SpaceX SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

SpaceX’s relentless innovation and launch cadence have redefined aerospace economics, but regulatory scrutiny, supply-chain pressures, and rising competition pose real strategic risks; our full SWOT unpacks these dynamics with operational detail and market context. Discover the complete picture behind the company’s market position with our full SWOT analysis—purchase the full report for a professionally formatted, editable Word and Excel package to power investment, strategy, or pitch decisions.

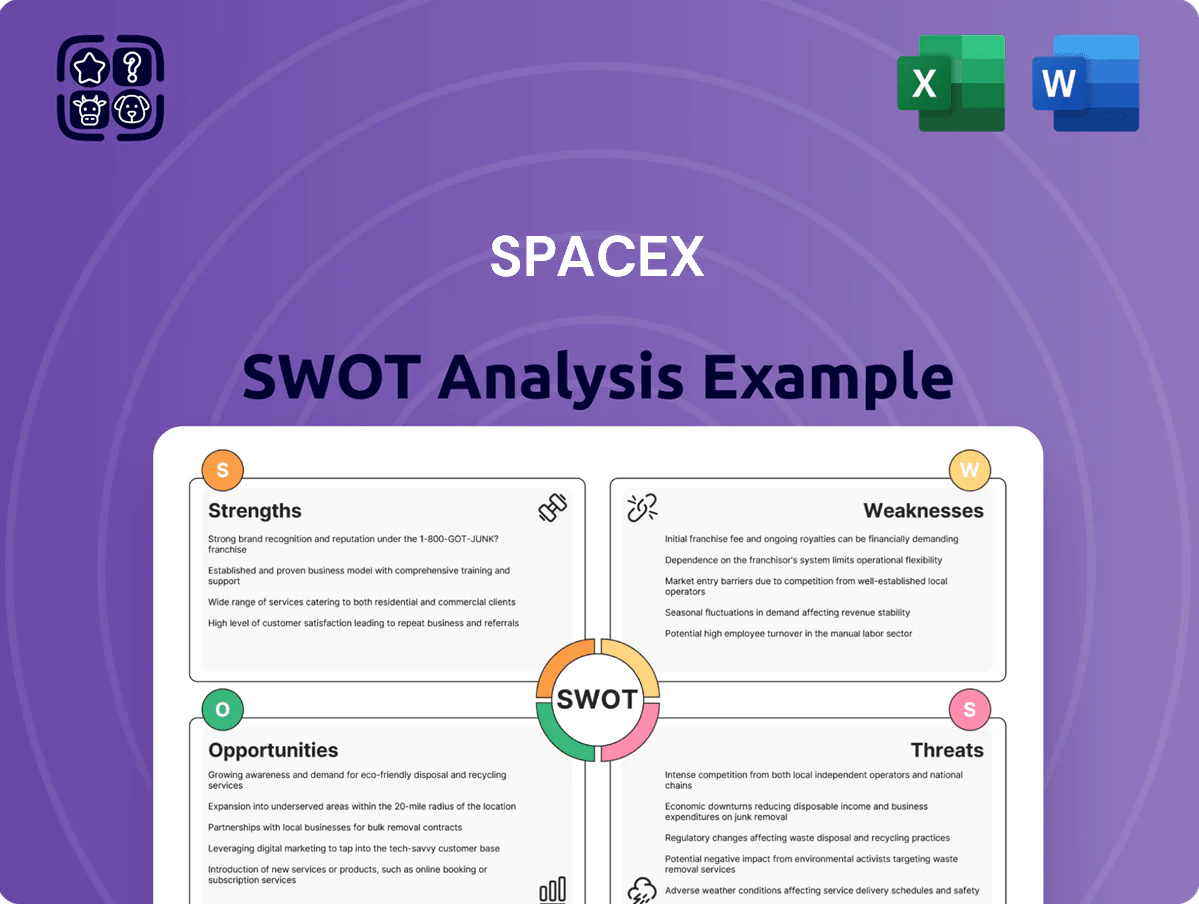

Strengths

Market Dominance in Launch Services

As of late 2025, SpaceX controls roughly 60–70% of global commercial launch market share, driven by 2025 launch cadence of ~130 orbital missions (Falcon 9/Heavy) versus ~90 for all rivals combined; this scale cuts cost-per-launch and yields gross margins above peers in commercial launches.

Unmatched Reusability Capabilities

SpaceX remains the only company consistently recovering and refurbishing orbital-class boosters, cutting cost per kg to LEO—estimates suggest reuse lowered Falcon 9 marginal launch cost to about $20–30/kg versus $100+/kg for expendable models in 2025. By late 2025 SpaceX logged boosters with 20+ flights, proving hardware maturity rivals like Blue Origin and Arianespace have not matched. That reuse moat boosts gross margins and lets SpaceX underprice competitors while staying profitable.

Starlink Revenue Generation

By end-2025 Starlink had converted from capital drain to primary revenue engine with an estimated 3.4 million active subscribers, generating roughly $2.8–3.2 billion in annualized revenue and positive free cash flow in late 2025.

Vertical integration drives steady internal demand: SpaceX books hundreds of Starlink-dedicated launches a year, lowering unit launch cost and securing revenue for Starship development.

Service expansion into maritime, aviation, and rural residential added diversified ARPU streams—maritime/aviation premium plans and rural broadband reduced dependency on launch contracts.

Vertical Integration and Manufacturing

SpaceX vertically integrates most production—from Merlin and Raptor engines to Starlink satellites and ground stations—cutting vendor reliance and lowering supply-chain disruption risk; in 2024 SpaceX produced ~3,000 Starlink sats and ramped Raptor output to support 202+ launches backlog.

This in-house manufacturing speeds iterative design cycles, driving cost-per-launch declines (Falcon 9 reuse cut marginal cost ~40% vs expendable peers) and faster tech updates than legacy OEMs.

- Controls engines, structures, avionics, sats

- ~3,000 Starlink sats built in 2024

- Raptor scale supports 200+ launch backlog

- Reusability cut marginal launch cost ~40%

Strategic Government Partnerships

SpaceX is a core partner to NASA and the Department of Defense, securing multi-billion dollar contracts such as the $2.9B NASA Human Landing System award (2021) and repeated National Security Space Launch (NSSL) missions, giving revenue visibility into the late 2020s.

Delivering crewed and classified launches has built institutional trust and operational pedigree, cementing SpaceX as essential to US space infrastructure and lowering political and program risk.

- $2.9B HLS award

- Multiple NSSL missions through 2029

- Revenue visibility and institutional trust

SpaceX: Launching 130 Missions, 60–70% Market Share, Starlink $3B+ FCF Turnaround

SpaceX dominates commercial launches (60–70% share) with ~130 orbital missions in 2025; reuse cuts Falcon 9 marginal cost to ~$20–30/kg vs $100+/kg for expendables. Starlink reached ~3.4M subs and ~$3.0B annualized revenue in late 2025, turning positive FCF. Vertical integration produced ~3,000 Starlink sats in 2024 and supports a 200+ Starship/launch backlog; strong NASA/DoD awards (e.g., $2.9B HLS) add revenue visibility.

| Metric | Value |

|---|---|

| 2025 launch cadence | ~130 missions |

| Commercial market share | 60–70% |

| Falcon 9 marginal cost to LEO | $20–30/kg |

| Starlink subscribers (late 2025) | ~3.4M |

| Starlink revenue (annualized) | $2.8–3.2B |

| Starlink sats built (2024) | ~3,000 |

| Launch/backlog support | 200+ launches |

| Key government award | $2.9B HLS (2021) |

What is included in the product

Provides a concise SWOT overview of SpaceX, highlighting its technological leadership and cost advantages, internal limitations and scaling challenges, external growth opportunities in commercial and government space markets, and competitive, regulatory, and operational threats shaping its strategic trajectory.

Delivers a concise SpaceX SWOT snapshot for rapid strategic alignment and stakeholder briefings, enabling quick edits to reflect launch cadence, regulatory shifts, or competitive moves.

Weaknesses

Extreme Capital Intensity

The Starship program and Starlink expansion demand billions yearly: SpaceX disclosed >$3.5B capex in 2024-related disclosures and Starlink hardware+launch costs run ~$2–3B/year; such extreme capital intensity means schedule slips (Starship first orbital attempts delayed Jan–Apr 2025) quickly strain liquidity. SpaceX must keep raising private rounds or reach projected Starlink EBITDA of tens of billions to fund Mars ambitions, so financing risk remains high.

Concentrated Leadership Risk

SpaceX’s strategy and public image remain tightly linked to founder Elon Musk, who led Tesla, X, and Neuralink in 2025, risking distraction; Musk’s 2024 SEC settlement and 2025 public controversies reduced some investor confidence in related firms.

Centralized decision-making speeds iteration but creates a single point of failure: a leadership shift or scandal could dent hiring—SpaceX employed ~13,000 people in 2024—and hurt contracts and valuations.

Regulatory and Compliance Bottlenecks

SpaceX often faces delays from slow FAA launch licensing and environmental reviews at Starbase, Texas; FAA issued 24 significant actions on Starbase between 2020–2024, slowing cadence. As launches aim for 100+ Falcon and Starship flights annually, regulatory friction grows between SpaceX’s rapid cycle and rigid rules. These bottlenecks can stall missions, raise per-launch costs, and let international rivals narrow SpaceX’s lead.

Starship Development Complexity

- 15 test flights by 2025; limited rapid reuse proof

- Targets: 100–150 hr turnaround, 100+ t LEO

- Key tech gaps: heatshield fatigue, orbital refuel

- Failure risk: months-long grounding, Artemis IV delay

Environmental and Local Impact

Frequent heavy‑lift launches create noise, debris, and land‑use strain, sparking disputes with environmental groups and local communities near Boca Chica (Texas) and Vandenberg (California); FAA reported 61 Falcon/Starship licensed launches in 2024‑25 increased local complaints by ~35% vs 2022.

Legal challenges over ecosystem harm have forced restricted windows and mitigation costs—example: SpaceX agreed to $50–75 million in habitat mitigation and monitoring near Boca Chica in 2024, raising per‑launch operating overheads.

Managing social and environmental responsibilities demands growing admin and legal resources; SpaceX disclosed $120+ million in environmental compliance and legal provisions in its 2024 filings, pressuring margins as cadence scales.

- 35% rise in local complaints (2024 vs 2022)

- $50–75M Boca Chica mitigation (2024)

- $120M+ environmental/legal provisions (2024)

High capex, Starlink burn, founder risk and technical gaps threaten liquidity

High capex and cash burn: >$3.5B capex (2024) plus $2–3B/yr Starlink costs strains liquidity and forces fundraising. Founder risk: Elon Musk distractions and 2024–25 controversies centralize reputational exposure. Technical gaps: only 15 Starship tests by 2025, heatshield and orbital refuel unproven for 100+ t reuse. Regulatory and environmental costs raised operating overheads ($50–75M mitigation; $120M+ compliance in 2024).

| Metric | 2024–25 |

|---|---|

| Capex disclosed | $3.5B+ |

| Starlink annual cost | $2–3B |

| Starship tests | 15 |

| Mitigation cost | $50–75M |

| Env/legal provisions | $120M+ |

Full Version Awaits

SpaceX SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

SpaceX’s relentless innovation and launch cadence have redefined aerospace economics, but regulatory scrutiny, supply-chain pressures, and rising competition pose real strategic risks; our full SWOT unpacks these dynamics with operational detail and market context. Discover the complete picture behind the company’s market position with our full SWOT analysis—purchase the full report for a professionally formatted, editable Word and Excel package to power investment, strategy, or pitch decisions.

Strengths

Market Dominance in Launch Services

As of late 2025, SpaceX controls roughly 60–70% of global commercial launch market share, driven by 2025 launch cadence of ~130 orbital missions (Falcon 9/Heavy) versus ~90 for all rivals combined; this scale cuts cost-per-launch and yields gross margins above peers in commercial launches.

Unmatched Reusability Capabilities

SpaceX remains the only company consistently recovering and refurbishing orbital-class boosters, cutting cost per kg to LEO—estimates suggest reuse lowered Falcon 9 marginal launch cost to about $20–30/kg versus $100+/kg for expendable models in 2025. By late 2025 SpaceX logged boosters with 20+ flights, proving hardware maturity rivals like Blue Origin and Arianespace have not matched. That reuse moat boosts gross margins and lets SpaceX underprice competitors while staying profitable.

Starlink Revenue Generation

By end-2025 Starlink had converted from capital drain to primary revenue engine with an estimated 3.4 million active subscribers, generating roughly $2.8–3.2 billion in annualized revenue and positive free cash flow in late 2025.

Vertical integration drives steady internal demand: SpaceX books hundreds of Starlink-dedicated launches a year, lowering unit launch cost and securing revenue for Starship development.

Service expansion into maritime, aviation, and rural residential added diversified ARPU streams—maritime/aviation premium plans and rural broadband reduced dependency on launch contracts.

Vertical Integration and Manufacturing

SpaceX vertically integrates most production—from Merlin and Raptor engines to Starlink satellites and ground stations—cutting vendor reliance and lowering supply-chain disruption risk; in 2024 SpaceX produced ~3,000 Starlink sats and ramped Raptor output to support 202+ launches backlog.

This in-house manufacturing speeds iterative design cycles, driving cost-per-launch declines (Falcon 9 reuse cut marginal cost ~40% vs expendable peers) and faster tech updates than legacy OEMs.

- Controls engines, structures, avionics, sats

- ~3,000 Starlink sats built in 2024

- Raptor scale supports 200+ launch backlog

- Reusability cut marginal launch cost ~40%

Strategic Government Partnerships

SpaceX is a core partner to NASA and the Department of Defense, securing multi-billion dollar contracts such as the $2.9B NASA Human Landing System award (2021) and repeated National Security Space Launch (NSSL) missions, giving revenue visibility into the late 2020s.

Delivering crewed and classified launches has built institutional trust and operational pedigree, cementing SpaceX as essential to US space infrastructure and lowering political and program risk.

- $2.9B HLS award

- Multiple NSSL missions through 2029

- Revenue visibility and institutional trust

SpaceX: Launching 130 Missions, 60–70% Market Share, Starlink $3B+ FCF Turnaround

SpaceX dominates commercial launches (60–70% share) with ~130 orbital missions in 2025; reuse cuts Falcon 9 marginal cost to ~$20–30/kg vs $100+/kg for expendables. Starlink reached ~3.4M subs and ~$3.0B annualized revenue in late 2025, turning positive FCF. Vertical integration produced ~3,000 Starlink sats in 2024 and supports a 200+ Starship/launch backlog; strong NASA/DoD awards (e.g., $2.9B HLS) add revenue visibility.

| Metric | Value |

|---|---|

| 2025 launch cadence | ~130 missions |

| Commercial market share | 60–70% |

| Falcon 9 marginal cost to LEO | $20–30/kg |

| Starlink subscribers (late 2025) | ~3.4M |

| Starlink revenue (annualized) | $2.8–3.2B |

| Starlink sats built (2024) | ~3,000 |

| Launch/backlog support | 200+ launches |

| Key government award | $2.9B HLS (2021) |

What is included in the product

Provides a concise SWOT overview of SpaceX, highlighting its technological leadership and cost advantages, internal limitations and scaling challenges, external growth opportunities in commercial and government space markets, and competitive, regulatory, and operational threats shaping its strategic trajectory.

Delivers a concise SpaceX SWOT snapshot for rapid strategic alignment and stakeholder briefings, enabling quick edits to reflect launch cadence, regulatory shifts, or competitive moves.

Weaknesses

Extreme Capital Intensity

The Starship program and Starlink expansion demand billions yearly: SpaceX disclosed >$3.5B capex in 2024-related disclosures and Starlink hardware+launch costs run ~$2–3B/year; such extreme capital intensity means schedule slips (Starship first orbital attempts delayed Jan–Apr 2025) quickly strain liquidity. SpaceX must keep raising private rounds or reach projected Starlink EBITDA of tens of billions to fund Mars ambitions, so financing risk remains high.

Concentrated Leadership Risk

SpaceX’s strategy and public image remain tightly linked to founder Elon Musk, who led Tesla, X, and Neuralink in 2025, risking distraction; Musk’s 2024 SEC settlement and 2025 public controversies reduced some investor confidence in related firms.

Centralized decision-making speeds iteration but creates a single point of failure: a leadership shift or scandal could dent hiring—SpaceX employed ~13,000 people in 2024—and hurt contracts and valuations.

Regulatory and Compliance Bottlenecks

SpaceX often faces delays from slow FAA launch licensing and environmental reviews at Starbase, Texas; FAA issued 24 significant actions on Starbase between 2020–2024, slowing cadence. As launches aim for 100+ Falcon and Starship flights annually, regulatory friction grows between SpaceX’s rapid cycle and rigid rules. These bottlenecks can stall missions, raise per-launch costs, and let international rivals narrow SpaceX’s lead.

Starship Development Complexity

- 15 test flights by 2025; limited rapid reuse proof

- Targets: 100–150 hr turnaround, 100+ t LEO

- Key tech gaps: heatshield fatigue, orbital refuel

- Failure risk: months-long grounding, Artemis IV delay

Environmental and Local Impact

Frequent heavy‑lift launches create noise, debris, and land‑use strain, sparking disputes with environmental groups and local communities near Boca Chica (Texas) and Vandenberg (California); FAA reported 61 Falcon/Starship licensed launches in 2024‑25 increased local complaints by ~35% vs 2022.

Legal challenges over ecosystem harm have forced restricted windows and mitigation costs—example: SpaceX agreed to $50–75 million in habitat mitigation and monitoring near Boca Chica in 2024, raising per‑launch operating overheads.

Managing social and environmental responsibilities demands growing admin and legal resources; SpaceX disclosed $120+ million in environmental compliance and legal provisions in its 2024 filings, pressuring margins as cadence scales.

- 35% rise in local complaints (2024 vs 2022)

- $50–75M Boca Chica mitigation (2024)

- $120M+ environmental/legal provisions (2024)

High capex, Starlink burn, founder risk and technical gaps threaten liquidity

High capex and cash burn: >$3.5B capex (2024) plus $2–3B/yr Starlink costs strains liquidity and forces fundraising. Founder risk: Elon Musk distractions and 2024–25 controversies centralize reputational exposure. Technical gaps: only 15 Starship tests by 2025, heatshield and orbital refuel unproven for 100+ t reuse. Regulatory and environmental costs raised operating overheads ($50–75M mitigation; $120M+ compliance in 2024).

| Metric | 2024–25 |

|---|---|

| Capex disclosed | $3.5B+ |

| Starlink annual cost | $2–3B |

| Starship tests | 15 |

| Mitigation cost | $50–75M |

| Env/legal provisions | $120M+ |

Full Version Awaits

SpaceX SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.