead customers to switch to competitors. This dynamic limits the bank's power to unilaterally hike charges or reduce customer benefits, as it could result in a loss of business, especially for retail and small business segments that are more rate-sensitive.

Increasing Digital Literacy and Access to Information

As digital literacy surges across India, with smartphone penetration reaching approximately 70% by early 2024 and internet access expanding rapidly, bank customers are better equipped than ever to research and compare financial products. This heightened awareness allows them to easily identify and switch to competitors offering more favorable terms or lower fees, significantly amplifying their bargaining power.

Availability of Alternative Financial Service Providers

The increasing presence of Non-Banking Financial Companies (NBFCs) and burgeoning fintech startups significantly amplifies customer bargaining power. These entities offer specialized, agile alternatives for services like instant credit, digital transactions, and investment management, directly challenging traditional banks. For instance, by mid-2024, India's fintech sector saw a surge, with digital payment volumes alone crossing 10 billion transactions monthly, providing consumers with a wider array of choices and greater leverage.

This proliferation of financial service providers means customers are no longer solely reliant on established banks. They can readily switch to providers offering better rates, more convenient digital interfaces, or tailored products. This competitive landscape forces traditional institutions like South Indian Bank to innovate and improve their offerings to retain customers, thereby increasing the bargaining power of the customer base.

- Increased Competition: NBFCs and fintech firms offer specialized services, fragmenting the market and giving customers more options.

- Digital Transformation: Fintech advancements provide easier access to alternative financial solutions, empowering customers.

- Customer Choice: A broader range of providers means customers can seek out the best terms and services for their specific needs.

- Rate Sensitivity: Customers are more likely to switch providers for better interest rates or lower fees, driven by the availability of alternatives.

Customer Demand for Personalized and Seamless Experiences

Customers today demand hyper-personalized services and seamless digital interactions. This means banks must offer tailored products and easy-to-use online platforms. Failure to adapt can lead to customer attrition, as seen in the growing market share of fintechs that excel in these areas.

South Indian Bank, like its peers, faces pressure to invest in customer-centric innovations to retain its client base. In 2023, digital transactions through South Indian Bank's mobile banking platform saw a significant increase, reflecting this shift in customer preference. This ongoing trend necessitates continuous upgrades to digital infrastructure and service offerings.

- Customer Expectations: Modern consumers expect financial institutions to understand their individual needs and provide integrated, easy-to-access services across all channels.

- Digital Dominance: The increasing reliance on mobile and online platforms means that a poor digital experience can quickly drive customers to competitors.

- Fintech Competition: Agile fintech companies often lead the way in offering personalized and seamless experiences, posing a direct challenge to traditional banks.

- Investment Imperative: Banks must allocate resources towards technology and data analytics to meet these evolving customer demands and maintain competitiveness.

Customer Power Reshapes India's Banking Landscape

The bargaining power of customers in India's banking sector is substantial, driven by intense competition and rapid digital transformation. Customers have access to a wide array of choices, from traditional banks to agile fintechs and NBFCs, making it easier than ever to switch providers for better rates or services. This environment compels banks like South Indian Bank to remain competitive and customer-centric.

| Factor | Impact on South Indian Bank | Supporting Data (2023-2024) |

|---|---|---|

| Increased Competition | Limits pricing power, necessitates competitive offerings. | India's fintech sector saw over 10 billion digital payment transactions monthly by mid-2024. |

| Digital Transformation | Reduces switching costs, amplifies customer ability to compare. | Smartphone penetration reached ~70% by early 2024, facilitating easy access to online banking. |

| Customer Expectations | Demand for personalization and seamless digital experiences. | South Indian Bank's digital transactions increased significantly in 2023, reflecting customer preference. |

| Rate Sensitivity | Customers readily switch for better interest rates or lower fees. | Banks adjusted deposit rates in 2024 due to monetary policy changes, directly influencing customer decisions. |

Preview the Actual Deliverable

South Indian Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. This comprehensive Porter's Five Forces analysis delves into the competitive landscape of South Indian Bank, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector. Understand the strategic implications for South Indian Bank's market position and future growth.